Pavel Babic

The Investment Plan

Array Technologies (NASDAQ:ARRY) is a company operating in the United States and internationally. They specialize in manufacturing and supplying customers with solar tracking systems meant to further optimize the use of solar modules and boost the energy they generate. Their primary products they offer are the DuraTrack and the SmarTrack. The first one being a solar panel built like a single-axis to increase mobility. This then helps the panel move during the day against where the sun is for ideal exposure. It works together with the software that is SmarTrack, meant to help optimize where the panel best should be positioned.

Even though the company has impressive growth and a product with heavy demand, getting a good entry point is very important. I have the company right now as a hold and think investors would be wise to wait for any potential drops to add more for a long-term position.

Latest Earnings Report Highlights

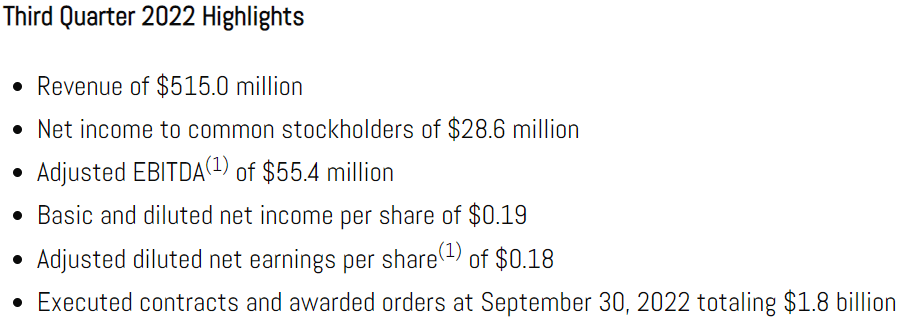

In the latest earnings report, for Q3 of 2022, Array reported revenues of $515 million. This was an impressive increase of 173% compared to last year’s same quarter. A big reason for this increase in revenues comes from a larger production volume for the company. But what the management noted was a big tailwind for them was the acquisition of STI Norland. This helped contribute $114 million to the company’s revenues in the quarter.

Earnings Report Highlights (ARRY Q3 Report)

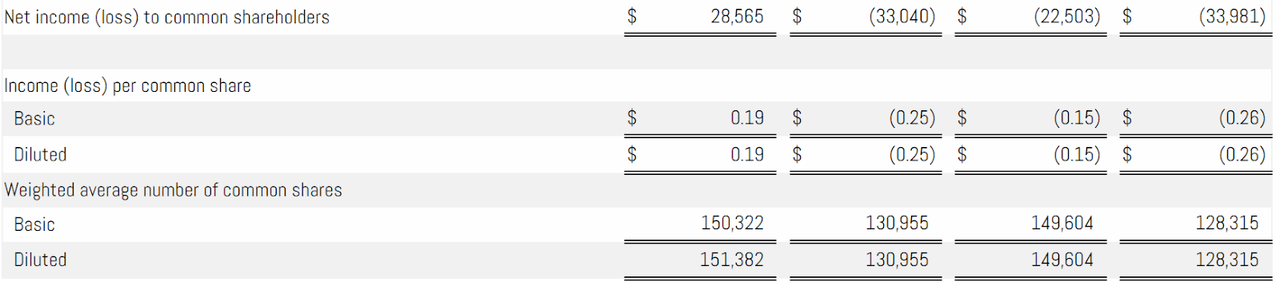

A notable improvement came for the bottom line. With the net income being $28.6 million, a big move compared to last year’s net loss of $33 million. EPS ended up being $0.19.

Looking at the margins, this is the fourth quarter in a row where we see improvement. An impressive thing despite the ongoing economic climate where a recession and slowdown is expected.

Revenue Statement (ARRY Q3 Report)

The company maintained optimistic outlooks with the IRA as a big tailwind, “While we do expect to see meaningful growth from the IRA, it is important to know that there is still much that is unknown about the final form of this Act”. I think this is a responsible comment from the CEO Kevin Hostetler, as investors might otherwise get disappointed thinking companies would have it way too easy selling their products. It will help incentivise customers to go for renewable energy sources, but in the end there are still costs to be considered.

Sector Outlook

Array is operating in the solar sector like I mentioned before. I think that this market is poised for a lot of growth in the next decades. As people are more aware of where they get their energy from, the electrification of the modern household will be more and more common, I think.

Solar Market Outlook (GrandViewResearch)

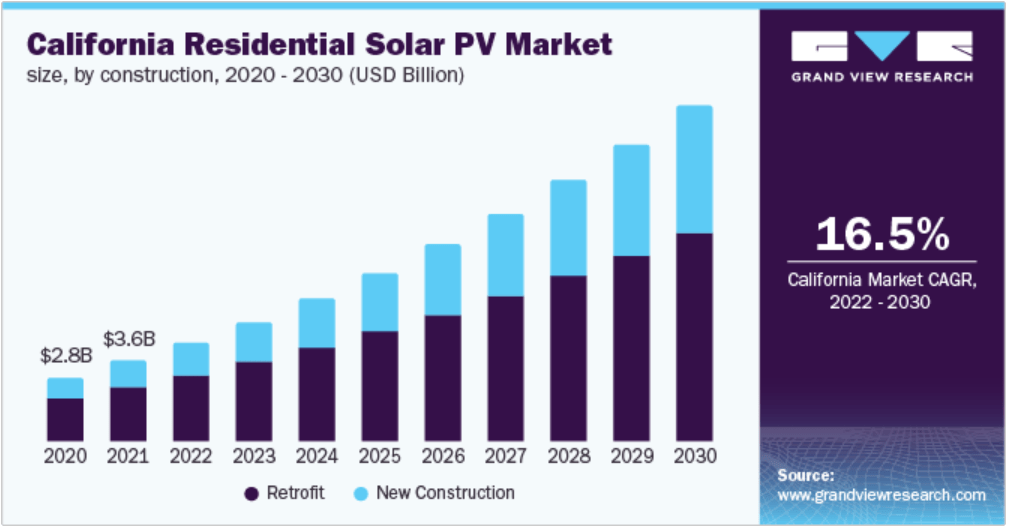

One of the largest markets in the US for solar is the residential part. California is one of the first states where the government is actively giving pushes towards green energy. This also happens to be one of the fastest growing parts of the country for solar adoption. Until 2030 there is expected to be a CAGR of 16.5% in terms of the TAM for companies. A large part is also for new constructions. Looking more internationally, I can also see that Europe will be a big customer of solar products. Here, Germany and France are leading the way and adopting more and more modules.

Competition

The solar sector is filled with different companies, all focused on creating a winning product. The niche that Array is in focuses a bit more on residential solar modules, but also for commercial use. Some of the notable competitors they have are Ascent Solar Technologies (ASTI), Solaria (OTCPK:SEYMF) and Enphase Energy (ENPH).

What might appeal investors to lean more towards Array is the steady growth rate they are projecting. An EPS growth of 15% YoY until 2030 is realistic, which also puts the company right now at a much better entry point than Enphase, for example. A company trading at a very high p/e. Besides this, Array also has a strong cash position compared to ASTI for example, a company who is burning through cash and barely generating enough revenues. Lastly, Array has Solaria beat by quite a bit, as the company is yet to generate any meaningful revenue stream. The product they have is also unlikely to be a disruptor to Array.

The Balance Sheet

I am a strong believer that knowing how the balance sheet is for a company is a deciding factor in whether or not you should invest money into it. There are some important factors I particularly like to look at, the cash/debt ratio, the way assets and liabilities are growing. But I also like to see if there is any share dilution and how cash flow is developing for the company.

ARRY Balance Sheet (ARRY Q3 Report)

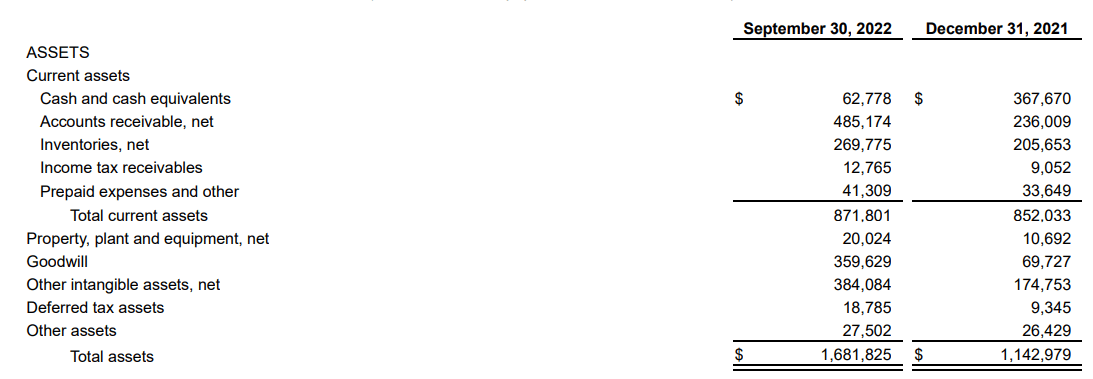

In the case of Array they have seen a significant decrease in cash from last year. In Q3, they held $62 million in cash, compared to 2021 numbers of $367 million. One of the reasons for the cash position not growing is that the management is focusing on paying down credit facilities, which I think is a good step towards a better financial state.

ARRY Balance Sheet (ARRY Q3 Report)

If I take a look at the debt, however, I can see that it’s been ever so slightly growing. The long-term debt increased 1.9% YoY. But given the positive cash flow that we will talk about later, I think this increase shouldn’t be worrying.

The ratio between assets and liabilities is currently 1.26. This means that there is ample collateral if the company ever gets themselves into a tough financial position where debts start to mount. A positive sign to me is that the assets are growing faster than liabilities. Assets grew around 47%, while liabilities grew 36%. For me, this means the company is making good investments and building out their structure in a healthy manner.

Outstanding Shares (Seeking Alpha)

Share dilution has been happening for the last several years, much because the cash flow has been negative during that time as well. With the company generating over $100 million in free cash flow in the latest quarter, I have hope that the share dilution might slow down.

Free Cash Flow (Seeking Alpha)

Lastly, the cash flow, as of the last quarter, they generated $100 million in free cash flow. To me, this positive news can’t come at a better time, as the money was well needed to pay down the credit facility. In the future, it will be important for me to look at if these cash flows are sustained, as the last quarter’s high revenues and good margins helped fuel the increase.

Valuing The Company

Let’s put a price target on what I think Array is worth. Having a realistic outlook for what the company might be able to perform and the premium you are willing to pay for it is very important.

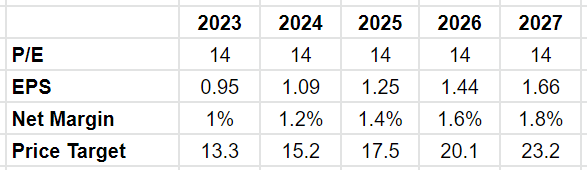

Valuation Estimates (Author’s Own Calculations)

I think that Array has a good growth path ahead of themselves. The market outlook is very positive and with tailwinds like the IRA. This makes me think they can at least grow the bottom line around 15% YoY until 2027. In here, I expect some share dilution, but that will be offset by the fast growth.

The terminal p/e of 14 I think does the company justice. It might be on the low end, but I want to be conservative. Especially for companies in the solar industry. Here it’s common to see some very rich valuations which bring too much downside with it. As a long-term investor, I, of course, want a good entry point.

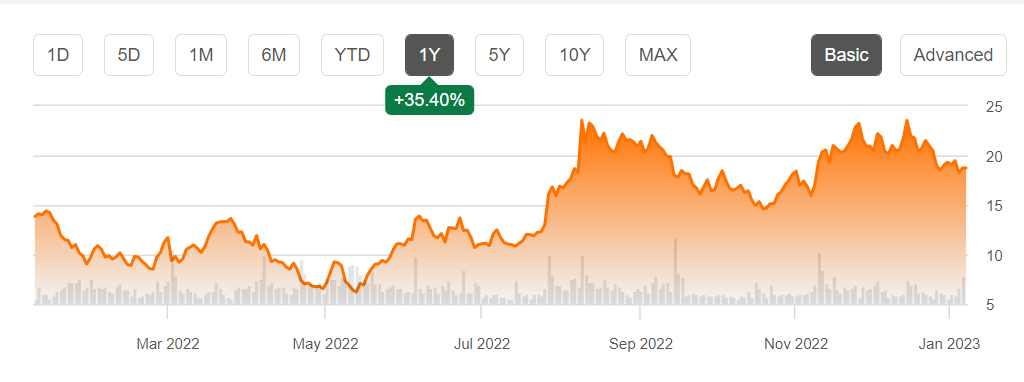

Price Chart (Seeking Alpha)

The TTM net margin is negative for the company currently, but as they scale up and further manage to build out their structure, I think a positive net income in 2023 is not unrealistic. This will be a very important point for me to look at, as if it remains negative, my calculations need to be adjusted lower.

Right now, investing in Array would yield around 4.8% CAGR until 2027. That’s too low for me, and I think waiting for a better entry point would be worth it. Right now, simply holding onto any shares would be the way to go, and then putting in more capital as the price might drop to lower valuations.

Conclusion

Array Technologies is a fast growing company with an exciting product and heavy demand for it. The SmarTrack could help make people even more interested in having solar panels, as their product is more efficient than the standard ones. Paired with their software segment, they are constantly developing their product line.

With a sector poised for growth and the residential solar market still being underpenetrated with a massive TAM, I think Array will have plenty of years with revenue growth.

The management has been taking good steps towards having a better financial state. In 2022, they have spent a lot of their cash to paying off debt and reducing liabilities.

But valuations matter a lot if you are making a long-term investment. Right now the price is a little bit too high for my liking and I think waiting for a potential drop in price to add more is the way to go. But I still believe it’s worth holding on to any shares in the company in the meantime.

Be the first to comment