marketlan

I have received some questions about how Antero Resources’ (NYSE:AR) free cash flow is affected by changes in natural gas prices (and oil prices). The natural gas strip for 2023 (and to a lesser extent further years) has been volatile due to concerns about below average storage withdrawals amidst mild winter weather and the continued delays with Freeport LNG’s restart.

Antero is mostly unhedged, but should still be able to generate positive cash flow in 2023 as long as oil prices remain relatively solid. For example, at $2.50 Henry Hub gas and $80 WTI oil, I estimate that Antero can generate $470 million in free cash flow in 2023. Current 2023 strip is around $80 WTI oil and $3.25 Henry Hub gas, and Antero can generate around $935 million in free cash flow at those commodity prices. This is down around $700 million from the projections from December 2022, but I still believe that Antero is worth around $32 per share at long-term (after 2023) $70 WTI oil and $4.00 Henry Hub gas, and $41 per share at long-term $75 WTI oil and $4.50 Henry Hub gas. My share value estimates have gone down a bit over $2 per share since December, but my long-term outlook on oil and gas prices remains unchanged. The weaker near-term gas prices should actually increase the chances of natural gas averaging $4+ in 2024/2025 due to the impact on development plans for 2023.

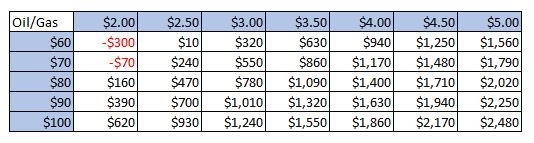

Estimated 2023 FCF At Various Oil & Gas Prices

The table below shows Antero’s estimated 2023 free cash flow (in millions of dollars) based on benchmark (WTI and Henry Hub) oil and gas prices during the year. I’ve assumed that Antero’s 2023 natural gas differential ends up at positive $0.35 and that realized C3+ NGL prices are 50% of WTI oil. Ethane prices are modeled it at a flat $11 per barrel and I have not attempted to model the decisions around ethane rejection/recovery to make things simpler.

Antero’s Projected 2023 FCF (Author’s Work)

Antero mentioned that its production costs change by approximately $0.10 per Mcfe for every $1 change in natural gas prices, due to the impact on GP&T as well as production taxes. I’ve also modeled a lesser impact on production costs (just from production taxes) from changes in oil prices.

The above numbers also include the impact of Antero’s hedges, although those only cover 2% of its 2023 natural gas production excluding the hedges related to Martica. The estimated distributions to Martica and the receipt of Antero Midstream dividends are also incorporated into those numbers. Antero is not expected to pay cash taxes in 2023 now.

At $60 WTI oil and $2 Henry Hub natural gas, Antero would be projected to have $300 million in cash burn if it doesn’t change its capex plans. At $80 WTI oil and $3 Henry Hub gas, it is projected to generate $780 million in positive cash flow. At $90 WTI oil and $4 Henry Hub gas it could generate around $1.63 billion in positive cash flow.

The current strip for 2023 is approximately $80 WTI oil and $3.25 Henry Hub natural gas, which would translate into expectations for around $935 million in positive cash flow in 2023.

Future Years

Antero is mostly unhedged in 2023, but may end up with more hedges in 2024 due to its swaption agreement. The counterparty in that agreement can decide in December 2023 if it wants to enter into a swap agreement to purchase 427,500 MMBtu per day at $2.77 per MMBtu in 2024. Antero could have around 20% of its natural gas production hedged in 2024 if the swaption is exercised and before any additional hedges are added.

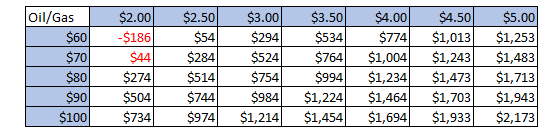

If the counterparty exercises its option, and all other parameters remain the same, Antero’s free cash flow at various oil and gas prices in 2024 would look like the following table. This does not include the potential impact of cash income taxes, which Antero may need to start paying in 2024 depending on commodity prices in 2023 and 2024.

Antero’s Projected 2024 FCF (Author’s Work)

The increased hedges results in a slightly narrower variance in projected free cash flow for 2024. At $60 WTI oil and $2 Henry Hub natural gas in 2024, Antero is projected to have $186 million in cash burn. At $80 WTI oil and $4 Henry Hub gas, it would generate $1.234 billion in free cash flow. The current strip for 2024 (around $75 WTI oil and $3.85 Henry Hub gas) translates into around $1.047 billion in projected free cash flow before cash income taxes.

Effect On Valuation

With the further decline in near-term cash flow expectations, I now estimate Antero’s value at approximately $32 per share at long-term (after 2023) $70 WTI oil and $4 Henry Hub natural gas. This increases to approximately $41 per share at long-term (after 2023) $75 WTI oil and $4.50 Henry Hub natural gas.

This is based on current 2023 strip of $80 WTI oil and $3.25 Henry Hub gas, resulting in $935 million in projected 2023 cash flow. Antero had approximately 300 million shares outstanding as of late October 2022, while its convertible notes can be converted into approximately 13 million shares. Antero has been repurchasing a significant number of shares too (10.5 million in Q3 2022), so 300 million shares may be a good number to use.

Thus if oil averages $70 and gas averages $2.50 in 2023 instead, Antero would be projected to generate $240 million in positive cash flow in 2023. This is a $695 million reduction (about $2.30 per share) from the base case scenario of current strip. At $70 WTI oil and $2.50 Henry Hub gas in 2023, followed by long-term $70 WTI oil and $4 Henry Hub gas after 2023, I’d value Antero at a bit under $30 per share.

If oil averages $90 and gas averages $4.00 in 2023, Antero would be projected to generate $1.63 billion in positive cash flow in 2023, $695 million (or $2.30 per share) more than what it is projected to generate at current strip. At $90 WTI oil and $4.50 Henry Hub gas in 2023, followed by long-term $70 WTI oil and $4 Henry Hub gas after 2023, I’d thus value Antero at a bit over $34 per share.

Conclusion

Antero is no longer looking at generating billions in free cash flow in 2023 due to sliding natural gas prices, but could still generate around $935 million in free cash flow at current strip (including $3.25 NYMEX gas). It may be able to generate $1.047 billion in free cash flow in 2024 at current strip as well. It is helped by prices of C3+ NGLs holding up better than natural gas prices.

I now estimate Antero’s value at approximately $32 at long-term $4 Henry Hub gas and $70 WTI oil and $41 at long-term $4.50 Henry Hub gas and $75 WTI oil.

Be the first to comment