Opla

Investment Thesis

This article is mainly about the close connection between Rio Tinto (NYSE:RIO) and China. I will take a closer look at the current Chinese developments. Based on this, I think the chances are relatively high that a reopening of the Chinese economy will be very positive for the Rio Tinto share.

Company overview

A British group of investors bought Rio Tinto in Spain in 1873. Rio Tinto means “red river,” and that name came from the red of the copper mined in southern Spain at that time. Today, Rio Tinto is now one of the largest mining companies in the world. By signing the Paris Climate Agreement in 2015, the company decided to withdraw from the extraction of fossil fuels altogether. In the course of this, the last Australian coal mines were sold in 2018 for $3.95 billion. Today they sell a range of minerals, including iron ore, aluminum, copper, gold, uranium, silver, diamonds, and titanium. Furthermore, they operate processing facilities, power plants, and port and rail infrastructure across twelve countries.

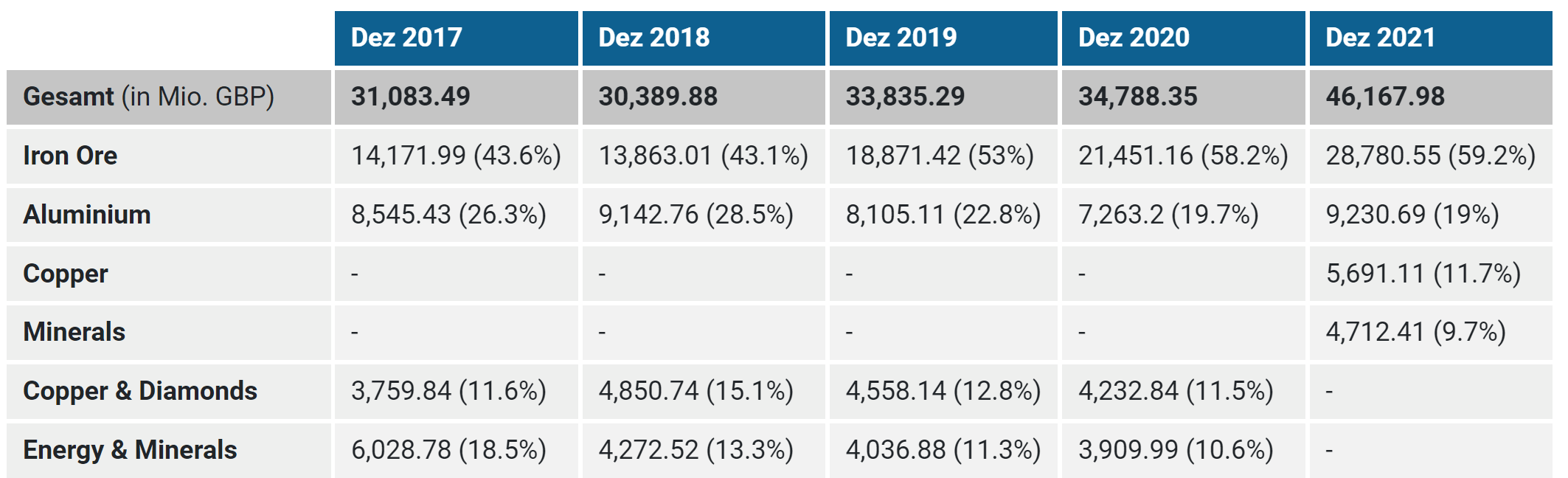

Revenue by segments

Sales by segment show that iron ore is the most important segment and has increased strongly in recent years while Aluminum has remained constant. In the illustration below, copper has only been listed separately since 2021, but it can be seen that it is gaining importance and contributed 11.7% of sales in 2021.

Aktienfinder

Why Rio Tinto needs Asia

The following chart shows the sales development of Rio Tinto by region. We can see that since 2017 sales in China have doubled, and China is by far the most important market. For Japan and Europe, sales remained constant. Overall, Asia accounts for 75% of sales, and the trend is upwards.

