Paul Campbell/iStock via Getty Images

Published on the Value Lab 12/27/22

Avid Technology (NASDAQ:AVID) sells software used for editing and producing music as well as comprehensive systems designed for professional studios and sound production facilities. The narrative has been around them transitioning from the perpetual license model to selling their services on a subscription basis instead, which grows their recurring revenue in the mix and understates their billings growth with the GAAP sales figures. While they still grow on the subscription side, the issue is that they’ve been exposed to supply chain issues on the sales of their integrated systems. Since the growth is in the more important channels for the margin, the current multiple looks increasingly fair as their price languishes and the possibility of a Fed pivot increases. Avid could be a buy from this level.

Key Q3 Observations

Let’s walk through the Q3 results.

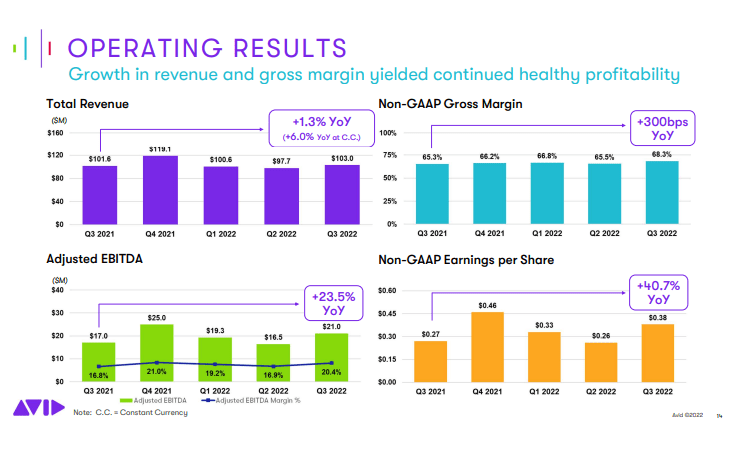

Financial Highlights (Q3 2022 Pres)

Revenue growth is pretty limited YoY at 1.3%. This is partially coming from the changes they’re making to their revenue structure. More revenue is coming from recurring products as Avid transitions away from the previous industry standard of selling perpetual licenses for their software.

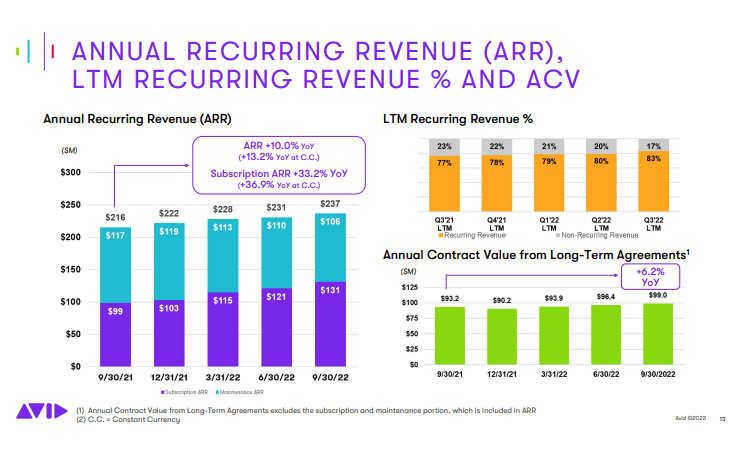

ARR (Q3 2022 Pres)

Recurring revenue is growing in the mix, and the ARR growth, even proportioning it downwards to represent the whole billings picture, exceeds the revenue growth figures due to revenue recognition principles around subscriptions. Indeed, even the direct revenue picture on a quarterly basis for growth in recurring revenue sources looks really good at 17.6% YoY. We remind readers that the decline in maintenance revenues is coming from some of those capabilities becoming paid for in the subscriptions.

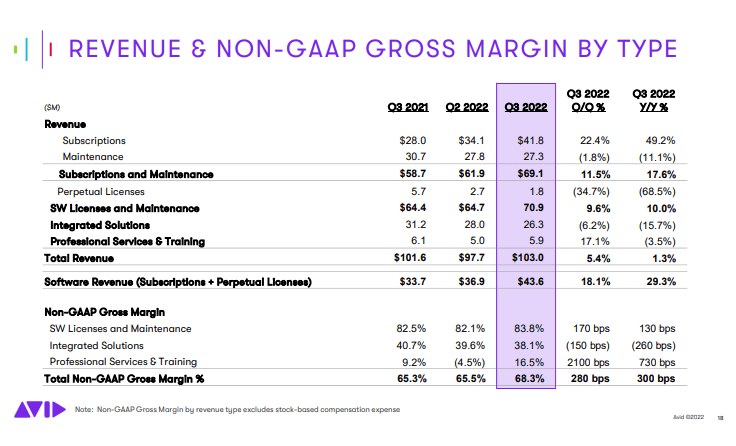

Revenue Splits (Q3 2022 Pres)

Outlook

Nonetheless, the baseline force to revenue growth is weakening and it’s coming from integrated systems, which drove a decline in non-recurring revenue sources by about 21%. Integrated systems have a much smaller margin impact than other sources of revenue as much of it comes from sourcing and combining partnered hardware with software plus a consultancy markup in providing integrated systems for media rooms, studios, sound production facilities etc.

Gross Margin (Q3 2022 Pres)

Sales of integrated systems go less than half the distance of sales in subscriptions, maintenance services and licenses. The gross margin is therefore actually improving despite a pressured sales picture due to mix effects.

Still, the pressured sales takes away from what could have been the sales and profit growth of the company, and the pressure on integrated solutions is coming from sourcing the components. There has been some sign of improvements:

Hey, Paul, this is Jeff. So first, I’ll take the first part of your question. I’ll let Ken take the question on the free cash flow site. On integrated solutions and the supply chain situation. What we have seen is that a lot of the more common components, which we were struggling with earlier in this year ICs, and some of the more common PCB availability, that has gotten better, or we’ve redesigned around some of those shortages, and gotten ourselves to more common components that can help us bring the supply up.

But the company believes the pressure will only really be relieved by mid-2023, which is a while from now.

Nonetheless, the substantial growth of over 40% in net income is enough to justify a 24x P/E multiple, and their products suite remains powerful standards in the music and media industries, including Sibelius which is more academic, but especially Pro Tools. With the possibility of a Fed pivot coming soon too, the hour for growth stocks may be drawing near. Moreover, any dilution risks from outstanding stock options appears limited for Avid at less than 3%. This could be a time to consider Avid as a quality pick with under-the-weather segments that are likely to see a revival as supply chains normalise.

Be the first to comment