Nordroden/iStock via Getty Images

The Q1 Earnings Season for the Silver Miners Index (SIL) is set to begin next month, and one of the most recent companies to release its preliminary results is Avino Silver & Gold (NYSE:ASM). While Avino saw an improvement in gold and silver production sequentially, gold production fell sharply, impacting the company’s silver-equivalent ounce [SEO] production in Q1. However, production should steadily increase as the year progresses. At a market cap of ~$120 million or $1.00 per silver-equivalent ounce, Avino is a cheap way to get exposure to silver, but I continue to see more attractive bets elsewhere for now.

Avino Silver & Gold Mine (Company Presentation)

Production

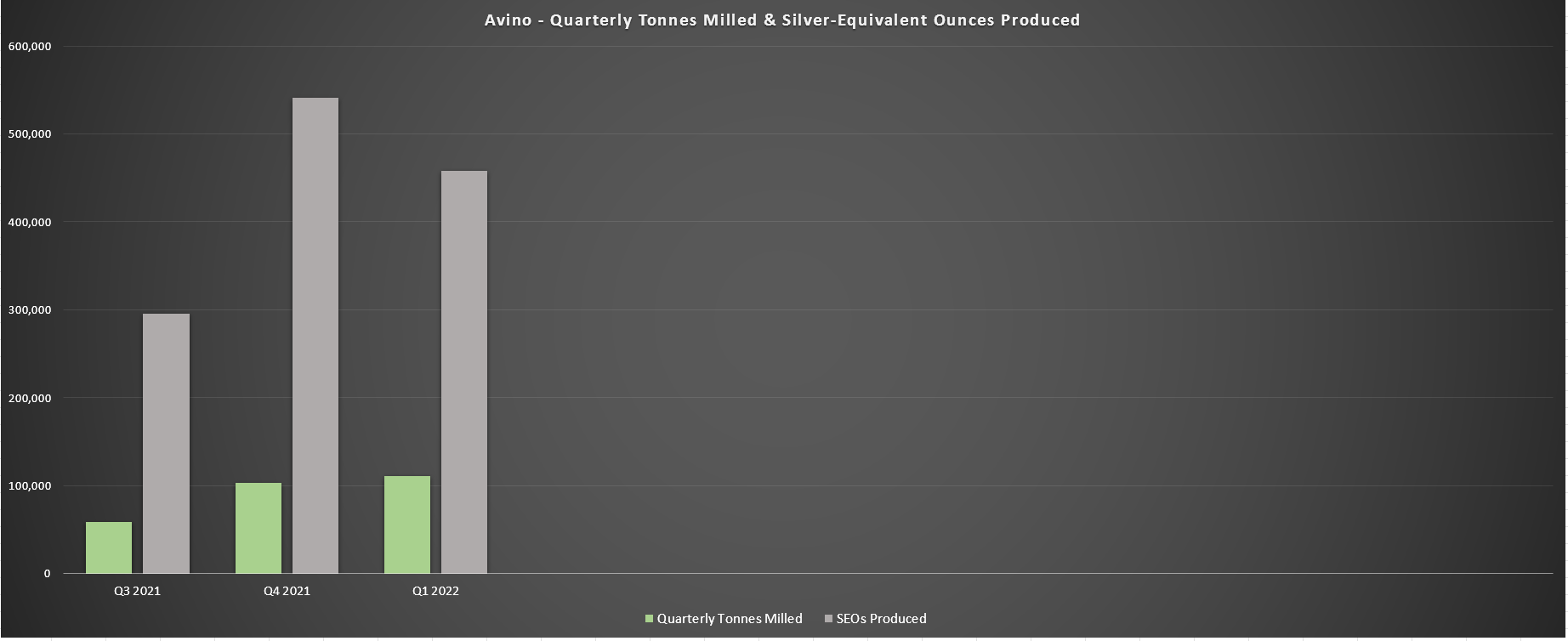

Avino Silver & Gold (“Avino”) released its preliminary Q1 production results last week, reporting quarterly production of ~457,800 SEOs, a 15% decline on a sequential basis just after returning to more normal production levels after an extended period in care & maintenance. However, while this production result looks disappointing, it’s worth noting that it was largely expected. This is because it was related to mining more normal grade areas of the mine from a gold standpoint, with Avino not benefiting from gold grades above 0.80 grams per tonne gold as it did in Q4 2021. Let’s take a closer look below.

Avino – Quarterly Silver-Equivalent Ounces Produced (Company Filings, Author’s Chart)

As the chart above shows, Avino saw another sequential improvement in throughput in Q1 to ~111,100 tonnes, a 7% improvement from the ~103,500 tonnes processed in its most recent quarter. However, while silver and copper production increased in line with the higher throughput, production was down on a consolidated basis from ~541,400 SEOs to ~457,800 SEOs. This was related to a 60% decline in gold grades from 0.86 grams per tonne gold to 0.29 grams per tonne gold, which led to the production of just 801 ounces of gold vs. 2,158 ounces in the most recent quarter.

As noted above, the decline in grades was related to mine sequencing to more typical areas of gold grades in the mine, impacting production in the period. However, if the company can return to its planned throughput rates north of 2,000 tonnes per day, this will offset the lower gold grades that the company benefited from in H2 2022, allowing the company to return to a 600,000+ ounce per quarter production profile. As it stands, Avino is tracking well behind its guidance mid-point of 2.4 million SEOs at just 19.1%, but a slow Q1 was to be expected as the operation ramps back up and heads into lower-grade zones from a gold grade standpoint.

Exploration

While production was a little below my estimates in Q1, the company had some exploration success, with the company continuing to invest in adding higher-grade ounces and upgrading resources. While last year’s results were mediocre, in my view, with strong grades but over relatively narrow widths (excluding the Brecha de Bajo Vein), Avino did report some decent results in Q1. This included 4.40 meters at 463 grams per tonne silver-equivalent (LP-21-06) and 2.95 meters at 668 grams per tonne silver-equivalent (LP-21-07) at La Potosina.

La Potosina lies just five kilometers from the Avino milling facilities, and the nine holes released were decent, with more than 50% of intercepts coming in above the company’s average M&I resource grade of 129 grams per tonne silver-equivalent. While the 2nd best hole (LP-21-06) came in at just 1.70 meters in true width (4.40-meter reported interval), it was more than triple the grade of the average M&I resource grade (463 grams per tonne silver). Meanwhile, LP-21-07 intersected 400% higher grades at 668 grams per tonne silver-equivalent, with high silver grades (617 grams per tonne) and moderate gold grades (0.60 grams per tonne gold).

While too early to speculate on a relatively small batch of holes, this is one of the company’s high-grade, near-surface targets and could supplement mill feed. For those unfamiliar, the operation is currently mine constrained, not mill constrained, with available throughput of 2,500 tonnes per day. For now, though, the results are encouraging, and it certainly wouldn’t take much material from La Potosina to make a difference, given that it looks to be at least twice the grade of current mined grades on a silver-equivalent basis.

