Maikel de Vaan/iStock Editorial via Getty Images

Introduction

ASML (NASDAQ:ASML) was officially formed in 1984 when Philips spun out their internal lithography division. Unlike Japanese companies such as Nikon and Canon who historically built components in-house, ASML had a better model sourcing components from suppliers around the world per the Chip War book by Chris Miller. Being located in the Netherlands, ASML was historically advantaged when there were trade disputes between Japan and the US.

Today ASML is the only company in the world that makes Extreme Ultraviolet (“EUV”) tools and they are in high demand from key customers like Taiwan Semiconductor (TSM) and Samsung (OTCPK:SSNLF). My thesis is that ASML will continue to grow prodigiously as the world relies on their equipment in order to make high-end chips.

At the time of this writing, €100 is equal to about $109.

Customer Demand

Per comments in the November 2022 Investor Day presentation, if we have a recession coming then there is a strong possibility that its length will be less than the lead time of ASML’s tools. As such, the plan is for 60 EUVs to be produced in 2023. If some customers push machines back due to recession fears, then there are other customers with more flexible financial situations and different time horizons that will step in and take those machines.

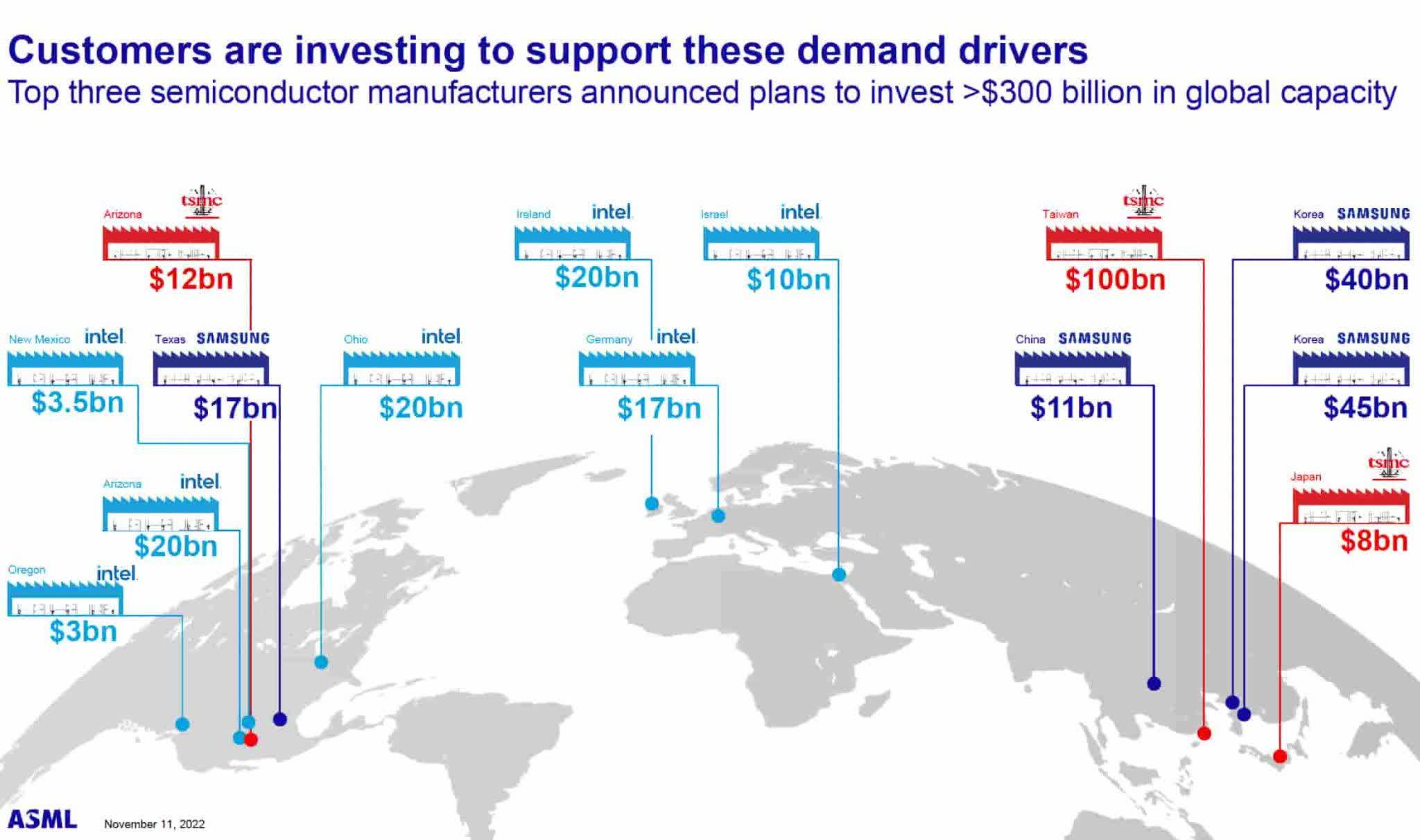

The November 2022 Investor Day presentation by CEO Peter Wennink shows that the top three semiconductor manufacturers are making heavy investments around the globe to meet demand:

Customer demand (November 2022 Investor Day presentation)

Valuation

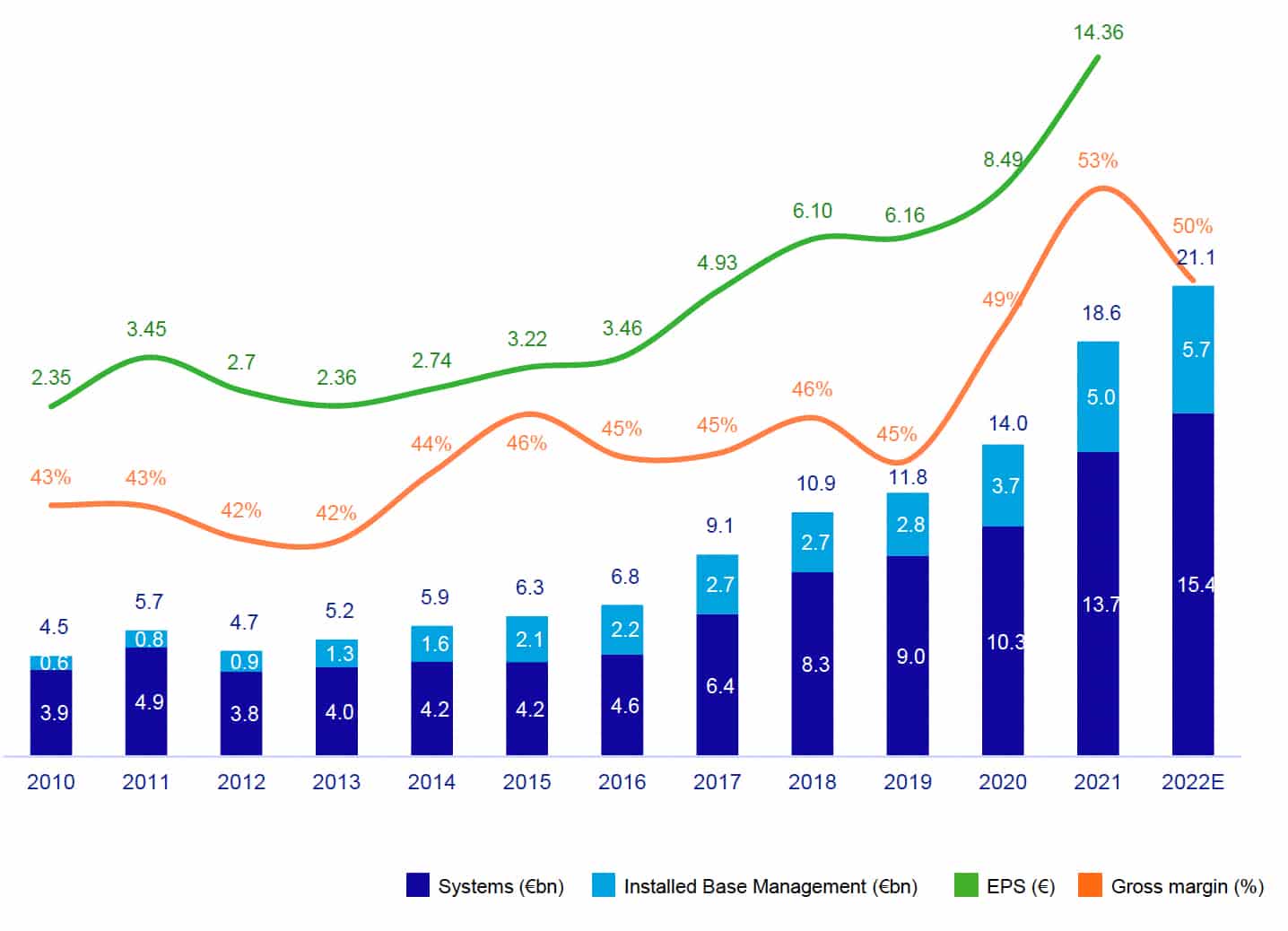

The November 2022 Investor Day presentation by CFO Roger Dassen shows that EPS has been growing at a CAGR of 18% since 2010 due to revenue growth, improving margins and buybacks. He specifies that 2% was from buybacks and the other 16% or so was from growth and margin improvements. The 4Q22 press release for quarterly and full year results came out since the time of this presentation; the 2022 EPS figure was €14.14, gross margin was 50.5%, system sales of logic and memory were €15.4 billion and installed base management sales were €5.7 billion:

EPS growth (November 2022 Investor Day presentation)

Here are financials from the 4Q22 presentation:

Financials (4Q22 presentation)

Revenue from EUV units has climbed nicely since 2016:

|

Year |

EUV Units |

EUV Total (in millions €) |

EUV Average (in millions €) |

EUV % of system sales |

|

2016 |

4 |

€331 |

€83 |

7% |

|

2017 |

11 |

€1,084 |

€99 |

17% |

|

2018 |

18 |

€1,880 |

€104 |

23% |

|

2019 |

26 |

€2,800 |

€108 |

31% |

|

2020 |

31 |

€4,464 |

€144 |

43% |

|

2021 |

42 |

€6,284 |

€150 |

46% |

|

2022 |

40 |

€7,000 |

€175 |

45% |

*60 EUVs are expected to be produced in 2023.

We need to go over the history and business model of ASML in order to think about their future and their valuation. They don’t face any competition with respect to EUV tools and it is crucial to understand how this came about in order to predict how long they will be in this position. The Chip War book explains that ASML got an opportunity when Intel didn’t want to produce EUV tools:

Intel’s goal was “to make stuff, not just to measure it,” Carruthers explained, so the company began searching for a company to commercialize and mass-produce EUV tools. It concluded no American firm could do it. GCA was no more. America’s biggest remaining lithography firm was Silicon Valley Group (SVG), which lagged technologically. The U.S. government, still sensitive from the trade wars of the 1980s, didn’t want Japan’s Nikon and Canon to work with the national labs, though Nikon itself didn’t think EUV technology would work. ASML was the only lithography firm left.

[Kindle Location: 2,549]

The Chip War book goes on to say that Nikon and Canon did not opt to build EUV tools as they were locked out of the research from national US labs. Frits van Houts started leading ASML’s EUV business in 2013 and he considered supply chain management to be paramount as ASML only made about 15% of the EUV components at that time. ASML acquired Cymer in 2013 and they rely heavily on this subsidiary for the light sources in the EUV tools.

At some point a competitor in China might emerge with the ability to make EUV tools but there are many hurdles. The Chip War book explains that just the laser alone in the EUV system requires 457,329 parts to be assembled together perfectly. And the machines are always changing per the Chip War book:

Perhaps in a decade China can succeed in building its own EUV scanner. If so, the program will cost tens of billions of dollars, but – in a revelation that is bound to be discouraging – when it’s ready it will no longer be cutting edge. By that time, ASML will have introduced a new generation tool, called high-aperture EUV, which is scheduled to be ready in the mid-2020s and cost $300 million per machine, twice the cost of the first generation EUV machine. Even if a future Chinese EUV scanner works just as well as ASML’s current equipment – hard to imagine, given that the U.S. will try to restrict its ability to access components from other countries – Chinese chipmakers using this hypothetical alternative EUV machine will struggle to produce profitably with it, because by 2030, TSMC, Samsung, and Intel will have already used their own EUV scanners for a decade, during which time, they’ll have perfected their use and paid down the cost of these tools.

[Kindle Location: 4,286]

Given the considerations above, I think ASML’s top line revenue numbers and general economics from EUV machines are safe for many years to come. This is a very important point from a valuation standpoint! It is one of the main factors that gets me comfortable with higher earnings multiples.

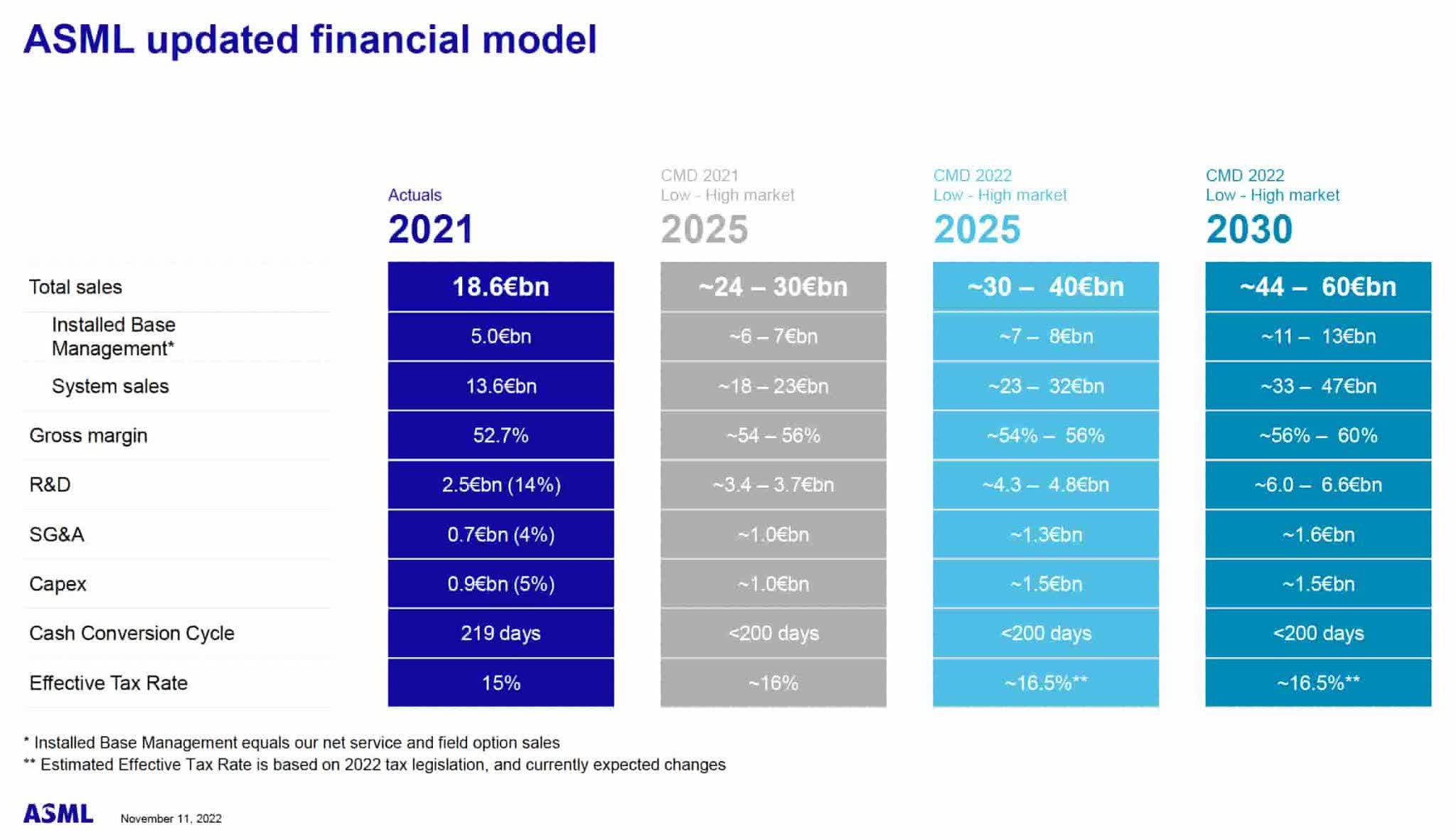

The November 2022 Investor Day presentation shows that 2025 revenue should be between €30 billion and €40 billion while 2030 revenue should be between €44 billion and €60 billion. In addition, gross margins should be higher than today’s levels:

Financial model (November 2022 Investor Day presentation)

The 4Q22 call explains that the 2022 sales figure would be much higher if we included fast shipments from early 2023:

Now for the total year, €21.2 billion in sales, of which about €3.1 billion of fast shipments went into 2023. So the net effect of the fast shipments plus the revenue of €21.2 billion would give you a normalized revenue, if you would have booked the fast shipments as revenue, of €24 billion, which is quite a significant increase as compared to last year.

The 4Q22 presentation says net sales growth for 2023 should be about 25% above 2022 and this comes to almost €26.5 billion. If this holds true and the operating margin stays at the 30.7% level that it was at in 2022, then we could have operating income of more than €8 billion in 2023.

Interest rates have gone up which means we now discount future cash flows at a higher rate such that valuation multiples have to go down. Still, I think ASML could be worth as much as 30x 2023 operating income or maybe even a little higher. This comes to about €240 billion or a little over $260 billion. This might seem a little crazy but it’s really not if 2030 revenue reaches the high end range of €60 billion with a gross margin of 60%.

The 4Q22 financials show 394.9 million basic weighted shares such that the market cap is about $270 billion based on the January 26th share price of $683.90. The enterprise value is about $4.1 billion less than the market cap due to the fact that the balance sheet shows €7,268.3 million in cash and only €3,514.2 million in long-term debt for a difference of €3,754.1 million or $4.1 billion.

Disclaimer: Any material in this article should not be relied on as a formal investment recommendation. Never buy a stock without doing your own thorough research.

Be the first to comment