naphtalina/iStock via Getty Images

Article Thesis

Apple (NASDAQ:AAPL) has undoubtedly been a strong investment over the last couple of years. But in the current environment, the downside risk could be larger than the upside potential, due to several reasons we’ll lay out in this article. Despite the recent share price decline, investors thus shouldn’t be “greedy” in the current environment. Instead, being “fearful” and staying away could be the better choice.

Why Apple Could Underperform Going Forward

Apple is up by a hefty 280% over the last five years. Clearly, everyone that bought it years ago has made a great choice. But that does not mean that buying today will be a similarly good investment. There are several reasons to believe that things will be different going forward.

Recession And Business Risks

The first reason is that Apple faces considerable risks to its business stemming from both an economic downturn and high inflation. Apple is primarily a consumer hardware company, clearly making it a discretionary consumer goods player. During harsh times, consumers are not saving money by buying less food, fewer cigarettes, or less toothpaste. Instead, they cut back on items that are nice but not necessary – such as a new car, holiday travel, dining at restaurants, or new phones. Many people buy new phones regularly even though their old ones still work – during a recession, that could change. After all, cash-strapped consumers might decide to keep their old phones for a little longer, or they might opt for a cheaper new phone.

To some degree, Apple is protected by the fact that many of its customers have above-average incomes. But that does not hold true for all of Apple’s customers, and even those with solid incomes are feeling the pinch of inflation and an economic downturn today. This summer, it was reported that two out of three Americans are spending their savings, thus even some people with above-average incomes are coming under pressure from a financial perspective. Combine this with increasing interest rates and a worsening macroeconomic picture, and it would not be surprising to see more consumers opt for fewer or cheaper purchases when it comes to discretionary items, which include Apple’s phones, tablets, PCs, etc. Apple’s service business could be better-protected from this trend, as consumers don’t make big single purchases when they opt for a subscription, but in essence, these items are discretionary (not needed) as well, and even though the service business could fare better, the vast majority of Apple’s revenue and profit is generated by the more vulnerable hardware business.

Apple is already forecasted to see its revenue growth drop to a low-single-digit rate over the next couple of quarters, according to the analyst consensus. In real terms, this means a significant revenue decline due to inflation running at a high-single-digit rate. Apple has just announced that it would not add to its iPhone orders, as demand is lower than expected. This makes it likely that Wall Street analysts will revise their estimates downward for the next couple of quarters, as Apple looks like it could underperform current expectations, where lower orders than previously thought were not yet accounted for.

That’s not the only macro issue, however. Apple could also come under pressure from inflation, as expenses rise. This holds true for employee compensation expenses in the United States, where major tech companies such as Apple, Alphabet (GOOG), Microsoft (MSFT), and Amazon (AMZN) are battling over engineers. Earlier this year, Bloomberg reported that Apple was giving out bonuses of up to $200,000 for engineers in order to retain talent. Pay increases for employees naturally increase expenses for Apple. When that goes hand in hand with low or no revenue growth, profits might come under pressure.

Other expenses are climbing as well, including for manufacturing, e.g. due to rising energy costs. Taiwan Semiconductor Manufacturing (TSM), one of Apple’s largest suppliers, is asking for higher payments per chip in the future. So far, Apple doesn’t want to pay that. But since both companies rely on each other to some degree, it would not be surprising if they eventually agree on some price increase, although possibly less than what TSM is seeking.

No matter what, it seems pretty clear to me that Apple is exposed to these macro headwinds. Profits will not fall off a cliff, of course. But even stagnant profits would be an issue when we account for high inflation, and it would also not fit well versus the current rather high valuation Apple is trading at, which gets us to the next point.

Apple Is Historically Expensive

Total returns are driven by underlying growth and shareholder returns. But valuation plays a role as well, due to the potential for multiple expansion and multiple compression. Buying companies when they trade below the normal range is thus a good idea, as it increases the upside potential for investors and as it reduces downside risk. On the other hand, buying at historically high valuations reduces the share price upside, as multiple compression is more likely than further multiple expansion. When shares are bought at a historically high valuation, the downside risk is more pronounced as well, making this a risky choice.

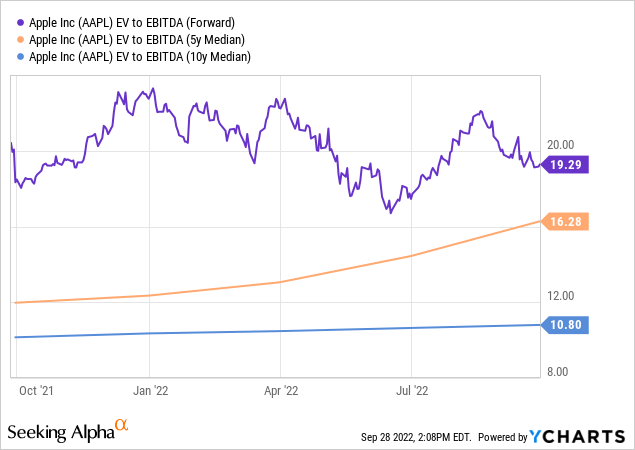

Apple is a company that is currently trading well above the historic norm:

Apple currently is valued at more than 13x forward EBITDA. That’s a pretty high valuation in absolute terms, considering Apple is an established company that’s not growing fast any longer. Even worse, the current valuation is way higher than it used to be in the past. Apple is trading at a 79% premium versus the 10-year average valuation. Even relative to the 5-year median, Apple is currently expensive. Interest rates have risen considerably in recent months, which should, in theory, lead to lower valuations for equities due to higher discount rates. Apple is thus historically expensive at a time when equities should become less expensive than they used to be in a zero-interest-rate-environment.

I believe that this means two things: First, Apple is at risk of seeing its valuation compress substantially. A reversal toward the historic norm would result in steep losses for investors. Even if that does not happen, it seems likely that future returns will be limited. Secondly, a stock’s valuation can’t increase forever, especially not in a recessionary environment where interest rates are climbing. Multiple normalization should offset some of the underlying growth Apple will generate in the future. In the past, buying Apple at or below the historic valuation norm worked very well. Buying it at historic highs will not work as fine, I believe. Five years ago, Apple was trading for 11x EBITDA – it was inexpensive in absolute terms and not historically expensive. Those that bought back then have benefitted from massive multiple expansion tailwinds. But the same will most likely not happen for those that buy here, as Apple is trading well above the historic norm right now, making further multiple expansion rather unlikely, I think.

It’s also important to note that the high valuation works against investors when it comes to share repurchases. Those were very effective at creating shareholder value when Apple was trading at half the current valuation. Today, shares have to be bought back at a pretty high multiple, meaning buybacks are less efficient and the positive impact on earnings per share growth will be diminished.

Apple Has So Far Not Fallen As Much As The Market

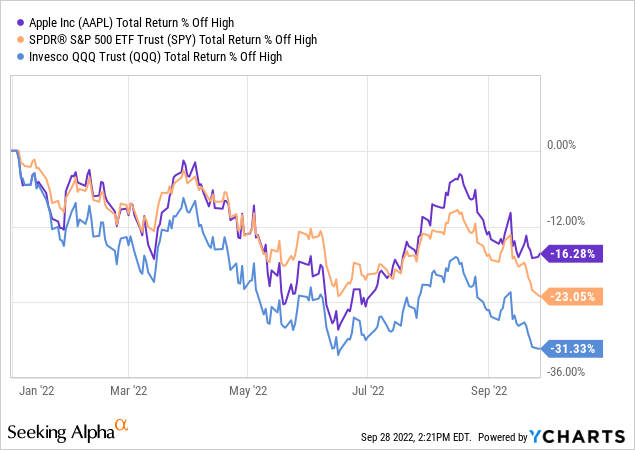

I believe that there’s a third reason to not be too optimistic when it comes to Apple’s near-term share price potential. The stock has declined versus recent highs, but not too much. In fact, Apple has outperformed the broad market:

From this year’s highs, Apple has declined by 16% so far. The broad market has dropped by 23%, while the tech-heavy Nasdaq index (QQQ) has dropped by a hefty 31%. Apple’s outperformance is positive for current holders, especially for those that are looking toward locking in gains. But I do believe that the less pronounced fall in AAPL’s stock, relative to the broad market, makes it less appealing for new buyers. After all, the best deals are made when stocks have dropped a lot. That is the case for a wide range of other equities, including many tech stocks. But since Apple has not dropped much, we don’t really have a pronounced buying opportunity here. Apple’s valuation also has declined less than that of the broad market, which could mean that it has further to fall in the coming weeks.

Apple repeatedly dropped by 30%, 40%, or even more from its highs over the last decade. Following these drops, it was always a great buy. But such a drop has not yet materialized here. In case it does, current holders would see significant share price declines – and those not buying today, when AAPL is still trading at a historically high valuation, could get a much better buying opportunity down the road.

Final Thoughts

Apple is a quality company, that is pretty clear. But even quality companies can be bad investments when bought at the wrong price/valuation. Microsoft during the dot.com bubble is a great example of that – despite great margins, great returns on capital, strong growth, and a clean balance sheet, MSFT saw its shares drop massively when the bubble burst.

Apple is not as overvalued as MSFT was back then, but Apple undoubtedly is expensive. Despite weak expected growth, Apple trades at a premium to the market. And even more telling, it is way more expensive than it used to be.

Since Apple is not immune to a recession and inflation, I do believe that it is not a good investment at current prices. Shares have not dropped a lot yet and are not at all a bargain at current prices, which is why “fear” seems more appropriate than “greed”.

Be the first to comment