JamesBrey

As we write this, the stock market remains volatile and directionless. The most recent downside pressure was caused by the renewed worries about interest rate hikes by the Fed and its general hawkishness. The Fed has indicated that it is committed to bringing down inflation, and it will do whatever it takes. However, there are serious concerns that in doing so, the fed may cause a recession, and possibly a deeper one.

Even though most investors have become accustomed to a constant cycle of boom-and-bust events, wouldn’t it be nice if there was less stress on a day-to-day basis? With the backdrop of the current state of the stock market, a great many folks would want an investment strategy that could avoid the roller-coaster ride of the stock market, works largely on auto-pilot, and is relatively stress-free. In addition, we would want our strategy to deliver high income and a decent long-term growth of over 10%, beating inflation and building wealth over time.

Being financially independent is not just for retirees. Sure, it is sort of a prerequisite for them, but it could be a great stress reducer for folks who are much younger and maybe several years away from retirement. At the same time, being financially independent does not necessarily mean F.I.R.E. (Financially Independent, Retire Early). However, it could be if that was your goal. For many folks, it could mean pursuing their chosen work/career without worrying about the next layoffs or the next downturn. Being financially independent just means that it affords you the choice of living life on your terms. You may still like to work for many more years and consolidate your gains and secure a wealthy retirement.

In simple or layman’s terms, being financially independent means that your passive investments generate (or can generate) enough income on a regular basis so as to meet your “basic” living expenses. Please note the emphasis is on basic living expenses and not all your desires and wants. Obviously, the surest way to achieve financial freedom is by saving more and investing wisely for the long term. It is also important to be able to distinguish between the “needs” and “wants” in your life and reduce unnecessary spending, thus lowering your basic living expenses. However, this is something that is very personal and can vary greatly from one person to another.

Whether you are a retiree or you just want to be financially independent, you need a strategy that should meet the following goals:

- Produce sufficiently high income to meet basic needs;

- Preserve capital in bad times (relatively speaking);

- Provide reasonably high growth for long-term wealth preservation.

Note: In our view, the strategies presented in this article are highly relevant in the current market environment. Our regular readers who like these strategies should benefit from some new ideas and updated information. Further, we think new readers would possibly benefit greatly from these ideas. Thanks for reading.

Income

It is not easy to define “sufficiently high income” since this is more of a subjective term, and it depends upon the size of your assets, your lifestyle, and basic living expenses. Obviously, different people have different needs. If you could lower your expenses, your need for income also gets reduced accordingly.

Percentage Yield required = 100 * (Yearly Expenses / Size of Assets)

In the above formula, retirees getting social security, pension, or any other fixed income should reduce their yearly expenses by the amount of such fixed income.

For example, a retiree couple, who needs $90,000 a year to meet their expenses, gets $55,000 in social security/pension income and has $750,000 in retirement savings. So, the yield requirement would be:

Percentage Yield required = 100 * ((90,000 – 55,000) / 750,000)

= 4.67%

It’s our belief that any portfolio that claims to (or aims to) produce more than 8% income would at least have some risk of depleting the capital unless you reinvest the income. It would certainly be very difficult to grow such a portfolio if the entire income is withdrawn. So, for these reasons, we would put the red line at 6%. Sure, your portfolio could be generating more than 8%, but any excess income over 6% should be reinvested back into the portfolio for it to prosper in the long term. Sure, if your asset size is large enough and income needs are smaller than 6%, you should reinvest the maximum possible back into the portfolio.

Capital Preservation

There’s almost no financial investment that can preserve the capital 100% of the time or in all kinds of situations. Even the value of cash is subject to inflation and currency fluctuations over time, especially now when inflation is running at a 40-year high. It’s a given fact that your investments (other than cash) will have some level of volatility – obviously, the lower, the better. The real test of capital preservation becomes apparent during times of high stress, something akin to what we saw in the year 2020 or during the 2008 financial crisis. Even the current market environment, with the S&P500 skirting back and forth near the edge of a bear market, would test many portfolios. An event or correction like this can act as a real eye-opener to review and judge if your portfolio is meeting its defined goals, especially risk tolerance. So, we recommend that every investor should have a fairly good idea of his/her tolerance for volatility and drawdowns.

Preservation of capital (at least on a relative basis) is important at any age, but it is of critical importance for retirees and older investors. So, our portfolio should be able to achieve much lower volatility and smaller drawdowns than the broader indexes while not compromising on growth during good times.

