Feverpitched

2023 Market & Commodity Outlook

It’s that time of year and we’d give our outlook for 2023 and how we are investing our own money. Since we have a background in commodities and run an energy royalty company, we do focus our outlooks on commodities – it’s what we know and so it will be commodity heavy. But just like all things traded, macro factors should influence markets heavily.

So where do markets go from here?

Bifurcated Markets In 2023: First Half Of Year May Be Ugly

When it comes to macro-analysis, it’s critical to take the obvious factors first as none of us know the future, so it’s much easier to predict implications of high-probability events versus predicting what the actual events will be.

The most obvious events that we see happening across the globe is the tightening of monetary policy. The Fed, ECB, BOJ (yes even Japan) have all been tightening monetary policies via interest rate raises, and more importantly, Quantitative Tightening – that is the running off of bonds held on balance sheet.

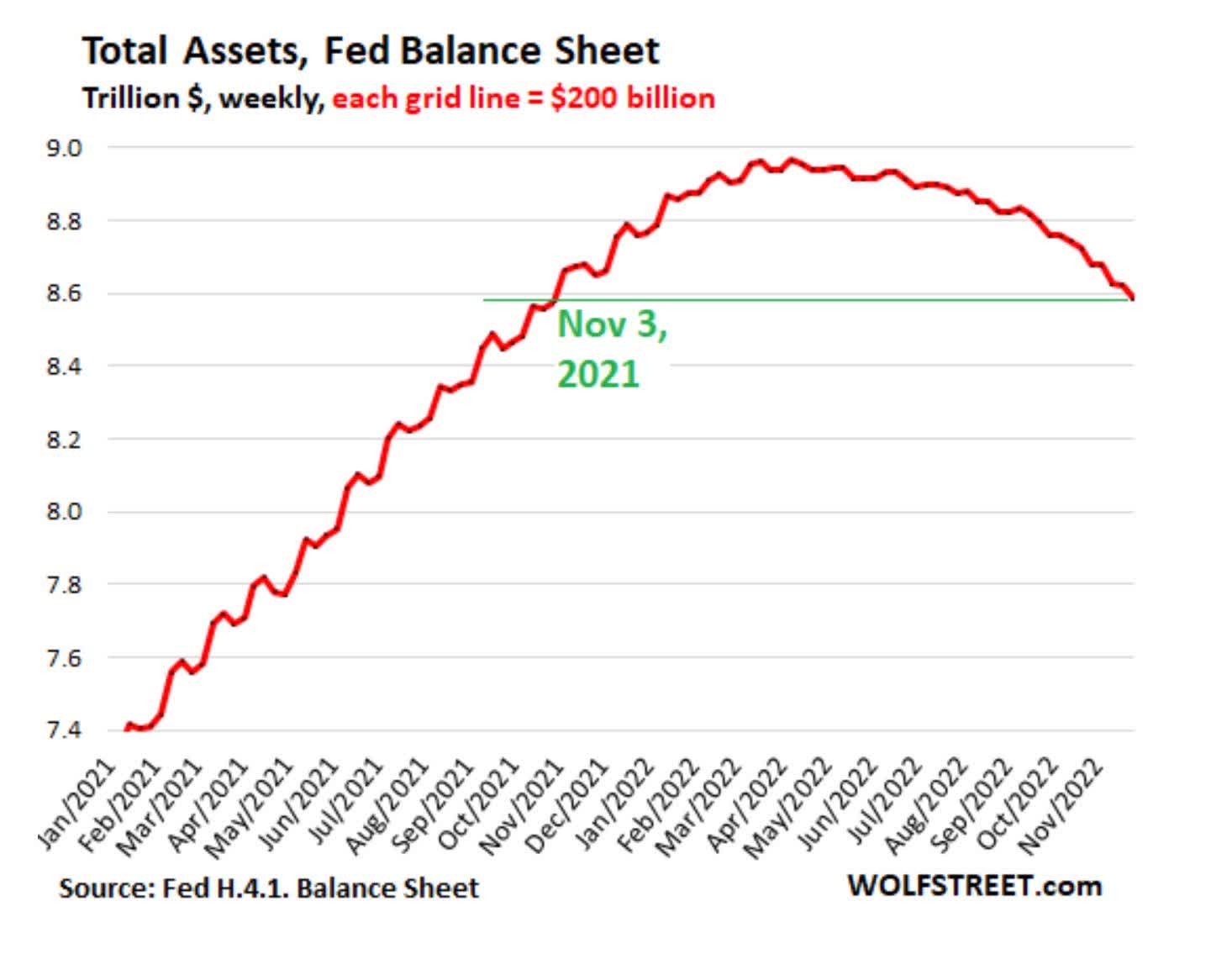

The Fed has been letting assets mature off its balance sheet for the last 8 months:

FED Balance Sheet

As balance sheet assets mature and are repaid back to the Fed, the Fed essentially “destroys” this money, which is the opposite of QE. And of course, as this happens the monetary base decreases and that means less money to pursue assets.

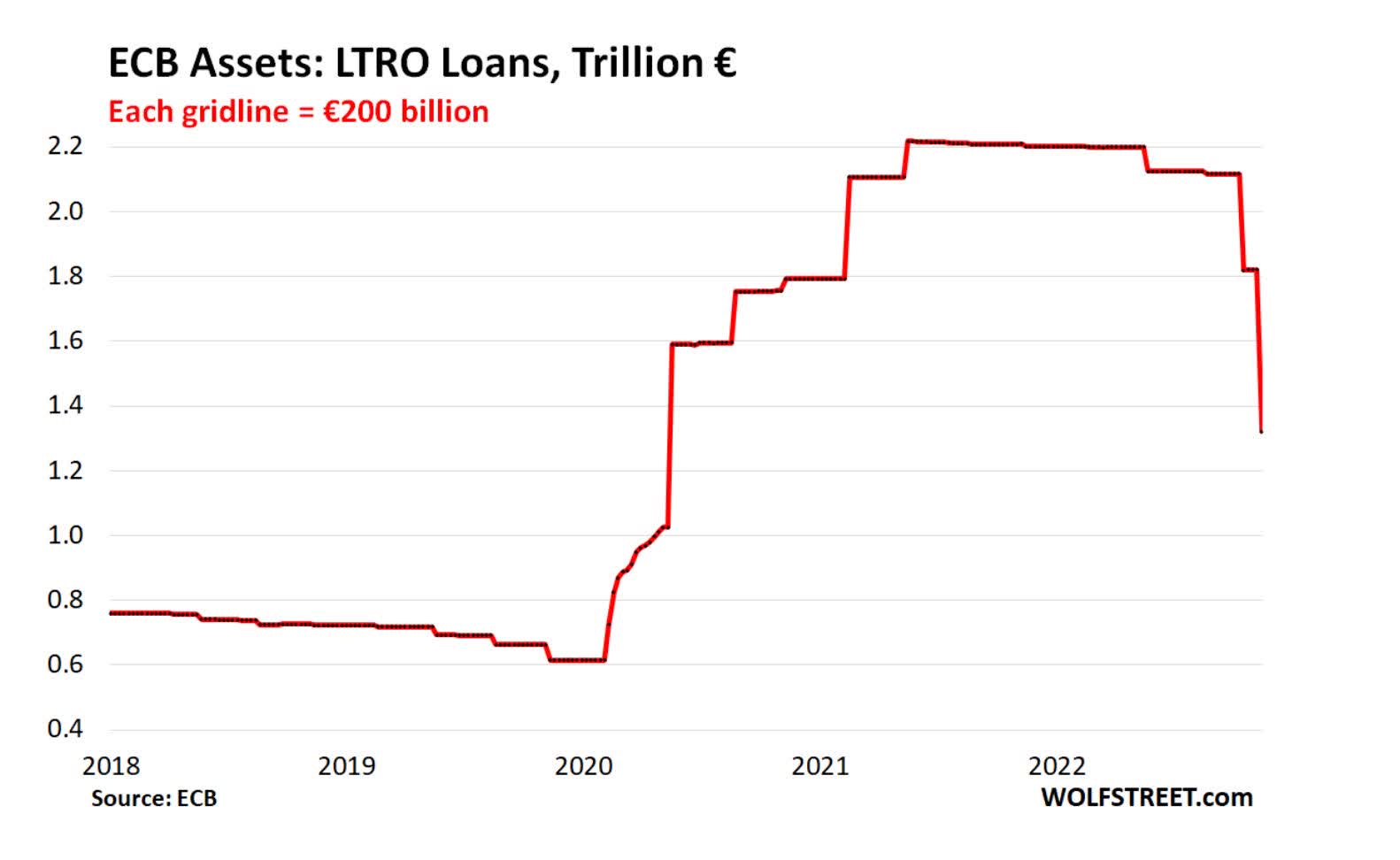

It’s not just the Fed, the Bank of Japan recently raised its bond-market peg (i.e. monetary tightening) and as WolfStreet reports, the ECB has been tightening its LTRO assets as well:

ECB LTRO Operations

While the ECB hasn’t yet started shedding its balance sheet bond assets, it has stated that by March 2023 it will begin letting bonds mature (i.e. Quantitative Tightening).

Thus the largest global central banks are tightening monetary policy via interest rates and balance sheet declines, that’s not the best environment for risk assets and certainly will be headwinds for markets and why we think the first half of the year will be bearish.

Having said that, we think that we are headed into a global recession as monetary stimulus ends and reverses, and firms across the globe start cutting hiring and capital spending. The Fed has cited a resilient job market as its reasons for continued tightening, but we feel the Fed is dead-wrong on the job market and is citing strength in the lower quality jobs where employers are finding it hard to find employees ($12-15 / hour jobs that still haven’t risen sufficiently for inflation) versus the much higher quality jobs where we are seeing layoffs (bank, technology, etc) – that will eventually trickle down to the lower end of the job market.

What all this means is that as global monetary tightening sets of a recession through the first half of the year, central banks will be forced to first drop their tightening, and then finally start once again with stimulus.

China Reopening: A Flop In The Making

Despite the weak economic outlook, whenever markets rise the reasoning almost always ends up with a reason coming back to a massive “Chinese Reopening”, and the implications of One Billion plus people “-re-entering” the global economy. Unfortunately, we are not buying it and we think it’s potentially the greatest “oops” of financial predictions for 2023.

Let’s take a step back here and really mentally process this. Have Chinese citizens been stuck in their homes not producing and eating Ramen noodles in front of their fireplaces for the last 2 ½ years waiting for the moment they could actually live again? Absolutely not – nothing could be further from the truth! Yes, China has been on lockdowns with limitations, but economic activity has continued significantly.

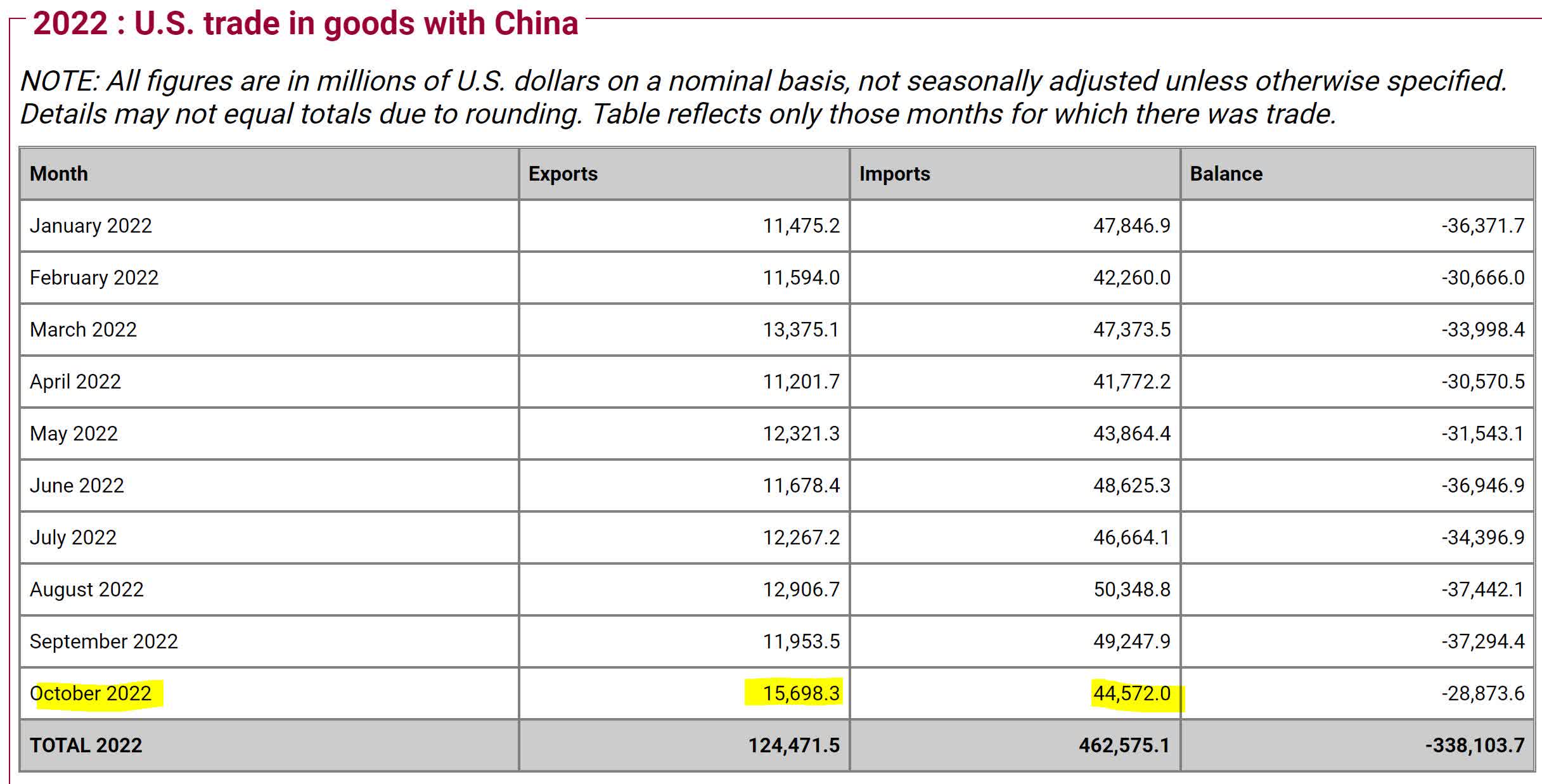

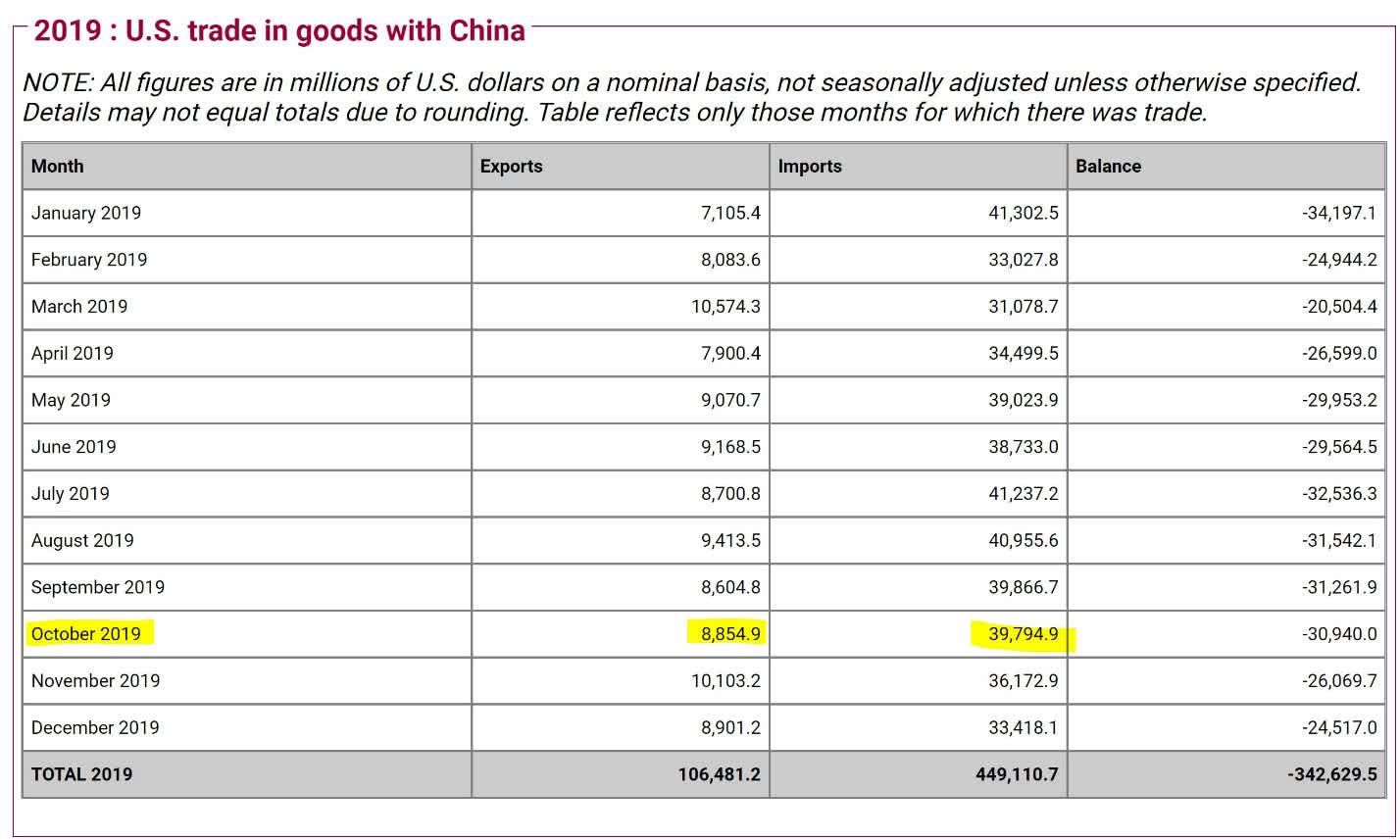

Instead of going on media headlines, let’s actually take a look at the data from the US Census Bureau for 2022 & 2019 (pre-Covid) trade with China:

US Census Bureau

US Census Bureau

As is shown in the charts above, Chinese trade with the US in October 2022 (Covid lockdowns still active in China) was $45 billion in terms of its exports compared to $39 billion in October 2019 before COVID. China has been exporting 15% MORE in COVID lockdowns this year than they did before COVID.

In fact, China has been exporting more to the US in EVERY SINGLE MONTH of 2022 than it did in 2019! That suggests that the economy has been humming along just fine despite Chinese lockdowns, and we fail to see what kind of boost will happen as China lockdowns end. Maybe more Chinese travel spending, but that will simply come from spending elsewhere and will not ultimately be new spending – the kind that markets are hoping for.

Additionally, if the rest of the world experiences a recession it will not leave China alone. China is the largest gross world exporter of goods and products, so any decline in the world will affect the Chinese economy, and in turn the Chinese worker.

Markets are hoping for a Chinese boom that simply is not coming.

Based On This Macro Outlook What Should Investors Do?

Investors should be cash-heavy and play it defensive at the beginning of the year and then switch once it becomes obvious that central banks are being forced to pivot because of a global downturn.

We like a very defensive portfolio to start the year with companies that have subdued expectations and pay good dividends to minimize the effects of a recession. We also would be looking for companies that have a lower debt position as we feel rising rates will significantly hurt some companies that have taken a debt-heavy capital structure. We don’t recommend any specific companies, but companies with profiles like the following would be companies we feel investors should look into. Companies like Walmart (WMT) and Target (TGT) in terms of the retail space, Microsoft (MSFT) and Taiwan Semiconductor (TSM) in terms of the technology space, and Merck (MRK) and Pfizer (PFE).

As for in the commodity sector, we are definitely bearish to start the year as we feel it will be difficult for commodities to rise in a recessionary environment, so while we like commodities like copper, aluminum, and natural gas in the medium-to-long term, we would avoid them to begin the year as inventories are rising and there is a very weak fundamental case for them in a recession.

As for precious metals, we are big believers in gold (GLD) and silver (SLV) as a portfolio stable, but we feel with weak industrial demand for silver and a rising interest rate environment, gold will have a lot of competition with much higher yielding bonds, and that will be a significant headwind at the beginning of the year. Additionally, international consumer spending (China and India) will be focused on the necessities and not gold and silver.

That will all change as the economy drops and central banks realize that they will have to loosen their monetary tightening. Once the seeds of that begin, then investors will want to pivot their portfolio to commodities and more of the risk-on stocks. We would also re-enter the gold market as we expect much better prices in the low $1700s and maybe even $1600s as the value proposition becomes much better and we wouldn’t rule out a return to $2000 if central banks are forced to come back to QE if the recession spirals too quickly. We have to keep in mind that world debt levels on both the corporate and government side, are at the highest levels in history – rising rates do have the potential to cause a debt-confidence spiral and that would benefit gold.

Investors will need to stay nimble and be patient, with cash being a must to take advantage of opportunities later in the year. Commodities and precious metals will have their moment, but it will probably not be until things get a bit ugly in markets.

Be the first to comment