imaginima

Antero Resources (NYSE:AR) management still goes after “every last penny” in a number of ways. Now, there has been criticism of missed opportunities as well as times when cash appeared to be flying “all over the place”. But management has to decide what is important and why. In this business, things change so fast that sometimes those choices look really stupid. That makes this a very humbling industry in so many ways. But generally, the managements that succeed do more right than wrong even if it appears to be pure luck.

One thing about a commodity business is there are a lot of opportunities. Management has to determine which of those opportunities is important. The result is there is always someone who will say “you made a mistake” because in their mind, the opportunities were incorrectly ranked in importance and the wrong ones per pursued.

Pricing

One place where management has come out ahead time and time again has been pricing.

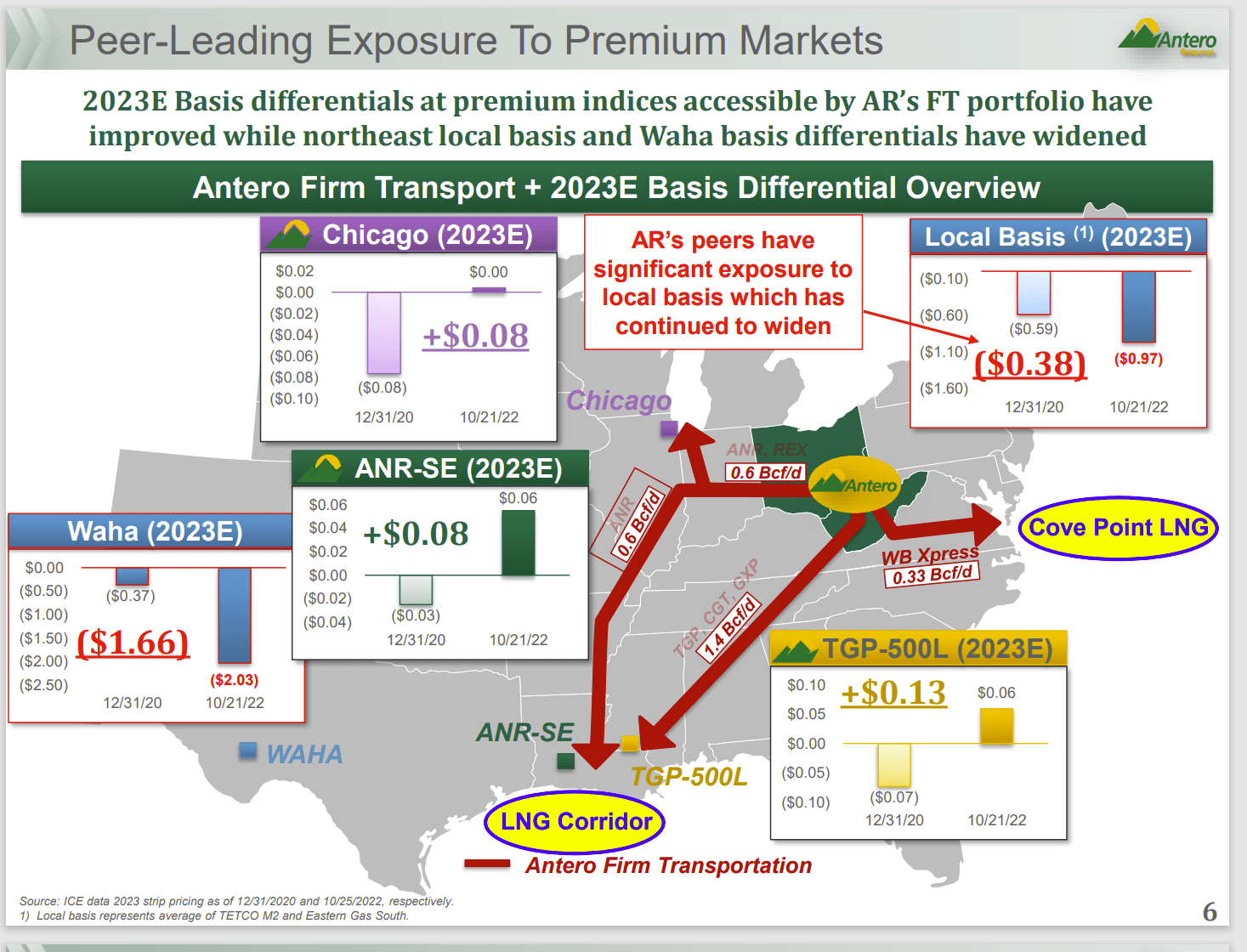

Antero Resources Firm Transportation Map To Superior Pricing (Antero Resources Third Quarter 2022, Earnings Conference Call Slides)

For as long as I have followed this company, management has taken advantage of the transportation options available to get their natural gas to markets that have in the past (at times) provided a huge premium over prices received by those selling in the basin area of operations. The advantage, of course, varies. But that pricing advantage has persisted.