Oxide Tailings Project

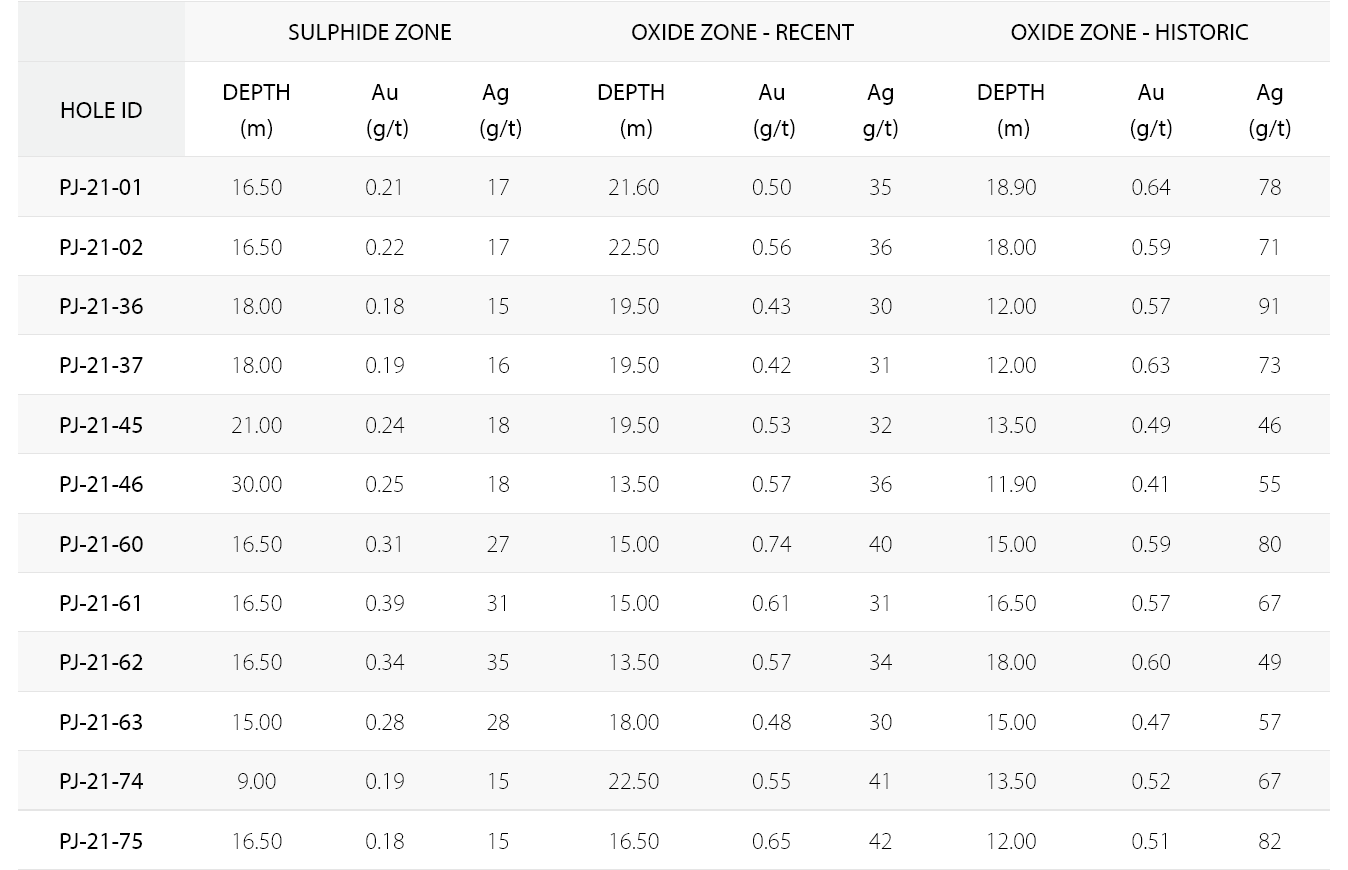

Meanwhile, southwest of the Avino Mine and Mill, Avino is continuing to work on its Oxide Tailings Project, which involves its current tailings storage facility. The table below shows drill results from its current tailings storage facility, which will soon be replaced by a much more environmentally friendly dry-stack tailings facility. This could open up the opportunity to allow the company to reprocess this material, which appears to have solid gold grades north of 0.50 grams per tonne gold.

Drill Highlights – Tailings (Company News Release)

While this is another upside opportunity for now with no Feasibility level work completed, the goal is to upgrade the inferred mineral resources to the M&I categories and expand the resources, and then upgrade to a Pre-Feasibility Study. Under the previous PEA (2017), capex was quite modest at just ~$29 million and had a projected 7-year mine life, with a pre-tax IRR of ~48% at conservative metals prices ($1,250/oz gold, $18.50/oz silver). The plan is for this to be a stand-alone project, producing 33,000 ounces of gold and just over 6.1 million ounces of silver over seven years, which would improve Avino’s production profile if it were to green-light the project.

Valuation

Compared to other silver producers like Excellon Resources (EXN), Avino may look expensive on the surface, given that it has a similar production profile and trades at nearly four times Excellon’s market cap. However, it’s important to note that Excellon is operating at a loss at current silver prices at its Platosa Mine, it doesn’t have a large project nearby with optionality (La Preciosa), and Avino has a significant resource base, even relative to some of its larger peers. In fact, with over 150 million silver ounces in the M&I category, Avino is valued at less than $1.00 per silver ounce (including La Preciosa) or barely $1.00 per silver-equivalent ounce excluding La Preciosa.

This represents a very reasonable valuation, especially for a company with some existing capacity at its mill that also could put a new project into production by 2025. So, for those looking for silver exposure at a reasonable price within the producer space, I would argue that Avino is not a bad way to gain exposure. Having said that, I see it as a swing-trading vehicle only, given that Avino operates in a Tier-2 jurisdiction and is a single-asset producer, making it a higher risk name than peers like Hecla Mining (HL), where any potential issues at one mine are not magnified.

So, where is the stock a Buy?

