JHVEPhoto

About one week ago, I asked in an article if I am wrong about CVS Health (CVS) – and a similar question can be asked about Walgreens Boots Alliance, Inc. (NASDAQ:WBA). Not only have both companies a similar business model, we can also see other parallels as well: both stocks are not really appreciated by investors and seem to trade at rather low valuation multiples and below their intrinsic values (at least in my opinion). And while CVS could almost double from its previous cycle low, Walgreens Boots Alliance is still trading close to a multi-year low.

I will structure this article in a similar way as my previous article about CVS Health as many of the issues and topics are similar. And when looking at the news in the last few months, I can understand why investors are currently not willing to invest in Walgreens Boots Alliance – but similar to CVS Health, I think they are making a mistake by taking a rather short-term perspective. Nevertheless, let’s ask the same question again: Am I wrong about Walgreens Boots Alliance?

Valuation

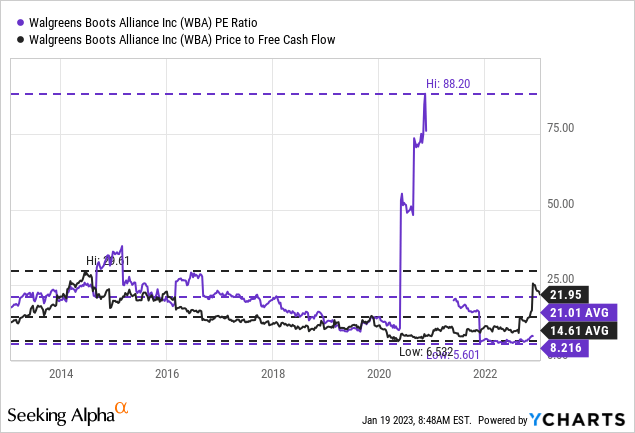

And once again we start by looking at the valuation multiples and intrinsic value, as this is still the strongest argument for Walgreens Boots Alliance in my opinion. When looking at the price-earnings ratio and price-free-cash-flow ratio WBA stock is trading for, it doesn’t look so cheap. We can start by looking at the price-earnings ratio and won’t find any useful numbers, as a meaningful P/E ratio can’t be calculated right now. In the last twelve months, Walgreens Boots Alliance generated a loss of $3.43 per share, and we must wait for Walgreens Boots Alliance to be profitable again before we can calculate a P/E ratio. However, there is a reason for the reported loss, and it has nothing to do with the fundamental business of Walgreens Boots Alliance (we will get to this).

When looking at the price-free-cash-flow ratio, Walgreens Boots Alliance is trading for 22 times free cash flow, which also doesn’t seem to be so cheap and certainly does not deserve the label bargain.

So, am I wrong when I see Walgreens Boots Alliance as a great investment? I don’t think so – and let’s provide some perspective on these numbers. Walgreens Boots Alliance recorded a $6.5 billion liability associated with the opioid settlements (we will get back to this) which led to a huge loss per share in the last quarter. When calculating a P/E ratio by using the expected adjusted earnings per share for fiscal 2023 of $4.55 (midpoint of guidance), the stock is trading for about 8 times earnings – and this is cheap.

When looking at free cash flow (“FCF”), I would rather calculate an intrinsic value by using a discount cash flow calculation and not just look at the P/FCF ratio. Free cash flow in the last four quarters was $1,403 million, and usually I would take that amount for my calculation. But when looking at the last few years, we can see that generated free cash flow was mostly between $3.5 billion and $5.0 billion.

And when assuming only a free cash flow of $3.5 billion annually from now till perpetuity, we get an intrinsic value of $40.53 for Walgreens Boots Alliance (assuming 10% discount rate and 863.6 million outstanding shares). And the current results are not great, but Walgreens Boots Alliance is probably undervalued when taking a mid-to-long-term perspective.

Quarterly Results

When looking at the last quarterly results, I also can understand that investors are rather fleeing instead of putting money into WBA. And we already mentioned the reason for the horrible results above – opioid litigations. However, when looking at the top line, we see sales declining from $33,901 million in Q1/22 to $33,382 million in Q1/22 – resulting in 1.5% year-over-year decline – and that can’t be explained by higher expenses. Instead of an operating income of $1,283 million in Q1/22, Walgreens Boots Alliance had to report an operating loss of $6,151 million in Q1/23 and diluted earnings per share also “switched” from $4.13 in earnings per share in Q1/22 to a loss per share of $4.31 in Q1/23.

WBA Q1/23 Presentation

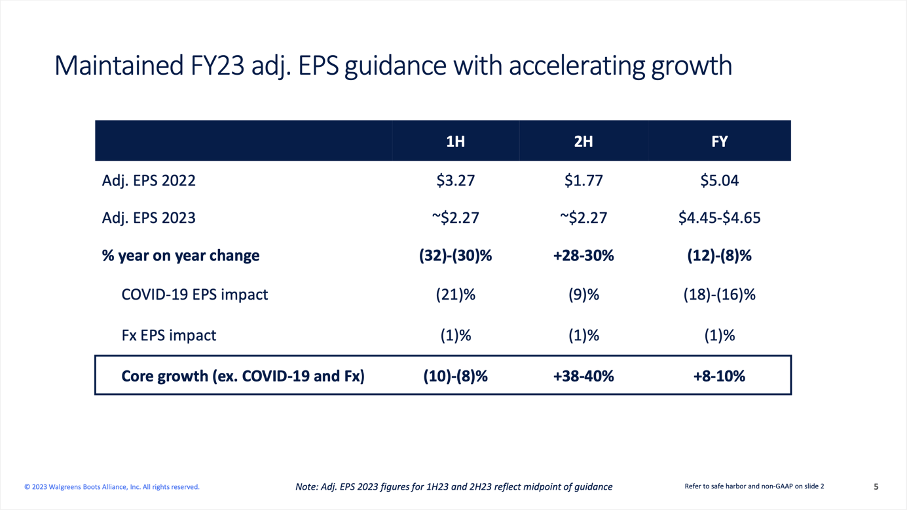

We can try to sugarcoat these results all we want – they are not great. But we can provide some additional information and try to look at the bigger picture. First, the guidance for fiscal 2023 is solid and Walgreens Boots Alliance is expecting adjusted earnings per share to be between $4.45 and $4.65. Compared to $5.04 in adjusted EPS in 2022 this can be seen as disappointing. But we must take into account the COVID-19 EPS impact, which is between 16% and 18% and when excluding that, the core growth will be between 8% and 10%.

WBA JPM Presentation

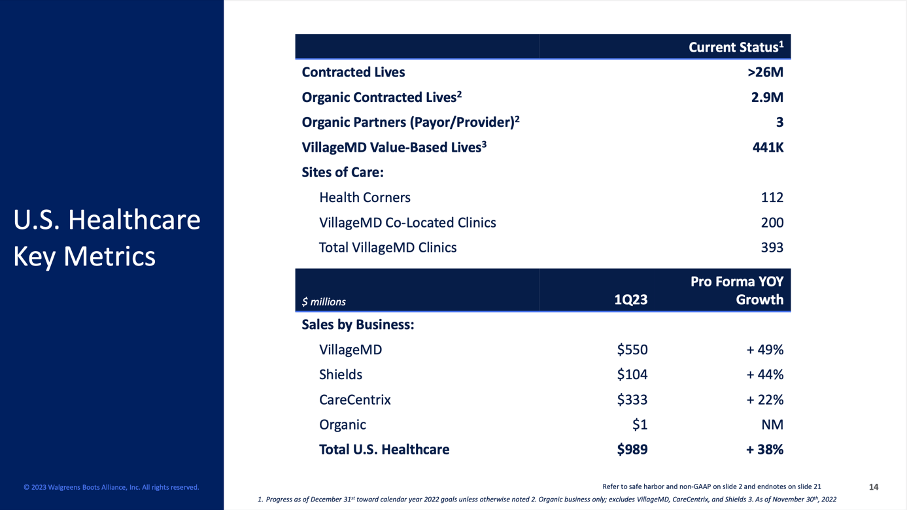

Second, we can look at the U.S. Healthcare business, which should drive growth in the years to come. In the first quarter of fiscal 2023, the segment generated $989 million in revenue, which is an increase of 38% year-over-year. And the number of total VillageMD clinics increased to 393.

WBA Q1/23 Presentation

Opioid Litigation

Another reason for the mediocre stock price performance – similar to CVS Health – could be the opioid litigations. Like CVS Health and Walmart (WMT), Walgreens Boots Alliance reached a settlement last year (or is very close). And on November 2, 2022, the company has agreed in principle to settlement frameworks. And under these frameworks, the company will pay about $4.95 billion in remediation payments, which will be paid over the next 15 years.

While this was announced in November 2022, Walgreens made the following statement during the Q1/23 earnings call:

“We made an important announcement on our opioid legal matters in November, reaching an agreement in principle to pay approximately $5.7 billion over 15 years to resolve a substantial majority of our opioid-related litigation brought by states, political subdivisions and tribes.”

But if I am not mistaken, the higher amount of $5.7 billion is due to approximately $754 million in attorney’s fees and costs Walgreens Boots Alliance must pay as well. In its Q1/23 income statement, Walgreens Boots Alliance recorded a $6.5 billion liability associated with the settlement frameworks and other opioid-related claims and litigations, which led to the bottom-line loss. And while Walgreens Boots Alliance is losing more than the free cash flow it can generate in one year, we should not ignore that these are one-time expenses that won’t have any effect on the fundamental, underlying business.

Acquisitions

In my article about CVS Health, I also mentioned acquisitions as a potential problem and a reason why the stock was trading below the price I would see as its intrinsic value. And when looking at Walgreens Boots Alliance in 2022, acquisitions could also be an issue and the narrative could be similar. The company acquired Shields (the acquisition closed on December 28, 2022), and in October, Walgreens Boots Alliance bought the remaining 45% stake in CareCentrix.

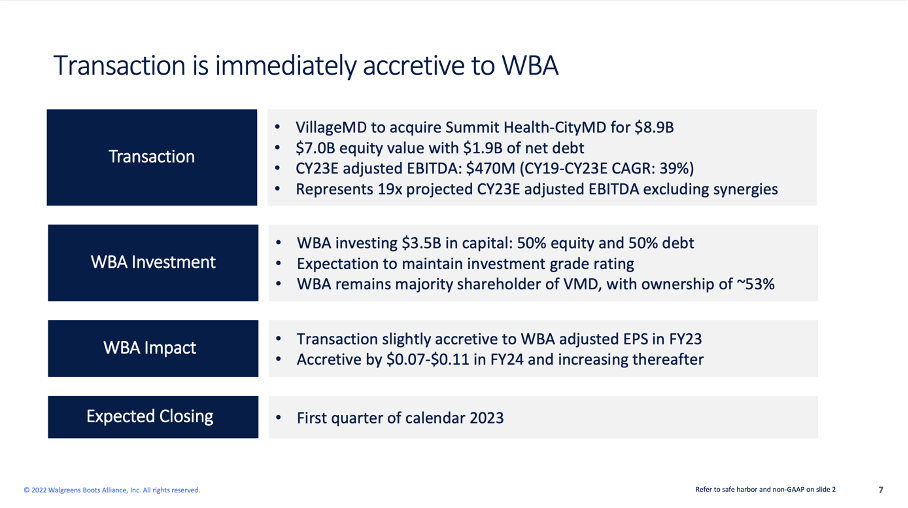

And in November 2022 another huge acquisition was announced. VillageMD (of which Walgreens Boots Alliance is the majority owner) acquired Summit Health-City MD for $8.9 billion ($7.0 billion in equity value and $1.9 billion in debt). Walgreens Boots Alliance also invested $3.5 billion in capital (evenly split between equity and debt). The transaction was closed on January 3, 2023.

WBA November 2022 Presentation

The company is expecting $470 million in adjusted EBITDA for the calendar year 2023, which would result in an EBITDA CAGR of 39% between CY19 and CY23 for Summit Health. As a result of the acquisition, Walgreens Boots Alliance raised its U.S. Healthcare segment sales outlook. Instead of $11.0 – $12.0 billion in sales in FY2025 it is now expecting $14.5 – $16.0 billion in sales. And the goal is also for the segment to contribute in a positive way to adjusted EBITDA by 2024 (more than $600 billion in FY24 and about $1.1 billion in FY25).

WBA November 2022 Presentation

Bullish Conclusion

Similar to CVS Health, I remain bullish about Walgreens Boots Alliance – and I remain bullish for several reasons. First, the dividend yield of 5% is certainly attractive for investors and will reward us in some way as long as we are waiting for the stock price to finally move towards its intrinsic value. Second, the stock and company are rather recession-resilient, which is a nice-to-have in the coming quarters. Third, I remain confident that Walgreens Boots Alliance can grow at least in the mid-single digits in the years to come (despite the above-mentioned short-term turbulences for the business). And as a result, WBA stock is clearly undervalued.

As I already mentioned above, Walgreens Boots Alliance, Inc. stock is even undervalued when assuming a rather low free cash flow and zero growth for the years to come. Nevertheless, we should calculate with more realistic assumptions. In the last five years, Walgreens Boots Alliance could generate $4,250 million in free cash flow annually on average. Let’s be cautious and assume $0 free cash flow in 2023, and for fiscal 2024 we take $4,250 million as basis. And for the following years, we assume 5% annual growth (which is below the company’s own long-term targets presented during its 2021 Investor Day as well as the average growth rates WBA could report during the last decade).

WBA Investor Day 2021

When calculating with these numbers (and once again a 10% discount rate and 863.6 million in outstanding shares), we get an intrinsic value of $89.48 for Walgreens Boots Alliance. And while this might seem completely unrealistic, we should not forget that the assumptions in this calculation were rather cautious (in previous articles I calculated an intrinsic value in a range between $80 and almost $140 – depending on the assumptions we use). As a result, I can only stay bullish about Walgreens Boots Alliance, Inc. stock.

Be the first to comment