jiefeng jiang

Most value investors will tell you that the time to buy a stock is not when it’s flying high, but when it’s beaten down with market sentiment working against it. That’s because getting a great starting valuation is one of the biggest drivers of long-term gains, and can shave years off of trying to play catch up after buying at too high of a price.

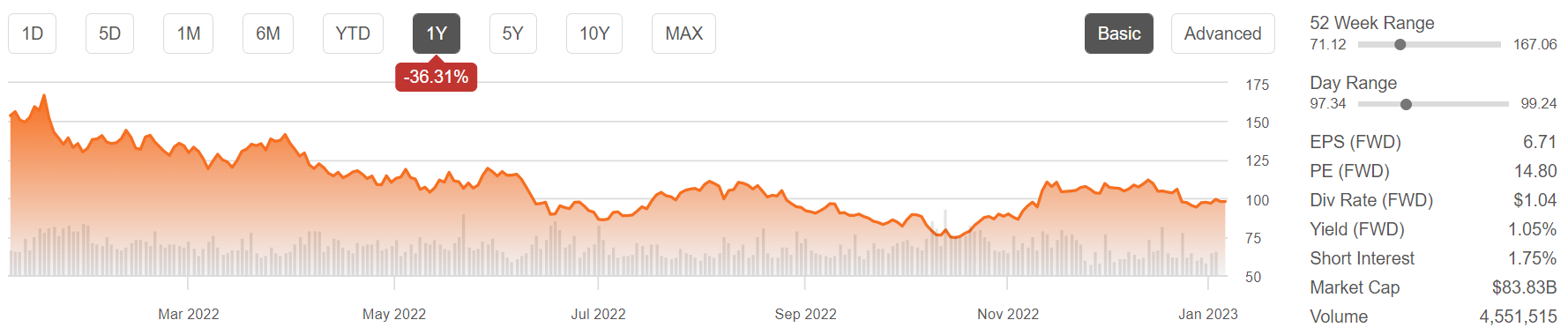

This brings me to Applied Materials (NASDAQ:AMAT), whose stock price has declined in value by 36% over the past year, bringing the PE to a very reasonable sub-15 level, especially for a growth company. This article highlights why AMAT appears to be a smart value investment for potentially strong long-term returns.

AMAT Stock (Seeking Alpha)

Why AMAT?

Applied Materials is a leading global supplier of equipment and services to the semiconductor, display, and solar photovoltaic industries, with solutions that are used to produce virtually every chip in the world. It was founded over 50 years ago with operations in the U.S. and internationally in Asia and Europe.

In addition to its core business in the semiconductor industry, Applied Materials has also made significant investments in the display market. The company’s products are used to manufacture LCD displays for a wide range of consumer and industrial applications, including smartphones, laptops, televisions, and other electronic devices.

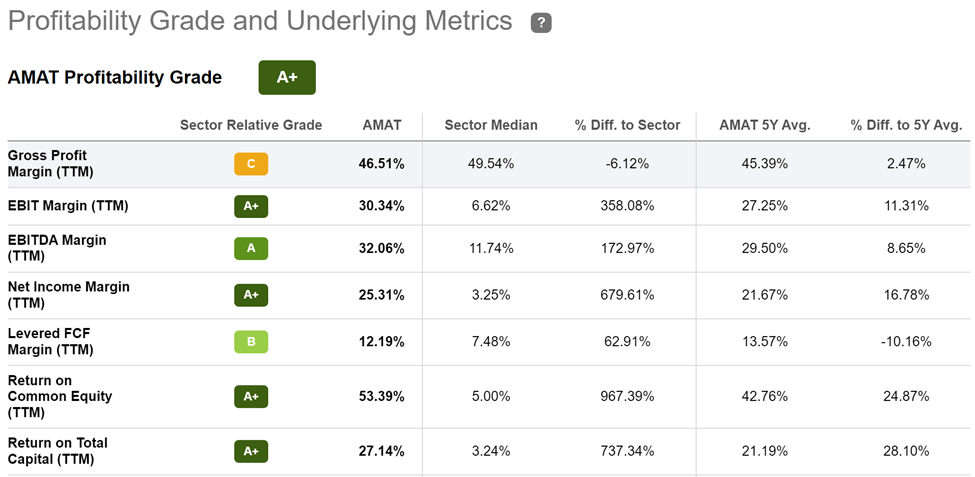

AMAT derives a strong moat from a very large install base of more than 43,000 tools with field service engineers at leading chip manufacturers. This results in significant switching costs, thereby turning them into loyal customers for AMAT. This also translates to pricing power for AMAT and is reflected by its A+ profitability grade. As shown below AMAT achieves high EBITDA and Net Income margins of 32% and 25%, respectively, sitting far above the sector median.

AMAT Profitability (Seeking Alpha)

Meanwhile, AMAT is doing well, with quarterly revenue up 10% YoY to $6.8 billion in its fiscal fourth quarter (ended Oct 30th). This capped a record fiscal year for AMAT with record annual revenue of $25.8 billion, up 12% over the prior year, and this was in spite of headline-making chip shortages due to supply chain issues with top chip manufacturers.

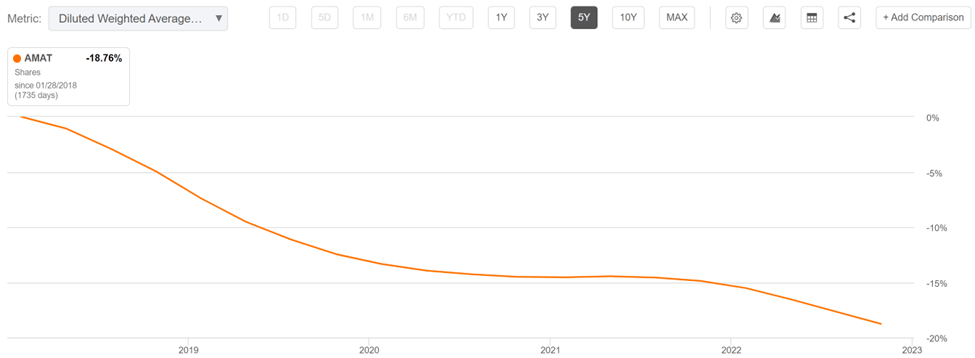

Importantly, AMAT generated a significant amount of operating cash flow, and returned $1.72 billion to shareholders during the fourth quarter alone, with much of it ($1.5 billion) going toward share repurchases. As shown below, AMAT has retired an impressive 19% of its share count over the past 5 years alone.

AMAT Shares Outstanding (Seeking Alpha)

Looking forward, AMAT faces potential headwinds from a potential slowdown in the chip industry, as players like Micron Technology (MU) have cut their outlook and spending forecast last month. However, management seems to be prepared for a potential slowdown with a strong backlog, and believes 2023 to be a blip in the long-term trajectory, as noted during the recent conference call:

We expect 2023 to be a down-year for wafer fab equipment spending, but we believe that Applied’s business will be more resilient thanks to our large backlog, growing service business and strong customer demand for our leadership products that enable key technology inflections. Longer-term, secular trends create opportunities for Applied to outgrow the semiconductor market by enabling the PPACt roadmap with our differentiated portfolio of materials engineering solutions. We are making strategic investments for the future, while slowing spending growth in the near-term.

Notably, AMAT maintains a strong A rated balance sheet. While its dividend yield of 1.1% isn’t high, it does come with a very low 13% payout ratio and a 5-year dividend CAGR of 21%. Investors should also keep in mind that AMAT is a total return story, given that management has prioritized capital returns in the form of share buybacks.

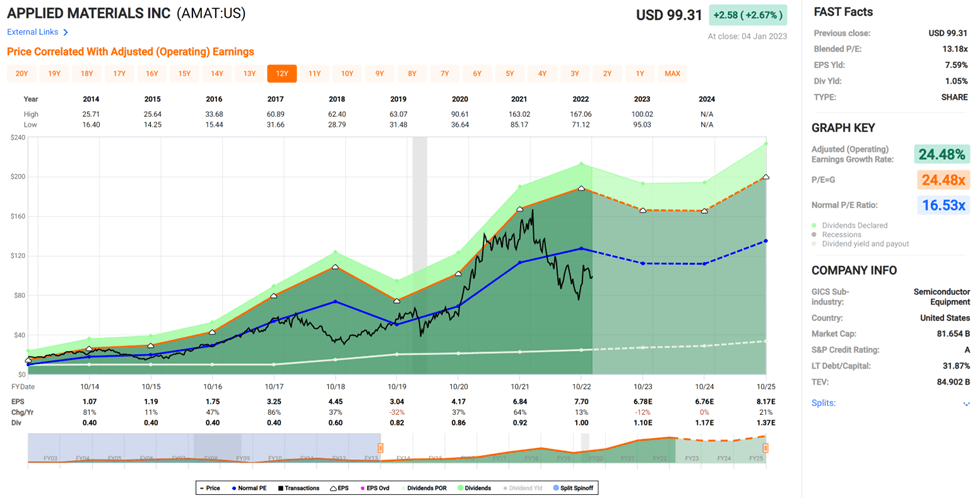

Lastly, I find AMAT to be fairly attractive at the current price of $97.92 with a forward PE of just 14.6, sitting below its normal PE of 16.5. Patient investors should be rewarded, as analysts expect for AMAT to resume meaningful growth after the current downcycle. Analysts have a consensus Buy rating with an average price target of $118.51, which could translate into strong total returns for investors at present levels.

AMAT Valuation (FAST Graphs)

Investor Takeaway

AMAT’s beaten down stock price is attractive for long-term value investors. The company has a strong competitive moat and a high degree of pricing power, which it has been able to leverage into very strong profitability and shareholder capital returns.

Despite potential headwinds in the near-term from the chip industry slowdown, AMAT remains well-positioned for the long-run. As such, value investors may want to consider the stock at present while market sentiment is working against it.

Be the first to comment