PaulMcKinnon/iStock Editorial via Getty Images

A&W Revenue Royalties Income Fund (TSX:AW.UN:CA, OTC:AWRRF) is powered by an extremely popular restaurant chain in North America – A&W. It is actually the second-largest hamburger chain in Canada behind McDonald’s Corporation (MCD). The home of the burger family is a household name in much of North America and is an under-the-radar dividend play in Canada.

Keep in mind the company is listed in Toronto and trades in Canadian dollars. It fits the portion of the market as a slightly more expensive option than McDonald’s, with the marketing of better quality of ingredients. It focuses on themes like no antibiotics and grass fed beef, trying to appeal to those looking for quality ingredients. This creates a company that consumers can trust, which is essential to people during a time where wallets are stretched. Features like glass mugs and metal trays at restaurants help give it a premium feel other fast food options lack.

It has shown impressive growth in Canada over the last 20 years, with over 500 restaurants added in this time. A&W Trade Marks Limited Partnership owns the ability to create the restaurants in Canada. It is a great option for dividend growth investors looking for a solid yield. The company takes 3% of all revenues from A&W restaurants in the pool as a royalty and pays it out monthly to investors. This means a very consistent flow of dividends to investors and no issues with margin compression. Inflationary issues continue to hurt other restaurant earnings but apparently are not an issue for AW.UN:CA.

This means that you avoid much of the issue of profit margins or capital expenditures. Instead, the revenue and same-store sales growth are the main focal points contributing to dividend growth. Same-store sales growth for Q3 was 4.0%, but the growth for the year-to-date was an impressive 8.9%. Total royalty revenue growth for the year as of Q3 was 11.9%. That is comparable to the other strong performers in the industry even after very strong 2021 same store growth of 14.0%.

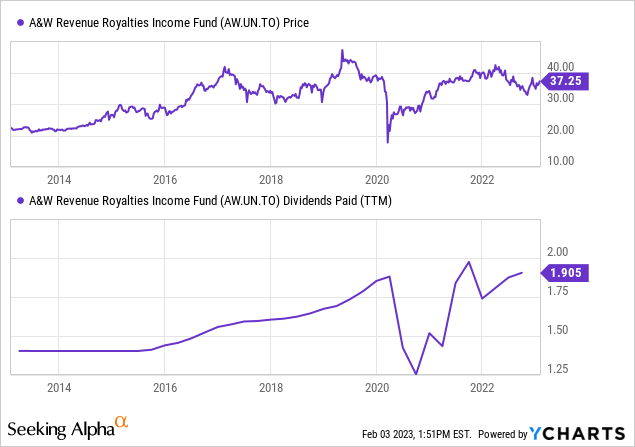

Growth of stores for 2023 are continuing to be slowed by the economy, with 29 new restaurants being added up to 1037. As of February 3, 2023, the stock is paying a $1.92 forward cash yield per year, or 5.15% at today’s price. The stock is particularly attractive above 5%, as that level it is above most high-yielding equities with a superior growth profile. It also is in a different sector than other equities with most of them being Utilities or REIT’s rather than a consumer discretionary name. This means you can use AW.UN to diversify your dividend portfolio and add something not correlated as much to interest rates. Rather the company does better during the start of bull markets with low interest rates and strong consumer confidence.

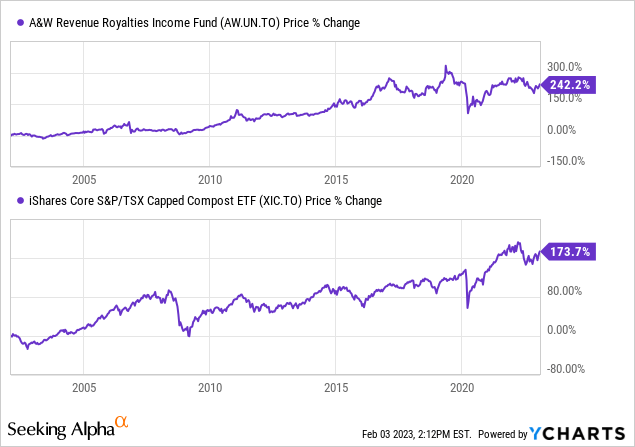

Since inception, the fund has beaten the TSX significantly, although it has underperformed in the past few years with the pandemic hurting restaurant sales. As you see below, it has almost 70% excess return against the wider TSX index over the past 20 years. Long term, A&W Revenue Royalties Income Fund has provided both a better yield and a better compound annual growth rate for investors. As you can see below, long-term CAGR since the fund was established in 2002 was 6.34% plus 3 to 5% of additional dividends. This includes heavy outperformance in significant market downdrafts such as in periods of weakness like 2008 or early 2016. 2020 was the exception to this, as many restaurants were forced to close completely for diners – a scenario likely to hopefully not happen again in our lifetimes.

If you believe that was an anomaly, the menu innovation and focus on quality should lead to long-term gains. The company has had great success with Beyond Meat (BYND) collaborations and is willing to try new things to drive sales growth. If plant-based options end up catching on in the future, they have shown they will embrace those trends. The track record of the chain and stability gives strong confidence in long-term dividend growth.

Conclusion

Now is not the time to take additional risk in this market, especially with continued pressure on net income margins in 2023. Royalty plays should outperform in 2023, as margins contract people search for significant yield with lower risk. A&W has a reasonable valuation right now, as yield options have gotten more plentiful with the higher bond yields. However, as longer-term yields begin to fall it will provide a tailwind for AW.UN to provide both solid yield and long term growth to shareholders.

Those with Canadian dollar portfolios should take a close look at AW.UN stock for their income needs. A&W Revenue Royalties Income Fund stock is a buy for investors that are holding Canadian dividend stocks, as it will help them diversify from their core sectors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment