gremlin

Investment thesis

I recommend buying Frontier Group Holdings, Inc. (NASDAQ:ULCC). ULCC has optimized its business model for cost savings, including operating a single family of aircraft, having a fuel-efficient fleet, distributing a high percentage of its tickets directly to passengers, and outsourcing non-core functions. These strategies enable ULCC to offer competitive prices to capture share from legacy carriers.

Business overview

Frontier Airlines is an ultra-low-cost carrier (“ULCCs”). They offer service all over the USA and to several international locations in the region. Its competitive advantage in the low-fare market is bolstered by its cost-effective organizational design and strong brand recognition.

ULCCs have lower unit costs

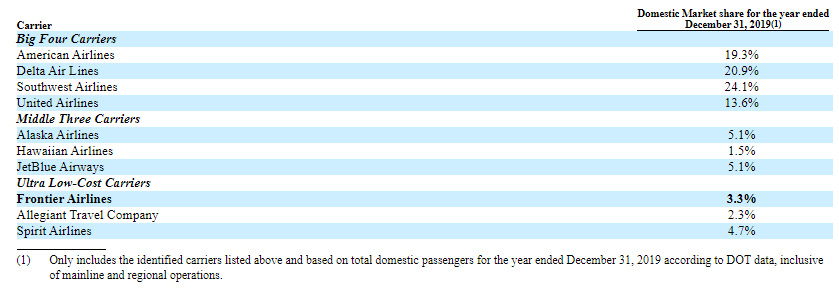

Illustrate who are the top carriers (S-1)

Most major and minor cities in the United States and abroad can be reached via regularly scheduled flights offered by the three largest legacy airlines. The “hub and spoke” network route structure is widely used by these airlines. This structure places an airline’s primary focus on a small number of hub cities, from which the airline provides either direct service to the hub’s spoke airports or connecting service to the spokes’ final destinations. One of the advantages of such an arrangement is that passengers can depart from a single airport and arrive at multiple destinations using the same airline. High fixed costs are offset by low marginal costs per additional passenger on hub-and-spoke systems. Low-cost and ultra-low-cost carriers (LCCs and ULCCs) have lower unit costs than legacy carriers because LCCs and ULCCs don’t have to pay as much for airport ground operations and maintenance facilities or provide as many gates.

Inefficient flight scheduling is a common problem for legacy network carriers because they must allow for connecting flights at hubs. This results in lower utilization and crew productivity. As a result, the scheduling, training, and maintenance of multiple aircraft types brings additional complexity and expense to the business as a whole in order to serve a wide range of markets. These factors contribute to the generally higher cost structures of legacy network carriers compared to other airlines.

ULCCs are a relatively new type of airline in the United States. Ryanair was a forerunner in Europe when it came to this type of operations management. Ryanair expanded on the model used by LCCs but put more emphasis on things like aircraft utilization, seat density, and revenue unbundling. As one might expect, ULCCs’ unit costs are significantly lower than those of legacy network carriers and LCCs, which allows ULCCs to greatly increase passenger volumes because of their low fares.

Super low-cost structure is the key advantage

ULCC has implemented several strategies to optimize its business model for cost savings. These strategies include: operating a single family of aircraft (A320), which allows for more efficient crew scheduling and training; having one of the most fuel-efficient fleets in the U.S., according to the S-1; distributing a high percentage (70+%) of its tickets directly to passengers, which reduces distribution costs; and outsourcing non-core functions such as call centers and ground handling services.

These methods enable ULCC to offer competitive prices for their services without sacrificing quality, and they also give them the freedom to adjust prices in response to fluctuations in supply and demand. Overall, the low-cost structure of ULCCs is an important strategic advantage because of their fuel-efficiency, low-cost operations, and low aircraft ownership costs.

ULCCs are able to increase ticket sales by passing on the benefits of their low-cost structure to their customers. I think a lot of people (myself included) would rather have a cheaper ticket and forego any extra perks that come with it. When taken together, these factors lead to higher aircraft utilization and a higher return on investment per plane. There is evidence that this was the case before the COVID-19 pandemic. Over the course of FY19, ULCCs flew their planes for a mean of 12.2 hours per day. According to the S-1, this is better than the Big Four’s daily average of 10.4 hours of mainline utilization.

This business requires a high degree of execution

For the ULCC method to work, the airport footprint and flight path must be meticulously planned. It is crucial to do this in order to determine which routes should be prioritized in order to maximize profits and which new routes should be prioritized in order to generate demand. This tactic helps ULCC improve utilization and lessen revenue fluctuations throughout the year. In my opinion, this is already a significant competitive advantage because it necessitates exceptional skill in execution. In order for it to work, there are a few prerequisites:

- A wide geographic reach, which allows it to serve a variety of visual flight routes and vacation destinations.

- A strong presence in both high-demand and underpenetrated markets.

- A strict approach to selecting and cutting underperforming routes.

- A highly flexible operating platform that can easily adapt to changes in flight schedules and forecasts.

The fourth issue is the most challenging for any new ULCCs to solve, in my opinion. Due to the nature of the target market’s price sensitivity and high standards for service quality, this business requires a high degree of execution. Everyone knows it’s a “budget” flight, but if there’s even a single problem with the service (like a flight delay), it will hurt the company’s image. Here is an example of Scoot facing the wrath of a passenger.

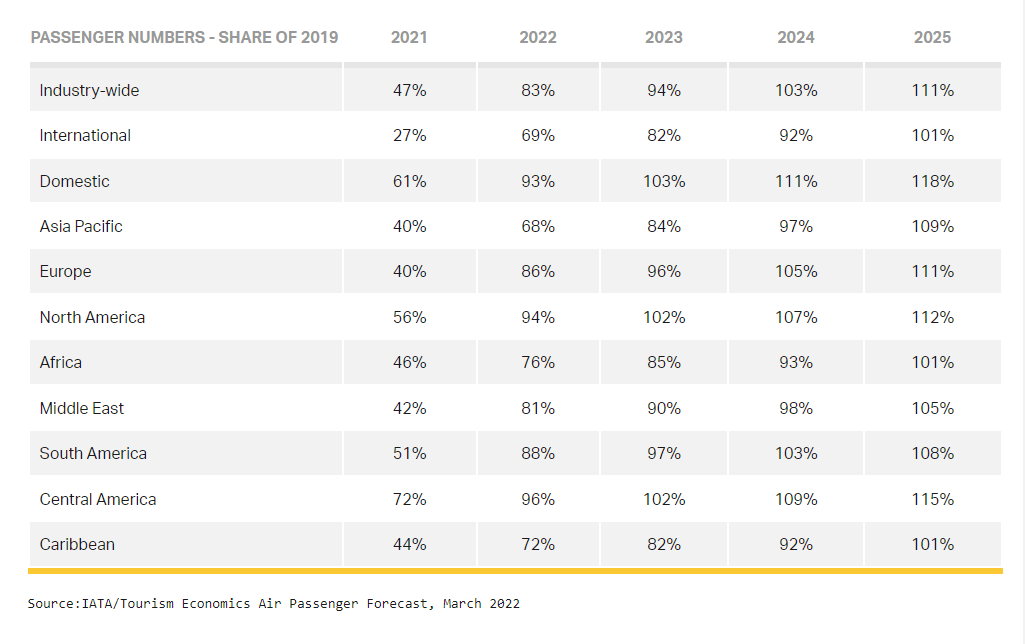

Domestic flight has mostly recovered from COVID

It looks like everyone can take to the skies again now that China has opened its borders. It is good news for ULCCs and the industry as a whole that the International Air Transport Association predicts that North American flight levels will exceed 2019 levels by 2023.

IATA

This is consistent with the forecast made by management at the company’s Investor Day on November 15, 2022. Management has reiterated their outlook for 4Q22 (pre-tax margin of 3% to 7%) and provided a roadmap to low double-digit pre-tax margins by 2H23, bringing the company back to its historical norms. Management also anticipates an annualized pretax profit of $3 million per aircraft by the second half of 2023, based on a load factor of 86% and ancillary revenue of $85 per passenger by the fourth quarter of that year.

There is likely more room for improvement in profit per passenger as a result of increased ancillary spending. During the Investor Day, ULCC shared that they plan to earn $100 in ancillary revenue from each passenger by 2026. Growth in ancillary revenues is anticipated to be driven by increased seat pricing, the introduction of new products, etc.

Pilot hires remain an issue, but management is working on it

I agree with management that the regional jet market has suffered because of the persistent domestic pilot shortage. ULCC is not spared as well. They have been facing persistent staffing challenges, but upper management has assured that certain idiosyncratic qualities will help the company get pass this. I guess this does give me some level of confidence.

To address this, ULCC has taken the reins on pilot hiring by moving to managed recruiting channels. About 89% of new hires in the second half of 2022 will come from direct hires or Australian E-3 visa holders, while the remaining 11% will come from programs managed by ULCC. However, half of ULCC’s pilots will come from Frontier-managed programs by the second half of 2023, while the other half will be direct hires and E-3 visa holders. In 2024, Frontier plans to have 25% of its employees come from direct hires, 25% from E-3s, and 75% from managed programs.

Valuation

Suppose everything is smooth-sailing, air travel recovers, fuel prices do not surge to new crazy high levels due to the Ukraine conflict, and no more pilot shortages. I believe there is significant upside to ULCC stock.

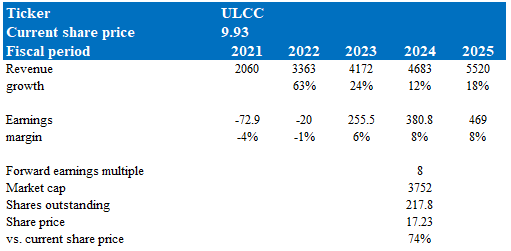

My model suggests ULCC could be worth 74% more than it is today, if it trades at 8x forward earnings multiple in FY24.

Model walkthrough:

- Revenue to continue experiencing recovery-like growth rates (high 20s in FY23), followed by historical-like growth rates underpinned by share gains

- ULCC to trade at a forward earnings multiple of 8x earnings in FY24, which is where it is trading at today. There is a possibility that ULCC trades at the same level as Spirit Airlines, Inc. (SAVE), which could serve further upsides.

Own calculations

Risk

Further surge in fuel prices

If a higher fuel price environment emerges, it may be more challenging to raise prices, as leisure travelers are much more price conscious. Similarly, the demand for leisure travel is higher on a normal basis, regardless of economic conditions. Air travel demand may decrease if consumers’ spending habits weaken, especially among middle-class families in the United States.

Conclusion

Overall, the buy case for Frontier Airlines is based on its status as a ULCC with a strong competitive advantage in the low-fare market due to its cost-effective business model. This low-cost strategy should enable Frontier Group Holdings, Inc. to capture share from legacy carriers that are not able to capture price-sensitive passengers.

Be the first to comment