4kodiak/iStock Unreleased via Getty Images

Amazon’s (NASDAQ:AMZN) AWS has been driving the company’s overall growth for many quarters now. But this time around, in Q2, the segment’s revenue growth decelerated sequentially and bears have now begun speculating if its stellar run is coming to an end. But that’s not necessarily the case here. In this article, I’ll highlight industry comparables to explain why AWS’ results were nothing short of spectacular in Q2 and its growth momentum remains intact.

The Resilient Results

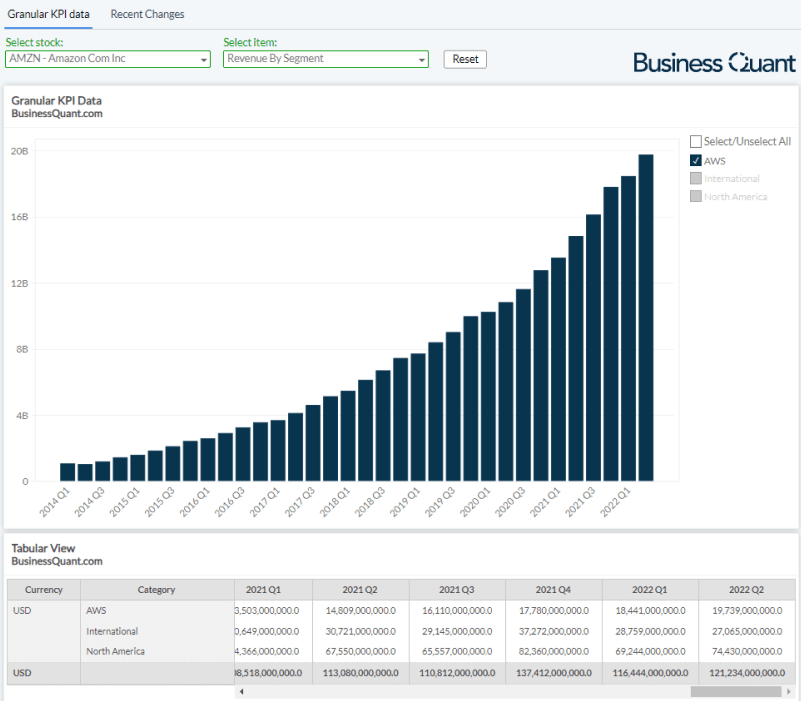

Let me start by giving credit where it’s due. The platform and infrastructure cloud services industries have cutthroat competition and companies are always on the lookout to roll out new offerings as soon as new pockets of growth emerge. But in spite of this fierce competition, Amazon’s AWS has managed to grow revenue consistently in all of the past 33 quarters. I believe this is a commendable feat and an enviable position to be in.

BusinessQuant.com

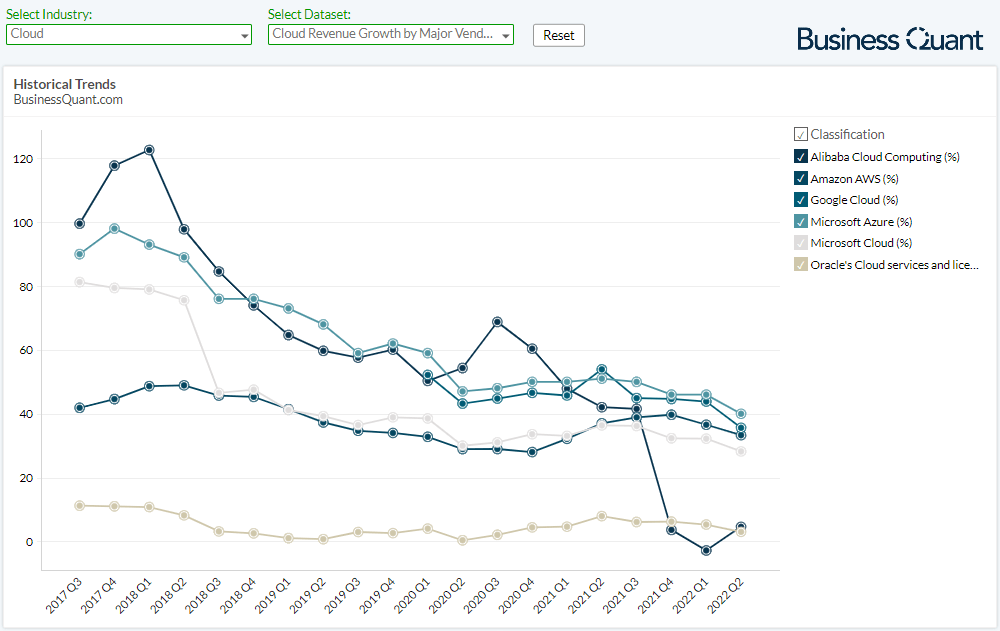

Now, Amazon AWS’ pace of revenue growth did decline over the years, but that’s only natural since the business has grown manifold. But what’s concerning investors more is the fact that AWS’ pace of growth has declined by 5,600 bps in the last 4 quarters alone. Investors are now wondering if this is the beginning of a prolonged slowdown and if so, then how much lower can its growth rates drop. While that’s a valid concern, there are two reasons why investors shouldn’t be worried just yet.

First, the chart below highlights that Amazon AWS’ pace of growth is still higher than its 2019 and 2020 levels. This means the segment’s performance is still very good on a standalone basis.

BusinessQuant.com

Secondly, note how growth momentum for other cloud platforms has significantly decelerated over the past 4 quarters. For instance, Microsoft (MSFT) Azure’s and Google Cloud’s (GOOGL) pace of revenue growth has declined by 8,000 bps and 9,300 bps over the last 4 quarters, respectively. In comparison, Amazon AWS’ pace of revenue growth has dropped by 5600 bps, meaning its performance has remained relatively resilient over the period.

The industry-wide growth moderation suggests that there were spending cuts on cloud services of late due to challenging macroeconomic conditions. But the fact that Amazon’s AWS was impacted the least in its peer group, leads me to believe that its services are deemed relatively more essential amongst enterprises. The same cannot be said for Microsoft Azure, Alibaba Cloud (BABA) and Google Cloud, though, as their growth deceleration was more prominent.

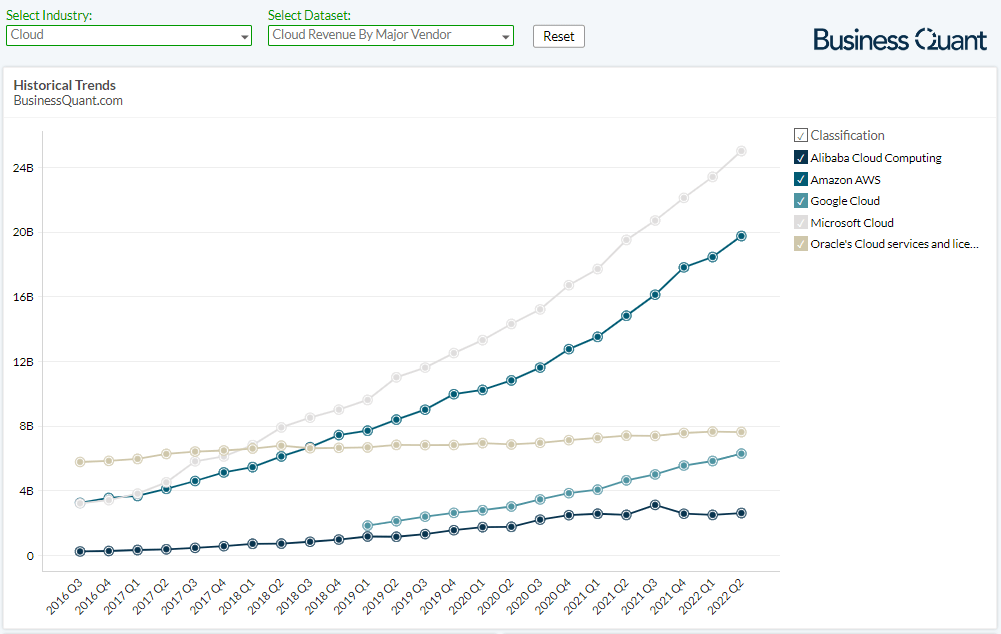

For the uninitiated, Amazon’s AWS is dominating the cloud infrastructure and platform industry globally. While others are catching up, there’s still a long way to go before they start to rival Amazon’s formidable position in the space. Also, for the record, AWS accounted for nearly 16% of Amazon’s total revenue last quarter. This means the segment has a sizable contribution to the company’s top line and any fluctuations there is bound to affect Amazon’s financials.

BusinessQuant.com

So, we’ve established that Amazon AWS results were solid in Q2. But the question that now arises is – what lies ahead for the segment?

What Lies Ahead

For starters, Amazon’s management is optimistic about the growth of AWS and they’re ramping spending for the same. Although they didn’t reveal exact figures or issue a segment-specific guidance, they did note on the Q2 earnings call that they’re ramping capital investments for AWS. The added capacity, new offerings and geographical expansion suggests that Amazon’s AWS is likely to continue growing at its rapid rate in the foreseeable future as well.

AWS continues to grow at a fast pace, and we believe we are still in the early stages of enterprise and public sector adoption of the cloud… For full-year 2022, we do expect to spend slightly more on capital investments than last year, but the proportion of capital spending shifts among our businesses. We expect technology infrastructure spend to grow year-over-year, primarily to support the rapid growth in innovation we are seeing with AWS.

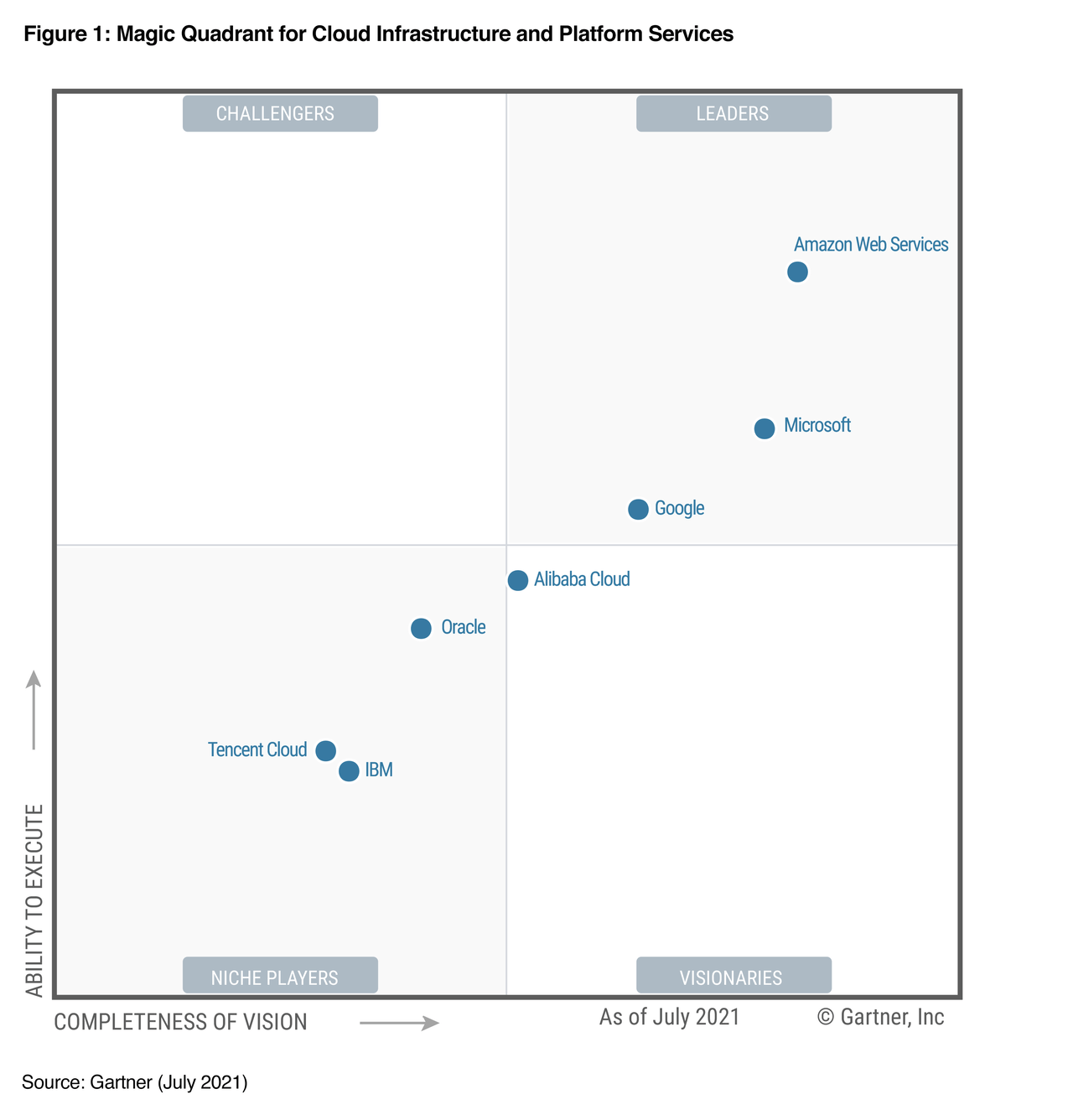

Secondly, Amazon’s AWS remains favorably positioned (top-right corner) in Gartner’s quadrant for cloud infrastructure services. Other prominent cloud vendors, like Microsoft Azure, Google Cloud, Oracle (ORCL), have been operating in the space for more than 5 years now but they don’t even come close to AWS in terms of value proposition, per the quadrant. This, again, suggests that Amazon AWS’ user adoption will continue rising and its revenue growth momentum will remain elevated in the quarters ahead, at least until the competitive landscape doesn’t change materially.

Gartner

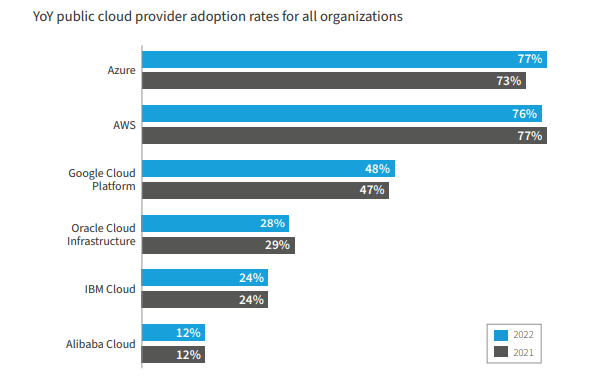

Lastly, a survey conducted by Flexera revealed that 76% of their respondents were using Amazon’s AWS. This is a gigantic proportion of users relying on Amazon for their cloud infrastructure needs. It’s a clear indication that rival cloud platforms just aren’t able to dent Amazon AWS’ growth momentum or nab users away from its ecosystem. So, I expect the e-commerce giant’s foray into the cloud vertical to continue growing rapidly in the coming years as well.

Flexera

Final Thoughts

Although other cloud vendors are reeling with a sales slump, Amazon’s AWS continues to thrive. It isn’t a matter of luck or by fluke, but rather because of aggressive capital expenditure planning, relentless execution, hardware upgrades, capacity expansions and smart integrations with new and upcoming cloud infrastructure software.

BusinessQuant.com

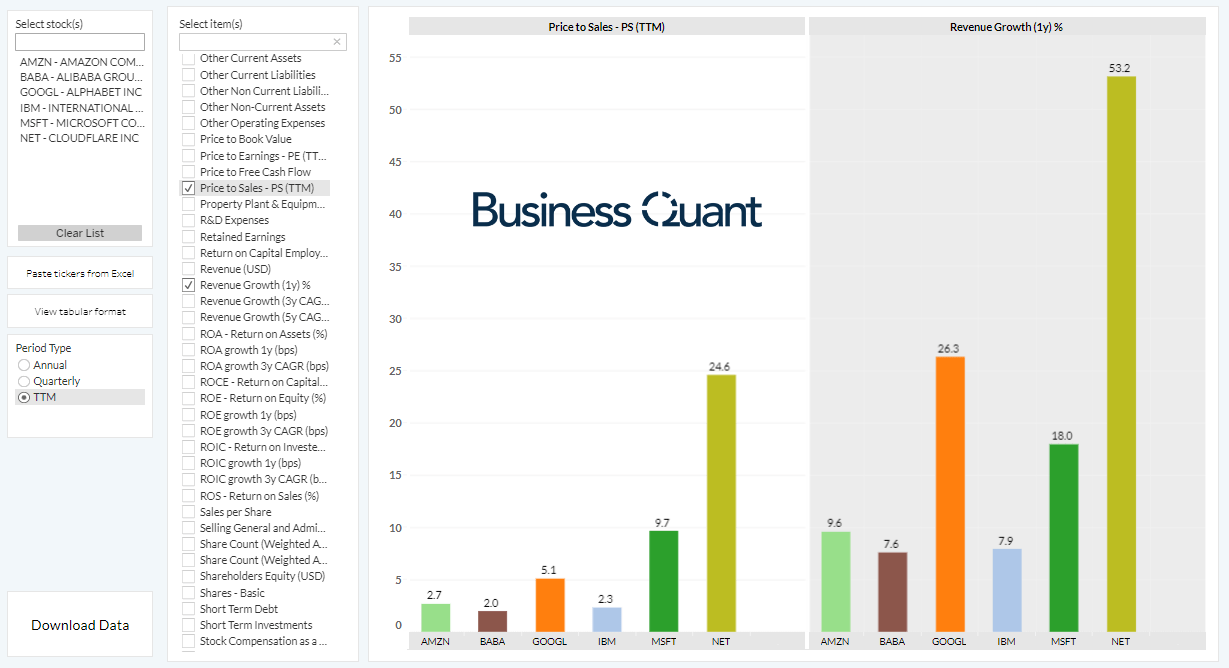

So, I expect Amazon’s AWS to continue growing at its rapid rate and drive the company’s overall growth in the foreseeable future. As far as valuations are concerned, Amazon’s shares are trading at just 2.7-times its trailing twelve-month sales. This is quite low when compared to some of the other rapidly growing cloud vendors and it makes Amazon an attractive buy at current levels. Therefore, investors with a multi-year time horizon may want to accumulate shares of the e-commerce giant on potential price corrections.

Good Luck!

Be the first to comment