Leon Neal

The implosion of the crypto markets in 2022 created many victims. The coins themselves were, of course, decimated, but there are related stocks, including miners, holders of crypto, and exchanges. In this article, we’ll take a look at one of the latter, Coinbase Global, Inc. (NASDAQ:COIN), which was once a darling of Wall Street, but its share price is now a mere shadow of its former self. While there are signs of a potential tradable bottom, I cannot recommend this as any sort of investment.

Signs of a bottom?

That’s the key question, and for now, the answer is “maybe.” Coinbase was obliterated as the crypto markets melted down in 2022, taking with it trading volume from retail traders. Since Coinbase’s business largely relies upon retail traders creating transaction volume, that was a serious issue, and remains one today. At some point, Coinbase may have fundamental value, but it is my view that point has not been reached just yet.

However, that doesn’t mean it cannot be traded short-term, and if you’re very aggressive, we may be at the spot where a quick long trade can be made.

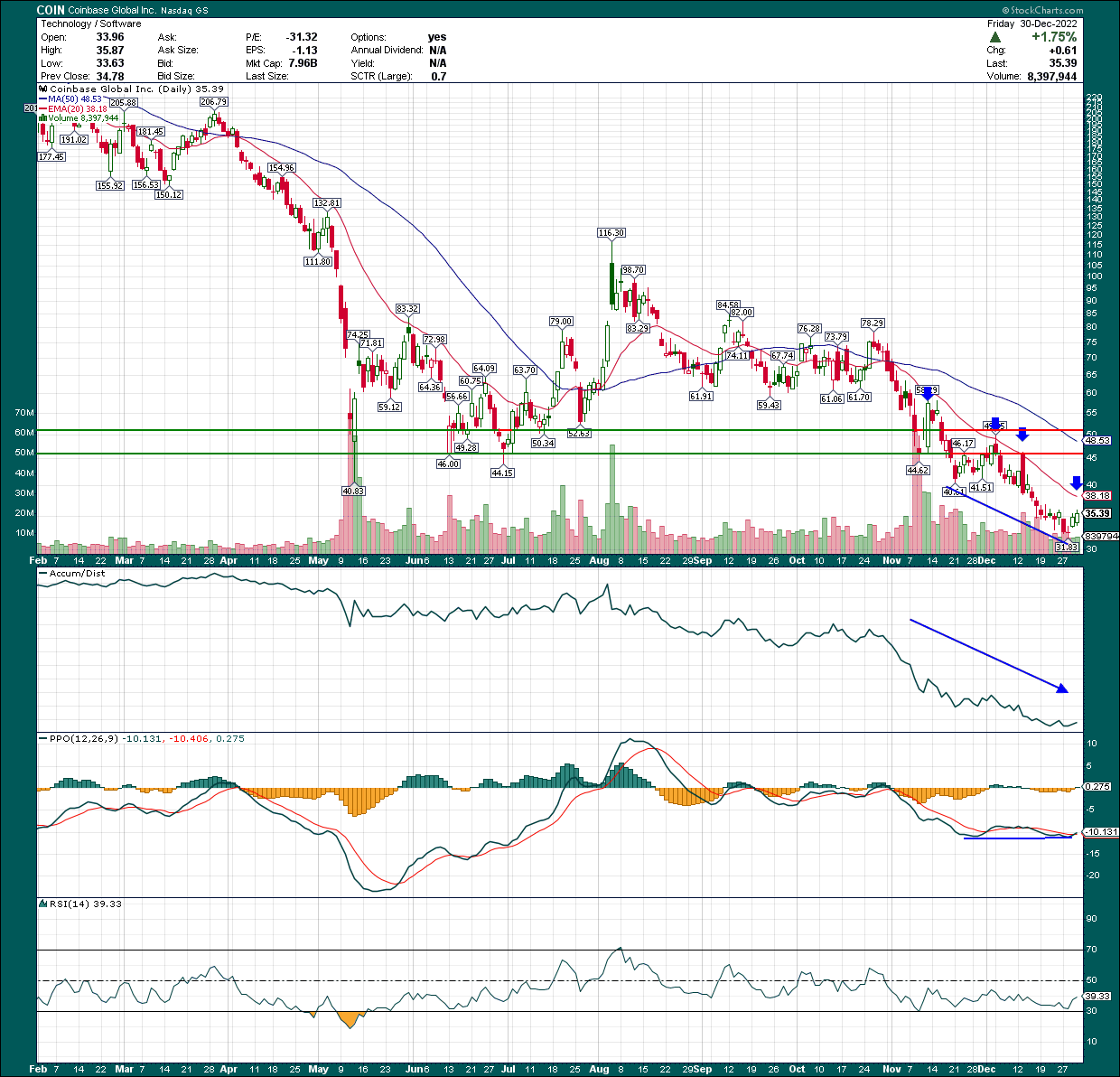

StockCharts

The reason is because, as we can see, the most recent price breakdown that began in November, has created positive divergences for the first time in a while. The last time this happened was over the summer, and the stock doubled before returning back to earth. It is entirely possible we see something like that again, particularly if risk assets are in vogue again in early 2023.

The accumulation/distribution line is awful, but has flattened out in recent weeks. This line measures if a stock is being bought throughout the day or sold, and Coinbase is firmly in the latter camp. However, the PPO has produced a double bottom while price has made a significant new low, which is the positive divergence I mentioned. This can often portend a trend change, and in Coinbase’s case, that would be quite bullish short-term.

Now, there are virtually countless levels of resistance overhead, including the 20-day exponential moving average, which has been a brick wall for months. That’s the first level to watch if you’re bullish, and it’s $38 now, but rapidly declining. If the stock breaks through that line, that’s a very strong indication that the short-term bottom is in.

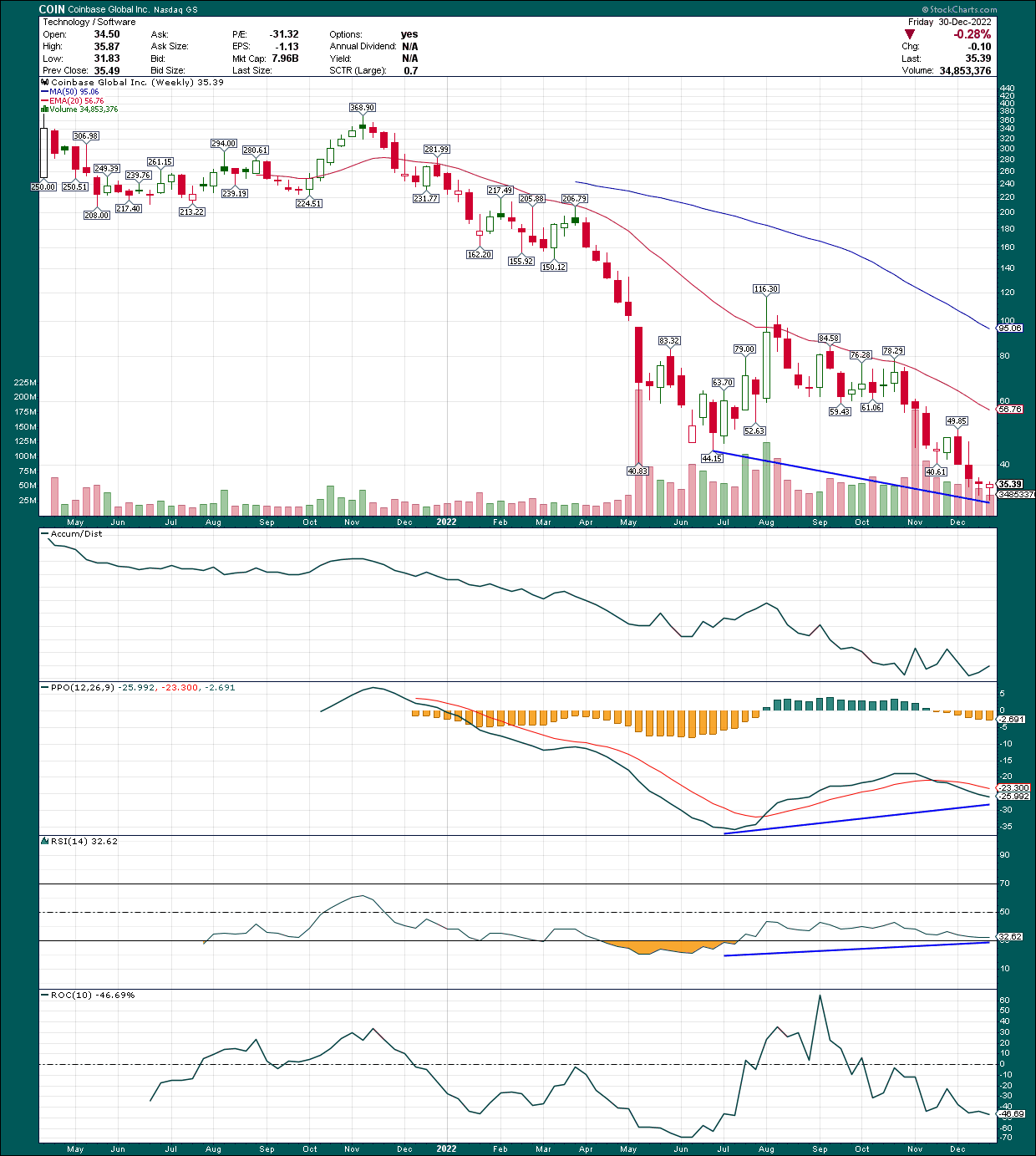

Let’s take a quick look at the weekly chart for a longer-term perspective.

StockCharts

We see much the same behavior here, as the A/D line is horrible, but we have positive divergences in place. The summer bottom and the current price level have created a large positive divergence on the weekly PPO and 14-week RSI, which again, indicate there could be a bottom forming. The one caveat on the weekly chart is that the weekly PPO histogram is solidly negative, so you’d want to ideally see that turn higher again to indicate more bullish momentum.

The bottom line on the chart is that this stock continues to look awful as an investment, but it is possible that a short-term, tradable bottom is forming.

Weakening fundamentals everywhere

The headline on Coinbase’s fundamental situation is that it needs retail traders to generate transaction volumes on its platform to make money. And what retail traders need to do that is a bull market in cryptos, which we haven’t had for some time. Crypto, perhaps more than any other asset class I’ve seen, goes through boom and bust cycles. That means interest in the class mushrooms during bullish periods, and collapses during bearish periods. We’ve been in a bearish period for some time, and it means that companies that serve the crypto market, like Coinbase, have nowhere to hide.

The company’s shareholder letter from the third quarter is quite telling in that its metrics continue to deteriorate to the point where cutting costs is really the only thing the company can do. As has been seen countless times throughout stock market history, when a company’s “strategy” is to reduce costs, that means all other options have been exhausted. It’s not a good place to be. Healthy, growing companies don’t focus on reducing costs; they focus on growing the business. Coinbase does not have that luxury, and I’m not sure when it might again.

The company notes numerous headwinds, resulting in transaction revenue falling 44% quarter-over-quarter. Remember, that’s not year-over-year, that’s over a three-month period. It’s tough out there.

These headwinds include daily average crypto market cap and volatility – both of which are critical for generating revenue for Coinbase – declining 30% and 24%, respectively, on a sequential basis. In addition, trading volume has shifted from the U.S. to international traders, as U.S. volume plunged 50% and international volume fell a more modest 18%. Given the company’s concentration in the U.S., that’s a sizable issue. Finally, Coinbase noted that competition is growing in the crypto space, so even if/when a bull market in crypto returns, it may lose market share over time.

Q3 shareholder letter

We can see that monthly users peaked in Q4 of 2021, which was the peak of the bull market in risk assets – not coincidentally – but MTUs (monthly transacting users) have fallen steadily since then. MTUs were still higher year-over-year in Q3, but we can see that didn’t help revenue generation, as that fell by well over half during the past year.

Now, there are very few companies in the world that can see their revenue get cut in half and still maintain profitability. Coinbase is no different, and profitability completely disappeared with the fall in the top line. This is why the company is trying so desperately to cut costs; this deleveraging is impossible to overcome with revenue performance like this, and it means that the company does not believe it will return to the run rate of $1.2 billion per quarter that it had in 2021’s Q4 anytime soon. In other words, it’s scaling down to meet lower demand as it bleeds cash each day it operates.

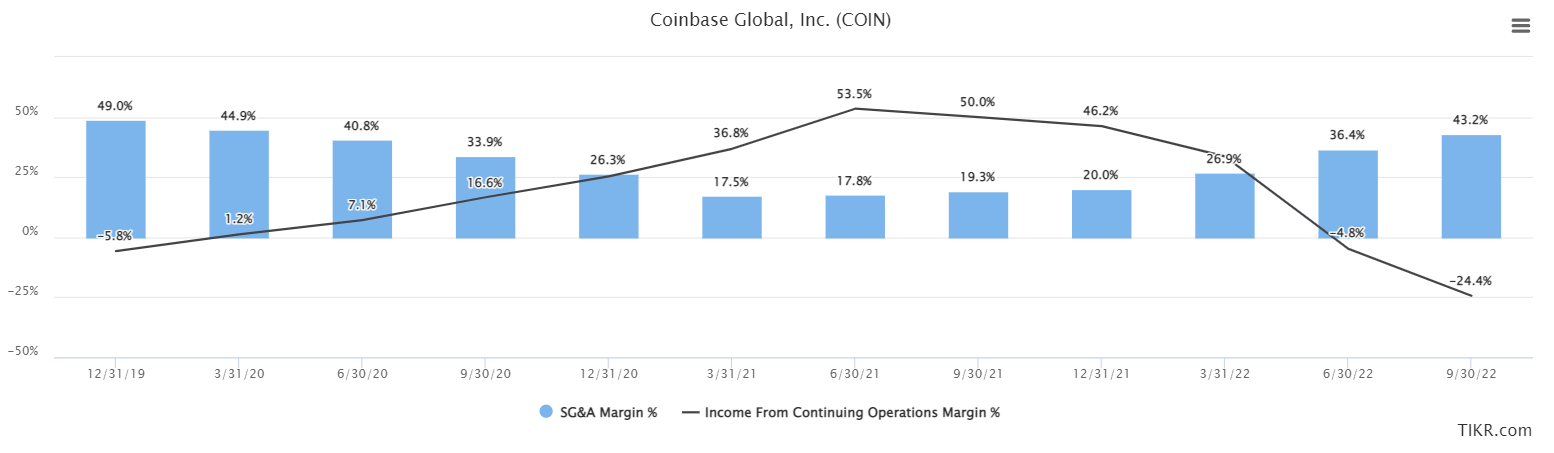

For a look at why cutting costs is so important, we have SG&A costs and operating income margin on a trailing-twelve-months basis for the past several quarters below.

TIKR

There is a very clear correlation between SG&A leverage and operating income, as you’d expect. With revenue leverage apparently not an option, the only thing Coinbase can do to try and reset this is to cut SG&A via headcount reductions. This is the chart you want to keep an eye on in the quarters to come.

Finally, the company’s guidance for 2023 states:

“For 2023, we’re preparing with a conservative bias and assuming that the current macroeconomic headwinds will persist and possibly intensify.”

That doesn’t sound particularly bullish to me.

Looking ahead

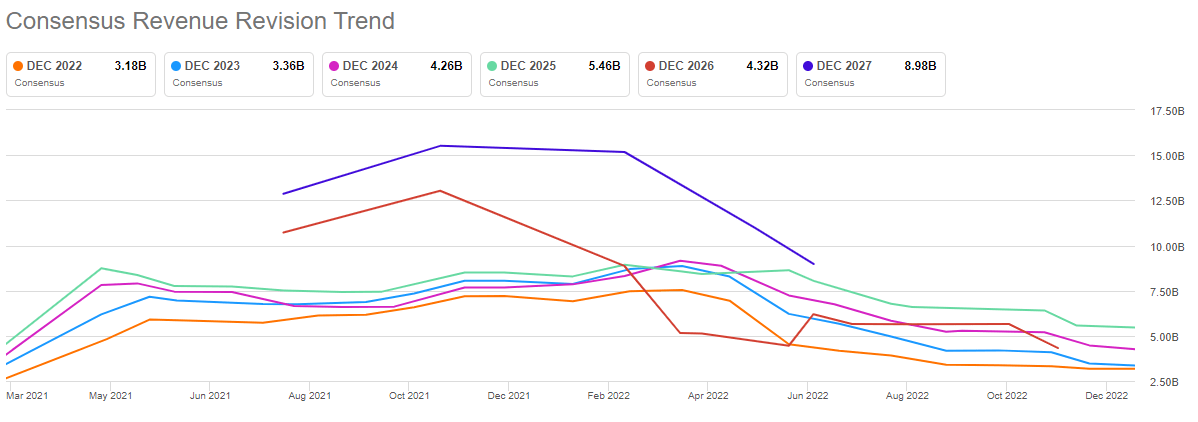

Let’s begin our look ahead with what analysts see as the future for the company’s top line.

Seeking Alpha

We can see revisions have been extremely negative in the past year, which you’d expect given the crypto markets have plunged into a nasty, prolonged bear market. The good news is that estimates have leveled out some, so it’s possible we’re at an inflection point. However, the bottom line is that Coinbase needs the crypto market to enter a new bullish phase, and it just isn’t at the moment.

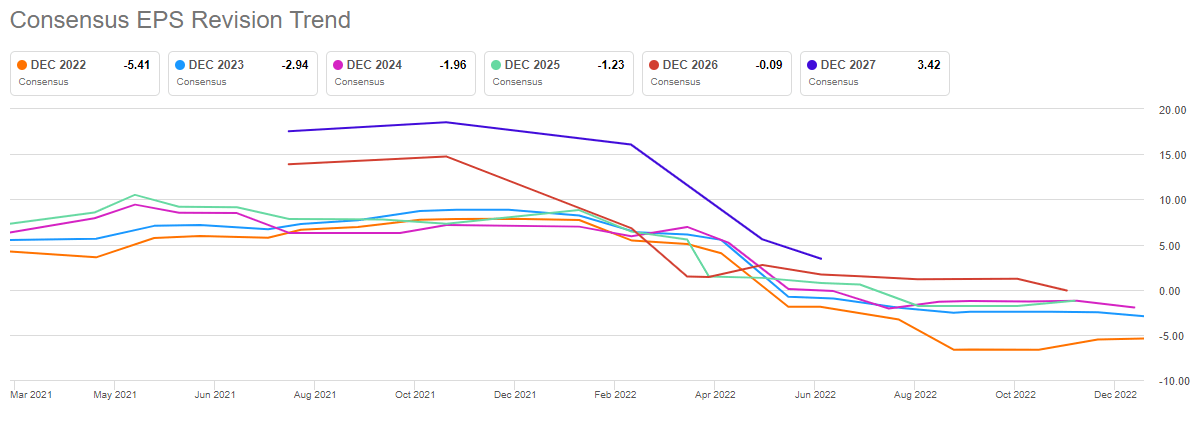

EPS revisions have been much worse, which we know to be the case given the extreme deleveraging of costs the company has experienced as revenue has fallen.

Seeking Alpha

For instance, estimates for 2022 peaked at almost $8 late in 2021, but today’s estimate is -$5.41. That’s deleverage at work. To be fair, should revenue start to recover, so will EPS estimates, particularly as the company is working to cut costs. But it all comes down to crypto bullishness returning, so Coinbase is a bet on a new crypto bull market.

Given Coinbase has no earnings, we cannot value it that way. Let’s instead use enterprise value to revenue, which we can see below.

TIKR

Now, before we get too bullish on this, remember that Coinbase went public at what could be considered the best possible time during a raging bull market. That led to some eye-popping valuations, but also consider that Coinbase’s fundamentals have continued to deteriorate. When the company was printing money with its strong earnings, a higher EV/S multiple was justified. Today, the company’s operating margins are firmly negative, so its valuation should be much lower on an EV/S basis.

Thus, while the stock looks cheaper based on this, whether it’s cheap enough or not is in the eye of the beholder. I cannot make the case this stock is cheap enough to buy, because the situation with demand from retail crypto traders is so weak. I am confident demand will return at some point, but whether that’s tomorrow or three years from now is anyone’s guess. To my eye, it’s chronically unprofitable at the moment, so I don’t know where the bottom should be in terms of EV/S.

The bottom line here is that Coinbase has what could be the beginning of a sustainable, tradable bottom forming. We have positive divergences in the daily and weekly charts, so that’s a very good start. Short interest is elevated so moves in this stock are exaggerated in both directions, and that’s a risk to keep in mind if you want to trade this one.

I can’t make a fundamental case, however, for owning this stock. If the crypto bear market continues for months or quarters, Coinbase Global, Inc. could easily see its stock continue to plummet indefinitely. I simply don’t see a bullish case here, so if you want to trade it, set your stop loss no lower than the recent low at $31.83. If that level fails, Coinbase’s bottoming formation is invalidated and it could be in for another substantial leg lower. This one is for a trade only (potentially), and not an investment; there’s simply too much uncertainty and risk here with Coinbase Global, Inc. for my taste.

Be the first to comment