thexfilephoto

Over recent quarters, midstream has made significant progress in rebuilding a track record of growing payouts. Names that cut their dividends during the energy market volatility and pandemic-related uncertainty of 2020 have largely returned to growth. More companies maintained their payouts or continued to grow through 2020, but their consistency may have been underappreciated. Today’s note recaps 2Q22 dividends for Alerian MLP and midstream benchmark indexes and discusses the positive outlook for midstream payouts.

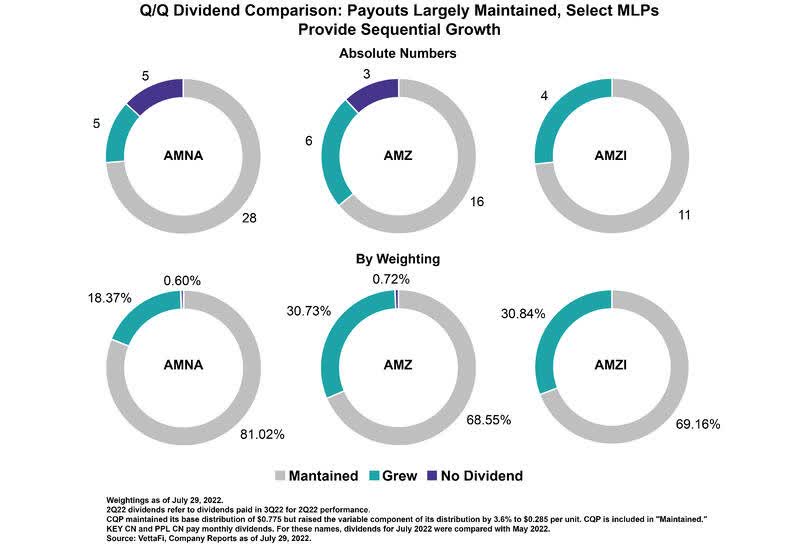

2Q22 Dividends: Most maintain in fourth straight cut-free quarter for midstream.

Midstream companies continued to build on their track record of positive dividend trends with their latest payouts. For the fourth straight quarter, there were no dividend cuts across the Alerian energy infrastructure index suite. The majority of names maintained their payouts sequentially, as increases tend to be biased to 4Q and 1Q payouts, but there were still notable examples of growth concentrated among MLPs.

Energy Transfer (ET) increased its quarterly distribution by 15.0% to $0.23 per unit, making progress towards its target of restoring the payout to $0.305 per unit. DCP Midstream (DCP) became the latest name to increase its distribution for the first time since cutting in 2020, announcing a 10.3% increase consistent with prior management commentary. Other examples of growth include Enterprise Products Partners’ (EPD) 2.2% increase, Hess Midstream’s (HESM) 1.2% increase, Green Plains’ (GPP) 1.1% increase, and Delek Logistics’ (DKL) 0.5% increase.

The pie charts below show the quarter-over-quarter changes to dividends for the Alerian Midstream Energy Index (AMNA), Alerian MLP Index (AMZ), and Alerian MLP Infrastructure Index (AMZI) by comparing 2Q22 with 1Q22. To be clear, 2Q22 dividends refer to the dividends paid in 3Q22 as a result of operational performance in 2Q22.

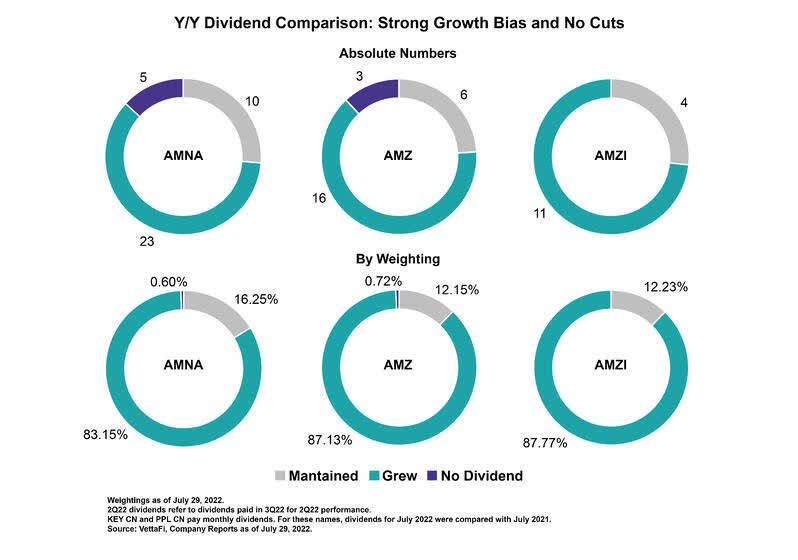

Year-over-year comparison highlights strong growth bias.

Looking at 2Q22 dividends relative to 2Q21 shows a strong tilt towards growth, with more than 80% of each index by weighting having increased its payout on a year-over-year basis. Importantly, there are no cuts. The last midstream distribution cut came from Shell Midstream Partners (SHLX) in July 2021. Combining the strong year-over-year growth with four consecutive cut-free quarters, the momentum for midstream dividends is as strong as it has been in years – certainly the best it has been since 2014 when oil prices started to fall due to oversupply.

Outlook for dividend growth remains constructive.

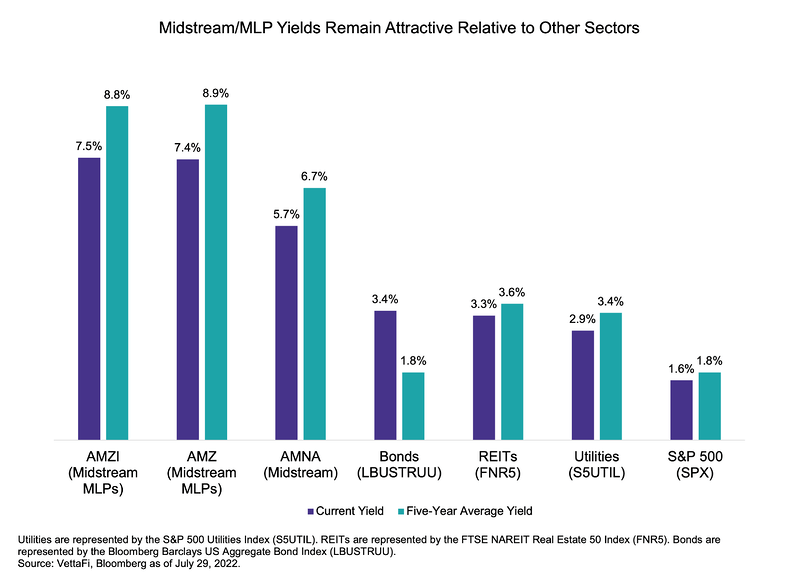

As shown in the chart below, MLP and midstream yields remain compelling relative to other investments, even as bond yields have increased. Energy infrastructure companies are well positioned to continue moderately growing their payouts as they generate significant free cash flow (read more). Beyond income, equity repurchases are adding to the total return potential of the midstream space. Relative to the other income investments below, midstream is clearly differentiated by its more generous yield – as has long been the case. However, the improving dividend track record and tailwinds provided by excess cash flow generation are newer developments that add confidence to the income opportunity and strengthen the fundamental investment case.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMZ is the underlying index for the JPMorgan Alerian MLP Index ETN (AMJ) and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA).

© Alerian 2022. All rights reserved. This material is reproduced with the prior consent of Alerian. It is provided as general information only and should not be taken as investment advice. Employees of Alerian are prohibited from owning individual MLPs. For more information on Alerian and to see our full disclaimer, visit Disclaimers | Alerian.

Be the first to comment