ezypix

Investment thesis

I believe investors should wait for all the near-term overhangs to be cleared before investing in TuSimple (NASDAQ:TSP), despite the significant upside potential.

There appears to be two camps here, one that believes TSP is a fraud and one that does not, and I have no view on how the investigation on TSP would turn out. This post is to illustrate the bull case for TSP, assuming it is not a fraud, and what is the potential upside if everything checks out.

TSP is a provider of autonomous technology for semi-trucks that has collaborated with other ecosystem participants to create the world’s first Autonomous Freight Network. TSP’s ability to complete local terminal-to-terminal routes via surface streets distinguishes it from other autonomous truck competitors. TSP can provide better service to customers by being closer to the shipper’s distribution center, lowering capital intensity, and potentially reducing transit times and costs. Overall, if all goes well, TSP’s AFN and OEM partnerships, combined with its focus on its camera system, position the company well in the growing market for autonomous trucks.

Business overview

TSP’s autonomous technology, tailored for semi-trucks, has allowed them to create the world’s first Autonomous Freight Network [AFN] in collaboration with other ecosystem participants.

$4 trillion dollar TAM

Prospectus estimates place the total value of the truck freight market at $4 trillion. While the potential size of the market for autonomous trucks is large, the reality is likely to be smaller. A Level 4 solution that is both affordable and reliable has the potential to convert a sizable number of heavy trucks in the long run, despite autonomous truck technology’s small share of the total available market.

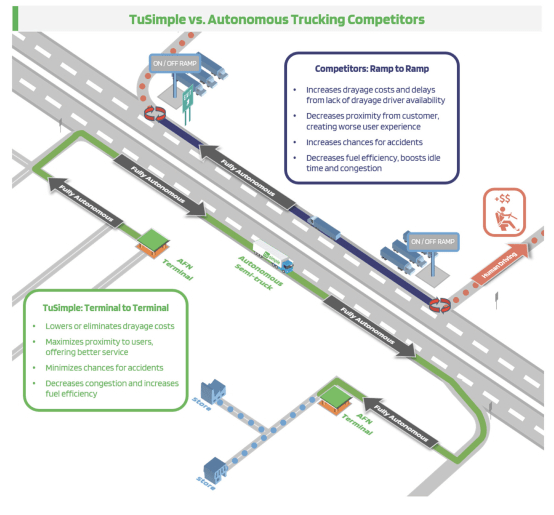

The 5G of autonomous freight network?

TuSimple’s ability to complete a local terminal-to-terminal route via surface streets, as opposed to a ramp-to-ramp route that begins and ends next to the highway, is a major differentiator when compared to other AT competitors. I share the company’s perspective, but I’d like to point out that the ramp-to-ramp solution requires new facilities to be built near major highways, which could be expensive to acquire alone or would require a partnership to own and operate. The cost savings from an autonomous line haul may be reduced if local truck haul from the ramp to the final destination is required. In addition, drayage expenses are notoriously hard to quantify and show substantial regional variation. To keep costs down, increase safety, and possibly slow down transit times, I think a terminal-to-terminal solution is the way to go.

S-1

An autonomous truck system can provide a better service if it is located closer to the shipper’s distribution center and can potentially lower capital intensity by going directly to the destination rather than stopping at an intermediate ramp. While it may not be feasible to have an autonomous truck network without a visible presence, there are strategic advantages to developing the AFN alongside the L4 truck. For example, it allows TSP to secure key locations in corridors where L4 testing and commercial rollout are permitted and to identify and test routes with major shippers and carriers to ensure their viability and potentially gain truck bookings for full L4 operations.

Strategic partnership with commercial potential

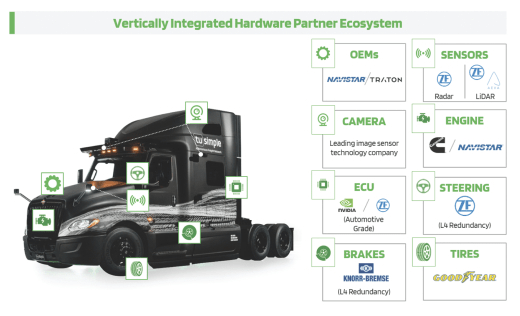

Given the difficulty in securing OEM commitments without the support of Tier 1 suppliers, TSP’s partnerships with OEM are noteworthy. While TuSimple’s embedded software “driver” is what makes an autonomous truck run, it takes all parties involved and their respective areas of expertise to mass-produce a L4 truck that is as safe, reliable, and high-quality as a traditional truck.

TSP’s camera system, which is a critical component of its autonomous truck system, is developed in-house, while other hardware components are sourced from Tier 1 suppliers. TSP’s focus on its camera system, which has long-range perception capabilities for highway driving, I believe, gives it a competitive advantage because it focuses resources on this key area while also leveraging lower production costs and shortening the time to market. The camera system is an essential component of TSP’s autonomous trucks’ perception, motion planning, and control modules. The superiority of sensors, particularly camera systems, is expected to be a key point of competition in the emerging autonomous vehicle industry.

S-1

CEO was fired

The Board of Directors removed the CEO and Co-Founder after beginning an internal investigation that is still ongoing. The former CEO’s association with Hydron, a company started by another TuSimple Co-Founder, appears to have been the impetus for the dismissal. With numerous government agencies looking into possible financial and intellectual property ties between Hydron and TuSimple, I do not expect this matter to be resolved anytime soon.

After the events of the previous quarter, this incident has further damaged investors’ faith in the company’s leadership. Last quarter, TuSimple’s safety reputation took a hit when an improperly designed safety system control allowed a safety driver to activate the autonomous driving system in an unsafe situation.

It will be challenging, in my opinion, for the company to regain public confidence in its safety culture and broader framework for managing and spotting financial and operational risks. Although I do not rule out the possibility that these difficulties can be surmounted, I do not expect the stock price to react favorably to any upcoming or recent developments. The stock price will suffer, and top management, which is still in flux, will face yet another challenge in the form of possible government investigations. Given the potential for investigations into intellectual property transfers, the prospect of monetizing operations in China also appears less likely.

Even though I still think autonomous trucks will have a huge impact on the transportation and logistics industries, I fear that TuSimple’s blunders will cause it to lose support from key development partners and give its rivals an opportunity to catch up.

Valuation

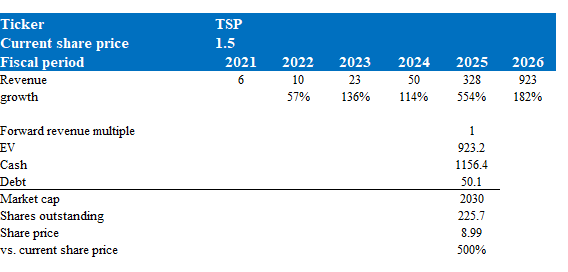

Suppose TSP is not a fraud and the technology it has innovated works as stated. I believe TSP can ride on the strong secular trend and continue to grow aggressively over the long term.

My model suggests TSP could be worth multiple times more than it is today, even if it trades at 1x forward revenue multiple in FY25 (TSP will only see meaningful revenue after FY25).

Model walkthrough:

- Revenue to grow as per what consensus are expecting previous (before the drop in coverage due to investigations)

- TSP to trade at a forward revenue multiple of 1x earnings in FY25, after applying a major discount to what Tesla (TSLA) is trading at.

Own calculations

Risks

Allegations are true

I have stated my thoughts on this above, and this would likely be the nail in TSP’s coffin. TSP stock could fall to 0 if regulators found substantial evidence to sue TSP.

Conclusion

TSP’s AFN and OEM partnerships, combined with its focus on its camera system, position the company well in the growing market for autonomous trucks. However, investors should wait for near-term overhangs to be cleared before investing in TSP, despite the significant upside potential.

Be the first to comment