Aktienfinder

A closer look at China

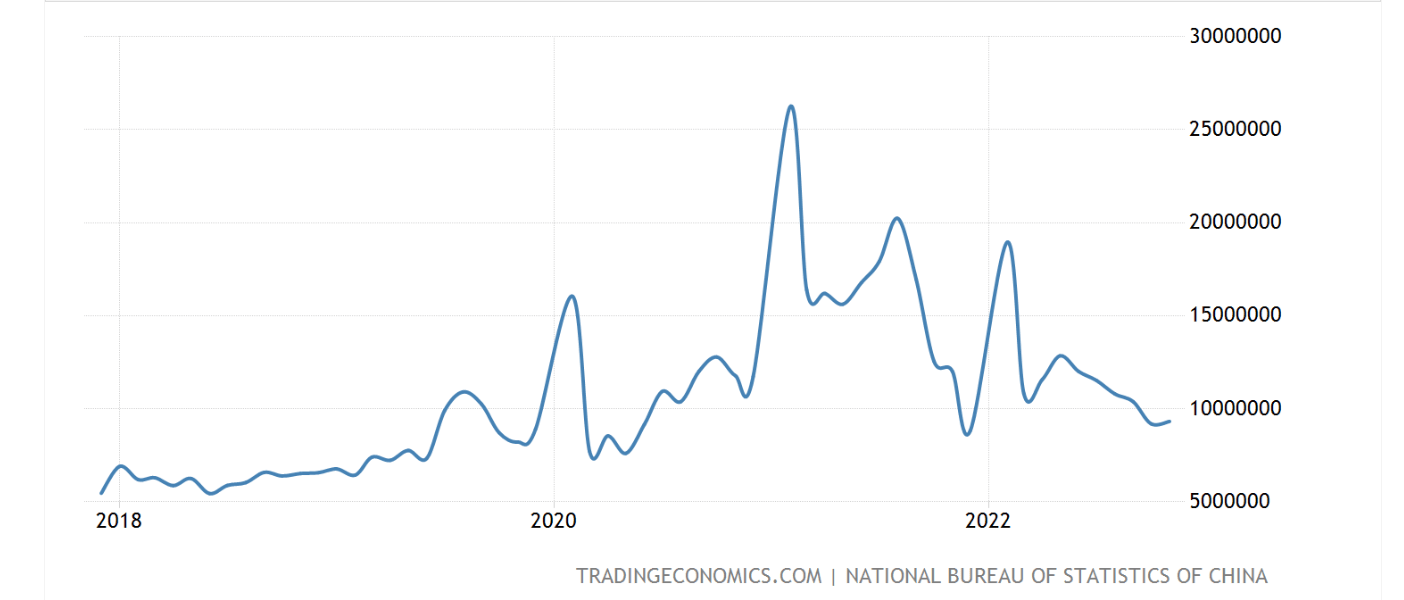

As I said, iron ore is Rio Tinto’s most important product. And China is by far the largest importer of iron ore. Around 70% of global production goes to China. In summary, the success of Rio Tinto depends very much on Chinese iron ore demand. The following chart shows the development of Chinese imports. We see here how these have fluctuated strongly since the beginning of the pandemic and are currently at a rather low level, significantly lower than at the beginning of the pandemic but still higher than in 2018.

tradingeconomics.com

The chart below shows the price of iron ore. The parallels with Chinese demand are certainly no coincidence.

tradingeconomics.com

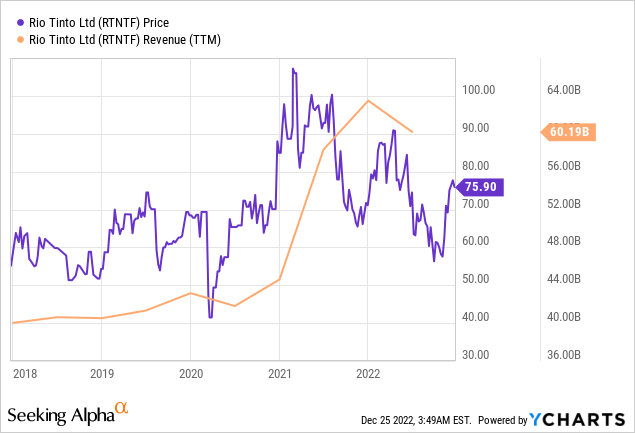

Iron ore had its peak price at the beginning of 2021. If we now compare this with a revenue graph of Rio Tinto, we can see how this has led to a delayed revenue peak at Rio Tinto. Since prices are currently significantly lower, it is no surprise that in 2022 the company will suffer a decline in revenue, and the same is expected for 2023.

The graph above shows a sharp increase in the share price in the last two months. I strongly suspect this is also related to the sharp rise in the previous two months of the iron ore price (see the iron ore graph above). The hope lies in reopening the Chinese economy, which should come through an increased lifting of the zero-covid policy. This would lead to an increase in Chinese demand and, thus, to higher prices.

We do not know precisely what is happening in this vast country. The official covid numbers are in the five-digit range, but there are rumors of extremely high covid numbers. For the Chinese economy, perhaps even the second case would be better because it would lead to a very fast natural immunization, the process that has taken two years in all other countries of the world and now makes the pandemic virtually irrelevant. China has closed itself to this natural immunization process but could now catch up quickly. In this case, it could be that in 2023 the Chinese economy can take off again.

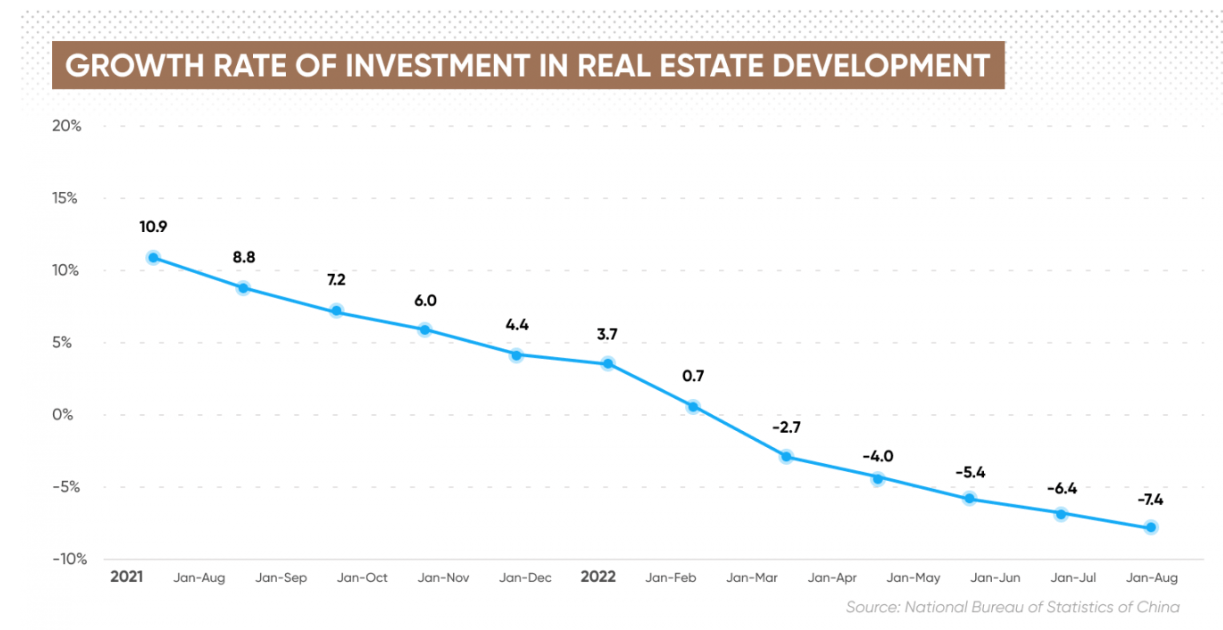

However, there are more problems in the Chinese economy. A massive real estate crisis also hit the country last year. One-third of China’s steel demand comes from the real estate sector. This year, investment in the real estate sector has already fallen sharply.

capital.com

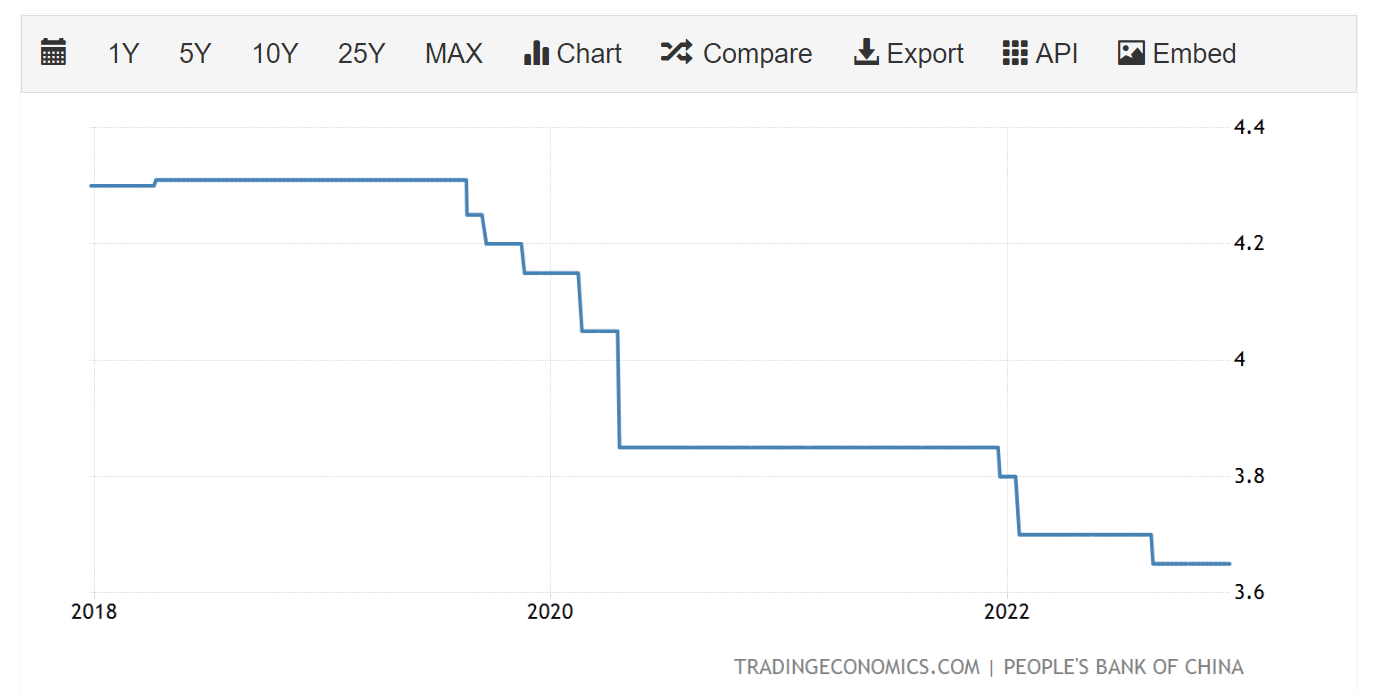

The Chinese central bank has tried to counteract the economic slowdown and is acting against the trend of interest rate hikes. On the contrary, it has tended to further lower interest rates. However, they are still far from the zero interest rates we have seen for years in the West.

tradingeconomics.com

My conclusion and outlook for China

All that said, I believe the following scenario is the most likely. The Chinese government has been forced by the population and the deteriorating economic data to lift the zero covid policy. This will result in a massive number of Chinese becoming infected with covid in the coming weeks and months. But, as in every other country, natural immunization will end the pandemic. After that, the Chinese government will do everything it can to revive the economy, which is ultimately the most important thing for the country’s long-term goals. These are to become a leader in all necessary technologies and eventually to displace the USA as the world power.

In addition, other factors suggest that iron ore, aluminum, and copper prices will remain high. For one, Ukraine was the fifth largest exporter of iron ore in 2021. Furthermore, there are the Russia sanctions. Russia was the second-largest aluminum exporter in the world in 2021. Indeed, only a small part of the world (the West) has imposed sanctions on Russia, causing severe market dislocation and inefficient trade routes. And the last point I want to mention here is that the copper demand will increase strongly in the future as for the energy transition, large quantities are needed. There are already reports that demand is higher than supply.

All these factors also explain why iron ore prices are still relatively high despite all these Chinese problems. Conversely, iron ore prices could rise sharply if China’s demand picks up again and these other factors remain negative.

Valuation

The valuation question here is relatively difficult because sales are closely linked to commodity prices. However, I think that estimates for 2023 are pretty accurate, as even a sudden increase in iron ore prices would only lead to significant revenue increases for Rio Tinto with a delay. The same is true not only for iron ore but also for aluminum and copper.

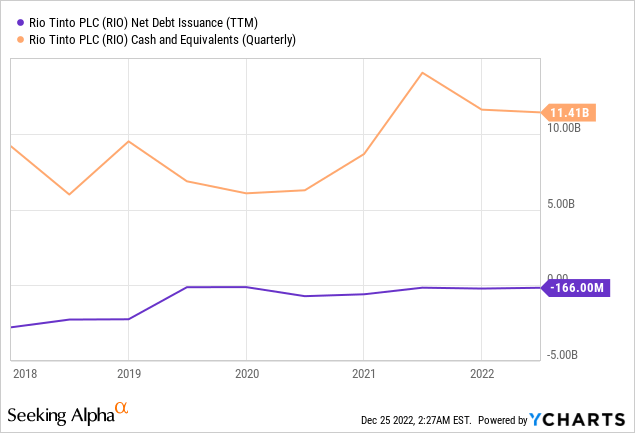

The company is currently valued at an enterprise value of $121B. The market cap is $ $116B, and the total debt is $12B. The company has been repaying debt for years while the cash position has improved.

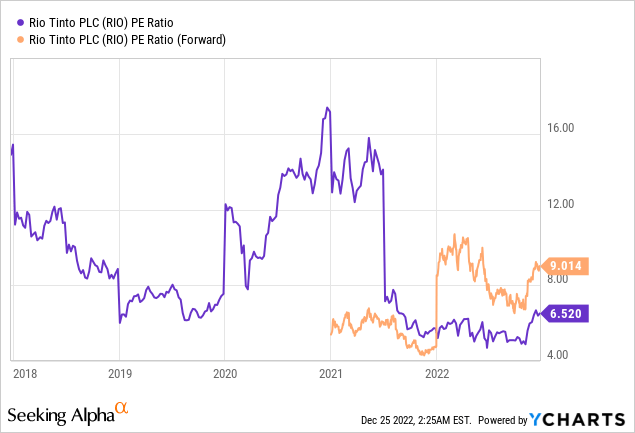

On a P/E basis, we can see that the company is currently trading at the lower end of historical valuations. However, the forward P/E is higher as analysts expect EPS to decline next year.

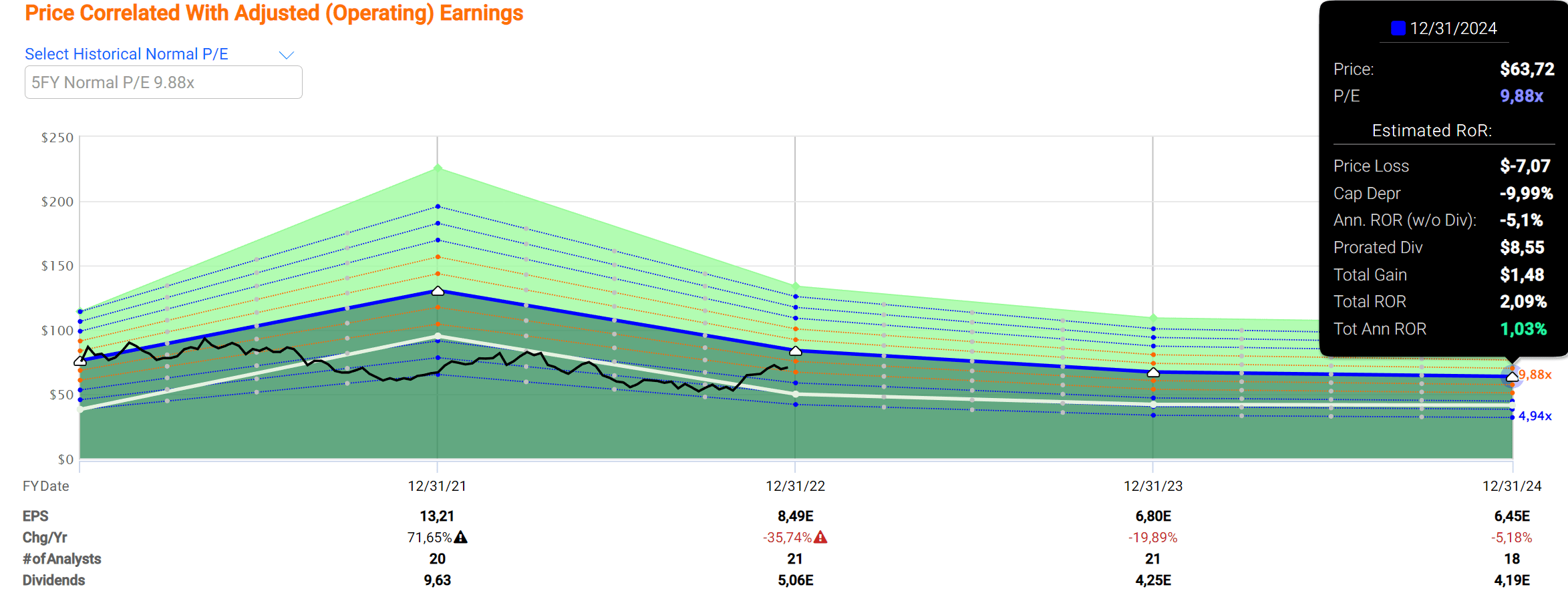

According to FAST Graphs, if the stock is trading at its average P/E of 9.8 again by the end of 2024, we can only expect a one percent annualized return. This estimate is mainly due to the market’s assumption of declining EPS and, thus, decreasing dividends.

FAST Graphs

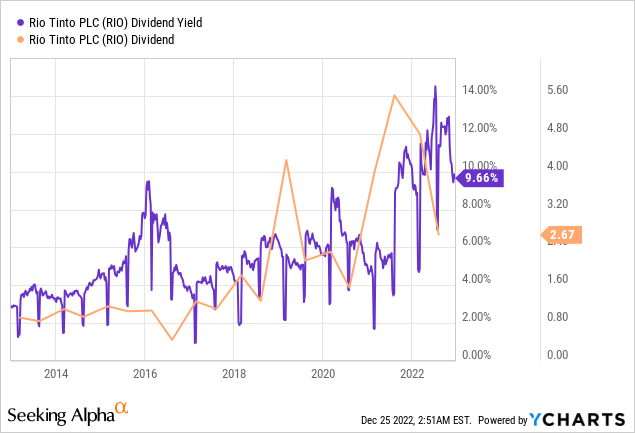

The company is particularly popular with dividend investors. These 10-year charts show that the payout per quarter fluctuates strongly, but the trend is upward. And since the stock is currently trading at a relatively low P/E ratio, the dividend yield is correspondingly high. The last dividend was $2.67 and even higher in the quarters before. Assuming the dividend is cut another 25% to an average of $2 semiannually, the future dividend yield would be 5.6% ($4 annual dividend at a $71 share price).

Risks

The main risk is relatively clear based on everything I have written in this article. If Chinese demand remains low, this will tend to keep the iron ore price low. This could happen for many reasons. I may be wrong in my assessment of natural immunization. Maybe covid will continue to be a big problem in China. Perhaps the real estate sector will not recover or crash even further.

China’s economic development affects the whole world, especially its direct Asian neighbors. Since 75% of Rio Tinto’s sales are in Asia, a continued weak Chinese economy would significantly impact demand for raw materials and, thus, on Rio Tinto’s sales. The company would still be profitable and pay dividends, but the share price could fall significantly in this case.

Although this article was almost exclusively about China, the USA also plays a role. Lower demand in the USA due to a recession would also have an influence. However, I have limited myself to China because these factors are much more important for Rio Tinto than the developments in the USA and Europe.

Share dilution and insider selling

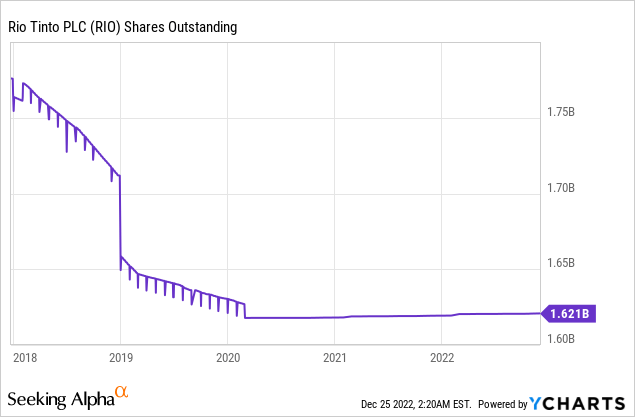

I always want to look at stock dilution and whether there is insider selling. Overall, we can see that the outstanding shares have been trending downward for five years, even though there have been no major changes since mid-2020. I have not found any information about insider sales.

Conclusion

My rating for the share is positive. I arrive at this assessment for several reasons:

- the current historically low valuation already prices in the expectation of lower commodity prices (but I have doubts about that)

- I think there´s a good chance that iron ore prices will rise due to the Chinese economy

- probably Ukraine will not be an exporter for the time being

- Russia sanctions lead to all sorts of distortions

- copper will remain in high demand in the long term

- even with lower revenues, the share would still have a high dividend yield.

Therefore, I believe the chances are relatively high that commodity prices will remain unexpectedly high. Analysts assume that Rio Tinto’s EPS will fall, but if this turns out differently, the share has excellent potential to climb back to its all-time high ($90).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment