coldsnowstorm/iStock Unreleased via Getty Images

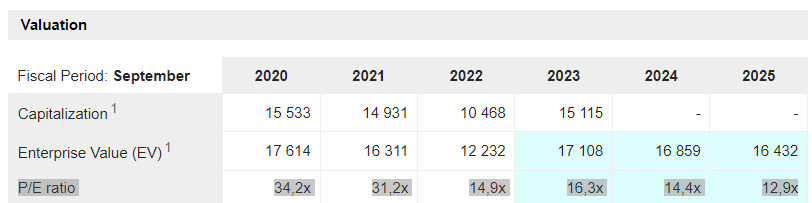

Associated British Foods (OTCPK:ASBFY), a diversified international food, ingredients, and retail group, posted a surprisingly strong Q1 2023 trading update on positive like-for-like revenue growth and an acceleration in new space growth. Despite the better-than-expected result at the retail (i.e., Primark) and ingredients segments, management left FY23 guidance unchanged, likely accounting for drought-related UK sugar crop headwinds. Yet, with commentary also calling for “encouraging” trading so far in 2023 and cost inflation headwinds for Primark and the food business beginning to fade, the guide could prove conservative heading into the H1 2023 pre-close later this month. While the stock has risen double-digits % this year, outperforming its UK retail peers, the ~14x fwd P/E valuation isn’t undemanding for a business growing in the high-teens % (FX-neutral). Backed by a strong balance sheet as well, the well-covered buyback should continue to re-rate the stock higher, unwinding the elevated short interest.

Marketscreener

Strong Q1 Update on Robust Primark UK/European Sales and New Space Expansion

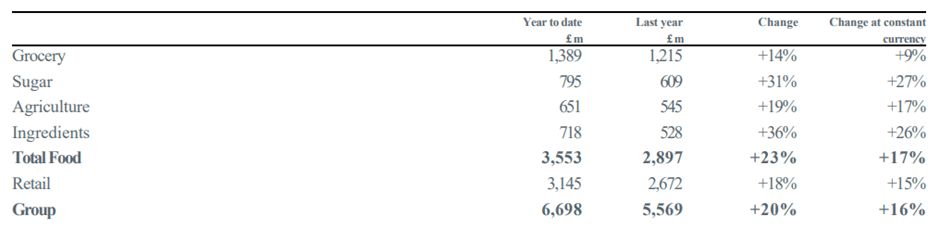

The key highlight from Associated British Foods’ latest trading update was Primark, which had an impressive run in the 16 weeks ending January 7, with sales up 18% YoY (15% in constant currency terms). The reason for this success? Strong like-for-like sales growth of 11% on higher volumes and average selling prices that exceeded management expectations across all markets. The performance in the UK was a particular surprise – sales rose by 15% (mostly like-for-like growth), driving an incremental 50bps market share gain (including online) for Primark to 7%. Even if the YoY comparison was favorable (Omicron impacted last year’s numbers), the pace of growth in the face of a challenging consumer backdrop this year has been impressive. Elsewhere, growth in Europe was similarly strong at +16% (+8% like-for-like), while sales in the US were up a slower 4% on resilient comparable sales growth and new store openings.

Associated British Foods

Supported by continued like-for-like sales strength in the first few weeks of 2023 (cited as “encouraging” by management), Primark has a clear runway to expand its store base. Management seems to agree, citing strong footfall across all store types, as they added an impressive 0.7m square feet of new trading space (+4.1% YoY), bringing trading space up to a total of 17.7m of square footage. Building on the 0.4m square feet added across ten new stores in Q1 2023, primarily in Europe, Primark is now targeting a net ~1m square feet of new space for FY23, along with 17 new stores (seven in the US, the rest in Europe). If the strong productivity levels of the twelve new store openings in the past twelve months are anything to go by, further store/space expansion should yield more share gains going forward.

FY23 Guidance Unchanged on Sugar Concerns, Potentially Conservative

Despite the impressive +20% YoY overall sales growth (+16% YoY in constant currency), management is sticking to its original FY23 guidance. The main drag is from anticipated sugar crop headwinds in the UK, which has driven flat YoY growth expectations for the sugar segment (down from +25% prior). On the other hand, continued trading strength in the ingredients and retail segments should balance this out; thus far, both businesses have navigated the inflationary headwinds well – on the cost side and the hit to customers’ disposable incomes. Management’s decision to factor in these risks, along with additional headwinds from a stronger USD and higher freight/energy costs in the FY23 adj EBIT margin guidance, seems conservative in light of the easing of these pressures in recent months. Relative to the unchanged “below 8%” margin guide, further P&L momentum, particularly from Primark, presents upside risk heading into the H1 2023 pre-close scheduled for February 27.

Expanded Buyback Offers Support

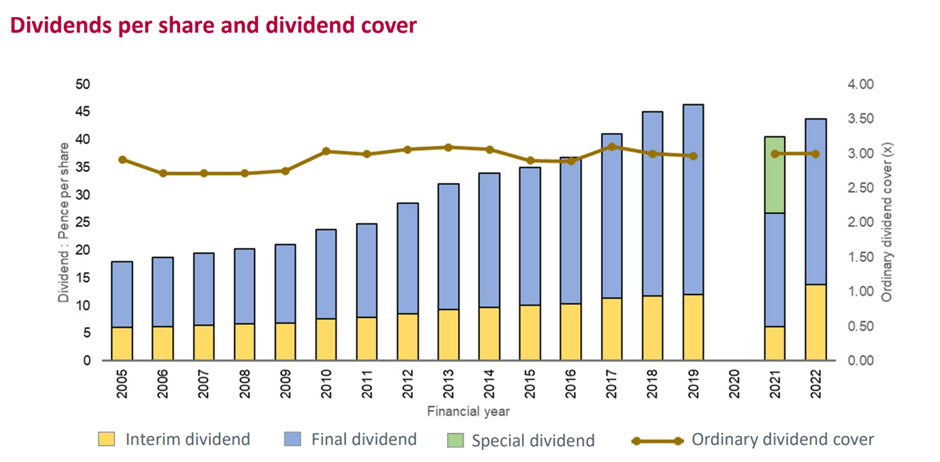

In the meantime, the capital return plan remains intact. Recall that the company last announced a GBP500m buyback (~5% of the market cap at the time of announcement) to be completed in FY23. While some form of cash return had been anticipated by the market prior to the announcement, the commitment to a buyback sends a positive message about the undervaluation of the stock. Note that the dividend will not be impacted – the announced GBP0.437/share for FY22 is well-covered, comprising a special dividend of GBP0.138/share and a GBP0.205/share final dividend (in line with last year).

Associated British Foods

From here, the positive outlook for the company bodes well for more capital return. In addition to the long-term compounding potential of Primark as it rolls out new stores outside of the UK, the retailer also stands to benefit from consumers trading down amid the ongoing cost-of-living pressures. Elsewhere, the diversified food business should also see margin tailwinds as commodity prices normalize lower, freeing up capacity for higher shareholder returns ahead.

Q1 Trading Update Defies Expectations

Associated British Foods had a great start to the fiscal year with a better-than-expected Q1 trading update thanks to rising like-for-like sales and square footage growth. Despite this, the company’s guidance for the full fiscal year remains the same, with lower profits from the sugar segment (due to expectations for a reduced UK sugar crop) offsetting positive results from Primark and the ingredients segment. This could prove conservative, in my view, as cost inflation continues to decelerate, potentially boosting food margins and the purchasing power of customers in the coming months. With the pace of store openings also accelerating as the store base extends further beyond the UK, the compounding potential is very much intact. A lot of the positives have likely been priced in with the stock up double-digits % YTD, but at ~14x fwd earnings (vs. high-teens growth) and a GBP500m buyback unfolding, the rally still has legs heading into the H1 2023 pre-close on February 27, 2023.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment