Darren415

This article was first released to Systematic Income subscribers and free trials on Oct. 14.

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the second week of October.

Be sure to check out our other Weeklies – covering the Closed-End Fund (“CEF”) as well as the preferreds/baby bond markets for perspectives across the broader income space. Also, have a look at our primer of the BDC sector, with a focus on how it compares to credit CEFs.

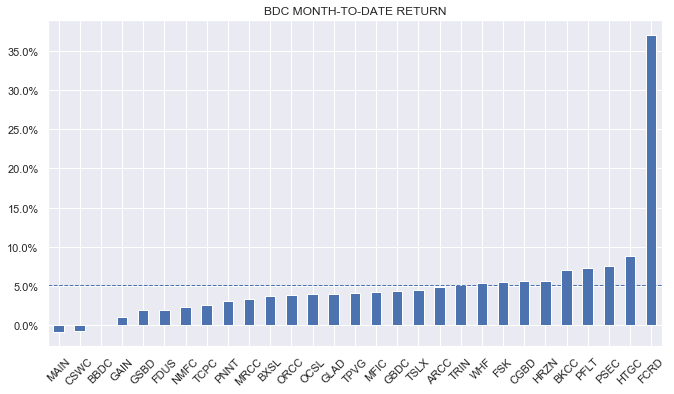

Market Action

BDCs managed to finish in the green this week despite continued high volatility across the broader income space. Most companies remain up so far in October after a tough September with only the two high-valuation companies at negative returns this month.

Systematic Income

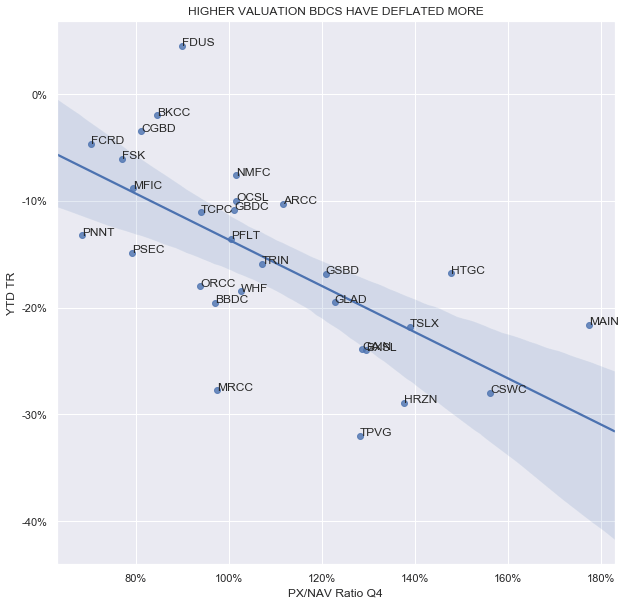

The theme of higher-valuation BDCs underperforming very much remains in play in the current weak market and highlights the danger of chasing “winners” in a strong market.

Systematic Income

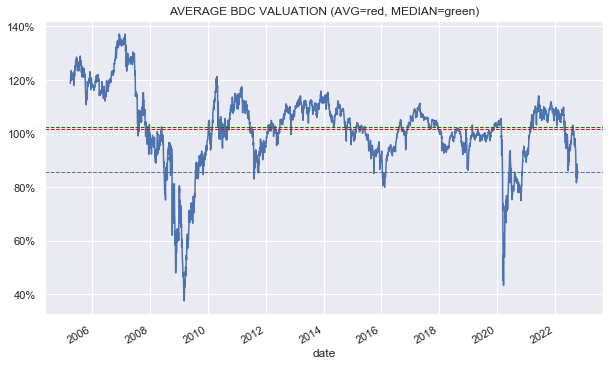

BDC sector valuation has stabilized around previous troughs outside of the GFC and the COVID crash. We don’t expect the sector valuation to approach these lower lows (i.e. 40% valuation trough) as the current macro picture looks to be a traditional Fed-induced recession rather than an existential crisis for the economy and markets.

