Cindy Ord/Getty Images Entertainment

fuboTV (NYSE:FUBO) is a virtual multichannel video programming distributor (MVPD) that offers a streaming platform with live and on-demand content. Long-term FUBO investors will be the first to tell you that the stock has been a rollercoaster over the past few years, with everything from the Pandemic to groups on Reddit driving prolonged stints of volatility.

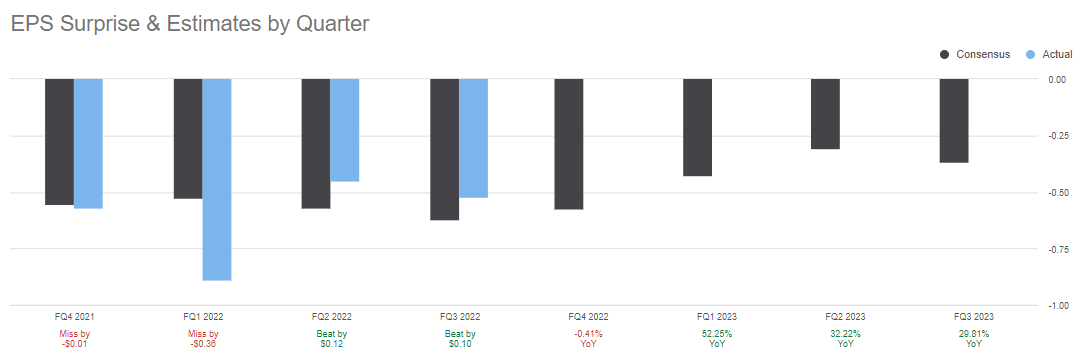

Earnings Download

This was another mixed quarter for investors and many will be left feeling that the growth is good but more is needed. In the third quarter of 2022, the company reported North American revenue of $290 million, a year-over-year increase of 40%, and ad revenue in North America of $22.5 million, a year-over-year increase of 21%. fuboTV also had 1,231,000 paid subscribers in North America and 350,000 in the rest of the world.

Despite these positive financial results, FuboTV’s CEO, David Gandler, announced that the company would be closing its FUBO gaming business and ceasing operations of its FUBO sportsbook in an effort to improve profitability and focus on its core streaming business. Gandler stated that the company remains open to the possibility of exploring ways to optimize its assets in the gaming space without investing its own capital.

On a positive note, Gandler also highlighted the improved adjusted EBITDA margin in the third quarter, which the company expects to continue throughout the remainder of the year. fuboTV is aiming to generate positive free cash flow in 2025 through sustained and profitable growth. I have concerns about how the company will get this far unless losses narrow drastically in the near term.

One of fuboTV’s strategies for driving ad revenue growth has been to invest in its advertising team, technology, and infrastructure in order to improve CPMs and fill rates. The company believes that media consumption trends are moving in its favor due to the frustration and fragmentation that consumers are experiencing with multiple streaming services and content. With the average U.S. household now subscribing to almost five streaming services, fuboTV’s aggregation model, which offers a personalized experience with unique content, is well-positioned to deliver a better experience to consumers.

However, fuboTV faces intense competition in the streaming market and will need to continue to innovate and adapt in order to maintain its growth. The company’s decision to close its gaming and sportsbook operations may be seen as a risky move, as it is giving up a potential source of revenue and possibly more importantly, a source of positive headlines. Additionally, fuboTV’s goal of generating positive free cash flow in 2025 is still several years away, likely leaving the company reliant on external financing in the meantime.

Cash Flow Issues

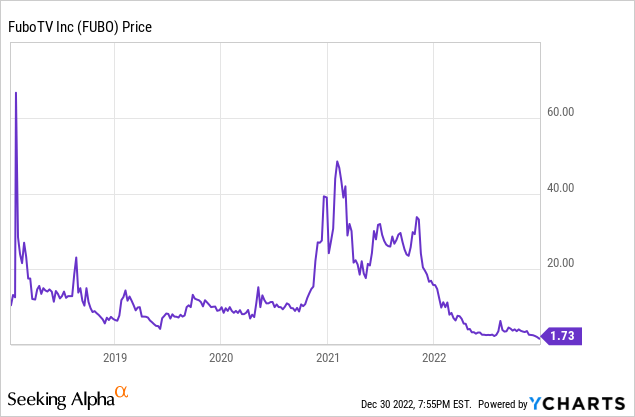

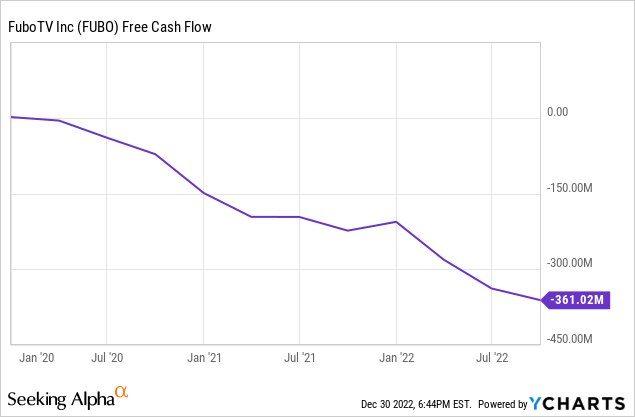

Going into a recession, it is common knowledge for investors to prioritize purchasing companies that have solid free cash flow trends with a strong balance sheet to protect against prolonged downturns. FUBO has neither of these. The company has established somewhat of a track record of burning cash, but the sensational moves due to encouraging press releases or the cult following on Reddit have always given the company the option of offering stock to fund shortfalls. Unfavorable conditions for growth stocks have brought mid to small-cap speculative stocks to their knees, which has severely limited the firm’s ability to raise cash via offerings. This has only highlighted the cash flow issues, which is a major reason the stock has done so poorly of late.

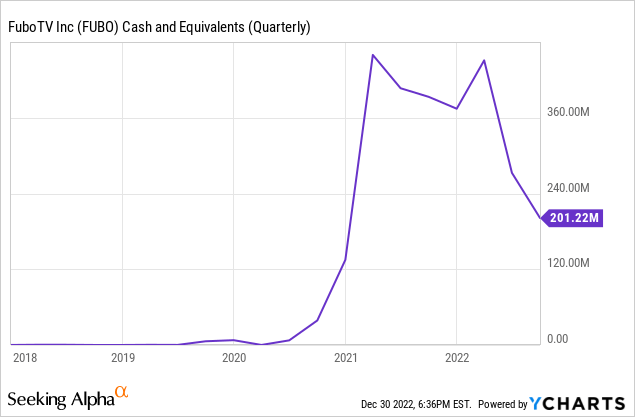

The issue is only exacerbated by the fact that the company has a relatively small cash balance on its balance sheet, totaling only $201.2 million.

Bulls will point to the fact that the company has made notable progress on the revenue front, but in a recessionary environment, EPS figures take precedence and this makes for a somewhat concerning viewing.

Seeking Alpha

We can see that the company is losing relatively large amounts on a per-share basis when compared to its stock price of $1.73. This is a concern because the company is burning through cash at a rapid pace, and it may not have enough cash on hand to sustain its operations if it does not find a way to generate more revenue.

Investors had been placing their hopes on the sports betting opportunities and the company’s buildout of a one-stop live sporting platform but this took a major turn when the company cut its sports betting operation. This was a major selling point for investors in the past, particularly following the Pandemic, when many betting companies saw violent rallies due to their ability to take part in impersonal sports entertainment. FUBO was a bit late to the game, waiting until late 2021 when they launched Sportsbook, but the announcements leading up to the rollout were a major talking point in small investing circles like Reddit. I had my reservations at the time due to the saturation of betting options as well as question marks about market growth and customer stickiness in the industry. While the move was geared toward creating a profitable business, I have serious reservations as to the likelihood of this happening without a cash injection. This is because they already have a pretty good product.

The company has a beautiful service, but competition is stiff in that category. Despite the simple pricing plan ranging from $69.99 to $99.99 at the time of the writing of this article, the company is still far off from profitability. There is a lot of value to be had in their catalog for consumers as the leadership team has built up quite a robust offering but balancing the cost of the premier offerings against the ever-changing costs has been one of the more challenging issues in the space.

The Verdict

FUBO’s strategy of being a one-stop shop hasn’t worked so far. Sports betting was a notable wild card, but the industry is too competitive due to the relatively low barriers to entry. Relying on growth due to customers looking to consolidate services is an exciting idea, but it isn’t easy to quantify that segment, and it will require the firm to continue maintaining an expensive catalog. There are also some huge competitors like YouTube TV from Google (GOOG). As we mentioned earlier, the cash burn is getting concerningly large when compared to the existing market cap and cash balances. Investors may want to look elsewhere until market conditions improve. It is likely that the company may refocus or eliminate other business segments to narrow losses, and we will need to see how sticky the customer base is under those conditions.

Be the first to comment