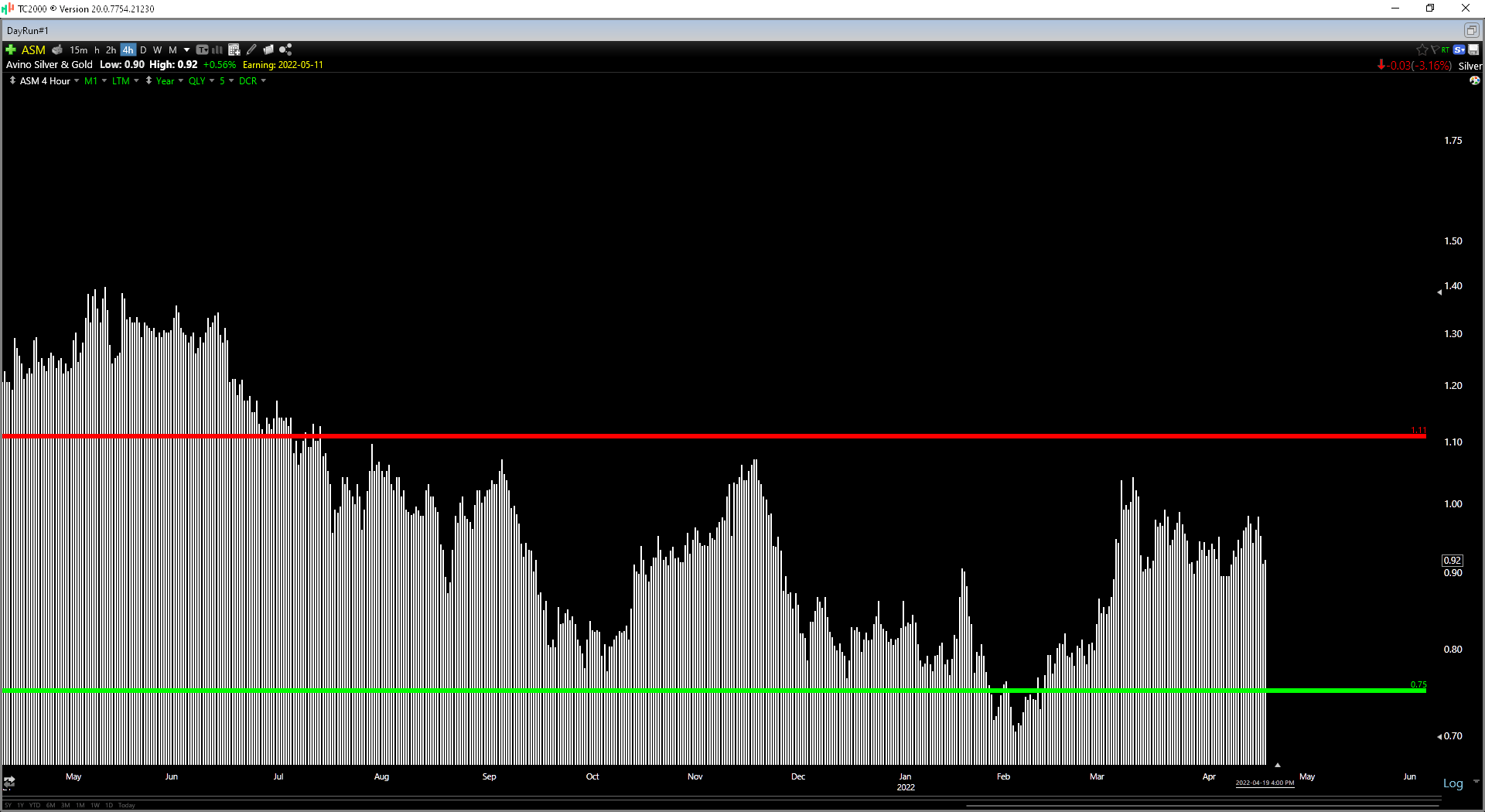

Looking at the chart below, we can see that Avino has strong support near US$0.75 and resistance between US$1.04 – and US$1.11. When it comes to single-asset producers and micro-cap names, I prefer to buy at or below support, which in Avino’s case would come in at US$0.75. So, with the stock sitting more than 10% above this level at US$0.92, I do not see this as a low-risk buying opportunity. This doesn’t mean that the stock can’t go higher. Still, with several producers paying dividends and buying back shares with higher-quality business models, I would only be interested in Avino at the right price. That price is US$0.75 or lower.

ASM Daily Chart (TC2000.com)

Avino had a slow start to the year due to unfavorable mine sequencing, but it should see a lift in production in H2, and I would expect the company to produce at least 2.2 million SEOs this year. At a $24.50/oz silver price, this would translate to ~$54 million in revenue, a meaningful improvement from last year’s levels. However, with ASM in the middle of its trading range, I’m not in a rush to buy just yet. To summarize, I think there are more attractive bets elsewhere in the sector, but I would strongly consider buying Avino for a trade below US$0.75.

Be the first to comment