Sladic/E+ via Getty Images

Investment Thesis

Apple (NASDAQ:AAPL) is primed for a sell-off. Not from its own doing, but because the global economy is slowing down. I highlight examples of companies that describe how the near-term macro outlook has weakened more than expectations.

I then remind readers about the global cost of living crisis, leading us to put a spotlight on Europe.

Next, I explain how the Wall Street game is played and how one should think about it as a passive shareholder.

Also, I emphasize how paying more than 20x forward earnings for a company growing its bottom line at close to 6% to 7%, does not provide investors with a margin of safety.

Finally, this is not a hard-sell article. But I do hope to provide food for thought about the underlying issues facing Apple for your attention before it’s too late.

Companies Shed a Light on Their Outlook

In the past several weeks we’ve seen companies that have their fingers on the macro environment declare that things are slowing down. I’m not talking about small shops that are making bearish calls to make a name for themselves.

I’m referring to global companies that want to do everything in their power to ensure that their stock stays up, but are having to mitigate carnage to their stock by getting ahead of the Street.

For example, FedEx (FDX) noted recently that its experienced macro weakness and has been forced to withdraw its fiscal 2023 forecast, stating,

Global volumes declined as macroeconomic trends significantly worsened later in the quarter, both internationally and in the US.

FedEx is an example of a company that has insights into global logistics and how things on the ground really are performing.

Another company that has recently acknowledged that things in the near term are challenging is Nvidia (NVDA), noting at a conference that the company has in the near-term witnessed a supply glut.

We took action immediately to also reprice price programs to move this inventory through.

Semis are a leading indicator of macro demand. Even if Nvidia then notes that next year things will be better.

Next, Ford (F) describes some of its supply chain woes as around 40K vehicles lack parts, forcing the company to downwards revise its next quarter’s guidance. Even though Ford felt that it could brave it through and reach its full-year guidance for the year.

Next, ArcelorMittal (MT) describes how weak demand for steel together with prohibitively high energy costs in Europe have caused the company to idle some of its plants.

These are not sensational comments seeking to spark controversy. I’m confident that you’ll agree that the selection I’ve mentioned is broad and representative of the underlying reality of what these different sectors are facing.

But what’s that got to do with Apple?

Global Cost of Living Crisis

Realistically, one way or another, the Fed needs to cool down the US economy. And I’m not in a position to speak outside of my depth about whether or not the Fed succeeds with its soft landing or not.

What I can easily see from the countless companies that I follow are seeing demand is rapidly falling. There’s softness everywhere. Even in unexpected places such as ServiceNow (NOW) whose platform is used by 50% of the Fortune 500 global blue chips. ServiceNow’s customers are the blues of blue chips, with the most financial resources. And yet, ServiceNow is seeing its sales cycles elongate.

Next, Alphabet’s (GOOG)(GOOGL) advertising revenues are also being impacted. As companies pull back on their advertising spending given the uncertain outlook that their business is facing.

Meanwhile, consumers across the globe are having to embrace high inflationary pressures at the same time as energy costs are going up. And this is particularly being felt in Europe.

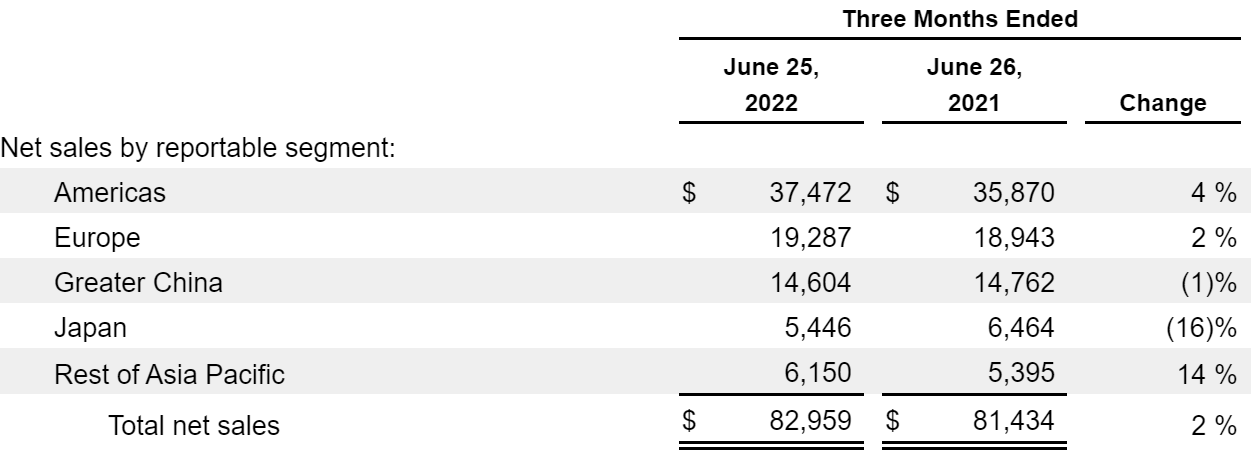

Apple’s 10-Q

As you can see above, Europe had up until the last quarter been a positive contributor to Apple’s revenue growth rates. And now 22% of total revenue is going to be a drag on Apple’s topline revenues.

Apple Stock – Don’t Fall for the Wall Street Game

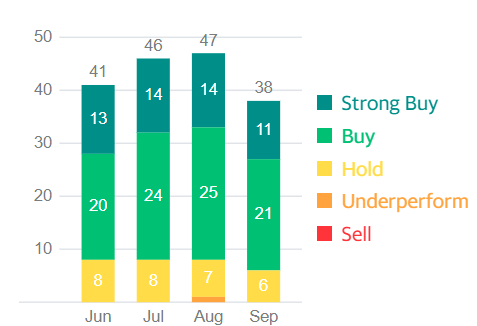

Moving on, most analysts that follow Apple have either a buy or strong buy rating on the stock.

Yahoo! AAPL

That ensures that the analyst house gets access to Apple’s C-suit executives. And they are able to get a feel for the whole supply chain. In essence, there are numerous indirect benefits of having a buy rating on Apple’s stock.

Having an underperforming rating on Apple’s stock is a proxy for a sell rating. And that doesn’t open any doors to the analysts.

Hence, when expectations are so high, where can the stock seriously go from here?

Apple is already being priced at approximately 24x forward earnings. There’s really no way that multiple can stretch much further, in my opinion.

Indeed, even if Apple does match analysts’ expectations, you don’t get a more than 20x multiple on your earnings, when the company’s bottom line is growing at mid-single digits CAGR.

No matter how great a business the company is, no business lasts forever.

So What’s the Takeaway Here?

The easiest thing to do in investing is to say that it will all be okay and to lay back and take solace that one is a long-term investor. A buy-and-hold forever investor.

After all, there are good reasons to stay with Apple. Particularly since it’s one of the few places left in the market that is still relatively untouched by the bear market.

Also, let’s be honest. For many readers, they’ve been hearing about tech being out of favor for more than a year, and given that their holding in Apple has shown no weakness, there’s the belief that somehow Apple will muster through, as it has done this far.

So what am I advocating for? To sell all your Apple stock? No, that’s not what this is about. I can’t predict how things will unfold for Apple. But I do believe that the odds of success from this point are small.

Apple is the final general that’s still holding strong in this market. And with so many passive ETFs being forced to buy Apple, this has meant that the stock has succeeded in chugging along. Incidentally, note that 7% of all passive S&P500 ETF purchases go to support Apple’s share price.

And that has worked out extremely well for Apple holders. But the pieces of the puzzle are now coming together, which will make Apple’s next few quarters not live up to expectations.

And when that happens, the stock will sell off. And when the sell-off starts, there’ll be a large number of institutions that will want to cling to their Apple gains, particularly as they harvest losses elsewhere in their portfolio.

The next group will then start to rethink their own position. Indeed, while the share price is staying strong, nobody asks difficult questions about their investment. It’s only when things go south, that investors ask tough questions.

And then the ETFs pick up momentum too. So what’s my point? My point is this, doing nothing is an active choice! And it may not be the best choice in this case. It’s OK to have a plan to sell some of one’s holdings. It’s not cheating. The stock doesn’t know or care that you own it.

Be the first to comment