Systematic Income

Market Themes

We have yet to fully enter the Q3 reporting season for the BDC sector, however, there are early indications that the sector is holding up quite well.

First, over the last few weeks a number of BDCs have increased dividends. These include TRIN, CSWC, GAIN and GLAD while WHF declared a new special dividend. Continued dividend hikes are not unexpected in a rising short-term rate environment – a big chunk of the sector raised dividends in Q2 as well.

However, perhaps more important is the fact that higher dividends are also an indication that sector portfolio quality is not falling off a cliff. After all, if non-accruals, PIK or defaults spiked over Q3, companies would be very unlikely to be raising dividends.

Second, we have also seen early indications of NAV estimates. SAR, which has already reported official numbers saw a drop of 1.5% (0.35% of that was due to bond extinguishment) – that’s much better than the Q2 drop as well as smaller than the average BDC NAV drop in Q2. CSWC announced an estimate for its NAV whose midpoint is only marginally below its Q2 level. Though this is still anecdotal it is another sign that we are not seeing a sharp fall-off in portfolio quality in the sector.

We are very likely not yet through the full market drawdown but the fact that in the middle of its tenth month the sector remains relatively resilient is a good result for BDC investors.

Market Commentary

Golub Capital (GBDC) said it originated $177m in new investments and that the fair-value of its portfolio fell by 3%. Unfortunately, this doesn’t actually tell us a whole lot. We don’t know how many prepayments it had so we don’t know what the net new investment number is. That said, it is very likely to be negative based on its previous prepayment run rate shown in the table below. The 3% drop in the portfolio sounds like the NAV is a lot lower but that could be all due to the drop in net new investments.

GBDC

Capital Southwest reported preliminary Q3 estimates. Q3 net income rose 5.5% QoQ and the Q3 NAV estimate came in flat to Q2. Overall, that’s a very good result for the sector. It will be interesting to see how the NAV change breaks down into unrealized depreciation (i.e. wider credit spreads), prepayment fees and NAV accretion from at-the-market sales. The boost from ATM sales should be low given the CSWC premium has fully collapsed from 175% to 101% and prepayment fees should be fairly low as well since prepayments tend to run low when financing costs rise. This suggests that unrealized depreciation is low which, in turn, suggests that portfolio quality should be holding up well across the sector.

Systematic Income BDC Tool

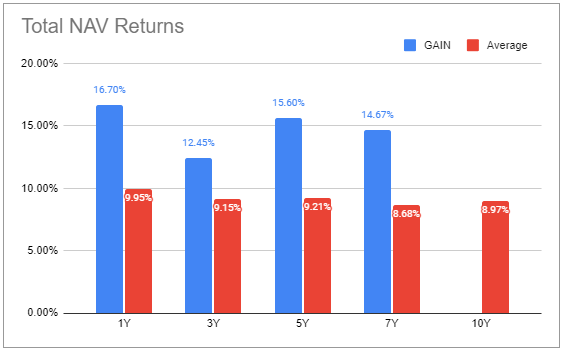

Gladstone Investment boosted its regular dividend by almost 7% – the total dividend increase is a more modest 3% given its supplemental which will also be paid in December. The company is a bit of an oddball in the sector due to its undiversified portfolio and large allocation to preferreds. Its net income is also well below its total dividend though its total value generation has been running at a very strong level as the chart below shows. GAIN is trading at a 91% valuation or 5% above the sector average and a 11.8% total dividend yield.

Systematic Income BDC Tool

Stance & Takeaways

We continue to see value in the BDC sector on the back of its rising net income, apparently resilient NAVs and attractive valuation levels. We continue to see value in names like CGBD, GBDC and FDUS held in our High Income Portfolio in both absolute and relative (i.e. valuation relative to sector) terms and would consider adding opportunistically to names like ARCC and GAIN on further weakness.

Be the first to comment