Associated Banc-Corp.’s (NYSE:ASB) earnings are expected to decline this year mostly due to the 50bps Fed rate cut that will squeeze margin. Further pressure is expected to come from higher provisions in the wake of turmoil in the international crude oil market. Despite management’s efforts to reduce exposure to the oil and gas sector, ASB still has a significant amount of loans related to the sector in its books that could hurt earnings this year. As a result, I’m expecting the company’s earnings to decline by a double-digit rate in 2020. Due to the recent market rout, ASB’s current market price is at a significant discount to the estimated December 2020 target price. While the outlook for return till the end of year is promising, the outlook is less bright for the short term of around three months. The exponential spread of COVID-19 and sharp decline in crude oil prices have created risks that I believe will keep ASB’s market price depressed for the near term. Hence, I’m adopting a neutral rating on the stock.

Provisions Charge to Drag Earnings

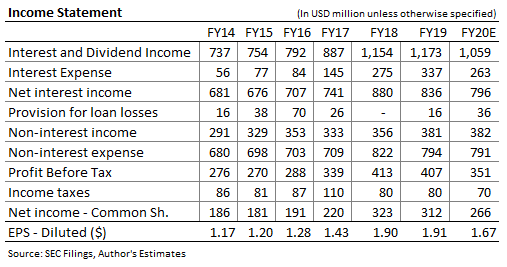

During 2019, ASB reduced the exposure of its loan book to oil and gas sector by $0.2 billion to $0.5 billion, as mentioned in the fourth quarter investor presentation. The current position in the sector is still high enough to cause some troubles to the bottom-line in the wake of turmoil in the international crude oil market. The failure of OPEC and its allies to reach an oil output agreement and the resultant price slash by Saudi Arabia has ignited fears that oil producers in the United States will be unable to service debt. Now that banks have switched to the expected credit loss model under CECL (accounting standard: ASU 2016-13) from the previous model based on incurred losses, the oil price decline is likely to have an almost immediate impact on provisions charge. Consequently, I’m expecting ASB’s provisions charge to surge to $36 million in 2020 from $16 million in 2019.

Asset Sensitivity to Lead to Margin Compression

Another factor that is expected to reduce earnings is net interest margin, NIM. ASB’s NIM declined by 2bps in the third quarter and 4bps in the fourth quarter of 2019 due to the 75bps Fed funds rate cut. The response of NIM to interest rate changes in the last two quarters shows that the balance sheet’s asset sensitivity is quite low. Going forward, the sensitivity is expected to continue to remain low as the deposit mix continues to be in a favorable position. As at the end of December 2019, non-interest bearing deposits made up 22.9% of total deposits, as opposed to 22.5% at the end of September 2019 and 22.9% at the end of December 2018. My estimates for yield, cost, and NIM are presented below.

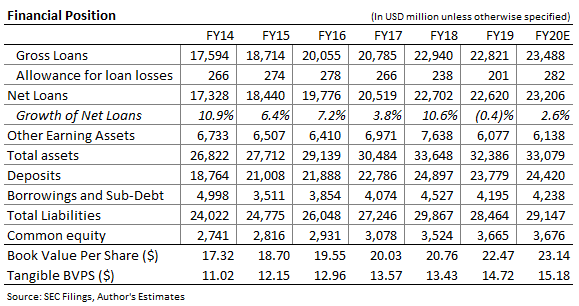

Part of the hit from NIM compression is expected to be offset by an expansion in the loan portfolio. As mentioned in the fourth quarter conference call, the management is optimistic about loan growth especially in the commercial real estate segment. The management expects total loans to grow in the range of 2% to 4%. Due to certain headwinds, I believe it is best to assume that net loans will grow at the lower end of management’s guided range. These headwinds include the COVID-19 outbreak and political uncertainty ahead of the presidential elections. The oil price slash will also discourage oil and gas producers in the United States to borrow for capital expenditure. As a result, I’m expecting ASB’s net loans to grow by a rate of 2.6%, which is at the lower end of the management’s guided range. The following table presents my estimates for key balance sheet items.

The combined effect of NIM compression and loan growth is expected to result in net interest income decline of 4.7% year over year in 2020.

Earnings Likely to Decline by Double-Digit Rate

Due to the expected increase in provisions charge and reduction in net interest income, ASB’s net income is likely to trend downwards this year. Some relief is expected from a slight reduction in non-interest expenses due to cost-control measures. Overall, I’m expecting ASB’s net income to decrease by 14.7%, and earnings per share to decrease by 12.4% to $1.67. The following table shows my estimates.

Major risks to my earnings thesis include the following:

- COVID-19. Taking guidance from similar outbreaks in the past, presently I’m expecting the epidemic to become manageable in two to three months’ time. Worsening of the epidemic beyond my expectations can lead ASB’s actual earnings in 2020 to miss my estimates. COVID-19 can impact both loan growth and net interest margin (through interest rates).

- International Crude Oil Price. I’m expecting WTI crude oil price to drift downwards and stay within a range of $27-$30 per barrel in the next six months. Decline in oil price beyond my expectation can lead to greater than anticipated provisions charge, and consequently lower net income.

High Risk in Near Term Justifies Neutral rating

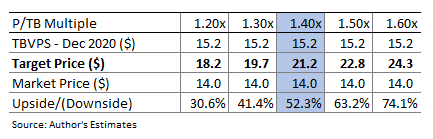

ASB has traded at an average price to tangible book ratio, P/TB, of 1.4x in 2019. Multiplying this P/B ratio with the forecast tangible book value per share of $15.2 gives a target price of $21.2 for December 2020. This target price implies an upside of 52.3% from ASB’s March 10 closing price. The following table shows sensitivity of the target price to P/B multiple.

Apart from the significant price upside, ASB also offers an attractive dividend yield of 5.2%, assuming quarterly dividend is maintained at the current level of $0.18 per share. As a result, ASB appears to be an attractive investment for a horizon of nine months or more. However, as noted above, there are high risks in the near term of three to four months. Due to COVID-19 and the uncertainty related to oil prices, it is advisable for low to medium risk-tolerant investors to stay away from the stock for now. These risks are likely to keep ASB’s market price depressed in the near term; hence, I’m adopting a neutral rating on the stock.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer: This article is not financial advice. Investors are expected to consider their investment objectives and constraints before investing in the stock(s) mentioned in the article.

Be the first to comment