Bussarin Rinchumrus/iStock via Getty Images

Aspen Technology, Inc. (NASDAQ:AZPN) has been spending a lot on sales in marketing in order to boost sales and drive growth, and has led the big surge in operating expenses, which resulted in another net loss in the last earnings report, even after the big S&M spend.

While the company has increased its average contract value and overall revenue, it continues to struggle to generate a profit, as expenses continue to climb.

A moat it has that has helped it retain over 95 percent of its customers is a strong one because of switching costs, but it’s one that could come under some pressure if some of its customers and potential customers decide to compete on price or decide to delay spend until economic conditions improve and there’s more clarity for the purposes of decision making.

Based upon company guidance and expense numbers, I think the company could come under more pressure in calendar 2023 if the economy gets worse and top managements makes decisions concerning prioritizing spend.

In this article we’ll look at its recent numbers, including a focus on expenses, why expenses are liable to continue to weigh on the company, and how the next year could unfold for AZPN.

Latest numbers

Revenue in the first fiscal quarter of 2023 was $250.8 million, compared to $77 million in the first fiscal quarter of 2022.

Operating expenses soared to $210.9 million in the reporting period, and including cost of revenue, total expenses jumped to $302 million, resulting an operating loss of $(51.2) million.

Non-GAAP operating income in the quarter was $92.6 million, which reflected non-GAAP operating margin of 36.9 percent. Non-GAAP net income was $142 million or $2.20 per share.

Investor Presentation

Net loss in the quarter was $(11.2) million, or $(0.17) per share. The company attributed that to a non-cash expense associated with “the mark-to-market adjustment for an Australia dollar foreign currency derivative related to the announced Micromine acquisition.” Until the deal closes that’s expected to fluctuate.

While the adjustment definitely had an impact on the numbers for AZPN, I don’t think it was the only factor. With sales and marketing expenses up between four and five times was it was in the first fiscal quarter of 2022; I see that as having a strong impact on earnings in the reporting period.

The company had free cash flow of $10.7 million in the quarter.

Cash and cash equivalents at the end of the first fiscal quarter were $382 million, compared to cash and cash equivalents of $449.7 million at the end of the first fiscal quarter of 2022. The company had $270 million remaining under its credit facility.

Guidance on expense

I think expenses are really the key metric to watch with AZPN, and in that category the company is facing significant challenges.

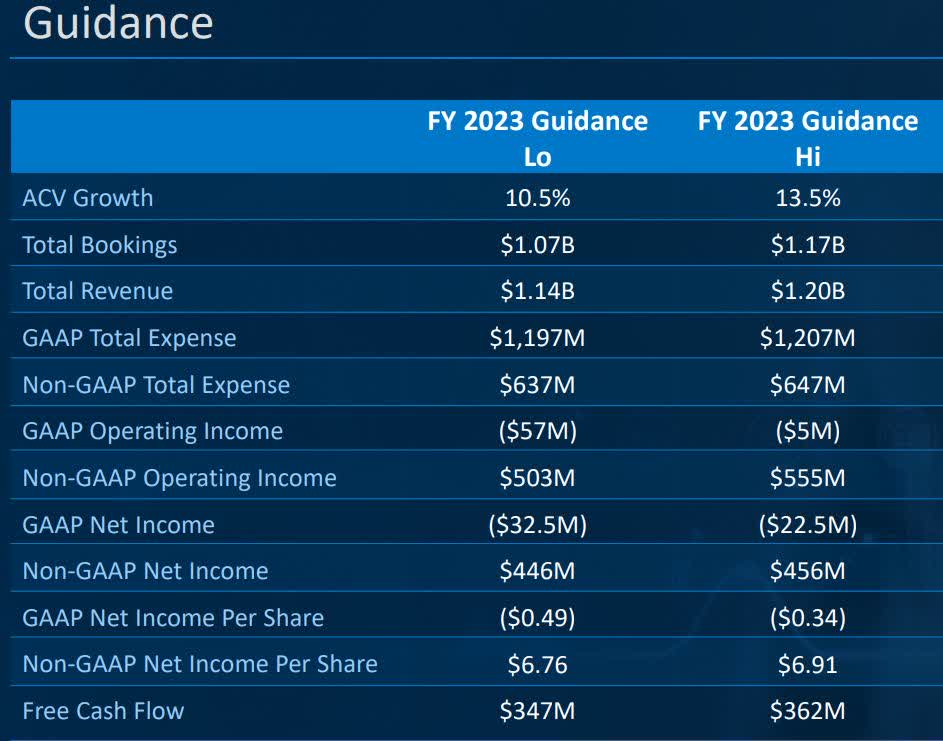

Guiding for fiscal full-year 2023, total GAAP expenses are projected to be in a range of $1.197 billion to $1.207 billion.

That is expected to generate a GAAP operating loss of $(5) million to $(57) million for fiscal 2023. Net loss on a GAAP basis is projected to be in a range of $(32.5) million to $(22.5) million.

GAAP net loss per share is guided to be in a range of $(0.34) to $(0.49).

Investor Presentation

One positive from guidance is the company expects free cash flow to being in a range of $347 million to $362 million. Further out, the company believes it has $110 million of adjusted EBITDA synergy by 2026. Management said its guidance included the variety of potential outcomes that could emerge from uncertainty in the macro-economic environment in calendar 2023.

One final observation I want to make on the expense side of things is concerning S&M in the first fiscal quarter. It jumped to $118.3 million, which obviously contributed to the overall revenue gain in the reporting period of $250.8 million. That compares with S&M spend of $25 million in the first fiscal quarter of 2022, which produced revenue of $77 million.

My point here is, based upon percentages, the return from S&M spend as it relates to revenue contrast, was much less in the first fiscal quarter of 2023 than it was the prior year. If that were to continue, the guidance concerning expense and the losses associated with it could be more than anticipated, even more so if the economy gets worse than expected.

I understand that there is a high switching cost in the sector AZPN competes in, not simply in capital, but in integration as well. That’s why the customer retention rate of Aspen Software stands at over 95 percent. I’ve seen this with other specialized software companies, and the same competitive advantage remains in place once the company gets its foot in the door.

The place I see some vulnerability here is in regard to renewals; specifically, if some of its competitors start competing on price if the economy falls off the cliff. Under that scenario the company may have to ramp up S&M in order to maintain its customer retention rate, which would put further pressure on the bottom line.

Conclusion

AZPN competes in a sector that includes high switching costs that provide a moat that results in support to its top line in regard to its existing customer base.

On the other hand, the company has been spending a lot on sales and market and acquisitions, which when combined with other costs, had resulted in ongoing losses for the company.

Taking that into consideration, it’s difficult to see what the turning point for the company will be in regard to sustainable profitability. It’s been spending a lot of capital for the purpose of growing revenue, but it isn’t producing results that are conducive to its bottom line. While the company has been on a nice run since March 23, 2020, when it traded at $72.00 per share, jumping by between 4x and 5x on October 3, 2022, when it hit its 52-week high of $263.59, it has since pulled back to trade a little above $200.00 per share as I write.

TradingView

Based upon its revenue gains and increasing expenses and losses, I think the company is likely to trade level or mixed in the quarters ahead, possibly entering into a period of volatility.

And if renewals in any way disappoint or rising expenditures don’t achieve the desired revenue and earnings results, the stock price would probably take a significant and sustainable dip until there’s more clarity concerning the economy and the company improves its bottom line.

Be the first to comment