Nastassia Samal

The past two years have been busier from an M&A standpoint in the precious metals space, but we’ve seen a marked slowdown in activity over the past year. In fact, after two massive deals and several small deals from Q4 2020 to Q4 2021 (Kirkland Lake, Saracen, Roxgold, Jerritt Canyon, Teranga, Great Bear, TMAC, Pretium, Premier, Bateman, Corvus) in the producer/developer space, it’s been a relatively quiet year. The only real deals of significance among producers and developers were the acquisitions of Golden Star, Orca, and Kupol, a slew of non-core asset sales (Boto, Rosebel, Mercedes, Chirano, Karma, Crown Sterling), and Gold Fields (GFI) offer to acquire Yamana Gold (AUY). Some Gold Fields’ shareholders weren’t elated with the latter, and some Yamana shareholders considered it a bit of a take-under and not the best fit.

However, the recent major development was Agnico Eagle (AEM) and Pan American’s (NASDAQ:PAAS) creative deal to come over the top of Gold Fields with a superior offer (15% premium to the implied price of GFI offer) that would give shareholders currency in the world’s lowest-cost senior producer, cash, and shares in Pan American. Meanwhile, the deal is more straightforward, with only 50.01% of PAAS shareholders required to vote in favor, no vote required from AEM shareholders, and the same 66.7% of votes needed by Yamana shareholders as the Gold Fields deal, but no review under the Investment Canada Act, with all three being Canadian companies.

I’ve already discussed the deal in length for Agnico Eagle, and in this update, we’ll look at how this deal looks for Pan American Silver and why I think it’s positive for the company:

Yamana Gold Pour (Yamana Presentation)

A Closer Look At The Deal

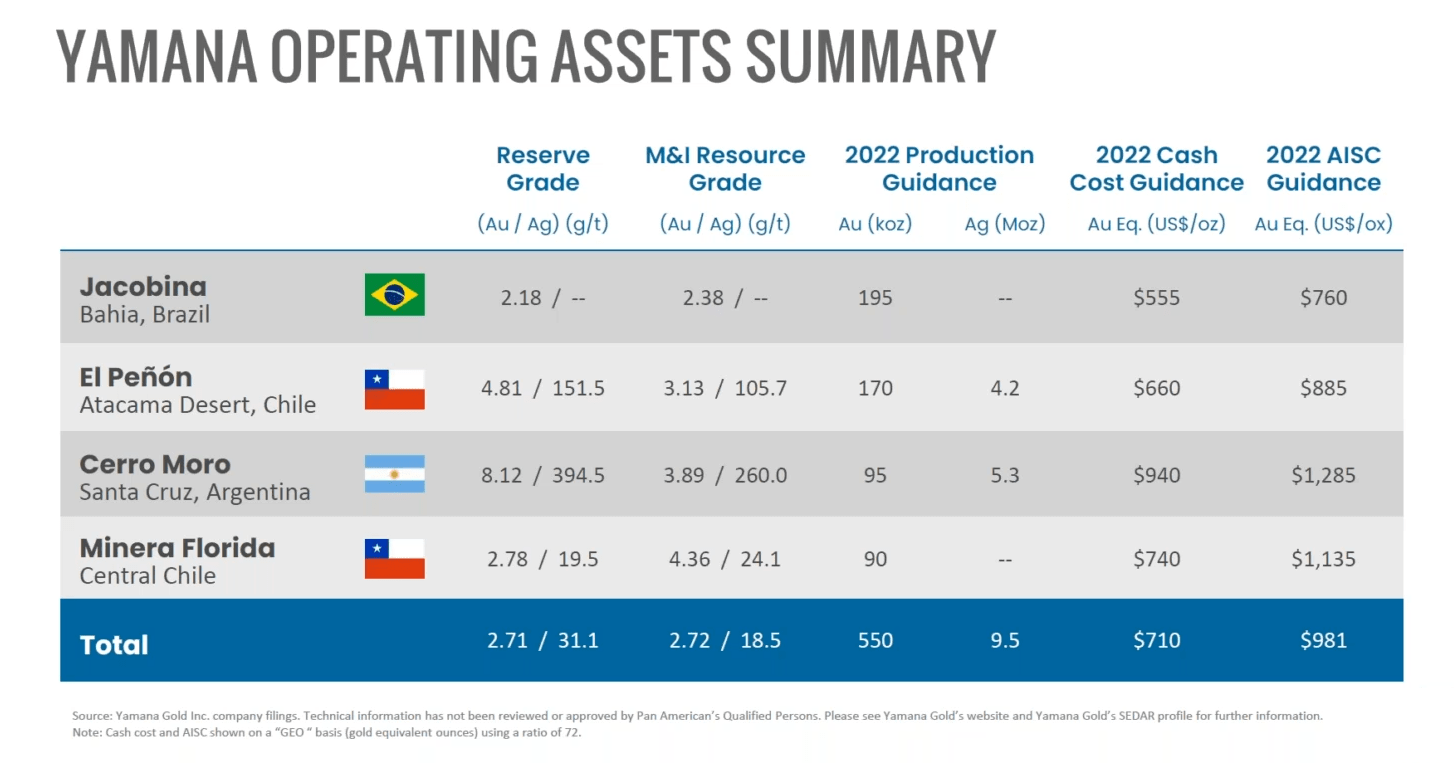

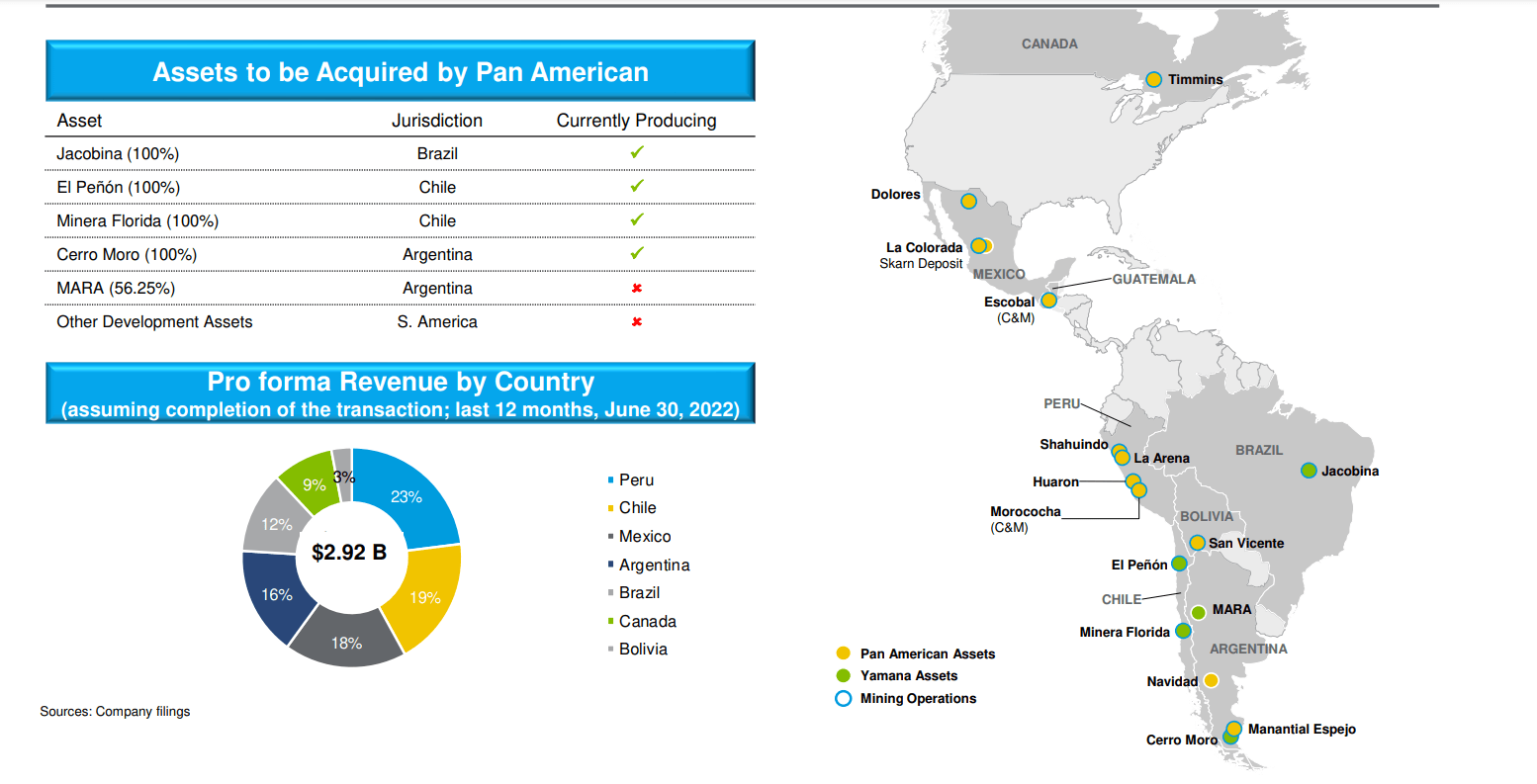

For those unfamiliar with the deal, Agnico Eagle will be acquiring 50% of Canadian Malartic, Wasamac, and three non-core exploration properties as part of the superior Yamana offer, and the company is paying a slight premium to net asset for these assets given their excellent fit in Agnico’s portfolio. Meanwhile, Pan American will be acquiring its Latin American portfolio, which includes multiple operating mines (Jacobina, Cerro Moro, Minera Florida, El Penon), a 56% interest in a major copper-gold development project in Argentina, a development stage gold project also in Argentina (Suyai), and a 57% interest in Jeronimo (part of the Agua de la Falda joint-venture in Chile) Let’s take a closer look below:

Yamana Operating Assets (Company Presentation)

As shown in the image above, the primary rationale for the acquisition is to add an operating mine in a region where Pan American already operates (Cerro Moro in southern Argentina) while adding three other gold mines in neighboring countries to a large portion of its production profile in Bolivia and Peru. These three mines are Jacobina (Brazil), Minera Florida (Chile), and El Penon (Chile). While they may not be in the same country as Pan American’s assets, Pan American will see synergies from regional procurement plus no need for two corporate offices in Canada (Yamana and Pan American). Based on the most recent presentation, Pan American estimates post-tax synergies of $400 to $600 million over ten years.

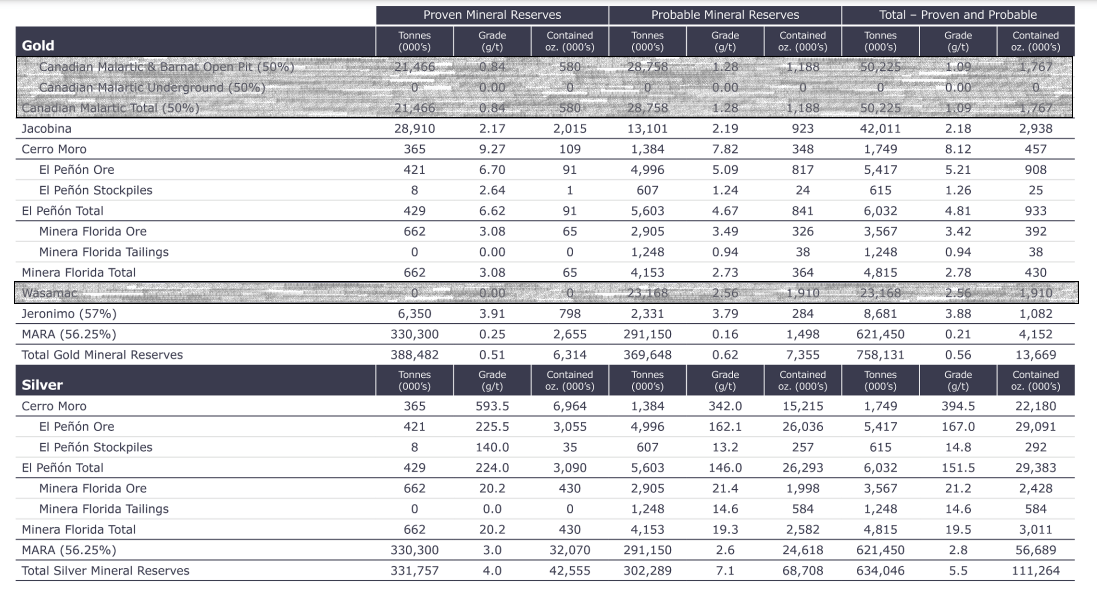

Yamana Reserves (Yamana Presentation)

Looking closer at Yamana’s assets above, Pan American will add ~8.4 million ounces of gold reserves at operating mines and ~5.1 million ounces of reserves at non-operating assets. In addition, it will add ~55 million ounces of silver at operating assets and ~57 million ounces of silver at non-operating assets (56% interest in MARA). This will place Pan American well ahead of its peers in terms of total silver reserves, largely due to Escobal in Guatemala, which is currently in care & maintenance and home to over 260 million ounces of silver. The hope is to restart Escobal, a mine whose license was suspended years ago under Tahoe. If successful, it would produce up to 20 million ounces of silver per annum for Pan American.

Moving over to the gold business, Pan American will see a healthy increase in its gold reserve base, improving from ~3.6 million ounces to ~12.0 million ounces, which doesn’t include non-operating assets non-operating assets like its MARA interest and Jeronimo. Given that its MARA is a large and capex-heavy project being added to an already significant pipeline (Pan American’s Escobal, La Arena Sulphides, and La Colorada Skarn), the company may look at divesting one of these projects given that it can’t possibly develop this massive pipeline which includes Jacobina Complex on its own any time this decade (combined capex for MARA, La Colorada Skarn, La Arena Sulphides likely to come in well over $4.0 billion).

The New Pan American Silver

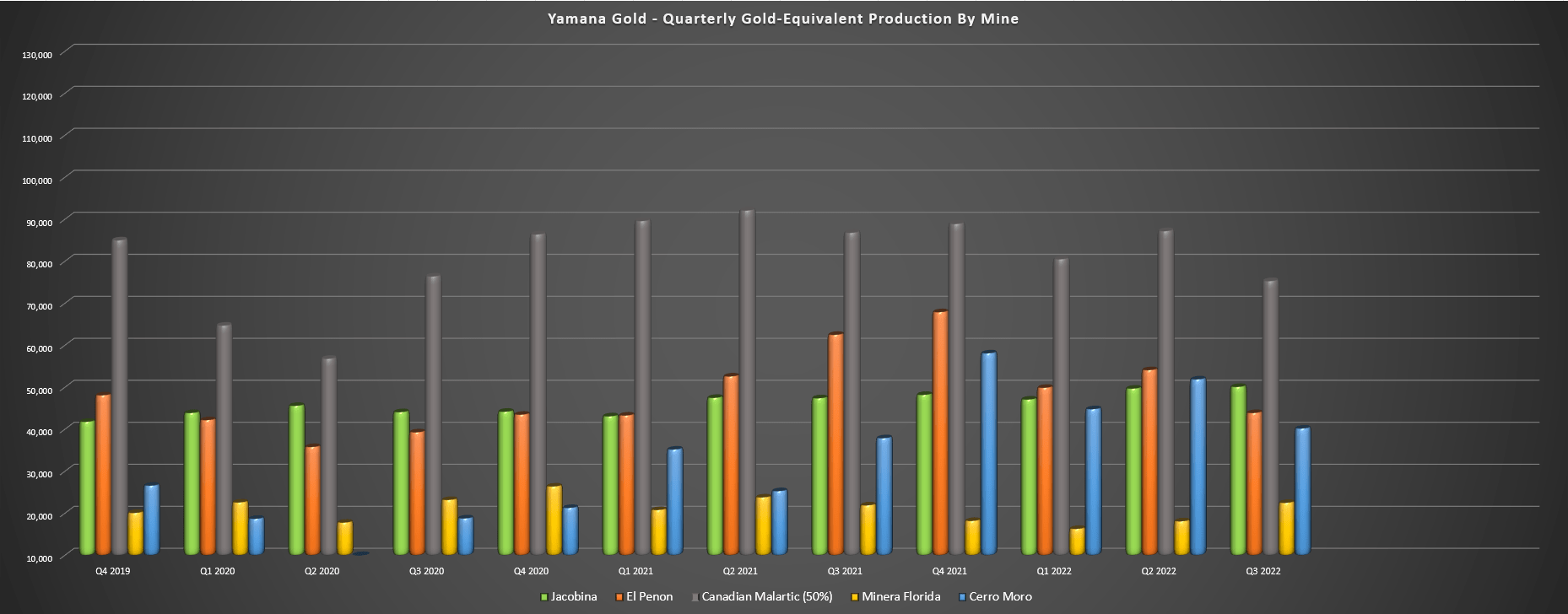

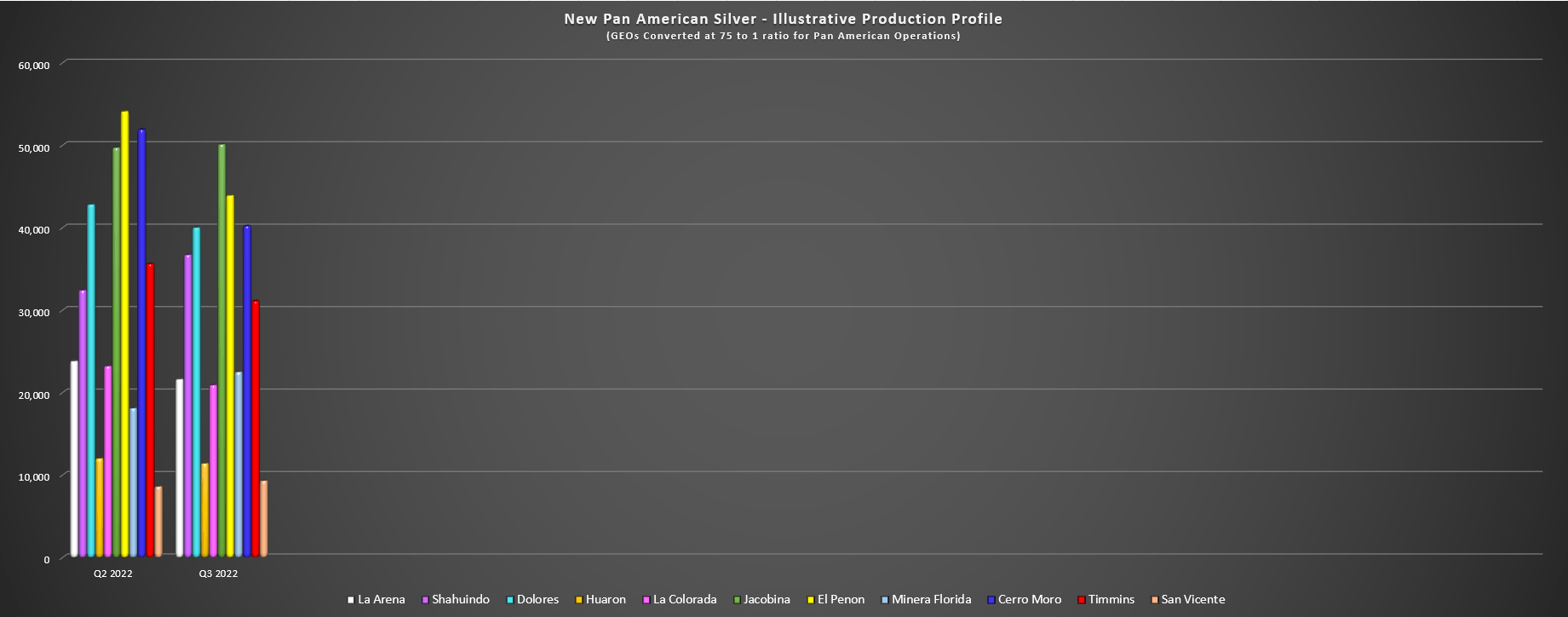

Assuming the deal closes, the new Pan American Silver will look much different and will see a meaningful improvement in diversification from the addition of Yamana’s operating assets. The chart below shows that these assets all have respectable production profiles with ~20,000 to ~55,000 gold-equivalent ounces per quarter, or roughly 700,000 GEOs per annum ex-Canadian Malartic. If we look at the second chart below, we can see what the combined company would have looked like in Q2 and Q3 2022, assuming these assets were in Pan American’s portfolio. As we can see, this creates a more diversified miner that will also benefit from a lower cost profile.

Yamana Gold – Quarterly Production by Mine (Company Filings, Author’s Chart) Pan American Silver – Quarterly Production by Mine (Q2 2022, Q3 2022) if Yamana Assets were in Portfolio (Company Filings, Author’s Chart)

Based on the above production profile, Pan American would have eleven operating assets, placing it in a similar position to Agnico Eagle and Gold Fields in terms of diversification, albeit these are obviously much less productive assets on a per-ounce basis (evidenced by Pan American’s smaller production profile). Still, when operating in some non-Tier-1 jurisdictions, diversification is certainly a key attribute. If Pan American can bring one of its development projects or Escobal online later this decade, this number would increase to 12 or higher, making Pan American one of the most diversified producers sector-wide.

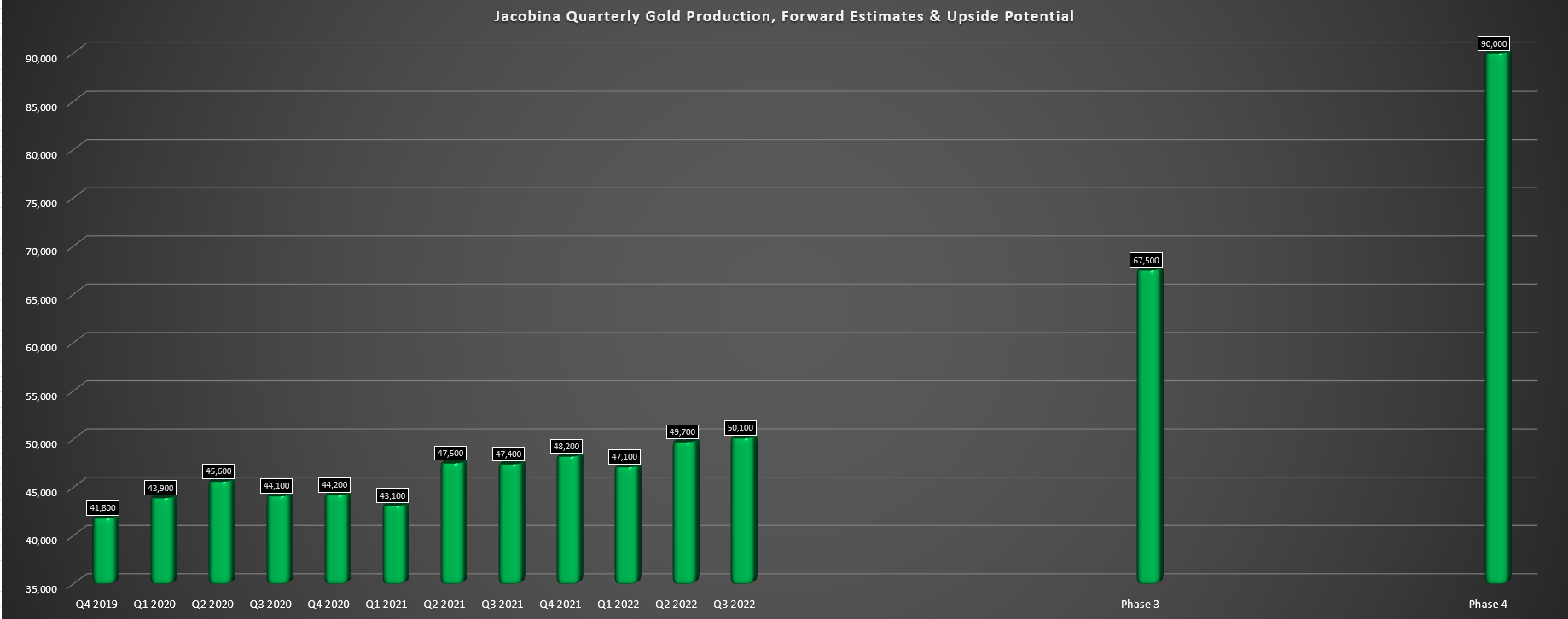

It’s also worth noting that there is considerable upside at existing assets, meaning that Pan American would not need to increase its number of assets to grow production. This includes a massive boost to the production of the La Colorada Mine if the nearby La Colorada Skarn is green-lighted (PEA due 2023), plus steady organic growth at Jacobina if this asset heads toward an ultimate goal of ~15,000 tonnes per day (~350,000 ounces per annum). The below chart shows how Jacobina’s production profile could progress if Pan American approves an expansion to Jacobina, with the potential to produce up to 90,000 ounces per quarter in the back half of this decade once fully ramped up.

Jacobina – Production Profile & Long-Term Potential (Company Presentation)

Meanwhile, taking a quick look at La Colorada Skarn, this is an incredible asset for Pan American Silver. The recent project update highlights a polymetallic resource of ~244 million tonnes with a rock value north of ~$130/tonne if the company chose sub-level caving as the optimal mining method. Assuming a throughput rate of 18,000 tonnes per day (~6.5 million tonnes per annum) and depending on recoveries/payability, this looks like it could be a 20+ million ounce per annum operation on a silver-equivalent basis, making this one of the most attractive silver development projects in North America from a scale standpoint.