There has been criticism of the fact that management has had too much transportation firmly committed and that firm transportation was going to cost a fortune. So far, it appears that the pricing advantage has far outweighed the cost of excess transportation.

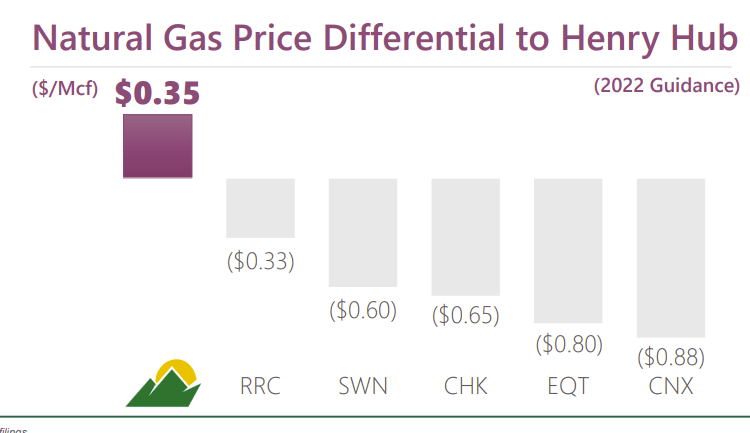

Antero Resources Pricing Advantage Comparison To Basin Competitors (Antero Resources December 2022, Corporate Presentation)

While the focus on the cost of excess transportation capacity is legitimate. The benefit in the form of far better pricing is clear. The commodity business is often a game of pennies. But, in this case, management found a giant advantage that is well worth the cost to produce a better margin.

The superior pricing has the effect of lowering the company breakeven when compared to the competition because the higher selling price earns extra dollars at the same price benchmark that does the competition shown above.

Under risks, one has to consider that this strategy of having options to different markets could have cost dearly. There were always readers that were darn sure it would in the future. So far, management has “won the bet” that transportation to different markets outweighed the cost of too much firm transportation. It is up to the reader to decide if it is luck or skill. But either way, management came out ahead.

Acreage Costs

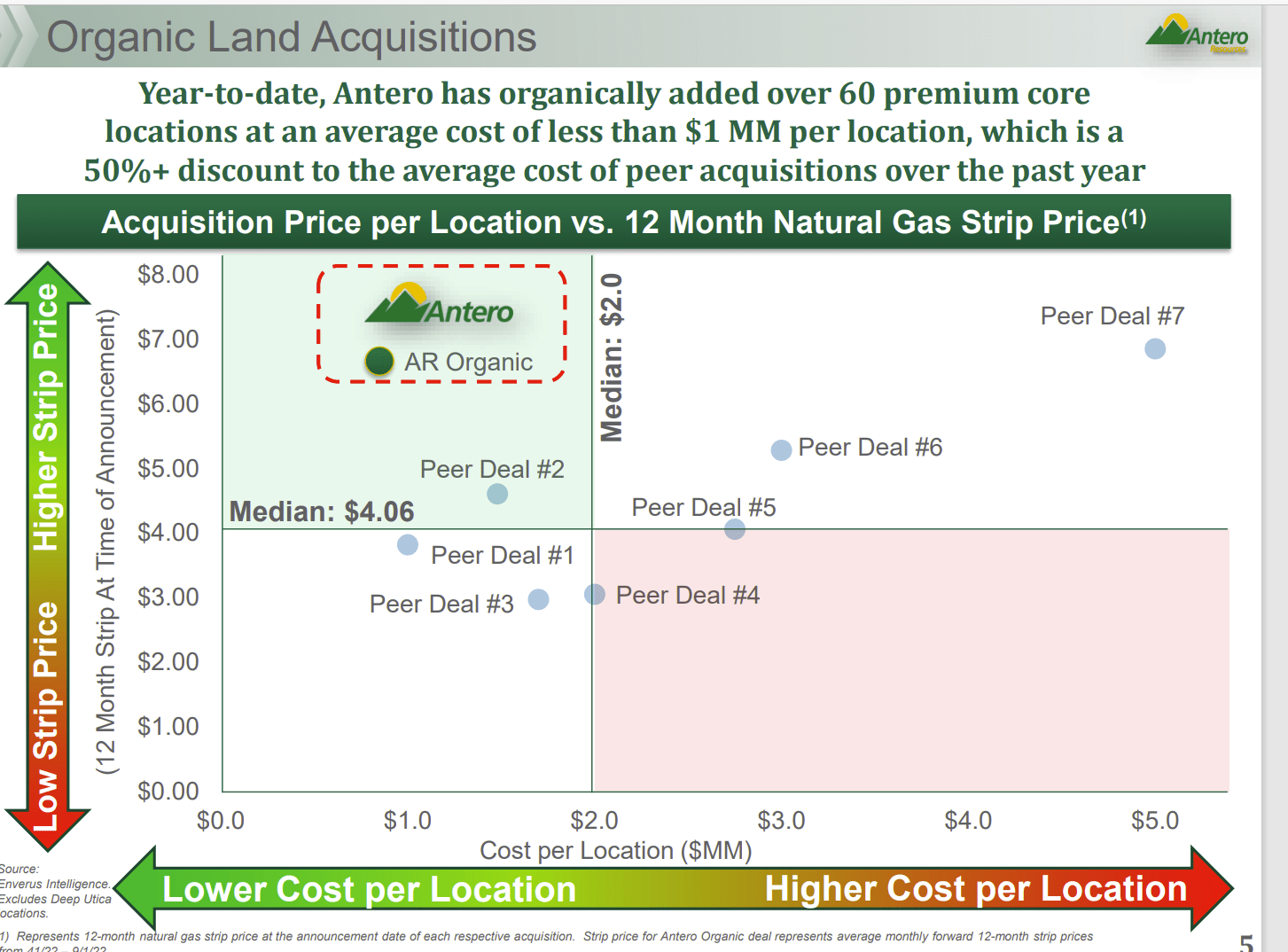

This management is pursuing a relatively labor-intensive strategy that is likely to save shareholders a lot of money over time.

Antero Resources Acreage Cost Per Drilling Location (Antero Resources Third Quarter 2022, Earnings Conference Call Slides)

Management is adding drilling the locations most likely through “bolt-on” additions of sub-optimal size holdings. Those relatively small acreage positions are often not real economical to the person owning them. In addition, the sales possibilities are often limited to the neighboring operator or sometimes operators.

The reason is that some of these acreage positions are so small that a well cannot be drilled economically or the well that can be drilled is less economic than the optimal well for the area. A large operator like Antero Resources can take advantage of the limited market to get the discount noted above while combining these small acreage positions into something more valuable.

In addition, operators often swap small acreage positions to create larger single positions that are more economical to drill and operate.

One of the advantages of this strategy is the location cost shown above to drill the well. Rarely do managements ever communicate the location cost of the well when they calculate payback periods as well as profitability. Yet, location cost is every bit as important to shareholder profitability as all the costs often listed on the revenue statement.

The problem with the average location cost to drill shown above is that more than $2 million in location costs need to be recovered on average for the usual deals made shown on the graph. That materially decreases the profitability of a well that typically needs to recover costs of (for example) $8 million. Yet, most managements never tell shareholders anything about location costs.

Instead, much of the time, any excess costs (and $2 million location cost per well is likely very excessive) are impaired during the next downturn when the lower-of-cost-or-market calculation usually starts a “clear the decks” massive impairment charge attributed to the low commodity prices rather than excessive management optimism about well profitability.

Rich Gas Advantage

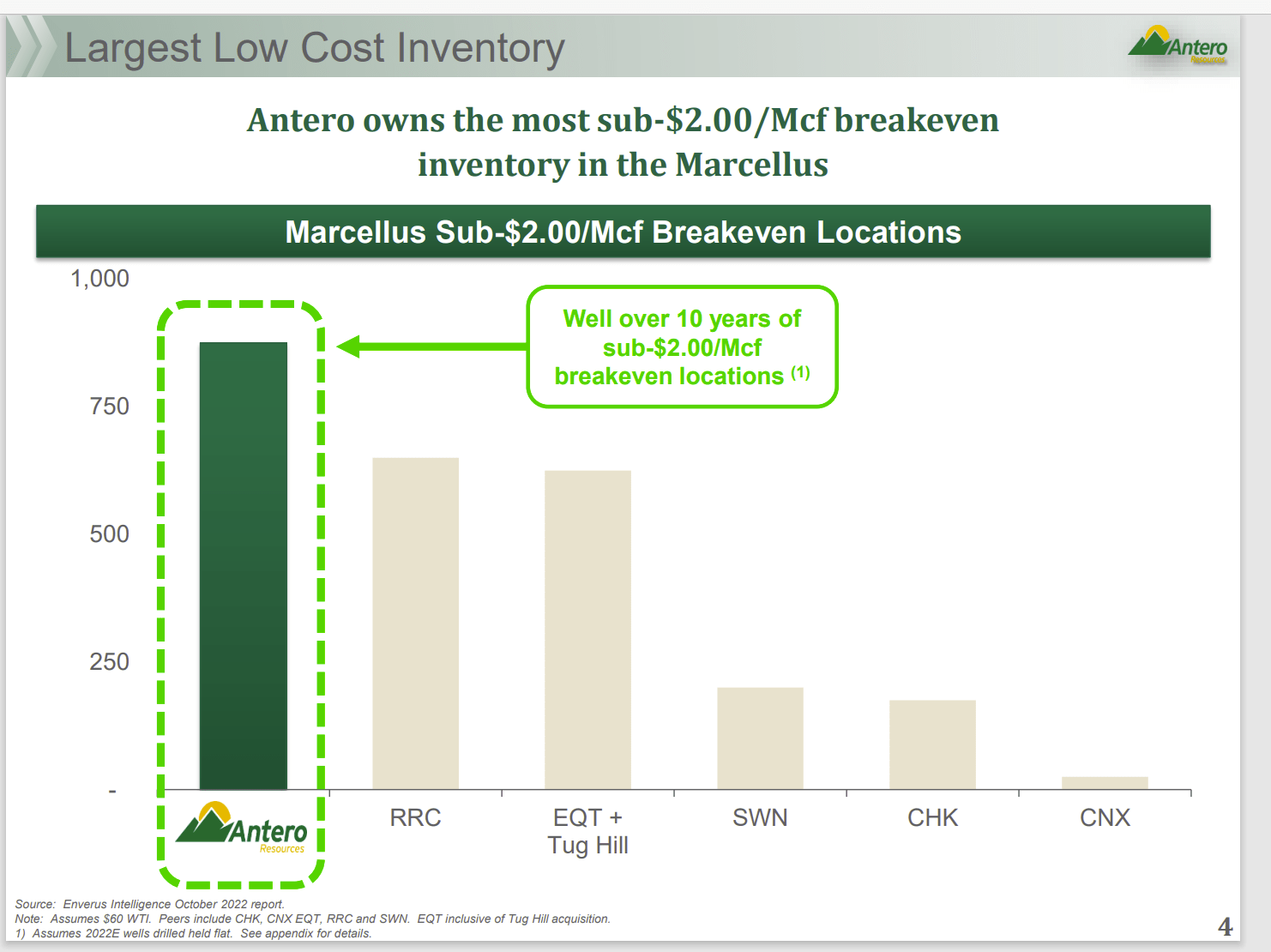

This management has developed extensive rich gas production opportunities to take advantage of the currently strong pricing environment as well as the rapidly growing ethane (also to some extent propane among other components) market. Ethane and propane (for example) are raw materials for plastic that can be used in the green revolution and a lot of other materials.

Antero Resources Natural Gas Price Breakeven Discussion (Antero Resources Third Quarter 2022, Earnings Conference Call Slides)

Antero Resources produces a variety of products because management has pursued rich natural gas production even when it did not look like “the thing to do”. Now, the prices for oil, natural gas liquids, and natural gas are such that the breakeven price for natural gas is very low. That breakeven will change with changing market conditions. But oftentimes, a rich natural gas strategy is more profitable than a dry natural gas strategy because the flexibility of selling a variety of products produced often ensures superior profitability under a wider variety of scenarios.

Debt: The One Controversy

The one-time a lot of comments did emerge was when management appeared to have waited too long to refinance the debt.

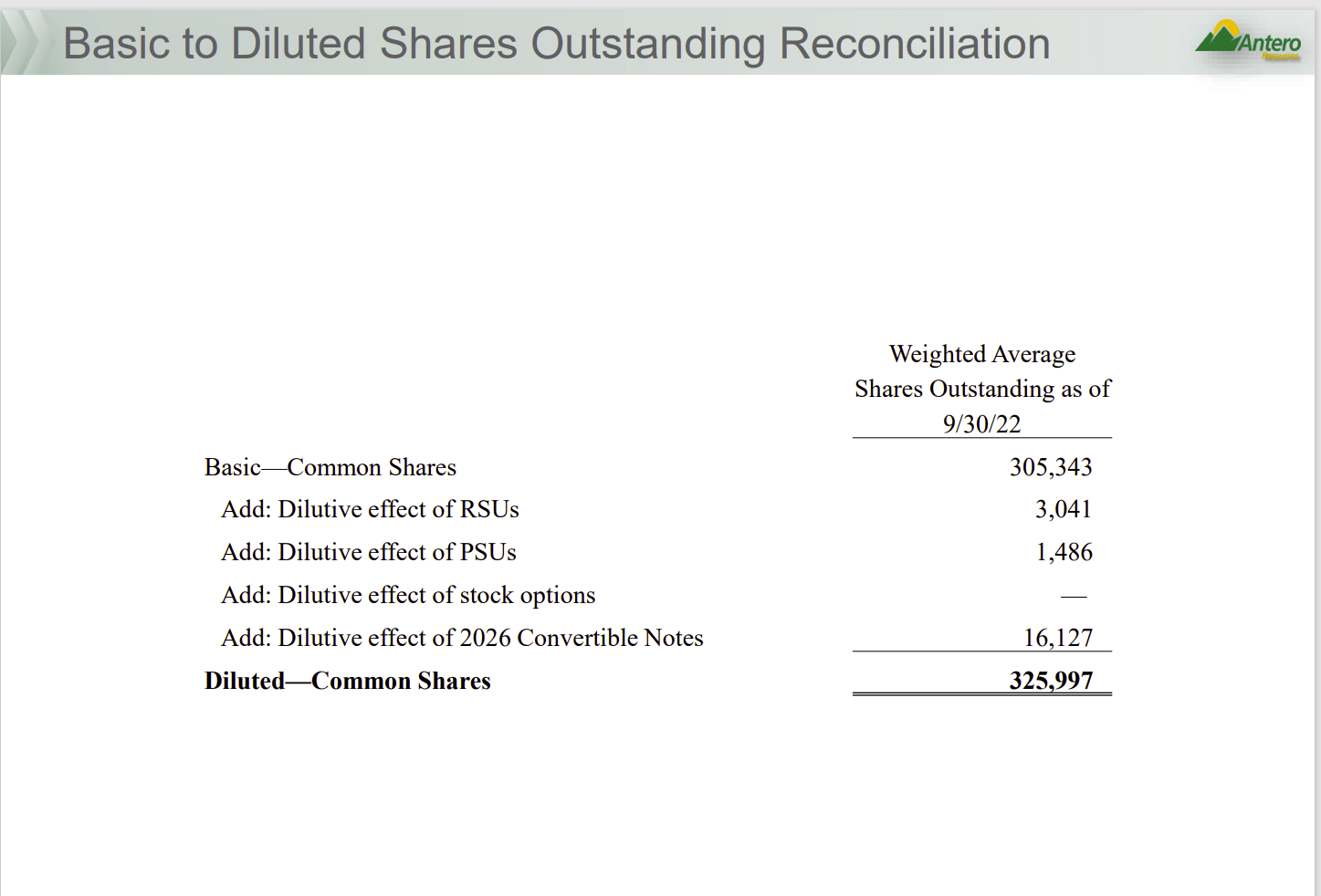

Antero Resources Calculation Of Fully Diluted Shares Outstanding (Antero Resources Third Quarter 2022, Earnings Conference Call Slides)

The opinion at the time was heading in the direction that the refinancing of the debt was too costly because management waited so long that the refinance occurred during the pandemic.

That extra cost showed itself still with the effect of the convertible notes shown above. Back then, management had repurchased some shares as they are now and sent them back out at a higher price (by way of converting the convertible notes). But some of the convertible notes were in excess of what common stock was purchased, and the conversion price was based upon the stock price back then. Those convertible bonds are now worth a small fortune compared to the value when they were issued back in the day.

Many thought that could have been avoided by refinancing earlier. However, it was a decision that management made to pursue other options thought to have a higher priority. I do not believe many saw the challenges of the pandemic ahead of time. Still, this was the decision that caused the most criticism.

The Future

Clearly, this management has made shareholders money even if shareholders do not agree with every last decision. My suspicion on the pricing strategy is that the strategy was worth billions of revenue dollars over the year compared to other operators in the basin. That alone overwhelmed a lot of other perceived actions that some did not agree with.

But that is the commodity business. Often management has a lot of choices, and many times must make a decision about the future in such a way that the right choices outweigh any perceived errors.

This management has done that in outstanding fashion. Investors should expect that to be the case in the future. So, returns in the future are likely to exceed market expectations one way or the other.

Be the first to comment