Reasonable Growth

It’s certainly debatable as to how much growth is reasonable. One size does not fit all. It can vary based on your personal expectations and factors like the rate of inflation and interest rates. But assuming an average of 3% rate of long-term inflation, in our view, a 9%-10% overall annual growth of the capital (including the income withdrawals) would be very reasonable. However, more recently, inflation has been running at a much higher clip, which is making life difficult for savers.

Financial Independence

We have already discussed the concept of financial independence in our introductory section. As we stated earlier, you could be in your 40s and still be financially independent. You could be pursuing a great career, whatever that may be, and still, be financially independent. Just like many things in life, the meaning of this term could vary from person to person. However, the way we see it is all about sustainable income on a regular and consistent basis, even if you have no need for that income today. So, your investment portfolio should be able to safely generate enough income to sustain your basic needs (not including luxuries or vacations, etc.) if any need arises.

Investment Strategy

In this article, we present a multi-basket strategy that attempts to meet most of the above goals. As such, besides growth, we focus on income-producing strategies that also preserve capital during times of crisis.

We will review our multi-basket strategy that’s not overly complicated and easy to get started. Moreover, we should be able to leave the majority of our portfolio on the auto-pilot. This is especially important for folks who are busy in their day jobs and can not spare much time on a day-to-day basis. We will provide as many as five sub-strategies (or buckets), but as an individual, you could just do fine by picking and mixing up to three sub-strategies. We also will provide some backtesting examples for each sub-strategy and how they would have behaved during the 2020 crisis or during the 2008-09 financial crisis.

Please note that we manage most of these strategies/portfolios in our Marketplace service that has live performance records at least since 2018 and for some limited portfolios since 2014.

Brief Description of Multi-Basket Strategy

Here we will discuss a multi-basket strategy, with each sub-strategy being unique in terms of income, growth goals, and risk levels. One of the buckets is specifically designed to provide the hedging mechanism to bring lower volatility and lower drawdowns to the overall portfolio. At the basic level, the strategy requires three baskets with an overall yield greater than 5%. For investors who may not need a high income (yield requirement less than 3.5%), they could just invest in two buckets.

Below we will provide several investment buckets for consideration, along with their performance overviews. Depending upon your personal situation, you can pick and choose various baskets and assign them the allocation percentages.

DGI Basket 1: (With Individual Stocks)

Allocation: 35-50%

We believe that a diversified DGI (Dividend Growth Investing) portfolio should hold roughly 15-25 stocks. We like to invest in individual stocks, and that’s what we are going to focus on in this bucket. The best part of owning individual stocks is that once you have acquired the position, there are no ongoing fees or expenses.

For our sample portfolio presented below, we will look for companies that are large-cap, blue-chip, relatively safe, and have solid dividend records. For our list below, we will try to select stocks that are likely to provide a high level of resistance to downward pressure in an outright panic situation.

We must put emphasis on diversifying among various sectors and industry segments of the economy. A selection of roughly 15-25 stocks could provide more than enough diversification. We will present 20 such stocks based on our past research, current dividend payouts, and a high level of dividend safety.

For this part of the portfolio, our focus is to select the majority of stocks that tend to do well in both good times and during recessions/corrections. Please note that this is just a list for demonstration purposes, and there can be many other stocks that could be equally qualified.

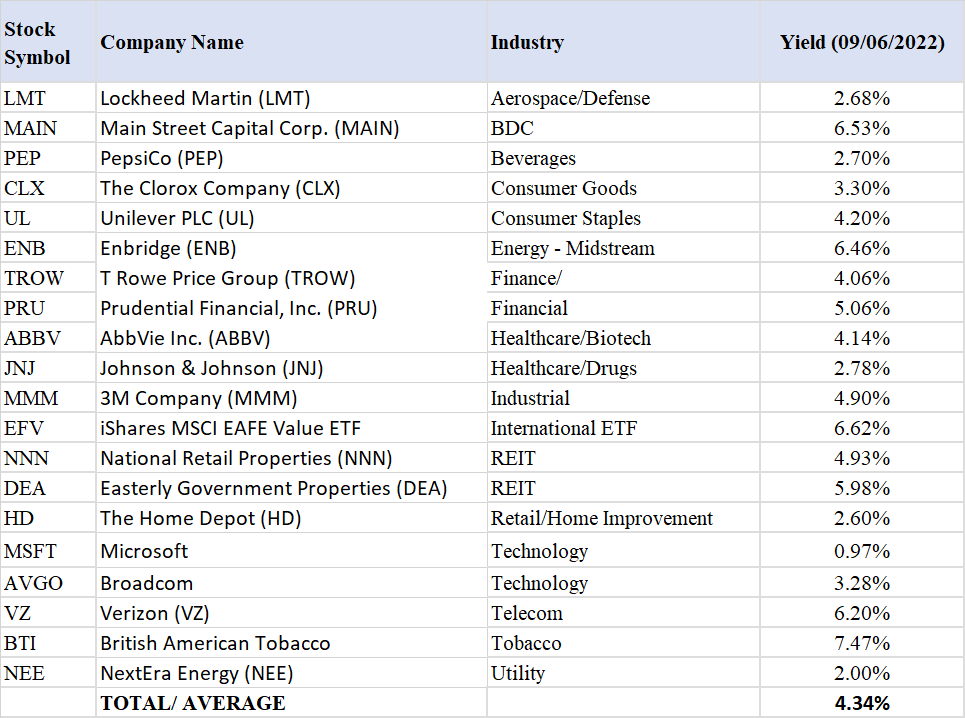

Stocks selected:

(LMT), (MAIN), (PEP), (CLX), (UL), (ENB), (TROW), (PRU), (ABBV), (JNJ), (MMM), (EFV), (NNN), (DEA), (HD), (MSFT), (AVGO), (VZ), (BTI), (NEE)

Table-1:

Author

The average yield from this group of 20 stocks is very respectable at 4.34% compared to 1.50% from S&P 500. If you still have some years before retirement, reinvesting the dividends for a few years would take the yield on cost up to 5% easily.

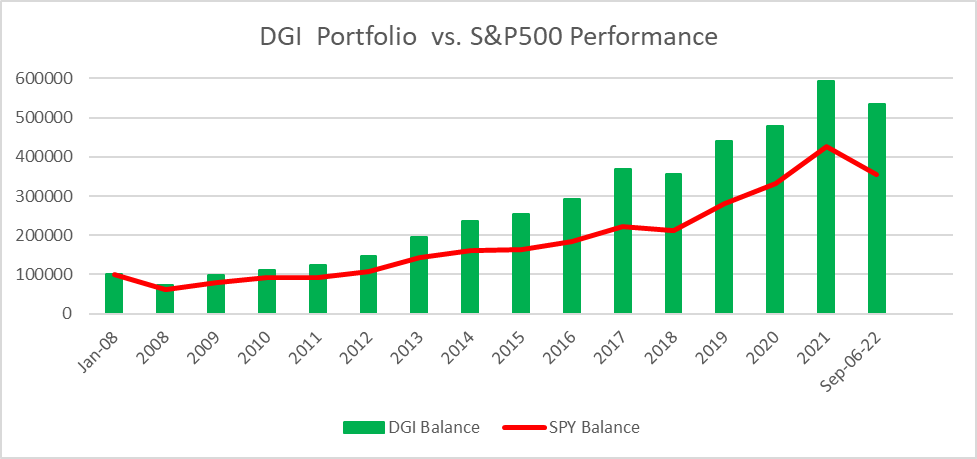

Chart 1:

The below chart provides a backtested performance comparison with the S&P 500, starting Jan. 2008 until Sep-06-2022.

Author

Note: For performance analysis backtesting, a couple of stocks that did not have a history as far back as 2008 were replaced with appropriate substitutes; for example, ABBV was replaced with its parent co. ABT, prior to the year 2013 (prior to spinoff).

Alternate DGI Basket: (With ETFs And Funds)

(Allocation: 35-50%)

This bucket is an alternative to the DGI bucket with individual stocks.

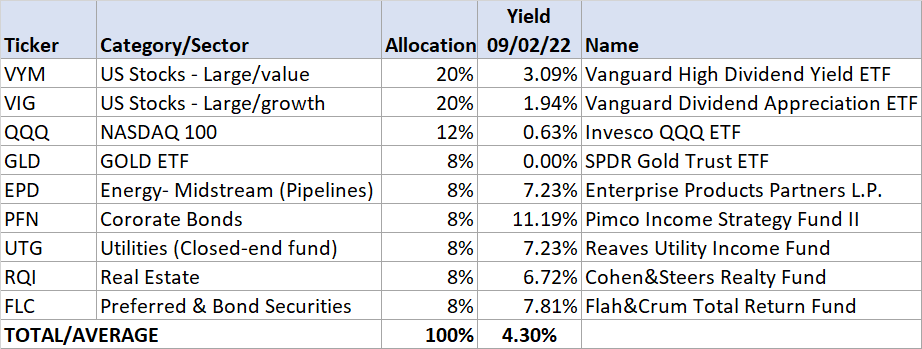

Many folks do not like to own individual stocks. Some do not have time or interest to research individual stocks, while others just want to have a more simplified way of investing. So, keeping in mind the interests of such investors, we will provide an option for the DGI portfolio based solely on funds or exchange-traded funds (“ETFs”). Even though constructing a DGI portfolio of individual stocks is not a complicated process, in this bucket, we will make it even simpler. The advantage of ETFs (or funds) is the wide diversification you can get with just one position. Since we are going to have several funds (roughly 7 or 8), we should be mindful to avoid duplicity. So, we are going to select funds with different goals and asset classes.

In this option, we will select a few low-cost ETFs and mix them with a few high-yield closed-end funds. As per backtesting results, this portfolio should match the market performance by and large, but the distribution yield is more than double of the S&P 500.

Please note that we allocated up to 40% to high-yield funds, including four CEFs and an energy partnership, and 60% to relatively safe, low-cost dividend ETFs.

Table 2: Dividend ETF/Funds (Moderately Aggressive):

VYM, VIG, QQQ, GLD, EPD, PFN, UTG, RQI, FLC

Author

Notes:

- EPD is a partnership and provides K-1 statements at tax time instead of the usual 1099-div.

Here is the comparative performance since Jan. 2008 for the DGI-Fund portfolios in comparison to the S&P 500.

Chart-2:

Author

Rotational Risk-Adjusted Basket:

(Allocation 35% – 45%)

This is our hedging or insurance bucket. This bucket performs the best during the boom or outright bust years, though not so great in a stagnant (frequent up & down) market. However, in the long term, by no means is this bucket a laggard. Here, in the article, we are providing one such strategy. Also, even though the strategy described below does not generate income specifically, due to low volatility, one can safely withdraw 6% of income on an annual basis. Since the Rotational strategies have limited drawdowns and low volatility, withdrawing income does not risk depleting the portfolio at the wrong time.

Please note that we do not recommend moving a very large chunk of money in one lump sum to these strategies. What we recommend is that if you are a beginner, start with a small amount and test the waters for a few months. Thereafter, one should increase the allocation gradually over a long period of time.

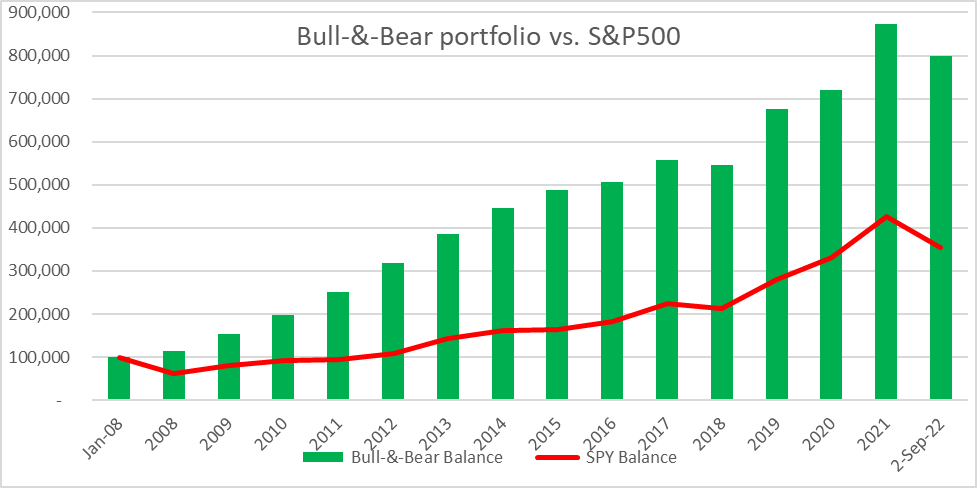

Bull-N-Bear Risk-Adjusted Rotation Model

This portfolio is designed in such a way that it will preserve capital with limited drawdowns during corrections and panic situations while providing excellent returns during bull periods. Due to much lower volatility, this portfolio is likely to outperform the S&P 500 over long periods of time. However, it may underperform to some extent during the bull runs.

The strategy is based on eight diverse securities but will hold any two of them at any given time, based on relative positive momentum over the previous three months. Basically, we will select the two top-performing funds. The rotation will be on a monthly basis. The eight securities are:

- Vanguard High Dividend Yield ETF (VYM)

- Vanguard Dividend Appreciation ETF (VIG)

- iShares MSCI EAFE Value ETF (EFV)

- iShares MSCI EAFE Value ETF (EFG)

- Cohen&Steers Quality Income Realty Fund (RQI)

- iShares 20+ Year Treasury Bond ETF (TLT)

- iShares 1-3 Year Treasury Bond ETF (SHY)

- ProShares Short 20+ Year Treasury (TBF)

Please note that TLT and SHY are long-term and short-term Treasury funds, which are used as hedging securities.

The backtesting results going back to the year 2008 are presented below. The fund TBF was not available until 2009, so it was not included for the years 2008 and 2009.

Growth Chart With No Income Withdrawals

Chart-3:

Author

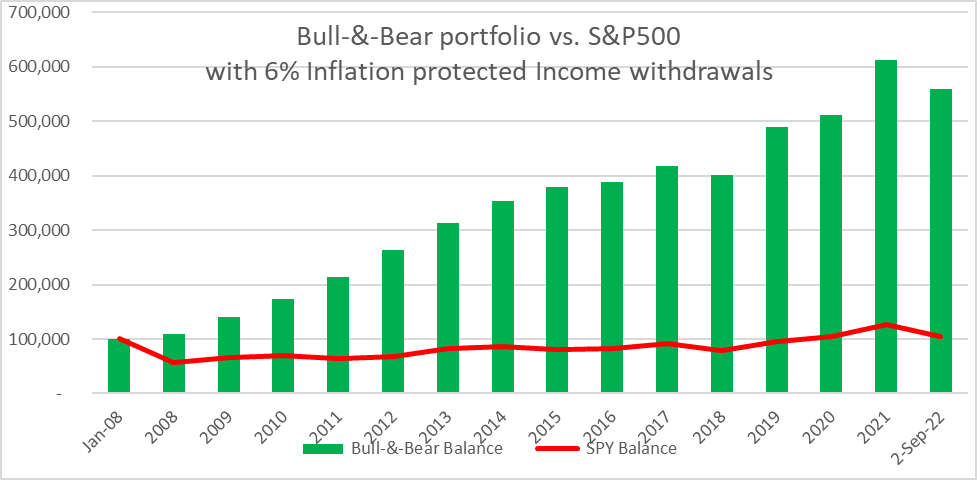

Growth Chart With 6% Income Withdrawals

Nothing can demonstrate any better than the below chart of the dangers of sequential risk (the risk of sequential returns) that it poses to retirees. This chart demonstrates how devastating a deep correction can be at the onset of retirement (if you are to draw income). So, yes, drawdowns matter a lot, especially if you are a retiree who needs to withdraw income and a correction happens early in your retirement years. Due to a deep drawdown and a 6% income withdrawal, the S&P 500 never got a chance to make a comeback in spite of the extraordinary growth of the S&P 500 in the last 12 years.

If you had invested 100,000 in Jan. 2008 in S&P 500 and withdrew 6% income (with 3% raise every year), you would be barely above water with a balance of $105,000. However, the same amount invested in the Bull-&-Bear strategy with similar withdrawals would have resulted in a balance of $590,000 today.

Chart-3B:

Author

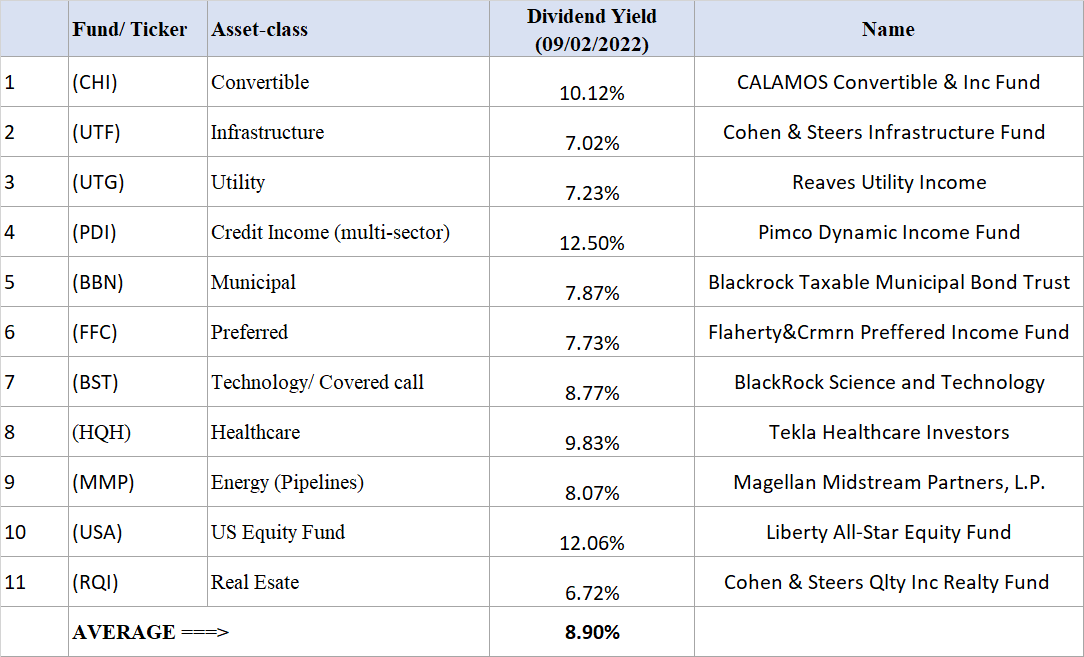

High-Income (8% Income) Basket:

(Allocation: Max 25%)

This basket is recommended for investors who need significant income either in their retirement or otherwise. The main advantage of this basket is that it can elevate the yield of the overall portfolio significantly while limiting the risk to a smaller bucket. In this basket, we usually recommend selecting one closed-end fund from each of the 10-12 asset classes that are available. We would want to select the best funds from each of the asset classes. Below are eleven funds that we have selected. In the energy midstream (pipelines) segment, we prefer individual partnership names like Magellan Midstream Partners (MMP) or Enterprise Products Partners (EPD) over a closed-end fund.

These 11 funds are:

(CHI), (UTF), (UTG), (PDI), (BBN), (FFC), (BST), (HQH), (MMP), (USA), (RQI).

Table-3:

Author

Note: MMP is a partnership and issues a K-1 statement for taxes instead of the usual 1099-div.

For the purpose of comparing the performance of this basket vis-à-vis the S&P 500, we will assume that we invested equally in these eleven funds as of Jan. 1, 2008. Now we will compare the performance of this portfolio with the S&P 500 from 2008 until May 20, 2021. A couple of these funds did not exist all the way back to 2008, so suitable replacements were made for those years.

Most CEF investors are aware that many of these funds use leverage, and leverage can work both ways. Also, this portfolio does not provide any downside protection. That’s why we recommend an allocation of no more than 25% but preferably less. Also, please note this portfolio does not provide any downside protection. The only purpose is to boost the income yield of the total portfolio.

Chart-4:

Author

Alternate High-Income Bucket (Options-Income)

(Allocation: Max 25%)

This is a bucket that would require constant and regular work on a monthly or weekly basis. So, in that sense, this is one of the most active baskets, and it is not for everyone. Also, It may appear to be a bit complex for readers who have never worked with options, and it does have a bit of a learning curve.

Nonetheless, if done conservatively, an options bucket has the potential to provide 10-15% income on a rather consistent basis. Just like any other strategy, there are risks involved with Options, but with some experience, the risks can be mitigated. At the same time, we do not recommend allocating more than 15-25% of the investment capital to this bucket.

If you do not have prior experience with options, we recommend reading some primer and a couple of good books on Options. We also suggest having a trial account (without real money) with your broker and gaining some experience before committing to real money. We also publish a monthly article here on the public SA forum. For the purpose of this section, we will assume that the reader has prior experience with stock options and is well-versed in how to write/sell cash-covered PUTs or CALL options.

We will use this bucket to sell some BUY-WRITE CALL options that would have a long-term expiry, roughly one year out or less. You could also use PUT options (selling cash-covered PUTs) to achieve similar results. You can buy or sell options as one contract or more, each contract representing 100 shares of the underlying security.

For writing a BUY-WRITE CALL option, you submit an online order to buy 100 shares of the underlying stock and sell the covered-call option for one contract at the same time. If you already own 100 shares (or more) of the specific stock in question, you may choose not to use BUY-WRITE but simply sell covered-CALL.

As diversification is important, it is recommended to use more than a few underlying stocks from different sectors/industry segments,

We are going to choose strike prices that are near or below the prevailing prices (ITM or in-the-money) not only to get the best premiums but also to lower the cost of owning the stock. Also, by doing so, the chances are that majority of options will be CALLED away, though that would depend on the market direction. Our purpose here is to earn premiums (income) and not to own the stock long-term. Please note If your purpose was to retain the stock long-term, then this strategy will not be appropriate. Here, with our strategy, there are probably four likely scenarios that could emerge:

- The market (as well as our stock) moves up from here substantially. In this situation, we can close our positions prematurely by buying back the call options and selling the shares at much higher prices, netting a 10-15% or more annualized gain.

- The market stays flat for almost the entire year (highly unlikely); we can then let the options run their entire course of one year. Chances are, 50% of our trades will get called away, and we can write fresh options on the remaining.

- The market dips 5-10% from here and muddles thru’ there for some time. In that case, we get to own shares at a nearly 10 to 15% discount from already lower price points, earn dividends, and write fresh options next year.

- The last and the worst scenario is that market (and our stocks) enters into a full-blown bear market from here. We will have to be patient in that case and keep earning nearly a 3% dividend. The consolation will be that we own some of the best and most stable dividend-paying companies, and we got to buy them at nearly 10-30% lower than their 52-week highs. It should serve us well in the long term. During a market recovery, these companies have the best chance of recovering faster than most others.

A suggestive and sample list of trades is presented below:

Table-4:

Author

* Premium and prices as of 09/07/2022.

If we were to write one contract on all seven trades (as above), we would need roughly $60,000 to buy these shares (buy-price minus premium earned back immediately). Let’s say we do nothing until the expiration date:

- If all the stocks/shares are called away at expiration, we will earn a decent 13% annualized (including dividends);

- If none of the shares are called away, we will earn an income of 42% during this time (including dividends);

- In reality, we will have many positions called away, probably more than half, as the strike prices are nearly 14% lower than current prices. For the rest, we can write new options. However, most likely, we will get plenty of opportunities to close many of these positions early and earn roughly 12% to15% (annualized).

Note: Please note that you should only write/sell options on stocks at strike prices that you would not mind owning long-term. Otherwise, there could be significant risks involved with writing options.

High Growth Bucket (No Income or Minimal Income)

(Allocation: 10% – 30%, depending upon age-bracket)

As noted above, this bucket will provide almost no income. However, this bucket is mainly for relatively younger folks who are in their late 30s or early 40s. They could invest in high-growth stocks and sectors to grow their capital faster when they are still young. For older investors, there is definitely a place to invest in hi-tech or high-growth stocks, but the allocation should be limited. Also, it will depend upon the income needs of the investor since, usually, high-growth technology stocks provide no dividends.

All that said, you should choose high-growth investments rather carefully. There’s a difference between growth stocks and speculative ones. A high-growth stock in 2022 may turn out to be a dud in 2023, and so on. Also, please note that this bucket has no hedging mechanism, so it will likely have high drawdowns in case of a market correction. If you do not have tolerance for large drawdowns, it is better to stay away.

We would recommend the following method choosing a set of high-growth stocks at a given time and then repeating this process at least once a year.

-

- Market capitalization > $10 Billion (preferably > $20 Billion)

- Forward EPS (3-5 years) Growth Estimates > 10%

- EPS Growth (3-year history) > 7%.

- Revenue Growth (last 3 years) > 6%.

- Revenue growth current year vs. the previous year > 6%.

- Price-performance (52 weeks) > Price-performance-52-WK for S&P500 (or Nasdaq-100)

- Price-performance (13 weeks) > Price-performance-13-WK for S&P500 (or Nasdaq-100)

The above criteria can be adjusted higher or lower based on how many stocks come up in the filtered list.

As investor approaches retirement, they should gradually reduce exposure to this bucket and increase allocation to other buckets like DGI, Rotation bucket, and high-income securities (CEFs, REITs, BDCs).

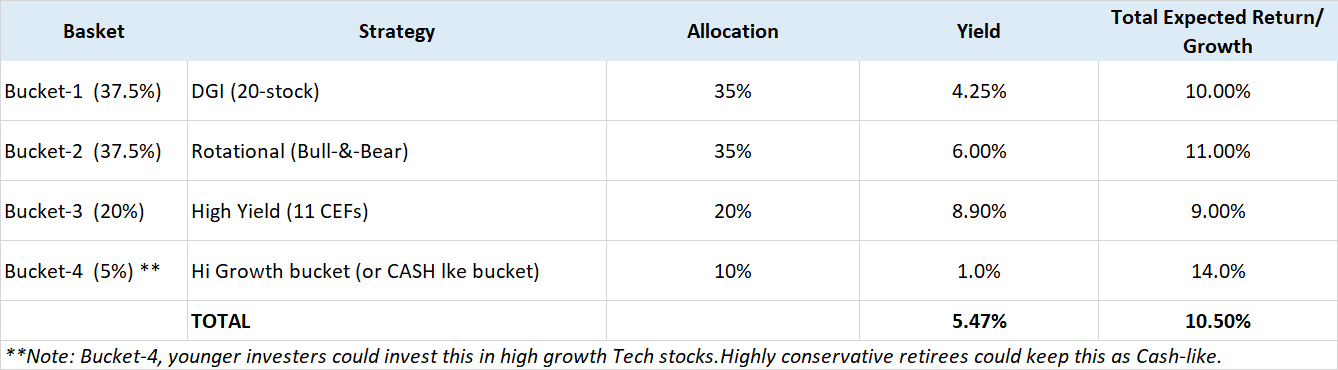

How to attain Financial Freedom in 15 years using the NPP strategy?

Table-5: Structure of an NPP Portfolio

Author

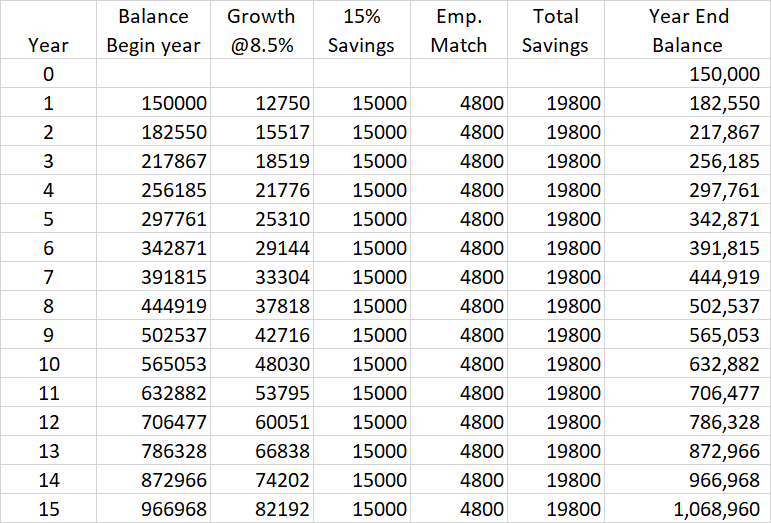

Let’s assume you are 40 years old and have $150,000 saved so far. Though goals can vary from one individual to another, let’s assume that you will need $1.0 million to achieve financial freedom to cover your basic expenses. We are not talking about retirement goals, as you will probably need much more to retire comfortably, especially with a higher inflation environment. To achieve your financial freedom goal of $1 million, you will need to do both, save aggressively (at least 15% of your income) as well as achieve an average of 9-10% rate of return over the next 15 years.

But for the purpose of demonstration, let’s assume a conservative rate of growth at 8.5% on a yearly basis. Also, assuming your annual income is $100,000, here is the table that shows how you can achieve your goal in 15 years.

Table-6:

Author

Concluding Thoughts

The boom-and-bust cycles have always been part of the market but may have become more pronounced due to Fed’s policies. In the last three years, at least thrice we had serious market declines. Obviously, the current situation is no different. The intent of this article was to present a set of strategies that an investor could use to form an investment portfolio that is less prone to market extremes (resulting in less stress), provides stable income, and has a decent growth trajectory.

We have presented six different types of strategies, and investors can pick and choose at least three of them to make a multi-basket portfolio. We certainly recommend a certain allocation to the Rotational bucket to provide the necessary hedge, lower volatility, and drawdowns, and smooth out the returns.

Be the first to comment