Yingko/iStock via Getty Images

A more in-depth version of this report, including metric definitions and targets, was first shared with members of my Quality + Value Strategies subscription service in the Seeking Alpha Marketplace on November 4, 2022.

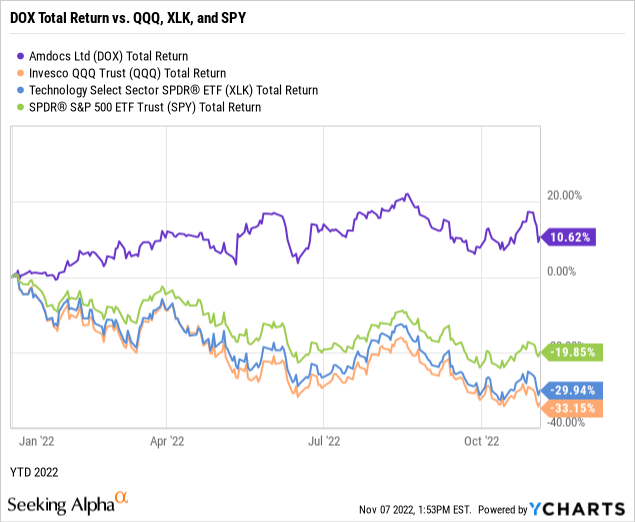

The technology-dominated NASDAQ, represented by the Invesco QQQ ETF (NASDAQ:QQQ), was trading today down -33.15% year-to-date. On the contrary, IT services provider Amdocs Limited (NASDAQ:DOX) was up +10.62% YTD for a stunning +43.77% outperformance thus far in the 2022 bear market.

By focusing investment research on fact-based current wealth and present value instead of unreliable predictive analysis and speculative growth, my stock picks have collectively outperformed the broader market since 2009. In this initial primary ticker research report on Amdocs, I put the company and its common shares through my proprietary, data-driven investment research checklist of the value proposition, shareholder yields, fundamentals, valuation multiples, and downside risk.

The resulting investment thesis:

Its prominent B2B customer base, including AT&T (T), Comcast (CMCSA), DISH Network (DISH), Epix (MGM), Rogers Communications (RCI), T-Mobile (TMUS), Verizon (VZ), and Vimeo (VMEO), plus hundreds of additional clients worldwide, provides Amdocs broad and loyal relationships that are rewarding its shareholders with bear market-beating returns.

My current overall rating: Buy, based on a bullish view of the company and a bullish view of the stock.

Unless noted, all data presented is sourced from Seeking Alpha Premium as of the intraday market on November 7, 2022; and is intended for illustration only.

Loyal B2B Relationships Worldwide

DOX is a dividend-paying mid-cap stock in the information technology sector’s IT consulting and other services industry.

Amdocs Limited, through its subsidiaries, provides software and services worldwide. The company designs, develops, operates, implements, supports, and markets open and modular cloud portfolios. The company has strategic collaborations with Amazon’s AWS (AMZN), Microsoft’s Azure (MSFT), and Alphabet’s Google Cloud (GOOG, GOOGL). Amdocs, with origins in Israel, was founded in 1982, registers on the Island of Guernsey (Channel Islands), and is headquartered in Chesterfield (St. Louis), Missouri, USA.

As a result of its registration, the company files with the U.S. Securities and Exchange Commission as a foreign issuer.

My value proposition elevator pitch for Amdocs:

Amdocs has close to 1,000 relationships with loyal major content producers, communications services, and media providers worldwide, providing an array of B2B technology products and services in 5G, automation, cloud, and digital.

The chart below illustrates the stock’s performance against the QQQ, the Technology Select Sector SPDR Fund ETF (NYSE:XLK), and the SPDR S&P 500 ETF Trust (NYSE:SPY) for year-to-date 2022.

Notably, DOX has outperformed the total returns of its sector and broader markets during the 2022 bear market, a rare feat for tech stocks.

My value proposition rating for Amdocs: Bullish.

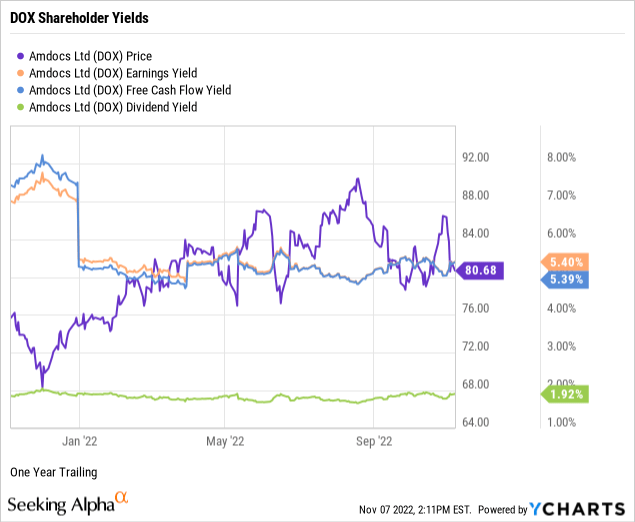

Compelling Long-Term Yield-On-Cost

As part of my due diligence, I average the total shareholder yields on earnings, free cash flow, and dividends to measure how a targeted stock compares to the prevailing yield on the 10-Year Treasury benchmark note. In other words, what is the equity bond rate of the common shares?

DOX was trading with an earnings yield of 5.40% and a free cash flow yield of 5.39%, as demonstrated in the below chart.

Amdocs was offering a modest forward dividend yield of 1.92%. However, its conservative 29.21% payout ratio indicates a safe, well-covered dividend with plenty of room for annual raises.

I prefer high dividend yields only when calculated on a long-term cost basis. Notably, DOX yielded 11.76% from an annual payout of $1.58 on a split- and dividend-adjusted cost basis of $13.44 per share on March 9, 2009, the last significant market bottom. Although an extreme example, with its yield-on-cost of 984 basis points above the forward yield, DOX provides another reminder that buy-and-hold quality value investing works.

Next, I take the average of the three shareholder yields to measure how the stock compares to the prevailing yield of 4.20% on the 10-Year Treasury benchmark note. For example, the average shareholder yield for DOX was 4.24% but 7.52% when using the 2009 yield-on-cost basis. Conventional market wisdom holds equities as riskier than U.S. bonds. Thus, securities such as DOX, which reward shareholders with yields at and above the government benchmark, argue for owning the stock instead of the bond.

Since earnings and free cash flow yields are inverse valuation multiples, each suggests that DOX trades at a reasonable stock price. I’ll further explore valuation later in this report.

My shareholder yields rating for DOX: Bullish.

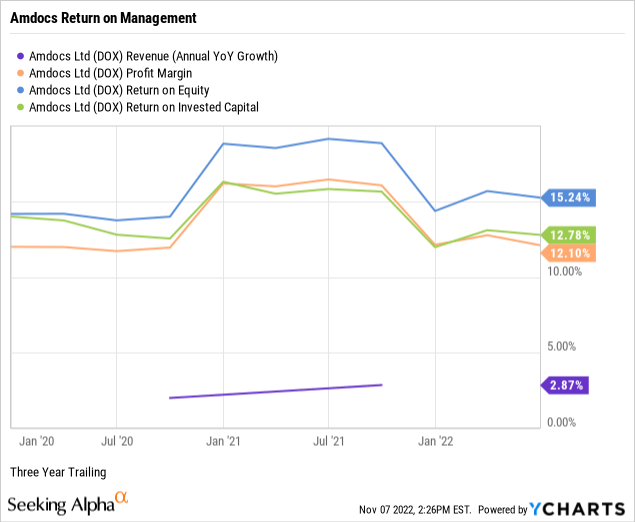

Modest Growth Subsidized by Robust Returns

Next, I’ll explore the fundamentals of Amdocs, uncovering the performance strength of the company’s senior management.

Per the below chart, Amdocs had positive three-year annualized revenue growth of 2.87%, underperforming the 6.32% median growth for the information technology sector.

Amdocs had a trailing three-year double-digit pre-tax net profit margin of 12.10%, outperforming the sector’s modest median net margin of 3.87%. I only screen for profitable companies to avoid unnecessary speculation.

The company was producing a trailing three-year return on equity of 15.24% against a median ROE of just 6.51% for the sector. Typically an accelerator of ROE, Amdocs has a history of aggressive share repurchases that appear to supersede forward dividend yields in generating shareholder returns.

At 12.78%, Amdocs’ return on invested capital, or ROIC, triples the sector’s median ROIC of 3.72%, indicating that its senior executives are capable capital allocators. ROIC needs to exceed the weighted average cost of capital or WACC by a comfortable margin, confirming management’s ability to outperform its capital costs. For example, Amdocs’ ROIC exceeds its trailing WACC of 8.53%, albeit on a higher-than-average capital cost basis. (Source of WACC: GuruFocus).

Despite modest revenue growth, it has double-digit net profit margin and sector-beating returns on equity and capital, indicating quality management performance in the English Channel and Show Me State.

My fundamentals rating for Amdocs: Bullish.

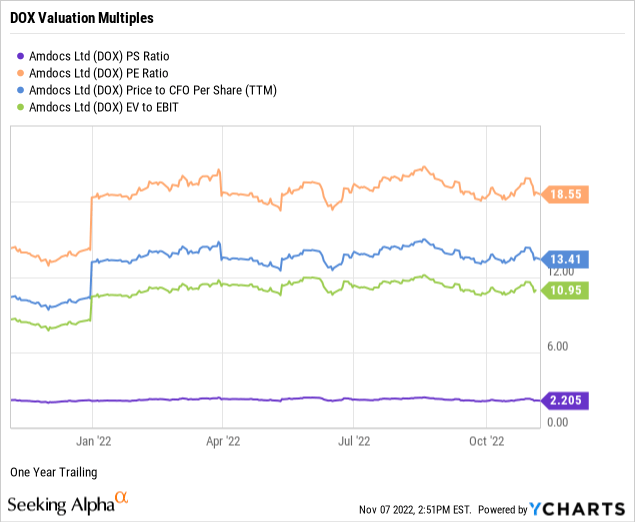

Shares Appear Underbought by the Market

I rely on just four valuation multiples to estimate the intrinsic value of a targeted quality enterprise’s stock price.

DOX was trading at a price-to-sales ratio or P/S of 2.21 times, in line with 2.41 P/S for the information technology sector and 2.26 times for the S&P 500. (Source of S&P 500 P/S: Charles Schwab & Co.) Thus, the weighted sector plus broader market sentiment suggests a reasonably-priced stock relative to Amdocs’ topline.

The stock had a price-to-trailing earnings multiple or P/E of 18.55 times against a sector median P/E of 20.95, indicating investor sentiment somewhat discounts the stock price relative to earnings per share. Further, DOX traded in line with the S&P 500’s overall P/E of 18.37. (Source of S&P 500 P/E: Barron’s).

At 13.41 times, DOX traded with a price-to-operating cash flow multiple at a discount to the sector’s median of 18.18, indicating that the market prices the stock below fair value relative to current cash flows.

Against the broader sector median of 16.91, DOX was trading at 10.95 times enterprise value to operating earnings or EV/EBIT, signaling the stock was oversold or underbought by the market.

Weighting my preferred valuation multiples suggests that despite the implied fair value based on sales and earnings, the market assigns a discount to Amdocs’ stock price relative to cash flow and enterprise value. Therefore, based on the fundamentals and valuation metrics uncovered in this report, risks and potential catalysts notwithstanding, I would call DOX a reasonably-priced, bear market-beating stock of an A-rated, award-winning IT services provider.

My valuation rating for DOX: Bullish.

Solid Debt Coverage Typical of a Tech

When assessing the downside risks of a company and its common shares, I focus on five metrics that, in my experience as an individual investor and market observer, often predict the potential risk/reward of the investment. Hence, I assign a downside risk-weighted rating of above average, average, below average, or low, biased toward below average-risk and low-risk profiles.

Alpha-rich investors target companies with clear competitive advantages from their products or services. An investor or analyst can streamline the value proposition of an enterprise with an economic moat assignment of wide, narrow, or none.

I assign DOX a narrow moat rating based on potentially its replicated services, countered by sticky customer relationships.

As reported on its June 2022 quarterly financial statements, Amdocs’ long-term debt coverage had current assets at 3.28 times its long-term debt. In theory, the company could pay off 100% of its longer-term debt obligations in a crisis using its liquid assets, such as cash and equivalents, short-term investments, and accounts receivables.

Amdocs’ long-term debt to equity was 22.69%, a further testament to its paydown capacity. In other words, I become concerned only when a company’s debt is more than twice its equity.

Amdocs’ short-term debt coverage or current ratio was 1.59 times. Thus, its balance sheet provides significant liquid assets to pay down 100% of its current liabilities, including accounts payable, accrued expenses, short-term borrowings, and income taxes.

DOX’s 60-month trailing beta was 0.71. At 0.62, its shorter-term 24-month beta was about equal. Thus, with price volatility trading below the S&P 500 standard of 1.00, DOX presents as a low-volatility mid-cap portfolio holding.

The short interest percentage of the float for DOX was a bear paws-off of 1.61%. So perhaps the near-sighted traders view the stock as a market-dominant, narrow-moat IT services provider with a loyal and sustainable customer base.

Amdocs is a fundamentally superior technology company with a unique value proposition and an attractive risk profile against a broader bear market.

My downside risk rating for Amdocs: Below Average.

Atypical Bear Market-Beating Performance

Catalysts confirming or contradicting my overall buy investment thesis on Amdocs and its common shares include, but are not limited to:

- Confirmations: Sales are accelerating from multi-year contract expansion and the addition of new engagements with large customers. A record backlog growth of 10% is a crucial indicator of momentum in network modernization, 5G, and cloud transformation efforts from customers. In addition, Amdocs has a sticky business model that generates strong free cash flow allowing for aggressive share buybacks.

- Contradictions: Over recent trading sessions, market sentiment has produced more volume on down days than up days, indicating a bearish condition. Unfavorable currency movements impacted total sales growth, and analysts expect FX headwinds to persist. Threats exist for a reduced volume of new projects should service providers reduce CapEx, digest new technologies, experience competitive losses, or experience higher-than-expected negative impacts from currency movements.

(Additional source of catalysts: Charles Schwab & Co.)

Due to its loyal customer relationships in IT infrastructure, worldwide market penetration, and strategic partnerships in the cloud, combined with solid fundamentals, reasonable valuations, and below-average risk, I expect DOX to continue its bear market-beating performance, at least in the near term.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top Ex-US Stock Pick competition, which runs through November 7. This competition is open to all users and contributors; click here to find out more and submit your article today!

Be the first to comment