Feverpitched

Investment Thesis

Apple’s (NASDAQ:AAPL) throne as the world’s most valuable company seems a little shaky, with the onslaught of negative news thus far. The company had to cut its iPhone 14 production output by -6.66%, back to its original plan of 90M handsets, similar to previous releases. On one hand, we expect some of those headwinds to be well balanced by the robust demand for its premium models, compensating for the lost volume with higher margins. On the other hand, it is apparent that the rising inflation, record high oil/gas prices, China’s economic slump (one of AAPL’s best markets), and geopolitical issues in the EU are impacting consumers’ discretionary spending, with the global smartphone market expected to deflate by -6.5% in 2022 to 1.27B units instead.

It remains to be seen if the Cupertino giant will suffer financially during this economic downturn, since the previous recession in 2008 had impacted AAPL’s top and bottom lines growth to a certain extent. The company reported a notable YoY growth of 14.4% in revenues and 34.69% in net incomes for FY2009, compared to 52.5% and 75.07% in FY2009. The recessionary impacts were considerably mild then, since consumer discretionary spending remained relatively robust for the company.

Nonetheless, we are already starting to see some stock weaknesses. AAPL has continuously failed to break its resistance level at the $180s and, consequently, lost -22.10% of its value from its peak levels in March and August 2022. The S&P 500 Index had also plunged by -24.10% YTD, indicating peak market pessimism and fear levels. During the previous recession, both stocks had tanked, with AAPL reporting a -52.21% plunge and the S&P 500 a -43.37% plunge between August and December 2008.

However, all hope is not lost, since the September CPI released in early October may provide the potential catalyst for the stock market’s recovery, due to the Fed’s projected terminal rate of 4.6% by 2023. This potentially indicates a 75 basis point hike in November, with January 2023 moderating with a 50 basis point hike. Therefore, we may speculatively assume that most of the pessimism is already baked in, barring an earnings miss ahead. We shall see.

Mr. Market Is Still Hopeful About This Last Frontier

S&P Capital IQ

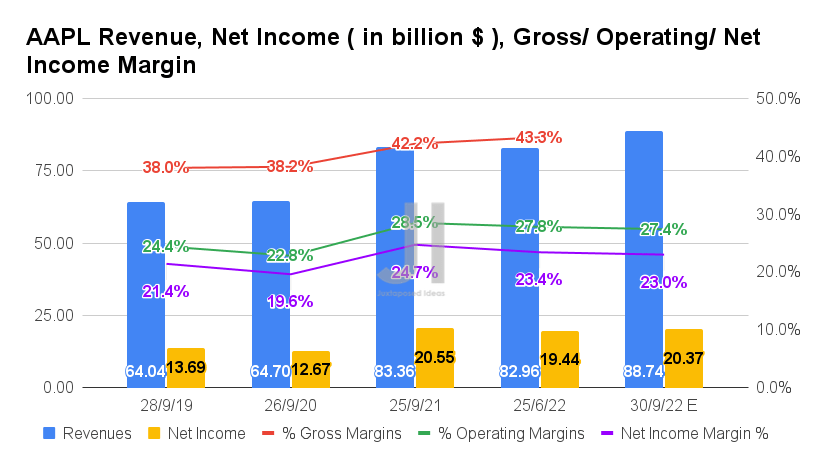

For FQ4’22, AAPL is expected to report revenues of $88.74B and operating margins of 27.4%, representing an increase of 6.96% though a moderation of 0.4 percentage points QoQ, respectively. Otherwise, an increase of 6.45% and a decline of -1.1 percentage points YoY, respectively, with the latter attributed to the rising costs. It remains to be seen if AAPL will be able to achieve its previous guidance of accelerated sales and gross margins between 41.5% to 42.5% for FQ4’22.

In contrast, consensus estimates that AAPL will report net incomes of $20.37B and net income margins of 23% for the upcoming quarter, indicating certain headwinds to its profitability, with a minimal increase of 4.78% and a decline of -0.4 percentage points QoQ, respectively. Otherwise, a notable decline of -0.87% and -1.7 percentage points YoY, respectively. With an estimated EPS of $1.27 for FQ4’22, AAPL would be looking at a decent 5.83% QoQ and 2.07% YoY growth. It might just be enough to satisfy Mr. Market’s highly pessimistic outlook, preserving its cult stock status ahead.

S&P Capital IQ

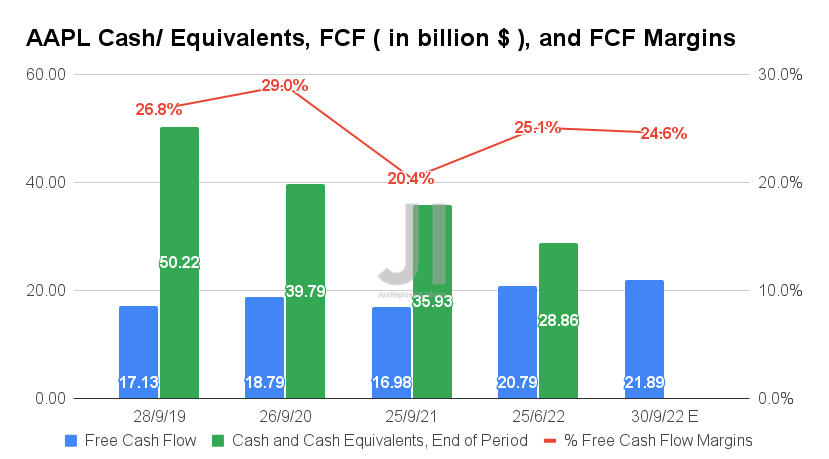

Nonetheless, Mr. Market is cautiously confident about AAPL’s projected cash flow, with a Free Cash Flow (FCF) generation of $21.89B and an FCF margin of 24.6% in FQ4’22. It indicated a decent improvement of 5.29% and -0.5 percentage points QoQ, respectively. Otherwise, massive YoY growth of 28.91% and 4.2 percentage points, respectively. AAPL’s chances of success would be higher as well, assuming aggressive cost cuts across the board. We shall see, given the historical trend of elevated capital expenditures thus far, especially in FQ4s.

S&P Capital IQ

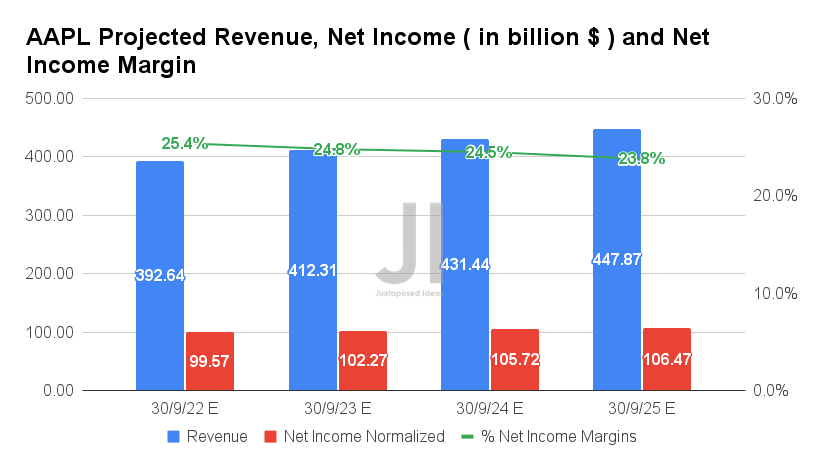

Over the next four years, AAPL is expected to report revenue and net income growth at a CAGR of 5.19% and 2.98%, respectively. For now, Mr. Market remains somewhat positive, since these long-term projections and FY2022 estimates remain in line since our previous analysis in August, though slightly discounted by -2.9% since May 2022. Its upcoming earnings call will make or break AAPL’s stock performance, as the EU enters its first winter without Russian gas and the Feds continue to fight against the rising inflation through 2023.

In the meantime, we encourage you to read our previous article on AAPL, which would help you better understand its position and market opportunities.

- Apple Vs. Meta: Battle Of The Mixed Reality

- An Apple A Day Keeps The Portfolio Healthy (And Potentially, Recession At Bay)

- Can Apple Be The New Tesla – Smartphone On Wheels By 2025?

So, Is AAPL Stock A Buy, Sell, Or Hold?

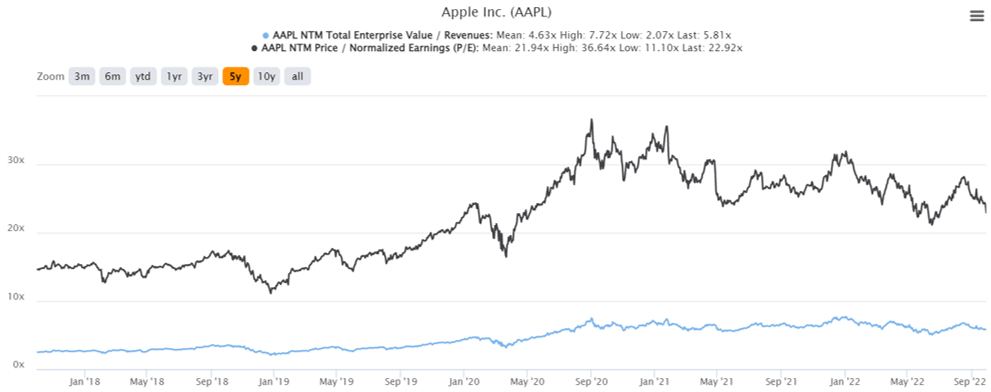

AAPL 5Y EV/Revenue and P/E Valuations

S&P Capital IQ

AAPL is currently trading at an EV/NTM Revenue of 5.81x and NTM P/E of 22.92x, higher than its 5Y mean of 4.63x and 21.94x, respectively. The stock is also trading at $142.84, down -21.91% from its 52 weeks high of $182.94, though at a premium of 10.69% from its 52 weeks low of $129.04. With a consensus estimate price target of $188.22, it is apparent that there is still a notable 32.10% upside from current prices

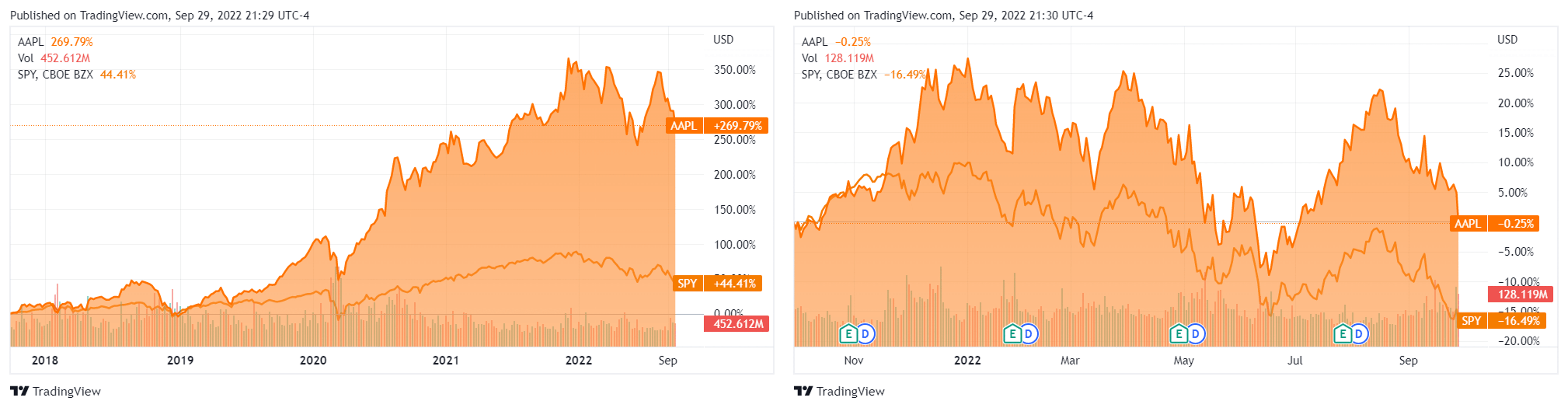

AAPL & SPY 5Y/1Y Stock Price

S&P Capital IQ

Both stocks also have had a relatively interesting co-existing relationship in their performance thus far, naturally, since AAPL accounts for 7.1% of the S&P 500 Index weighting. While APPL obviously had better returns thus far for the past 5Y at 289.6% and 10Y at 597.4%, the S&P 500 has also fared comparatively decent with 57.4% and 204.2%, respectively. These numbers are impressive, given that many other stocks have been decimated thus far.

With the stocks trading below their 50 and 100-day moving averages, both look relatively attractive, considering the massive returns upon market recovery by Q1’23. Naturally, the market will always be full of pitfalls for anyone who tries to pitch the perfect timing, since there may still be some downsides from current levels. As a result, investors with higher risk tolerances may consider nibbling at these levels, fully understanding the great importance of AAPL through the next decade.

Otherwise, conservative investors (like myself) will be waiting for more clarity from its upcoming earnings call, since the whole market seems to be heading for destruction one way or another. With little catalyst for short-term recovery, the AAPL stock will be testing the June lows of $130s over the next week or so. If that support level is breached, my oh my, we are in for a catastrophic rollercoaster ride indeed. Good luck all.

Be the first to comment