JHVEPhoto/iStock Editorial via Getty Images

Investment Thesis

Advanced Micro Devices, Inc. (NASDAQ:AMD) stock has had a lot going for it recently, but mainly on the negative end. AMD’s consumer segment has been affected by increasingly negative sentiments over Q2 shipments as notebook ODMs revised their shipments forecasts.

In addition, investors and analysts have been concerned over negative shipments growth exacerbated by the worsening COVID-19 lockdowns in China. Notably, China’s supply chain visibility has weakened further, given the production suspension and severe logistics bottleneck. Moreover, these challenges have increased more stress on potentially lower end-consumer demand due to higher costs and more abundant chip availability.

As a result, AMD stock revisited its critical $100 support level and broke decisively below it. Nonetheless, we also noticed that short-term and long-term momentum indicators had entered oversold zones. Furthermore, the market has also put aside its recent announcement to acquire Pensando (expected completion Q2’22). The acquisition is expected to further cement AMD’s heterogenous compute strategy, adding a pivotal DPU capability to its line-up. Notably, the announcement followed closely its recent Xilinx completion, with its FPGA, and adaptive SoC capability.

We also share our updated DCF valuation model with an upgraded FV estimate. It accounted for the recent Xilinx acquisition, which is accretive to its top line and profitability.

We discuss why we reiterate our Strong Buy rating on AMD stock.

Why Investors Are Getting Wobbly Again

The global economy has been coming under tremendous stress recently. Since the start of the Russia-Ukraine conflict, Fed Chair Jerome Powell highlighted the FOMC’s commitment to a more aggressive rate hike path, coupled with quantitative tightening. Then, a relatively mild COVID-19 lockdown in China’s Shenzhen worsened into a full-blown lockdown in Shanghai.

Given Shanghai’s critical position in China’s manufacturing supply chain, the worsening conditions weren’t welcome. Moreover, Bloomberg also reported on April 11 that the situation has not improved, despite attempts to ease the lockdowns selectively. Bloomberg reported (edited):

Shanghai’s struggle with the virus means other local governments may become more sensitive to flare-ups and step up mobility controls even when cases are low, according to Tommy Xie, head of greater China research at Oversea-Chinese Banking Corp. “The Chinese economy may have to brace for more short-term disruptions in the coming months,” Xie wrote in a report Monday. – Bloomberg

If that wasn’t enough, China was also battered by worsening logistics snafus due to local state governments’ closure of critical highways. Notably, the local authorities have been very concerned about “importing” infection into their states. As a result, it has worsened the supply chain situation even further.

Furthermore, notebook ODMs emphasized that they recently had less visibility over the worsening outbreak. However, these ODMs have maintained their optimism until recently. Nevertheless, semiconductor sales remained strong in February. SIA reported that global semiconductor revenue reached $52.5B in February, up 3.4% MoM and 32.4% YoY.

Therefore, the negative sentiments over consumer end-demand only intensified very recently. The notebook ODMs and component suppliers have grown increasingly concerned over extended delays in China. While they were initially less worried, given the supply chain’s resilience, they have since downgraded their forecasts. DIGITIMES reported (edited):

Notebook ODMs and component suppliers share the view that their order visibility is rather low for H2’22.

The Russia-Ukraine war and pandemic conditions in China will be the two major variables to their shipment performance for the period. In response to the variables, most brand vendors recently have re-estimated their 2022 shipments will stay flat at or slip from 2021 levels, compared to single- or double-digit increases projected in late 2021.

It is expected to drive the vendors to slow or scale down order placements with supply chain partners in the months ahead, the sources continued. – DIGITIMES

But, AMD Has Bolstered Its Data Center Capability Tremendously

We think AMD’s recent $1.9B acquisition of Pensando has largely gone under the radar due to current negative sentiments. However, AMD investors would be remiss to dismiss the inroads that it has been making to undergird its data center ambitions. With the Xilinx acquisition, AMD now has a “multi-chip” strategy to penetrate Intel’s (INTC) stronghold further. In addition, with Pensando, AMD also has a competitive answer to NVIDIA’s (NVDA) Bluefield DPUs.

Therefore, we believe AMD is now very well-equipped in its heterogeneous compute roadmap, supporting its highly remarkable EPYC processors. AMD CEO Dr. Lisa Su highlighted (edited):

All major cloud and OEM customers have adopted EPYC processors to power their data center offerings. Today, with our acquisition of Pensando, we add a leading distributed services platform to our high-performance CPU, GPU, FPGA and adaptive SoC portfolio. – AMD

In addition, industry experts were effusive in their accolades over the recent acquisition. Moor Insights & Strategy accentuated (edited): “The acquisition buys AMD a front-row seat to the DPU market. I might be a little weary if I didn’t look at their customer list — and their customer list is impressive. I see this as the AWS (AMZN) Nitro for everybody else. Which is why Azure, Oracle Cloud, and IBM Cloud are on it.”

Furthermore, Pensando articulated that it has accumulated a robust “ecosystem of partners and customers who have currently deployed over 100K Pensando platforms into production.” Therefore, investors should give due credit to Dr. Su & Team’s acquisitive roadmap to strengthen its competitive edge.

SDxCentral also highlighted (edited): “The company’s packet processors are widely deployed in enterprise and cloud data centers alike. It counts Goldman Sachs (GS), IBM Cloud (IBM), Microsoft Azure (MSFT), Oracle Cloud (ORCL), and HP Enterprise (HPE) as customers.”

Hence, we encourage investors to glean more insights from AMD’s upcoming Q2 earnings call. In addition, we believe Dr. Su & Team might share some insights on its “upgraded” strategy to further penetrate Intel’s closely guarded data center market share.

Revised Fair Value Indicates AMD Stock Is Now Significantly Undervalued

Following the integration of Xilinx into AMD’s portfolio, we have also revised our fair value (FV) estimates based on our DCF model. We have made the necessary adjustments to its revenue and profitability accretion and its expanded share base. We have also lowered our EBITDA exit multiple to reflect the compression in peer multiples. The intention is to derive an FV estimate that makes sense.

| Metric | Estimate |

| FY26E Revenue | $38.46B |

| Revenue CAGR FY22E-FY26E % | 10.8% |

| FY26E Adj. EBITDA | $14.42B |

| FY26E Adj. EBITDA Margin % | 37.5% |

| FY26E EBITDA exit multiple | 20x |

| Implied fair value estimate | $150.73 |

AMD stock DCF valuation. Data source: author, S&P Capital IQ, company filings

Our estimates imply a marked increase from our previous estimate of $142. Furthermore, we revised our exit multiple down from 30x to 20x to reflect the compression in peer multiples. We have also adjusted our revenue CAGR downwards to reflect some execution risk from the Xilinx integration. Notably, based on AMD stock’s last traded price, it represents a significant implied upside of 54.8%. Hence, we think there’s a substantial margin of safety embedded at the current levels.

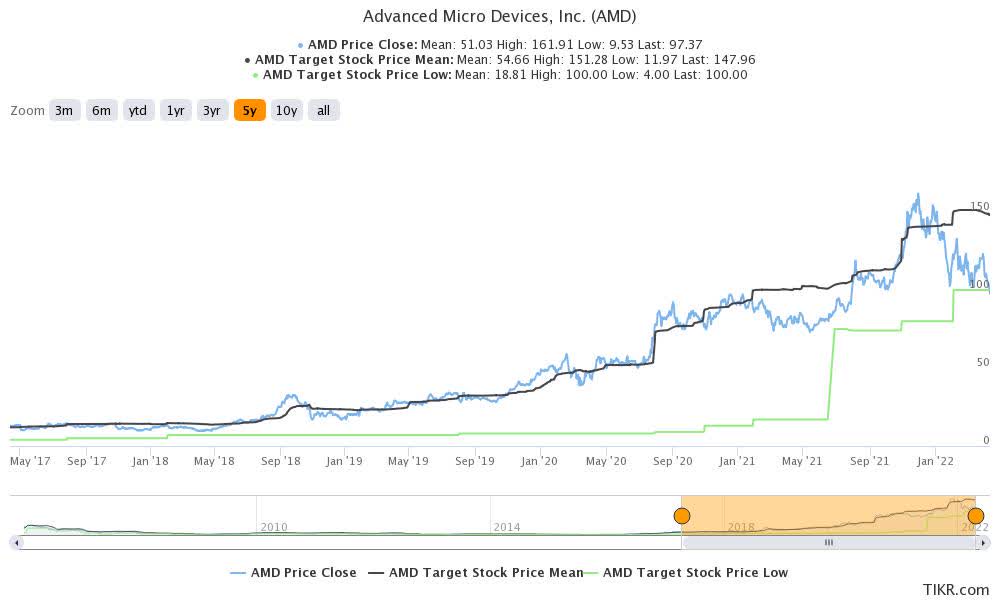

AMD stock consensus price targets Vs. stock performance (TIKR)

Furthermore, AMD stock last traded at the most conservative price targets (PTs) again. Investors can observe that AMD stock has consistently found its support along its most conservative PTs over the past five years.

Therefore, we are confident that the recent sell-off has presented AMD investors with a fantastic opportunity to add more exposure. We believe that those headwinds enunciated above are temporal. Investors should hold the long-term view and add AMD stock on weakness.

As such, we reiterate our Strong Buy rating.

Be the first to comment