1shot Production/E+ via Getty Images

A Quick Take On Park City Group

Park City Group (NASDAQ:PCYG) reported its FQ1 2023 financial results on November 14, 2022, beating revenue and meeting EPS estimates.

The firm provides various supply chain software functionalities to businesses worldwide.

Management will need to produce higher revenue growth than 4% to catch the eye of investors.

Until we begin to see that higher growth, I’m on Hold for Park City Group.

Overview

Murray, Utah-based Park City Group was founded to provide B2B supply chain software systems to organizations seeking to improve efficiencies and reduce risks in their supply chain processes and relationships.

The firm is headed by Chairman and CEO Randy Fields, who co-founded Mrs. Fields’ Cookies and developed early versions of software that were spun off into what became Park City Group.

The company’s primary offering is its ReposiTrak system, which provides the following solutions:

-

Supplier Discovery Marketplace

-

Compliance Management

-

Supply Chain Solutions

The firm acquires customers via its in-house sales and marketing teams.

Market & Competition

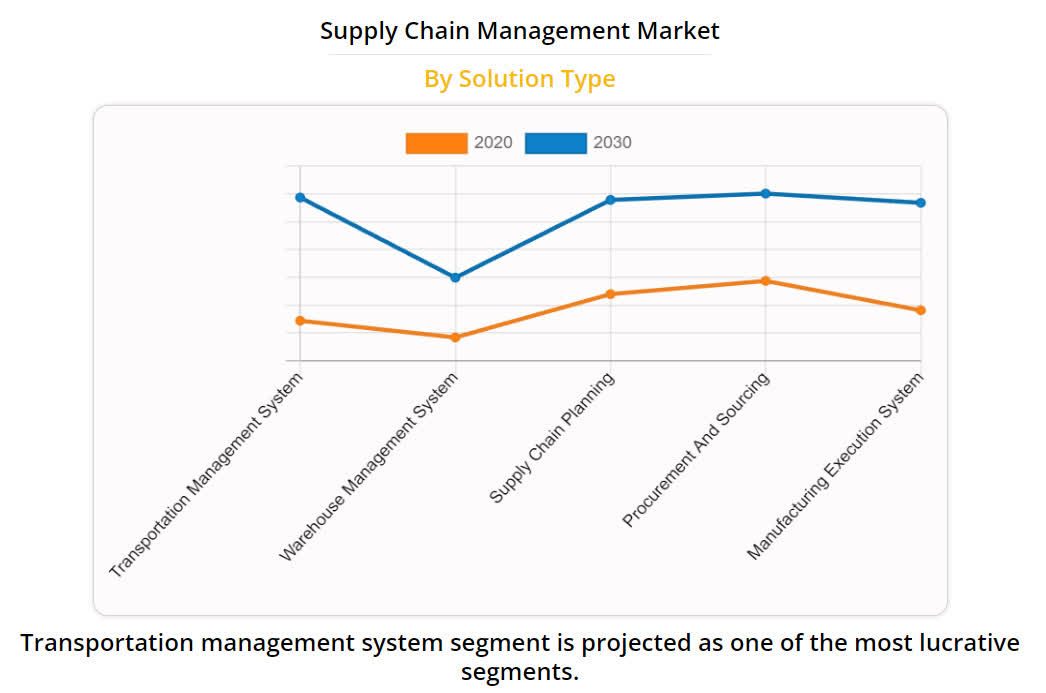

According to a 2021 market research report by Allied Market Research, the market for supply chain management software and services was an estimated $18.7 billion in 2020 and is forecast to reach $52.6 billion by 2030.

This represents a forecast CAGR of 10.7% from 2021 to 2030.

The main drivers for this expected growth are demand for increased supply chain visibility, especially after the disruptions caused by the COVID-19 pandemic.

Also, the chart below shows the supply chain management market changes between 2020 and 2030 by solution type:

Supply Chain Management Market (Allied Market Research)

Major competitive or other industry participants include:

-

Epicor Software

-

HighJump

-

Info

-

IBM

-

JDA Software Group

-

Kinaxis

-

e2open

-

Oracle

-

SAP

-

Manhattan Associates

-

Descartes Systems Group

-

Others

Recent Financial Performance

-

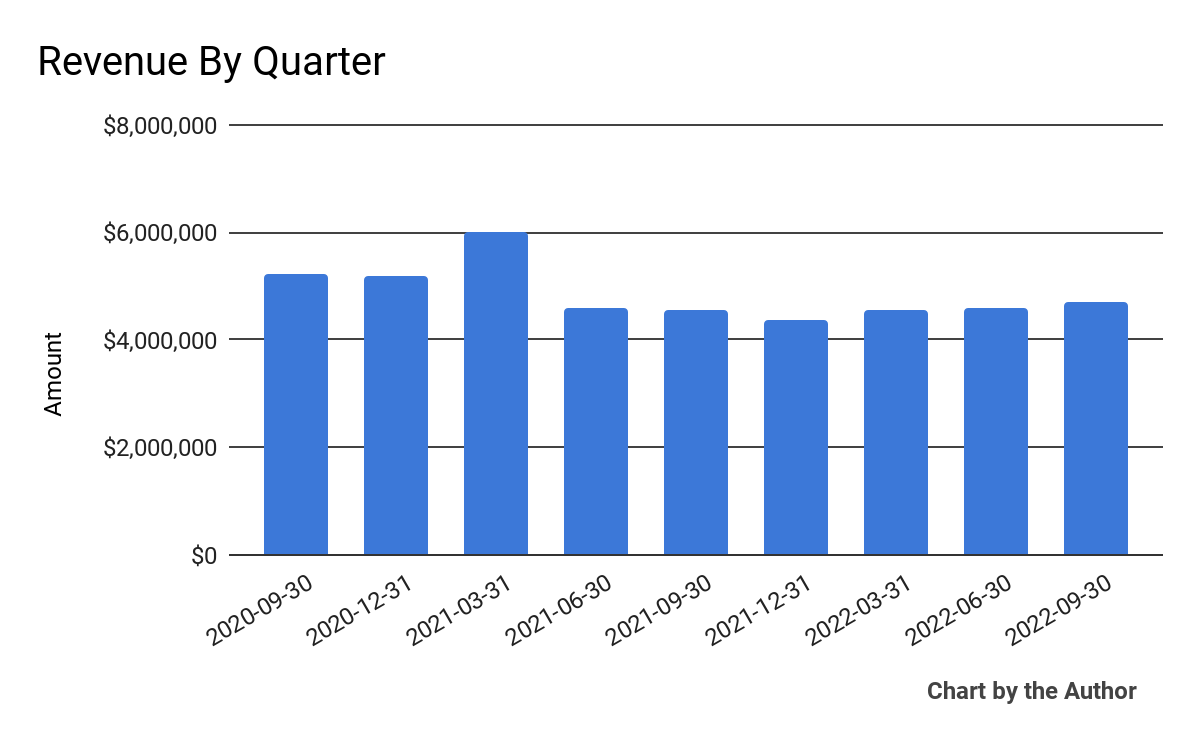

Total revenue by quarter has remained essentially flat in recent quarters, per the chart below:

9 Quarter Total Revenue (Financial Modeling Prep)

-

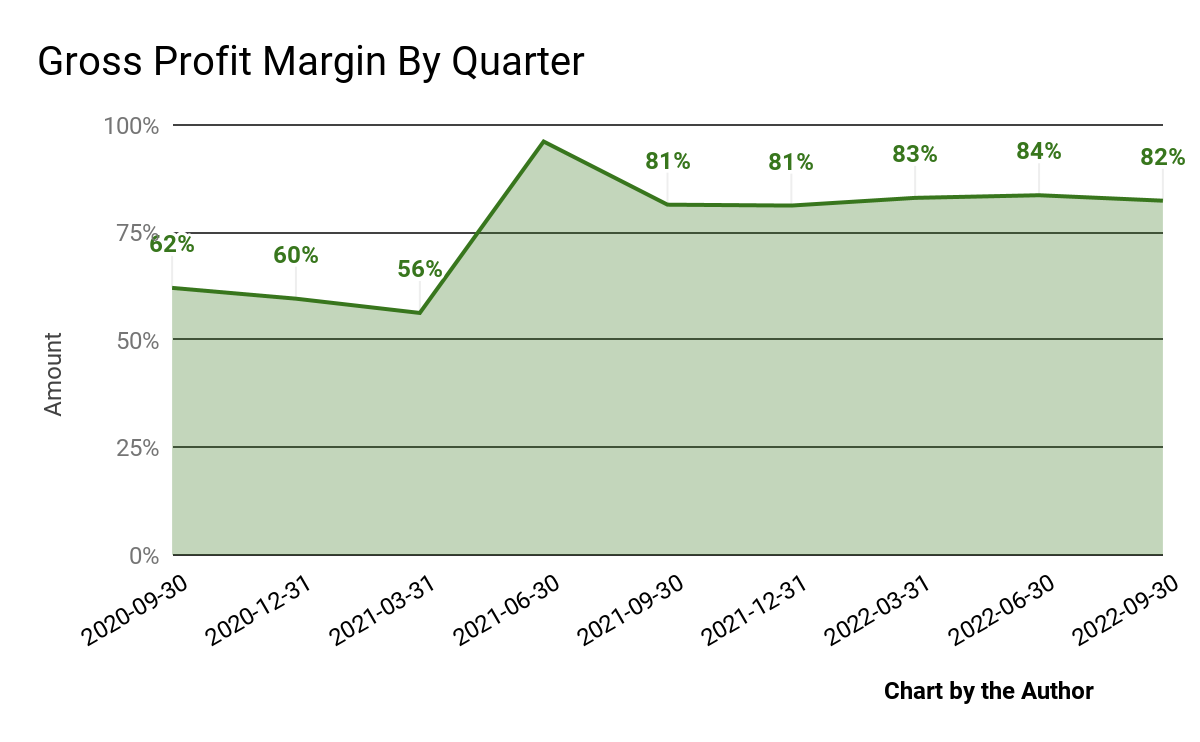

Gross profit margin by quarter has remained high in recent reporting periods:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

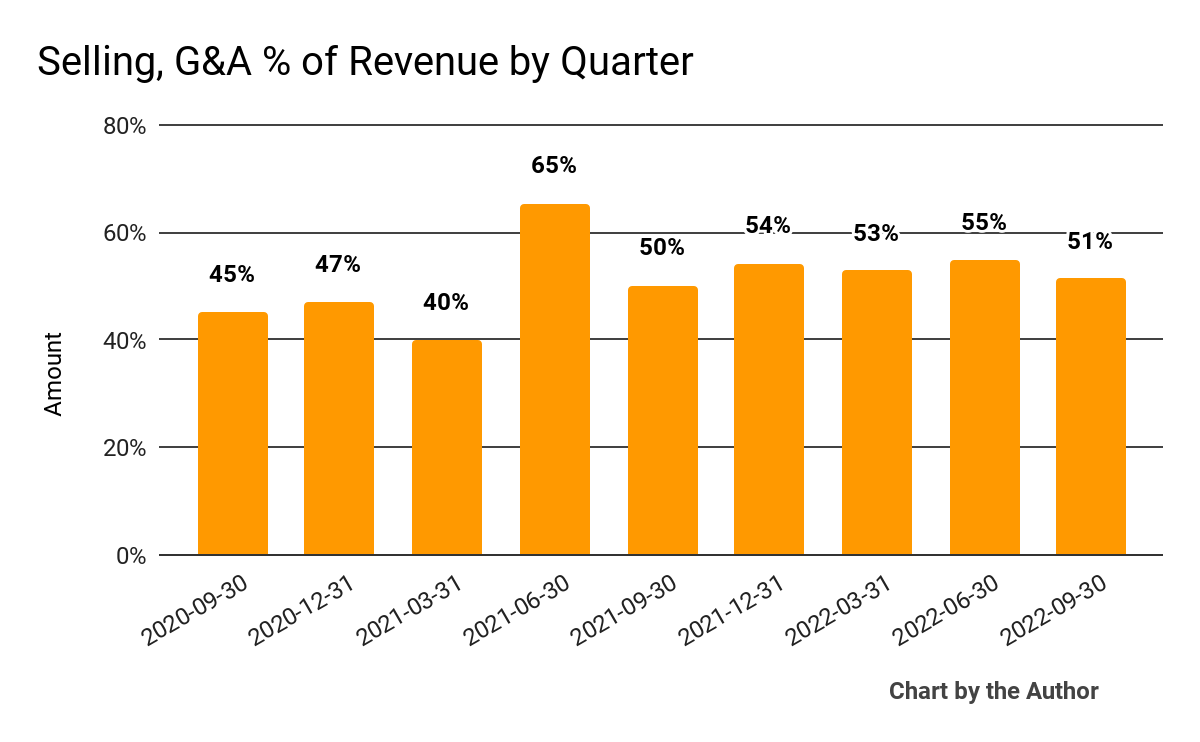

Selling, G&A expenses as a percentage of total revenue by quarter have varied within a narrow range recently:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

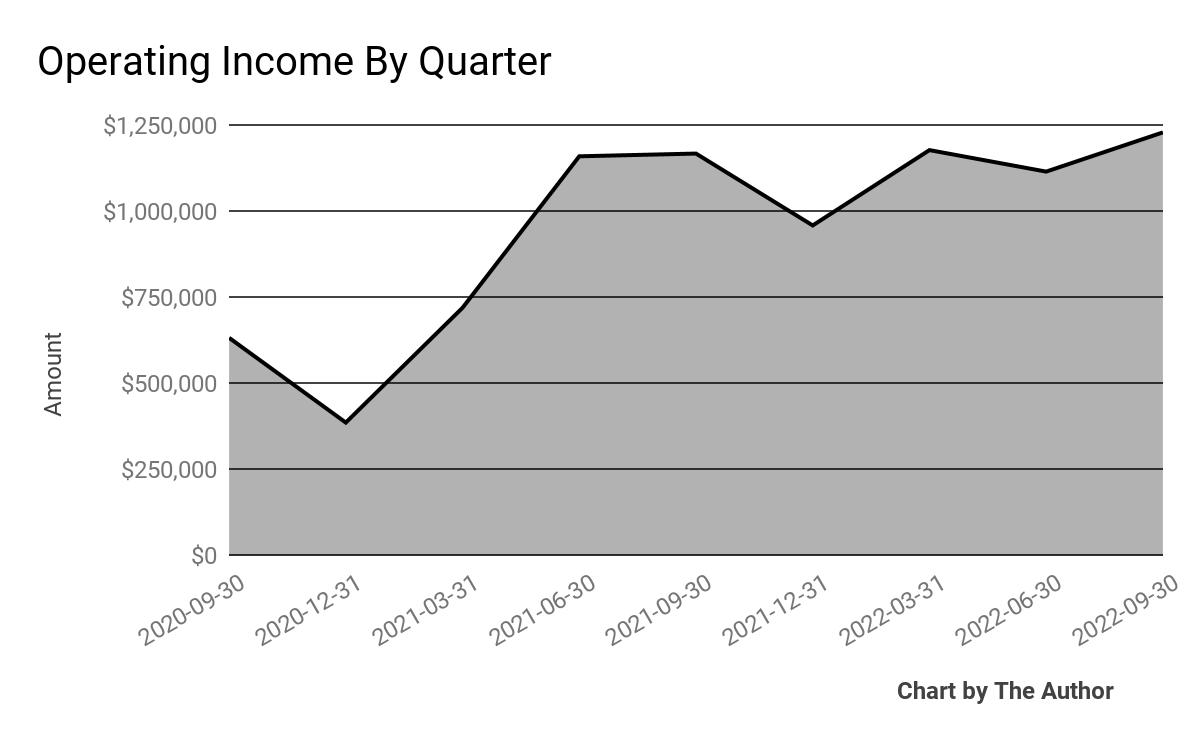

Operating income by quarter has been essentially flat in recent quarters, as shown below:

9 Quarter Operating Income (Financial Modeling Prep)

-

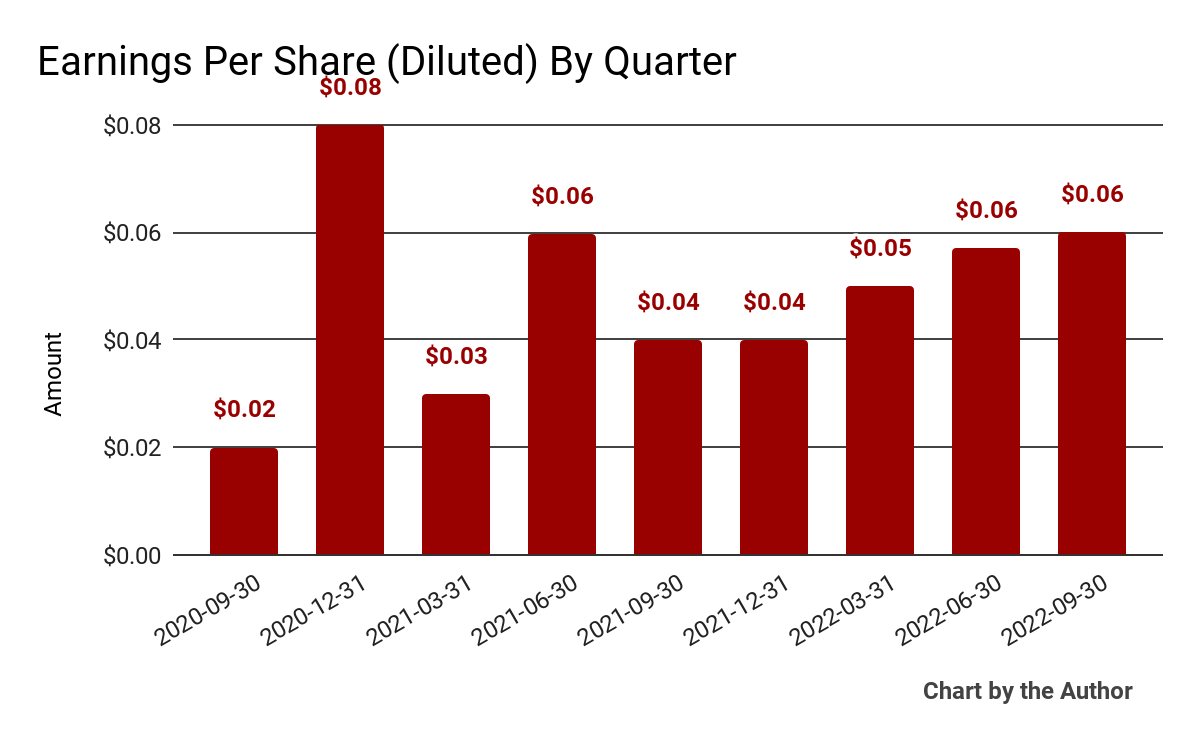

Earnings per share (Diluted) have risen in recent reporting periods:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

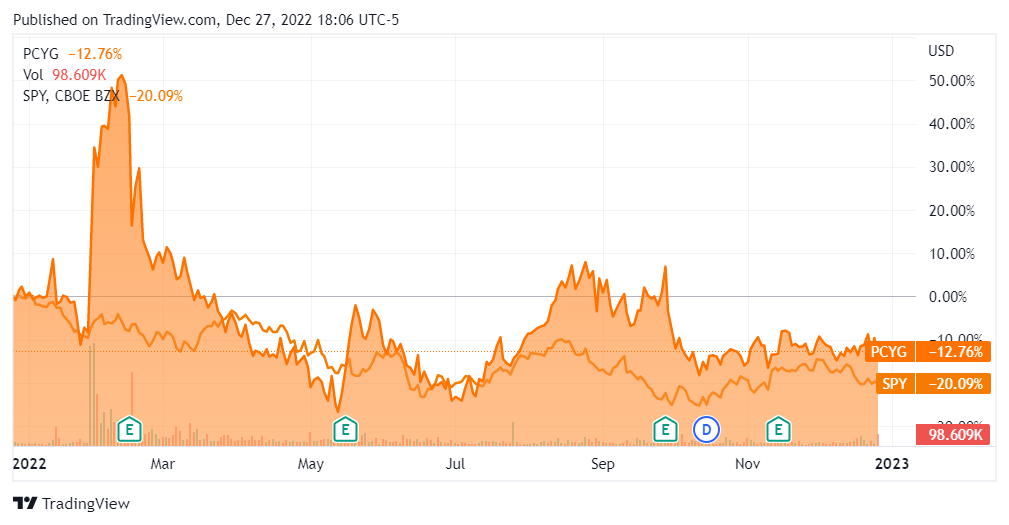

In the past 12 months, PCYG’s stock price has fallen 12.8% vs. the U.S. S&P 500 index’s drop of around 20.1%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

4.0 |

|

Enterprise Value / EBITDA |

12.6 |

|

Revenue Growth Rate |

-10.5% |

|

Net Income Margin |

23.8% |

|

GAAP EBITDA % |

32.1% |

|

Market Capitalization |

$93,107,542 |

|

Enterprise Value |

$73,713,585 |

|

Operating Cash Flow |

$7,913,092 |

|

Earnings Per Share (Fully Diluted) |

$0.21 |

(Source – Financial Modeling Prep)

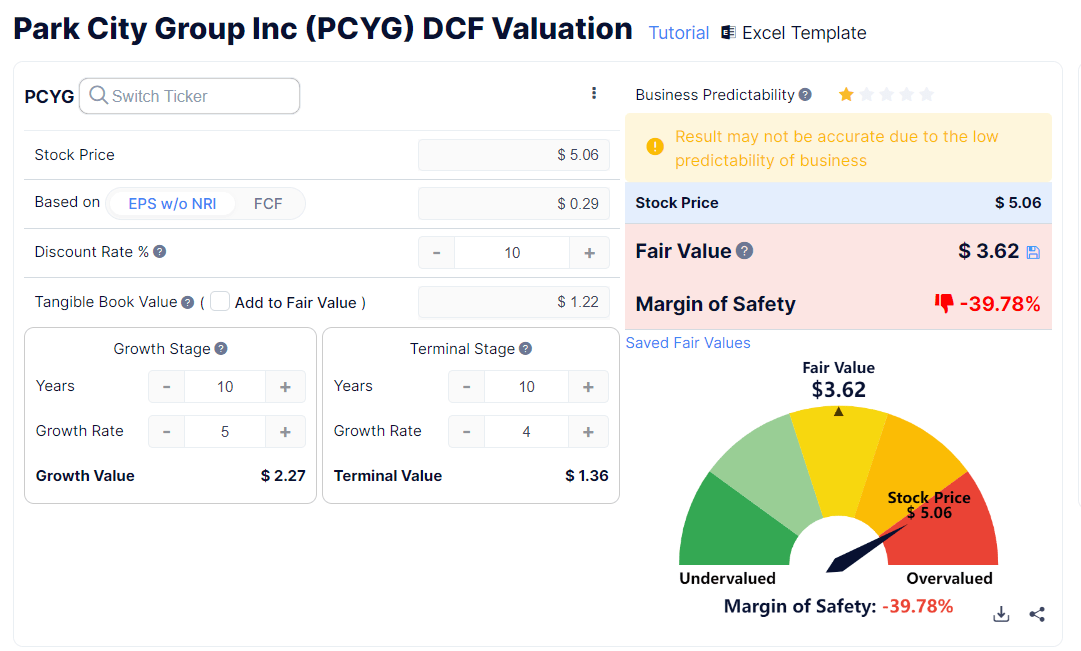

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

Discounted Cash Flow Calculation (GuruFocus)

Assuming generous DCF parameters, the firm’s shares would be valued at approximately $3.62 versus the current price of $5.06, indicating they are potentially currently overvalued, with the given earnings, growth, and discount rate assumptions of the DCF.

