Chip Somodevilla/Getty Images News

Introduction

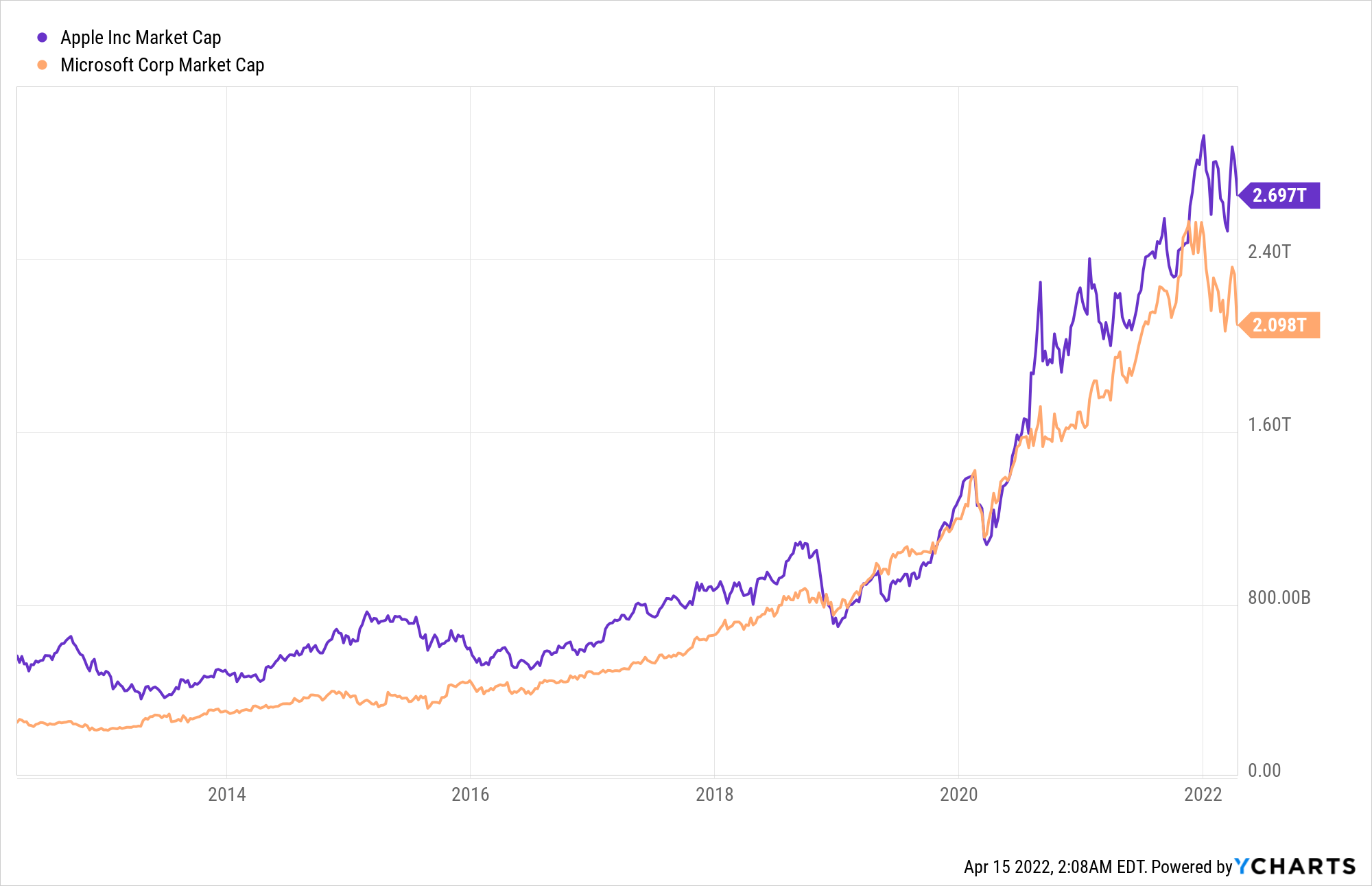

Today, Apple (NASDAQ:AAPL) and Microsoft (NASDAQ:MSFT) are two of the most dominant tech titans on the face of this planet, and it’s only fair that they happen to be two of the largest companies across the globe based on market capitalization. Due to incredible business moats, robust financial performance, rock-solid balance sheets, and humongous capital return programs, Apple and Microsoft have etched themselves as safe-haven investments in the minds of retail and institutional investors alike.

YCharts

While Apple and Microsoft have been fantastic vehicles of wealth creation over the last decade or so, they’re unlikely to repeat the feat over the next decade. For the long-term (5-10 years), I expect both Apple and Microsoft to deliver market-like (SPY) ~10-12% CAGR returns. However, I do not think these safe havens are safe for the medium-term (2-3 years). Why?

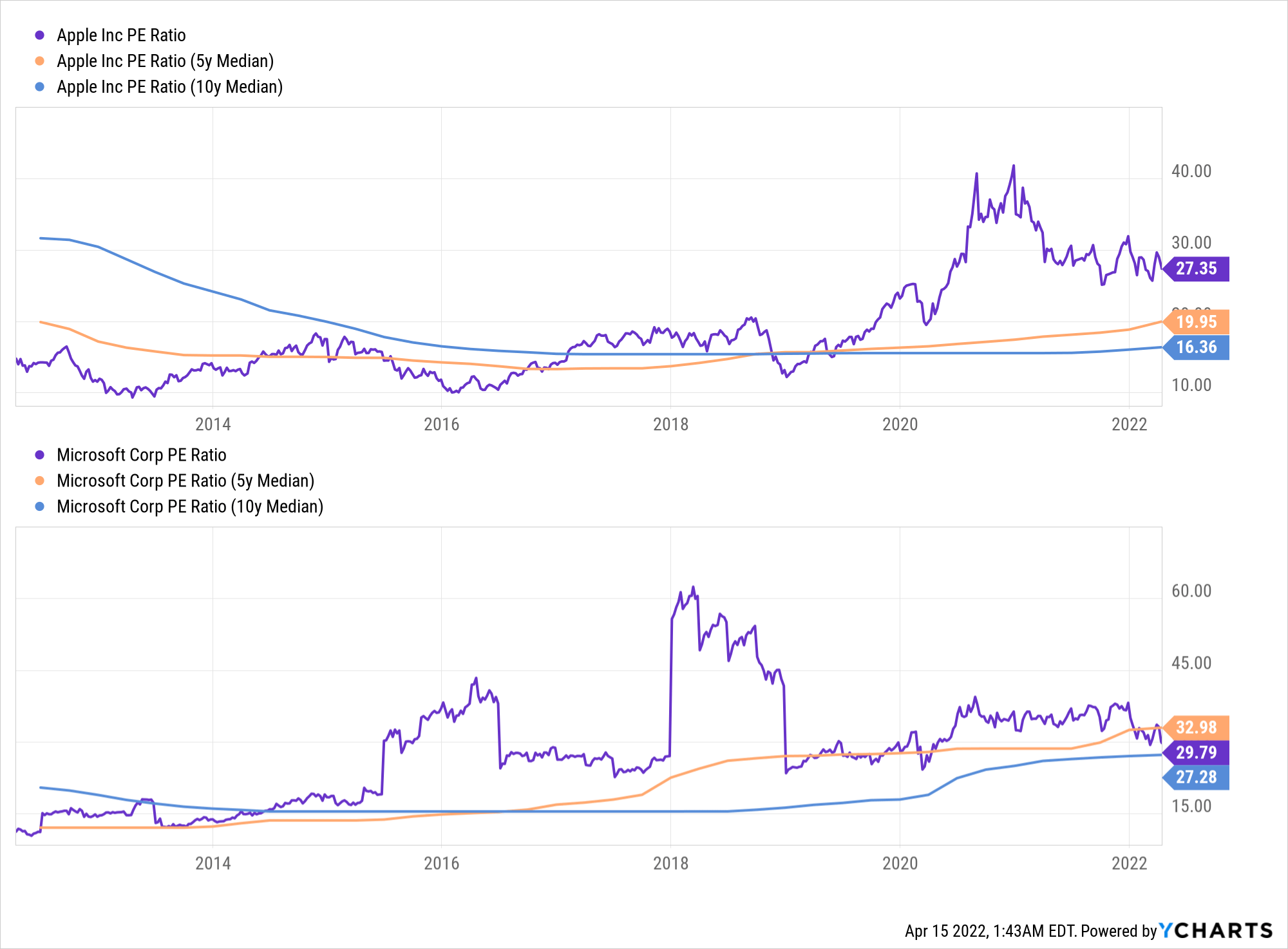

- Starting valuations: In 2012, Apple traded at a P/E ratio of ~14x, and Microsoft traded at a P/E ratio of ~12x. Today, both Apple and Microsoft trade at a P/E ratio of ~28-30x.

YCharts

- Considering business fundamentals, I think these premium trading multiples are probably deserved. After all, both Apple and Microsoft are highly-profitable businesses with a solid track record of delivering revenue and earnings growth.

YCharts

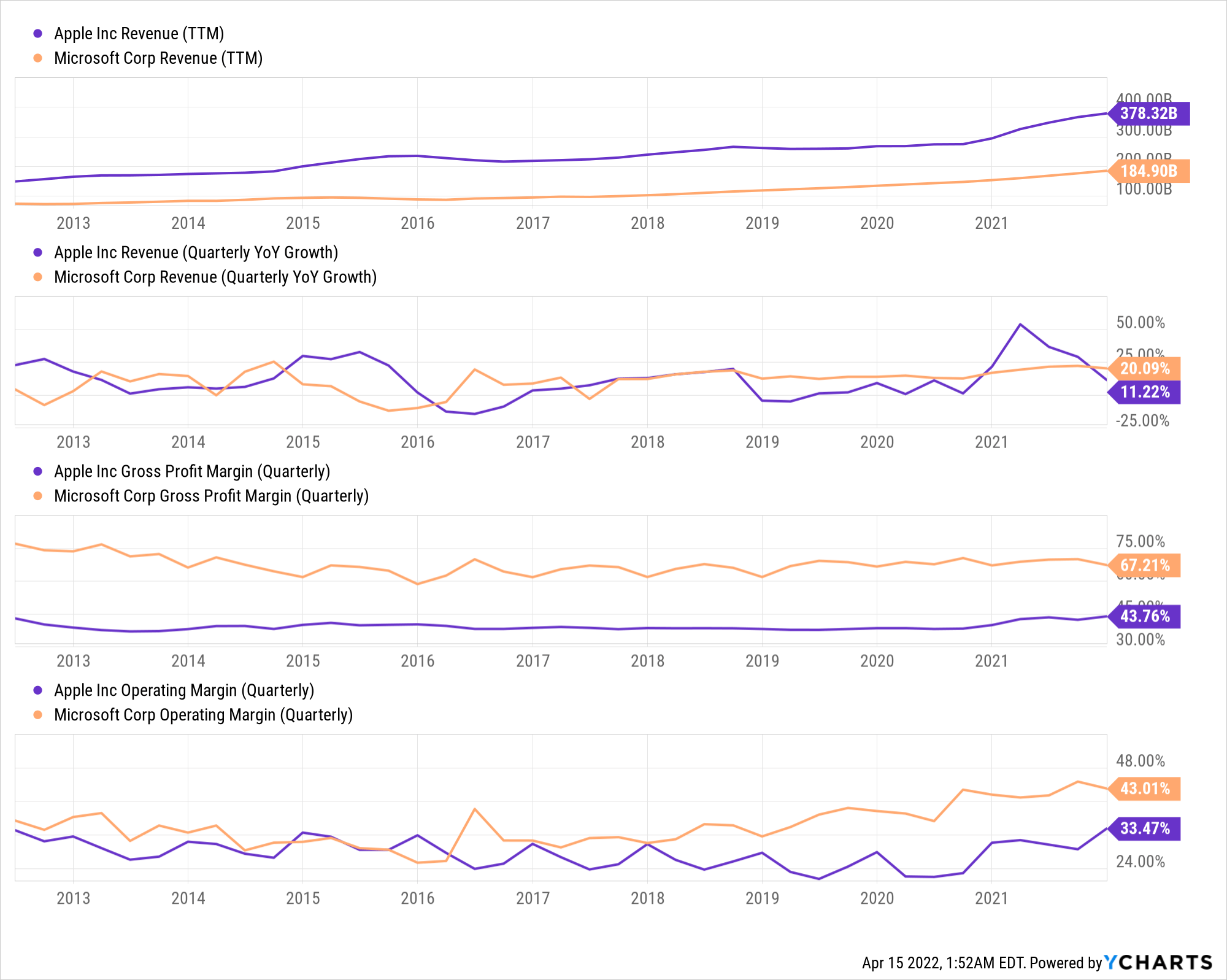

With that being said there’s absolutely no room for multiple expansion (which has been a massive driver of outsized returns in the past).