It’s also worth noting that recent drill results have extended the high-grade silver zone since the resource update, with a highlight intercept of ~194 meters at 48 grams per tonne of silver, 0.21% copper, 2.97% lead, and 4.26% zinc or a rock value of ~$390/tonne for this intercept. As it stands, it’s tough to pin down how this project could look if it is green-lighted, given that much more work needs to be done to determine the best way to mine this project. However, in the most recent Conference Call, Pan American’s COO, Steve Busby, noted that the high-grade zone could provide the opportunity to use long-hole stoping in the earlier years, which would have a lower throughput rate than sub-level caving, but benefit from significantly higher grades.

To summarize, Pan American already had a very impressive pipeline it wasn’t getting much credit for (La Arena Sulphides, Escobal restart, La Colorada Skarn), and this development pipeline has seen a further boost with the addition of Yamana’s development assets.

Putting It All Together

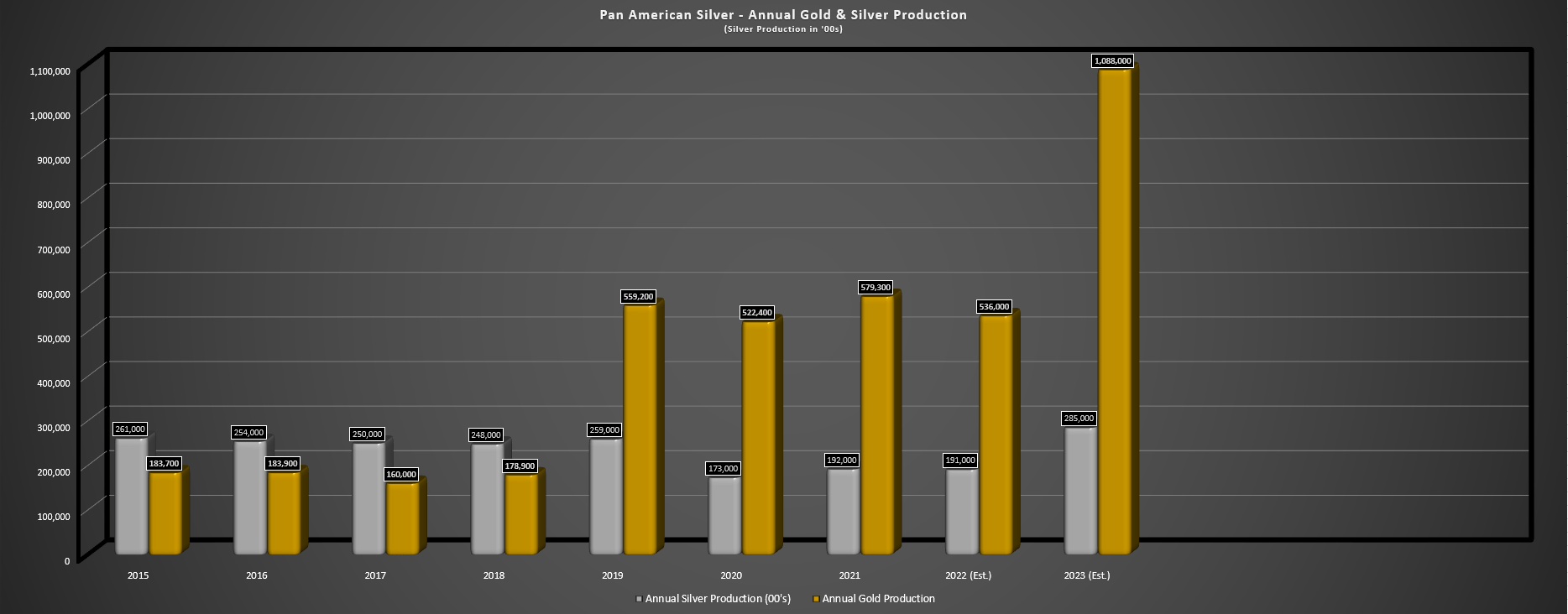

If we put these production profiles together and look at potential 2023 production, Pan American should see annual production of 28+ million ounces of silver and ~1.08 million ounces of gold, moving it into the million-ounce producer space on a gold basis with a hefty silver component as well. While the company may appear to have shed its silver status with the significant growth in gold production, it’s worth noting that Escobal alone could push Pan American’s long-term silver production above 45 million ounces, and La Colorada Skarn would also provide a very significant boost to production. Hence, unlike Fortuna Silver (FSM) which is overdue for a name change with less than 20% of revenue from silver once Seguela reaches commercial production, PAAS’ silver percentage of revenue may have dropped to nearly 25%. Still, its pipeline could lead to a meaningful improvement in this ratio.

Pan American Silver – Annual Gold & Silver Production + 2023 Potential (Company Filings, Author’s Chart & Estimates)

Meanwhile, from a jurisdictional standpoint, Pan American will have a much more significant presence in Central and South America, which would grow further, assuming Jacobina Phase 4 is approved and Escobal comes online. However, it will continue to have a meaningful production profile in North America with its largest silver producer La Colorada, the potential development of La Colorada Skarn, Dolores, and its Timmins operation in Canada. The result is that Pan American will be very well-rounded from a diversification standpoint with multiple countries and assets, significantly reducing the impact of any potential issues at a single operation. Let’s take a look at the valuation:

Future Portfolio & Jurisdictional Profile (Company Presentation)

Valuation

Based on ~364 million shares and a share price of US$16.80, Pan American will have a market cap of $6.12 billion (assuming the deal goes through), a very reasonable valuation for a producer with a production profile of ~1.5 million gold-equivalent ounces [GEOs]. This is especially true given that Pan American would have a phenomenal pipeline that isn’t reflected in its current production that would include:

- a controlling interest in the massive MARA Project (Argentina)

- the La Colorada Skarn polymetallic deposit (Mexico)

- the La Arena Sulphides gold-copper project (Peru)

- the ~20 million-ounce per annum Escobal Mine (Bolivia)

- an enviable organic growth profile at the low-cost Jacobina Mine (Brazil)

Lastly, it’s important to note that these are brownfields assets or already built (Escobal and Jacobina) that benefit from existing infrastructure, making them much more attractive than other undeveloped assets globally.

Comparing this market cap figure to an estimated net asset value of ~$6.9 billion (10% discount rate for Escobal and 5% for other assets) leaves Pan American trading at a discount to its net asset value. Based on what I believe to be a fair multiple of 1.20x P/NAV to reflect its strong gold assets and silver exposure partially offset by limited exposure to top-10 jurisdictions, I see a fair value for Pan American of ~$8.3 billion or a fair value of US$22.80 per share. If we measure from a current share price of US$16.80, this translates to a 36% upside from current levels despite the recent rally in the stock.

Given that I require a minimum 35% discount to fair value to justify starting new positions in large-cap precious metals names, Pan American Silver is not in a low-risk buy zone currently, with the low-risk buy zone coming in at US$14.80 or lower. Hence, I am not long the stock currently and have chosen to focus on other names for the time being with deeper discounts to fair value, such as Sandstorm Gold Royalties (SAND), which trades at a similar P/NAV multiple to Pan American despite a lower risk business model (higher margins, inflation-resistant, superior diversification). That said, if Pan American were to pull back toward its November lows, I would strongly consider starting a new position in the stock.

Summary

While I believe that Agnico Eagle got the better part of the AUY deal and will see less post-acquisition hangover given that it is consolidating an existing asset with minimal share dilution and no added complexity, this is a transformational deal for Pan American. In fact, I can’t think of a better choice from an acquisition standpoint with a fair price paid to acquire solid assets that provide it with improved diversification, an increase in its net asset value, and margin expansion. Additionally, Pan American could reduce its leverage ratio by divesting MARA, given that it has a lot on its plate from a capex standpoint, with four monster projects in the wings and a significant expansion at Jacobina.

To summarize, I see this as an intelligent move by Pan American that will elevate the company to the upper ranks of the million-ounce producer space by 2026 and right near Northern Star (OTCPK:NESRF) and Endeavour on a GEO basis, with further growth to nearly ~2.0 million GEOs if Escobal can move back online. So, with improved diversification, a more respectable margin profile, an improved [E]SG profile due to Yamana’s relatively low greenhouse gas emissions, and a very impressive pipeline, I would expect any sharp pullbacks below US$14.80 in PAAS to provide buying opportunities.

Be the first to comment