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

PCYG’s most recent GAAP Rule of 40 calculation was 21.6% as of FQ1 2022, so the firm needs improvement in this regard, per the table below:

|

Rule of 40 – GAAP [TTM] |

Calculation |

|

Recent Rev. Growth % |

-10.5% |

|

GAAP EBITDA % |

32.1% |

|

Total |

21.6% |

(Source – Financial Modeling Prep)

Commentary On Park City Group

In its last earnings call (Source – Seeking Alpha), covering FQ1 2023’s results, management highlighted the final Track & Trace rule from the FDA, called Rule 204.

Leadership believes this regulatory clarity will provide companies with the information and compliance push they need to intensify their food safety supply chain efforts.

The firm believes that large retailers and wholesalers will be the earliest adopters of Rule 204 requirements and that the company’s ‘universal translator’ approach to making sense of supply chain data will position it for future growth.

As to its financial results, total revenue rose only 4% year-over-year, while grew slightly, to a high 82%.

Management did not disclose any customer or revenue retention rate information.

The company’s Rule of 40 results have been in need of improvement, with a drop in revenue offset by positive GAAP EBITDA.

Gross profit margin edged slightly higher year-over-year, as did operating income. Earnings per share rose by 50% year-over-year.

For the balance sheet, the firm finished the quarter with $21.6 million in cash and equivalents and $1.4 million in total debt.

Over the trailing twelve months, free cash flow was $6.7 million, of which capital expenditures accounted for $100,000 in cash used.

Looking ahead, the firm has begun paying a quarterly dividend, with a current forward yield of approximately 1.19%.

Management believes it can produce moderate revenue growth but stronger earnings growth due to operating leverage and efficiencies.

Regarding valuation, the market is valuing PCYG at an EV/Sales multiple of around 4.0x.

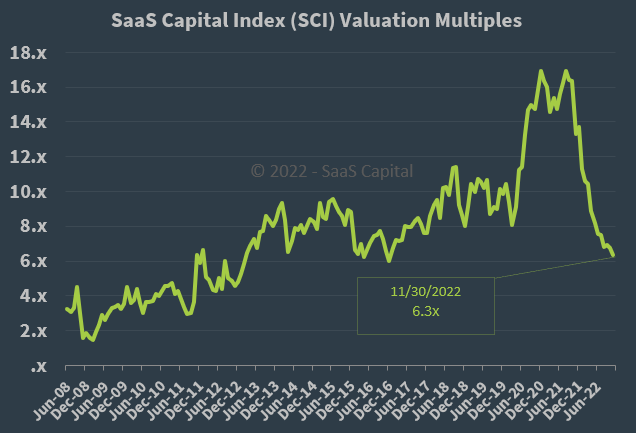

The SaaS Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 6.3x on November 30, 2022, as the chart shows here:

SaaS Capital Index (SaaS Capital)

So, by comparison, PCYG is currently valued by the market at a significant discount to the broader SaaS Capital Index, at least as of November 30, 2022.

The primary risk to the company’s outlook is an increasingly likely macroeconomic slowdown or recession, which may accelerate new customer discounting, produce slower sales cycles and reduce its revenue growth trajectory.

A potential upside catalyst to the stock could include the robust adoption of Rule 204 Track & Trace technologies by food industry participants, leading to greater revenue for the company.

But, management will need to produce higher revenue growth than 4% to catch the eye of investors.

Until we begin to see that higher growth, I’m on Hold for Park City Group.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment