M. Suhail/iStock Editorial via Getty Images

Investment Thesis

Bed Bath & Beyond (NASDAQ:BBBY) is about to report its Q3 2022 results next Tuesday, pre-market.

When the last quarter’s results came out I wrote an article titled, All the Direction Your Need, where I concluded it by saying:

I want to root for this underdog. I would love to see this stock receive a short squeeze that rockets it to outer space. But I don’t believe that’s a realistic sustainable event. Not a rocket ship. Just a rock.

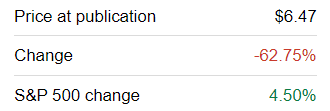

Since I wrote that Bed Bath is comparable to a rock, the stock is down +60% in about 3 months.

BBBY author’s work

Now, as we look ahead to Q3 2022, I am forced to question, how long until BBBY returns to $6.47? Or better said, will $6.47 ever return to be on the cards?

BBBY’s outlook is simply too uncertain. I urge readers to avoid getting involved in this stock.

Let’s Think Through Q3 2022

We are facing an economic contraction. And the dynamics afoot this Q3 2022 are strikingly different from the prior quarter in 2021.

Back in Q3 2021, the company’s prospects were not strong. But I believe we could acquiesce and agree that the prospects were fair.

However, I strongly believe that the same won’t be said about this holiday season just past.

And then, to further complicate the bull case even further, the market is always looking ahead by at least 6 months. And as we look ahead over the next few quarters, households are facing a squeeze between a cost of living crisis and high inflation.

So, with this in mind, here are 3 reasons why investors should avoid this name.

Top 3 Reasons to Avoid BBBY

In the first case, this is not an environment that’s conducive to discretionary spending. And then, to really add the nail in the coffin, let’s think of the main demand for BBBY’s products. BBBY thrives when the housing market is strong.

Yet, as we know the housing market is in turmoil. The housing market right now has seized up. And if households are not moving much, that means that their appetite to refurbish and upgrade their properties will be muted. At least compared with the prior year.

The second reason is a has two parts. Since BBBY is unprofitable and has been unprofitable since fiscal 2019, that means that its merchandise suppliers will be highly anxious about not getting paid. That could mean that suppliers will require payment upon delivery.

Needless to say, since BBBY already has poor liquidity, any further requirements on its capital could be deathly for BBBY.

This leads me to my third reason. I estimate that when BBBY reports its Q3 2022 results it will show on its balance sheet more than $1.6 billion of net debt.

So, not only is BBBY attempting to refinance its debt which may not be successful. But it’s attempting to refinance its debt at significantly higher coupon rates.

And not only higher coupon rates. But attempting to sweeten the deal to creditors by bringing forward their maturities. And even then, the uptake of this offer by debt holders is relatively small.

BBBY SEC filing, Exchange Offer

The debt holders don’t want to tender their notes for convertible notes. They want to avoid BBBY’s equity.

BBBY Stock Valuation – Cheap Can Always Become Cheaper

On the surface, BBBY’s market cap is $210 million. For a company with annual sales of more than $5 billion, this might seem like a terrific bargain. But I can assure readers that it’s not.

What’s more, we know that BBBY finished Q2 2022 with approximately 80.3 million shares outstanding. However, since that report came out, as of December 19, 2022, BBBY had a total of approximately 117.3 million shares outstanding.

That means that BBBY’s market cap has now increased to $280 million, simply through its share dilution in the past quarter.

However one appraises this investment, it might seem cheap on the surface, but cheap can always become cheaper.

Risk Factor to the Bear Case

Anyone interested in BBBY knows that it has a very high short ratio. That means that it’s a crowded short stock.

Accordingly, if for whatever reason BBBY’s Q3 2022 results are perceived to be better than expected, that would lead to a short squeeze.

Therefore, anyone short this name is carrying a lot of risk, as a short squeeze is possible.

The Bottom Line

A few days before Christmas, Ben Rosenzweig, an independent director, resigned. Recall, Rosenzweig, took his seat when the agreement with Ryan Cohen took place to attempt to unlock shareholder value.

I believe that BBBY shareholders would do well to take a cue from Rosenzweig and call it a day here.

Be the first to comment