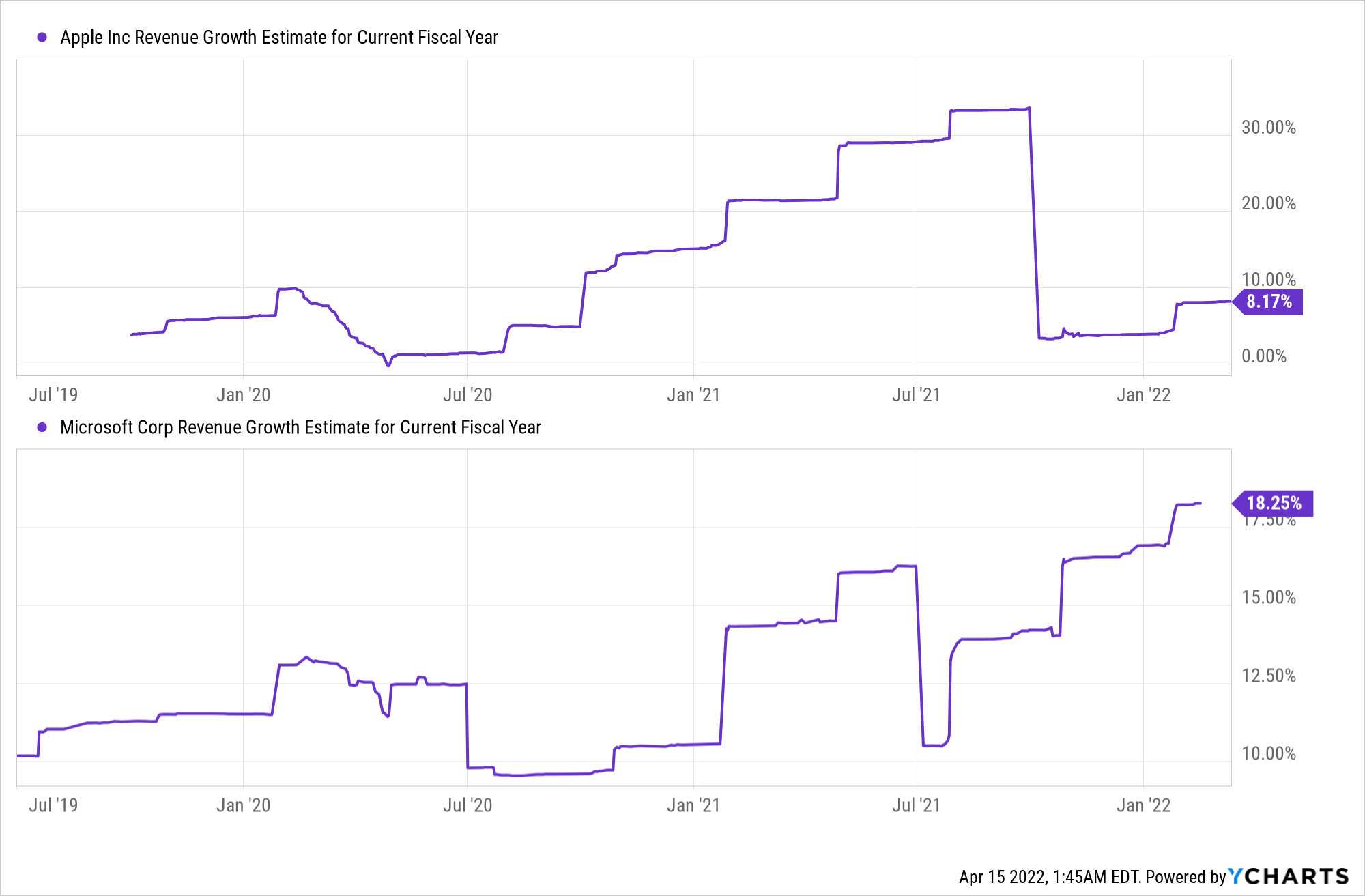

- Growth slowdown: After multiple decades of sales growth compounding, Apple and Microsoft have reached huge revenue bases. Despite obvious dominance in their respective serviceable markets, future growth rates are likely to be lower than past growth rates. The coronavirus pandemic boosted demand (and growth rates) for both Apple and Microsoft. While these businesses would continue experiencing secular tailwinds, the pull forward in demand could dampen sales growth over coming quarters. Furthermore, high inflation could start hurting margins (profitability).

YCharts

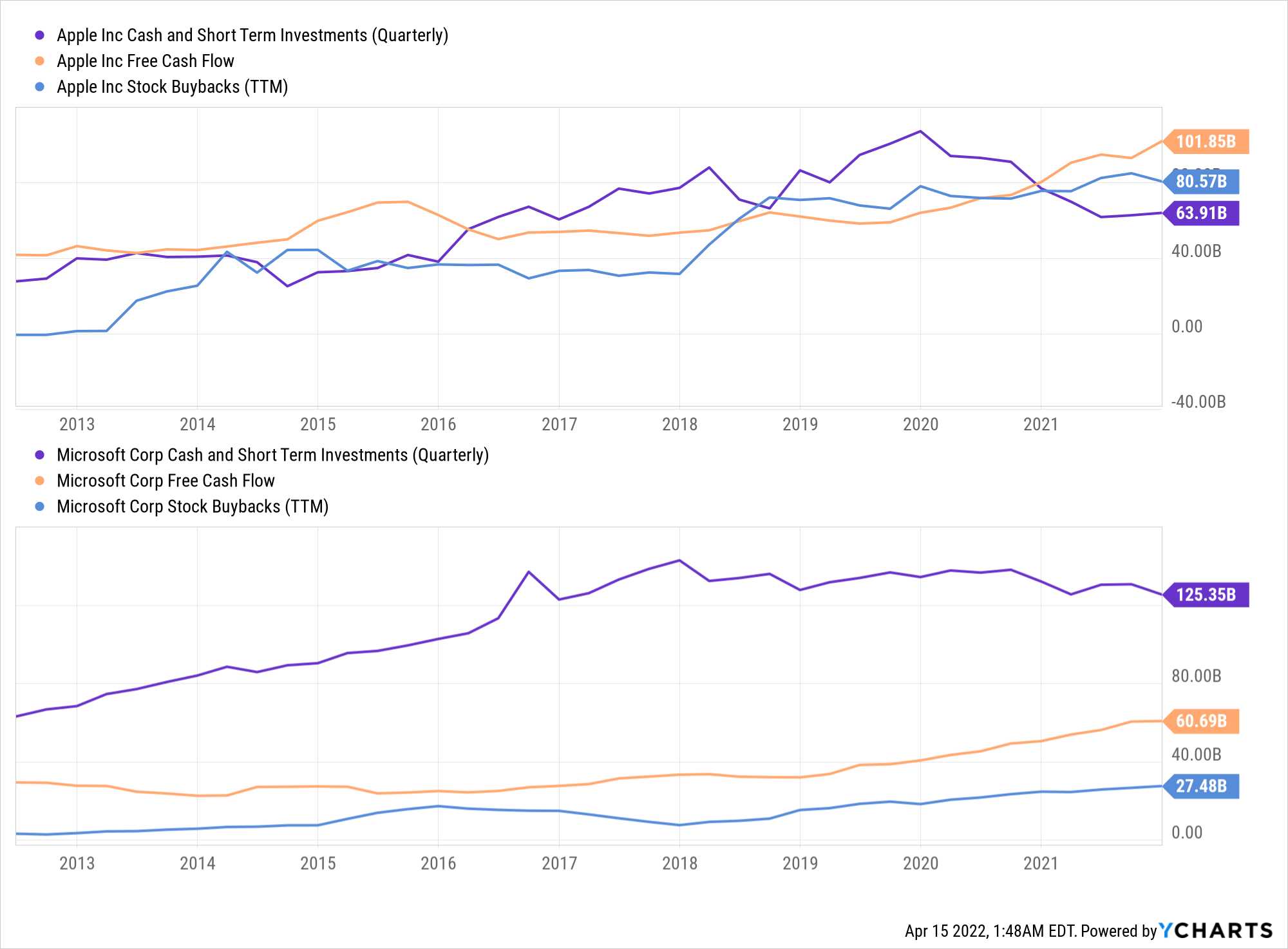

- Buybacks becoming ineffective: At elevated valuations, Apple and Microsoft’s buyback programs are getting less effective at boosting FCF per share (stock price). Both Apple and Microsoft have robust balance sheets and free cash flow generation; hence, I continue to think of them as infinite buyback pumps. However, these buybacks may not be enough to defend trading multiples in a rising interest rate environment.

YCharts

- Rising interest rates: A slowdown in growth combined with rising interest rates could trigger a mean reversion on trading multiples. As Berkshire Hathaway’s (BRK.B) Warren Buffett has said – “Interest rates are like gravity for asset prices.” Since I view surging interest rates as the greatest downside threat for Apple and Microsoft, I would like to discuss this subject in more detail.

The Yield Curve Looks Ominous

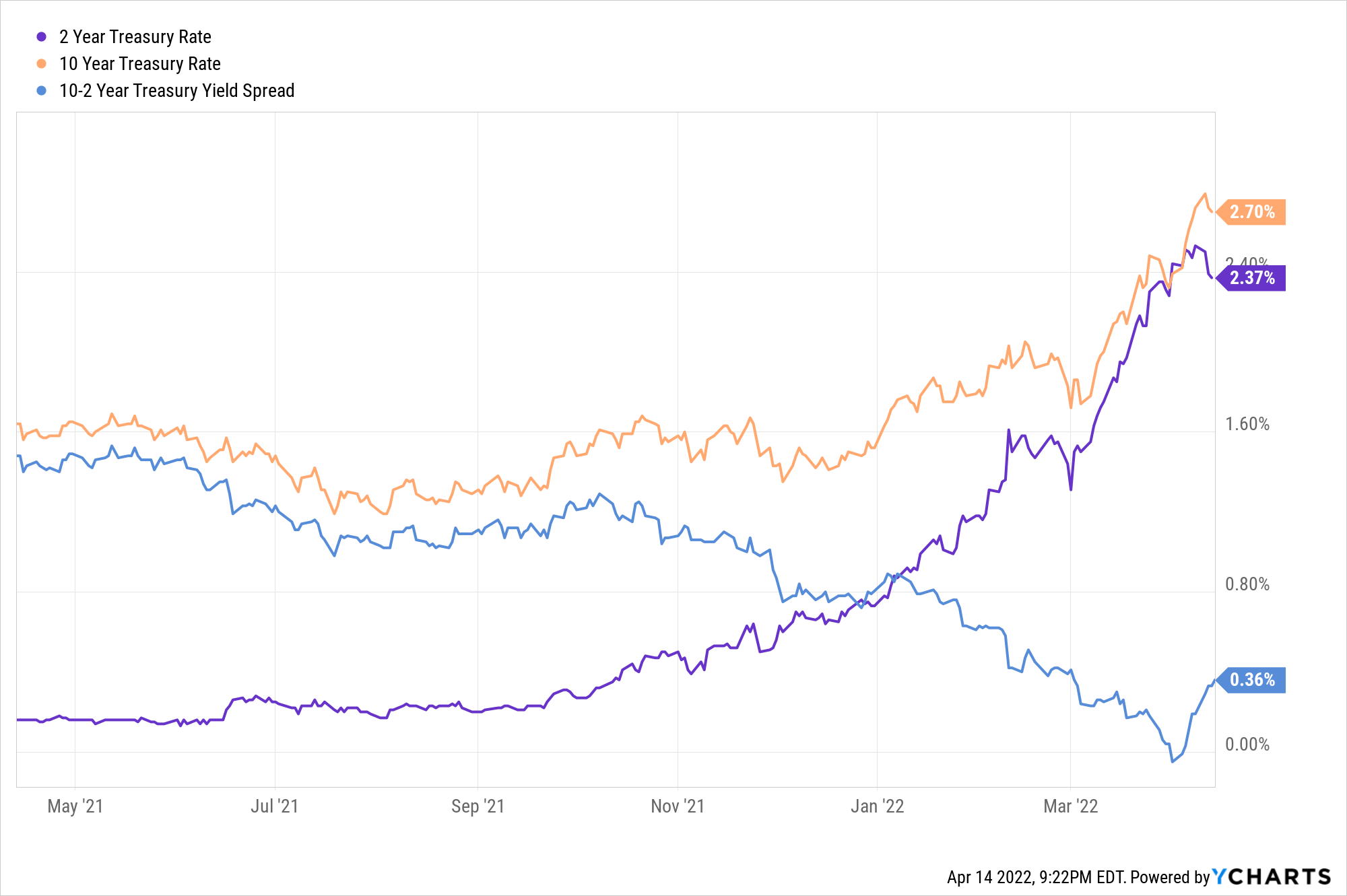

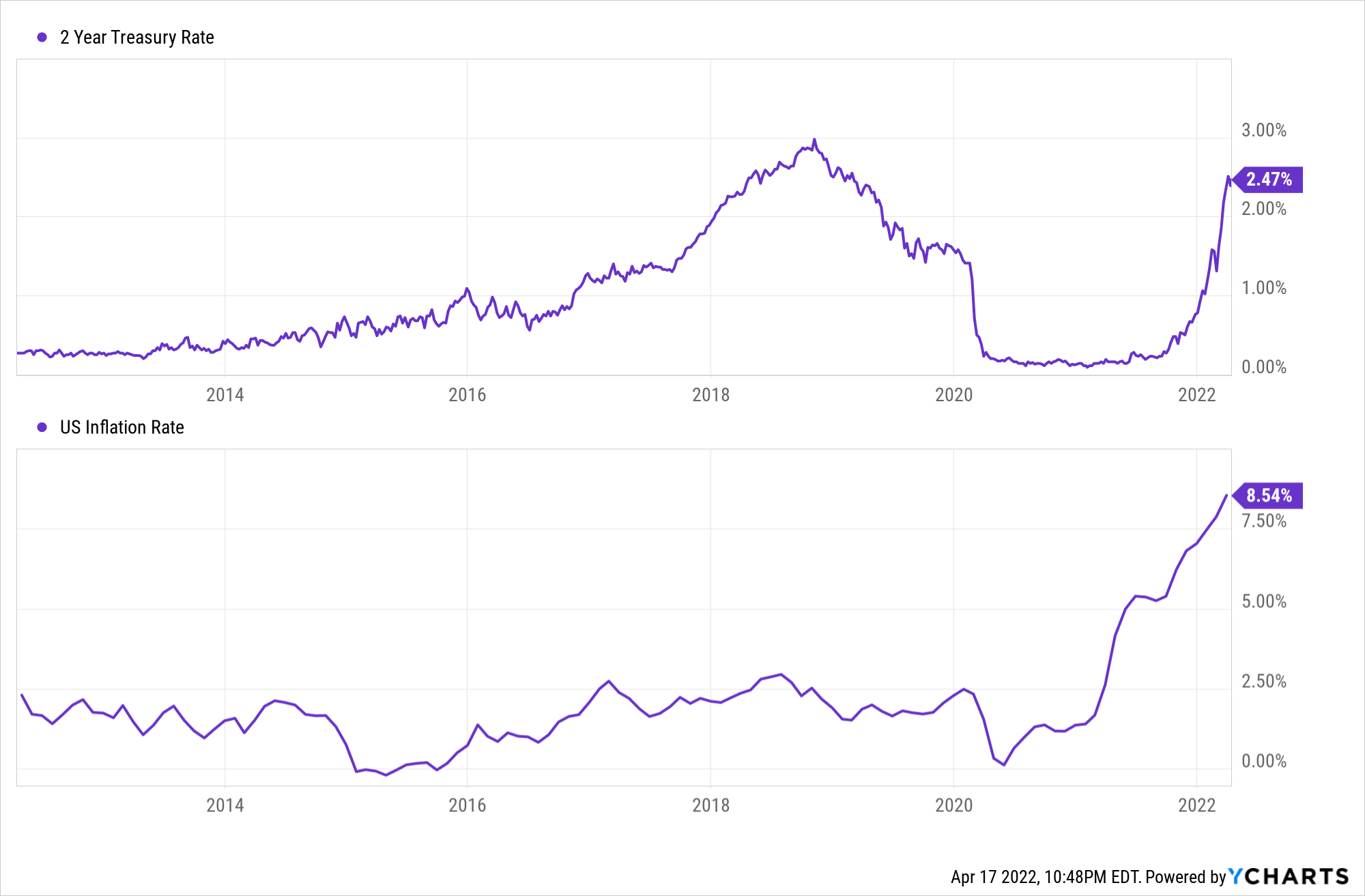

In early April, we saw a yield curve inversion (10-2 year treasury yield spread turned negative), which is looked upon as a sign of an impending recession. While recent recessionary periods have been preceded by yield curve inversions, not all yield curve inversions lead to recessions. And so, nothing is guaranteed. However, we could very well be in the late-cycle phase of this business cycle, and economic growth may slow down in upcoming quarters.

YCharts

Both Apple and Microsoft are operating at the heart of multiple secular growth trends, but a recession could hurt their growth expectations too. I understand the logic (robust FCF generation and strong balance sheets) behind viewing Apple and Microsoft as safe-haven investments during periods of heightened uncertainty. However, surging yields could change this perception very quickly, simply due to the immutable laws of money.

A Reversion To The Mean Could Bring A Lot Of Pain To Investors

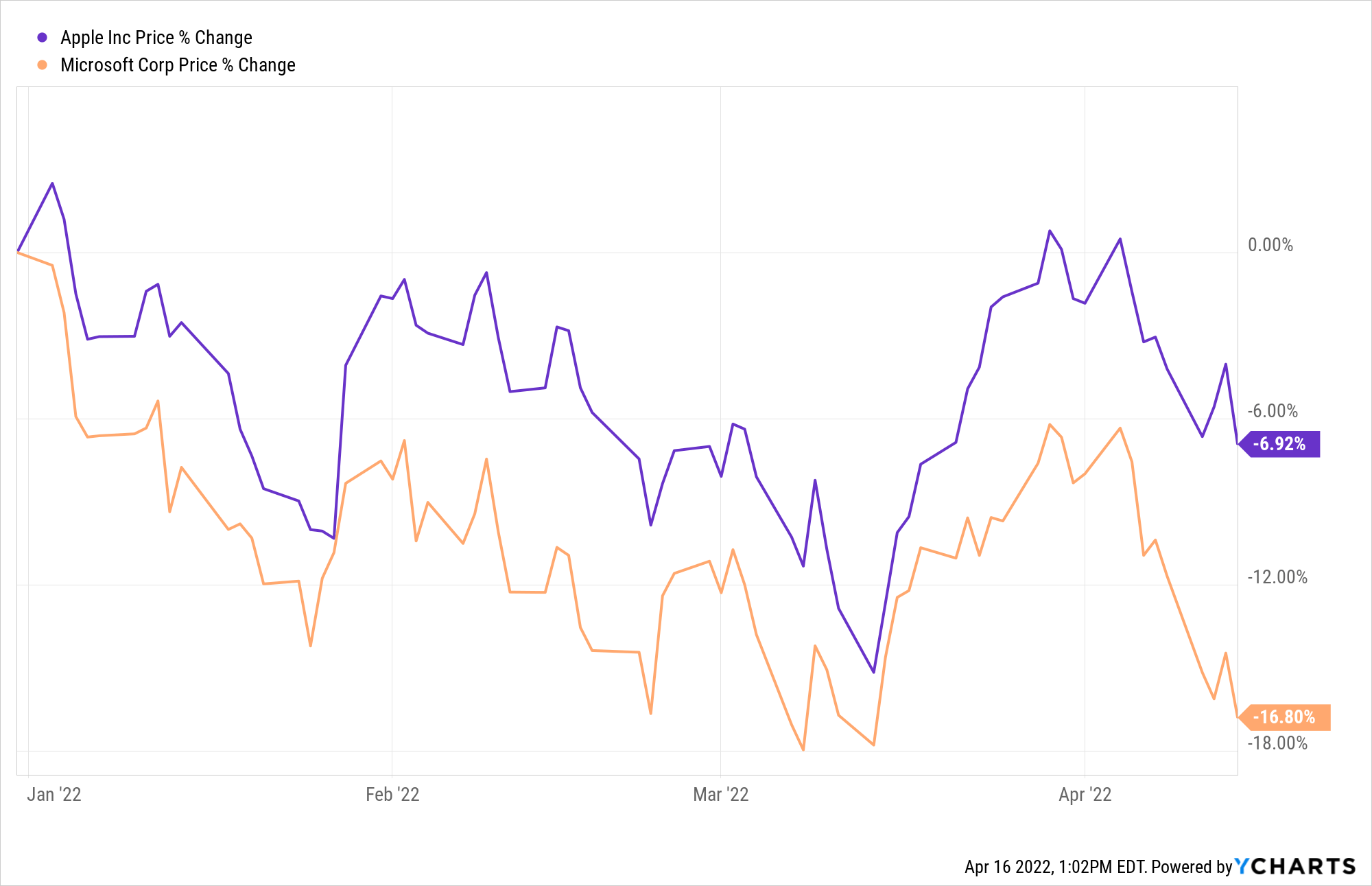

So far in 2022, Apple is down ~7%, and Microsoft is down ~17%. Are these safe havens set to join the bear market in technology (and growth) stocks? And if so, why?

YCharts

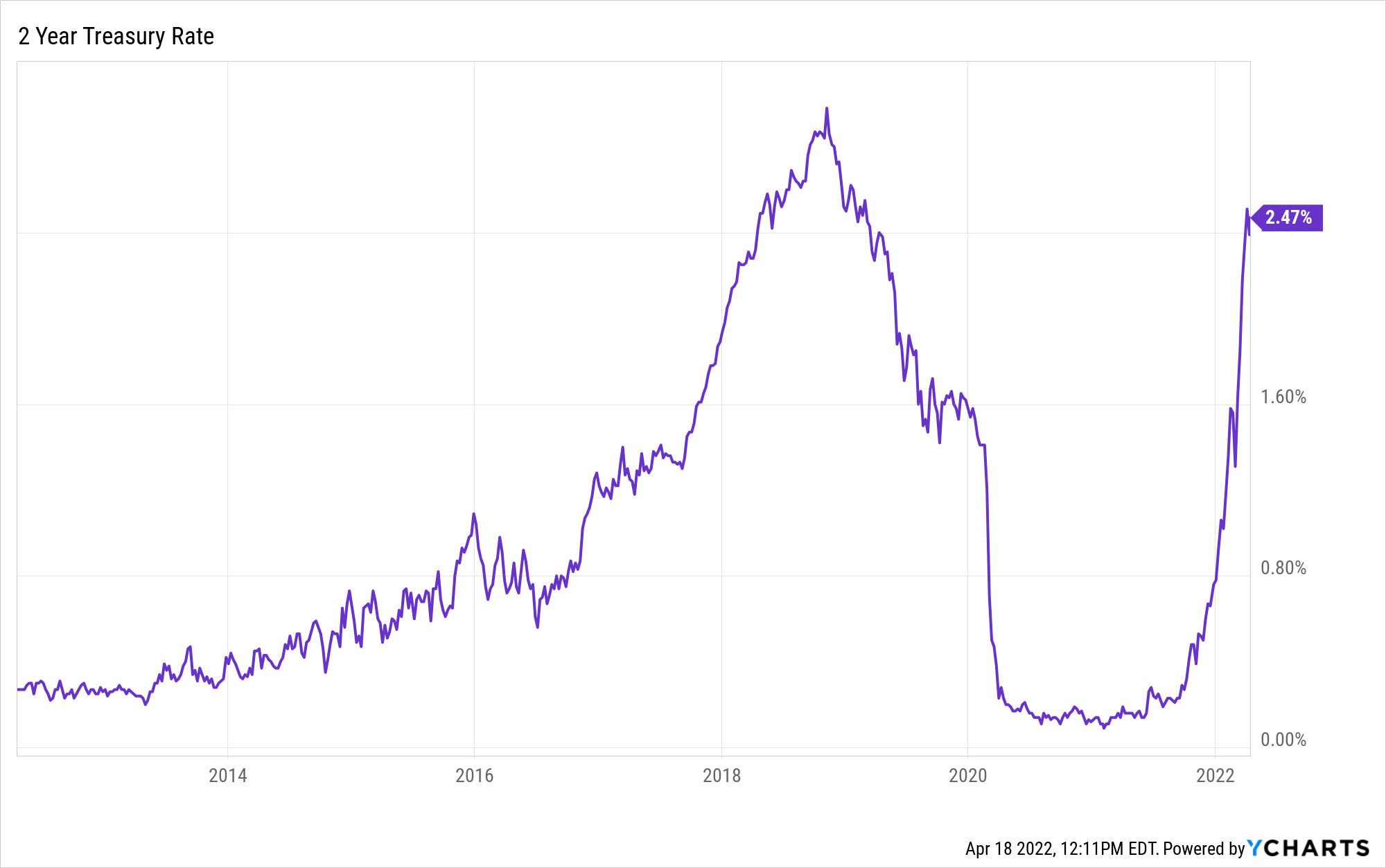

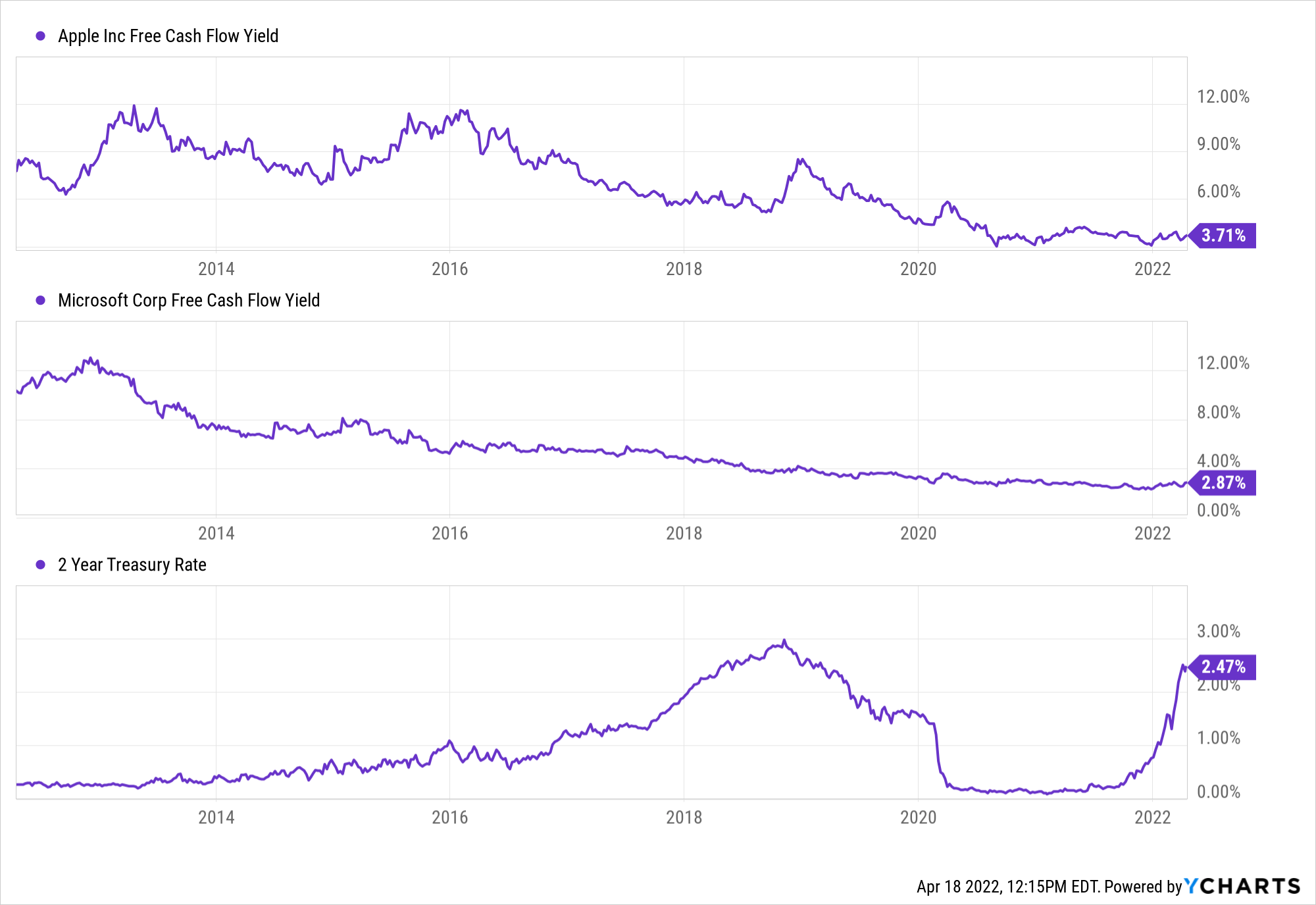

The business fundamentals for Apple and Microsoft have never been stronger. However, their valuations are pretty rich. With treasury yields surging higher, Apple and Microsoft are becoming less attractive to investors looking for safety in the face of multi-decade high inflation and the growing threat of an economic recession. The 2-Yr [2.5%], 10-Yr [2.9%], and 30-Yr [3%] treasuries have climbed to three-year highs, which is enough to change the math for investors. If the risk-free rate goes up to 3.5-4%, why would a sane investor buy Apple or Microsoft at FCF yields lower than the risk-free rate?

YCharts

YCharts

The last time 2-Yr Treasury rates were at 2.5%, Apple and Microsoft offered FCF yields of 6% and 3.5%, respectively. Today, Apple offers 3.7%, and Microsoft offers 2.8%. The risk premium here is too low, and if growth were to slow down, the probability of a mean reversion would be very high.

Throughout the 2010s, Apple and Microsoft traded at P/E ratios of 10-30x. Today, both Apple and Microsoft are trading at the high end of this range, and if we were to see a mean reversion to, say, ~15x P/E, we could be looking at ~40-50% downside on both Apple and Microsoft. Now, this is not my base case scenario, and I believe that high-quality businesses like Apple and Microsoft deserve a premium. However, I look at Meta’s P/E of ~15x, and then it is impossible to ignore the downside risk.

YCharts

In my view, investors are not being compensated fairly for the near to medium-term downside risk in Apple and Microsoft. For the long term, I believe both Apple and Microsoft could deliver double-digit returns to shareholders. However, they may not serve well as safe havens in the medium term. In summary, taking on 40%-50% downside risk in exchange for 10-12% CAGR returns is not attractive to me as an investment. So, where do we deploy capital in this environment?

For starters, treasury bonds are not the way to go. With highly-negative real yields, bonds are simply uninvestable. Period

YCharts

Inflation is at multi-decade highs, and my followers know that I have been projecting “higher inflation for longer” as the Fed’s most-likely path forward since the end of 2021. So, maybe investors should buy defensive stocks?

YCharts

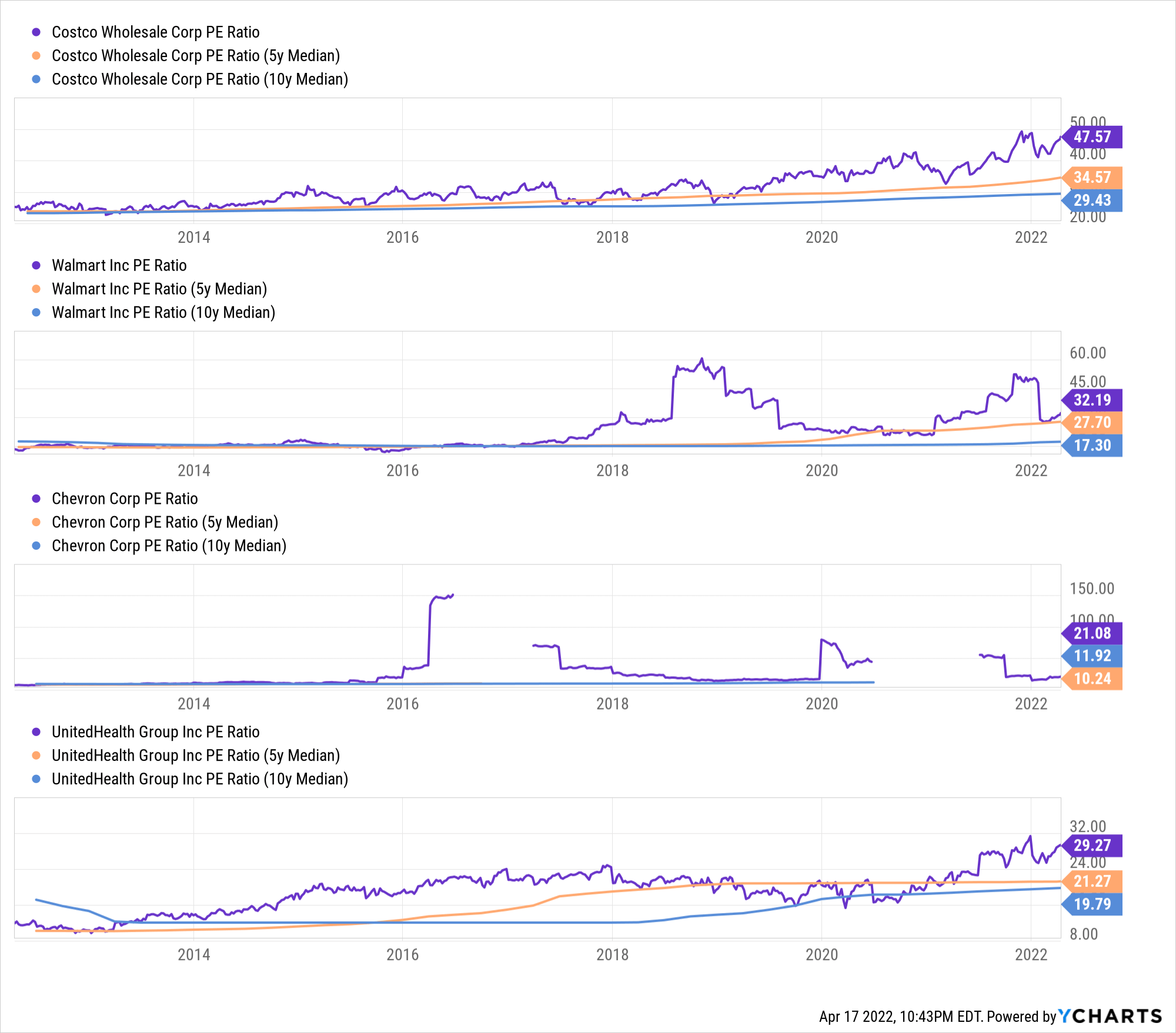

Unfortunately, that boat has sailed way too far off the shore to get onboard. Defensive “value” names like Costco (COST), Walmart (WMT), Chevron (CVX), or UnitedHealth (UNH) are all trading way above their historical averages. The markets are forward-looking, and there’s no way we will make money in the next 3-5 years by buying Costco at ~48x P/E.

Concluding Thoughts

In this hunt for a safe haven, there’s really no good alternative among investments that are widely perceived as being safe. Cash is rapidly losing value due to multi-decade high inflation of ~8.5%, so that’s not an option. As we saw, bonds are still yielding negative real returns, making them uninvestable. The so-called defensive “value” stocks offer no value at all. And perennial safe havens like Apple and Microsoft have 40-50% potential downside. How does an investor deploy capital in this difficult market environment?

I think the best investment opportunities for generating alpha and outpacing inflation are available in the beaten-down high-growth tech space. Our strategy is to invest in rapidly-growing, small-cap companies operating at the heart of secular-growth trends because these stocks could be big winners in the future regardless of economic factors. And there’s not been a better time to buy these stocks in the last two years.

Here are my top ideas for 2022:

and a recent update on these ideas:

If you’re interested in learning more about my outlook on the macroeconomic environment and my logic for buying small, rapidly-growing companies in this market, please feel free to read the following notes:

- Inflation Hits 7%, But The Fed Is Stuck Between A Rock And A Hard Place

- Don’t Try To Rationalize Mr. Market’s Irrationality, Use It To Your Advantage

In the battle of safe havens, there’s no winner right now. Both Apple and Microsoft are decent investments for the long-term, but I think the potential downside risk is not baked into their current prices. With negative real yields, treasury bonds are simply uninvestable. While Apple and Microsoft do give a sense of safety to investors, I do not view them as safe-haven investments at current valuations. Hence, I’m not deploying fresh capital in these stocks. If you are hell-bent on finding a safe haven for the next 2-3 years, I recommend you to look at Meta (FB).

Key Takeaway: I rate both Apple and Microsoft as Hold at current levels. With real yields being negative, treasury bonds are uninvestable.

Thanks for reading, and happy investing. Please share your thoughts, questions, and/or concerns in the comments section below.

Be the first to comment