Ljupco/iStock via Getty Images

Introduction

Altria Group, Inc. (NYSE:MO) had an eventful late October, agreeing to hand back its U.S. IQOS license to Philip Morris (PM) on October 20, releasing Q3 2022 results last Thursday (October 27) as well as announcing a new partnership with Japan Tobacco (OTCPK:JAPAY) on the same day. Shares have gained 3% since October 20.

We upgraded our rating on Altria to Buy in February 2020. Since then, MO shares have gained 17% (including dividends), though they have fallen back 19% from their roughly $57 peak in May 2022:

|

Altria Share Price (Last 1 Year)  Source: Google Finance (01-Nov-22). |

Q3 2022 results were again weak operationally. EPS grew 4.9% year-on-year, but half of this was driven by buybacks. Altria’s cigarette volume fell 10% year-on-year excluding inventory. For now, we can look past this decline as being partly driven by exceptional macroeconomic headwinds and partly a reversal of a temporary boost during COVID-19. However, Altria’s strategic position has worsened considerably, with Philip Morris set to compete in its U.S. home market. We are pessimistic about Altria’s own new product efforts and its joint venture with Japan Tobacco.

The investment case for Altria, more than ever, depends on the U.S. market’s shift to Reduced Risk Products being relatively slow. For now, this is our base case, and Altria stock has an undemanding 9.5x P/E and 8.1% Dividend Yield. Our base case forecasts indicate a total return of 50% (15.5% annualize) by 2025 year-end, but there is a material risk of an outcome much worse than the base case. We reiterate our Buy rating for now but will monitor the company closely.

Altria Buy Case Recap

Our investment case on Altria has been based on the continuing ability of its cigarette business to deliver on its traditional earnings algorithm, which includes:

- A low-to-mid single-digit annual decline in cigarette volumes

- A mid-to-high single-digit annual rise in average cigarette prices

- Together these give a low-single-digit annual growth in revenues

- Revenues After Excise tend to grow even faster as excise growth lags

- EBIT margin expands with higher unit price and operational savings

- Including buybacks, EPS tends to grow at mid-to-high single-digits

The U.S. cigarette market has historically been exceptionally profitable, due to relatively favourable tax levels and FDA regulations serving as strong barriers to entry against most potential competitors.

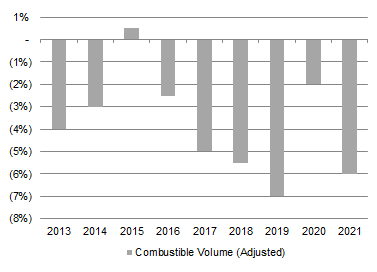

Altria’s cigarette volume decline accelerated during 2016-19, partly attributed to an explosive growth in U.S. e-vapor. However, Altria still guided to an EPS growth of 4-7% in both 2019 and 2020, and achieved 5.8% in 2019. FDA actions against vaping in late 2019 sent e-vapor volume into a decline until Q1 2020, after which modest growth resumed. The COVID-19 outbreak boosted U.S. cigarette consumption from 2020, as pandemic restrictions generated more smoking occasions and government stimulus programs supported smokers’ disposable incomes. Altria’s cigarette volume decline decelerated to just 2% in 2020, and was just 4% during H1 2021 (but rose to 6% for the full year).

|

Altria Cigarette Volume Declines (Adjusted) (2013-21)  Source: Altria company filings. NB. Figures adjusted for inventory movements. |

Operational results have been weak in 2022, with H1 results showing Altria’s cigarette volume falling 9%, Net Revenues After Excise falling 2.9% and Operating Companies Income (“OCI”, equivalent to EBIT) rising just 0.8% year-on-year.

Q3 results were again weak operationally, though more due to macro than competition.

Altria Q3 Results Headlines

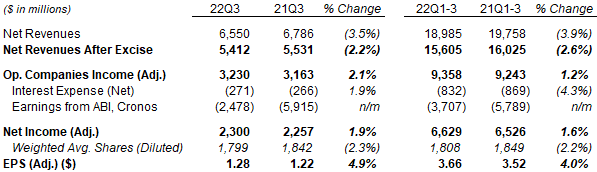

In Q3 2022, Altria’s Adjusted EPS grew 4.9% year-on-year, but half of this was driven by buybacks cutting the share count. Net Income grew 1.9%, in line with Adjusted OCI growth of 2.1%, and Net Revenues after Excise fell 2.2%:

|

Altria Group P&L (Q3 & YTD 2022 vs. Prior Year)  Source: Altria results release (Q3 2022). |

Q3 year-to-date results were similar, with Adjusted EPS growing just 4.0%, Adjusted OCI growing just 1.2%, and Net Revenues After Excise fell 2.6%.

As before, the Smokeable segment dominated the group with nearly 90% of group Adjusted OCI. Smokeable Adjusted OCI grew 1.8% year-on-year in Q3 and 2.6% year-to-date:

|

Altria OCI by Segment (Q3 & YTD 2022 vs. Prior Year)  Source: Altria results release (Q3 2022). |

Excluding the divested Wine segment, Adjusted OCI grew 3.0% for Q3 and 1.9% year-to-date.

Management narrowed full-year 2022 outlook slightly, and now expects Adjusted EPS growth of 4.5-6% (was 4-7%).

Altria Cigarette Volume Fell 10% Again

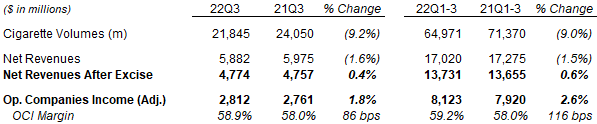

In Q3, Altria’s cigarette volume fell 10% year-on-year excluding inventory, and by 9.2% as reported. With a 6% rise in Marlboro’s retail pack price and the usual dynamics like lagging excise duties, net price realization was 10.2%, which meant Net Revenues After Excise was up 0.4%; Adjusted EBIT was up 1.8% thanks to lower costs:

|

Altria Smokeable Financials (Q3 & YTD 2022 vs. Prior Year)  Source: Altria results release (Q3 2022). |

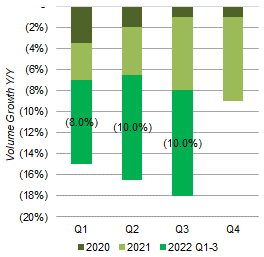

Adjusted for inventory, Altria’s cigarette volume decline has been getting worse through 2022, both on a year-on-year basis and on a “stacked” basis that includes the prior two years:

|

Altria Cigarette Volume Declines (Adjusted) (Since 2020)  Source: Altria company filings. |

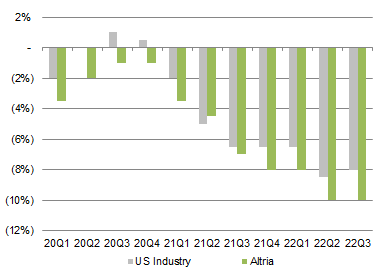

Altria’s volume decline has been partly driven by exceptional macroeconomic headwinds that saw industry volume declines similarly re-accelerating since 2020, especially in recent quarters:

|

1-Year Cigarette Volume Decline – Altria vs. Industry (Since 2020)  Source: Altria company filings. |

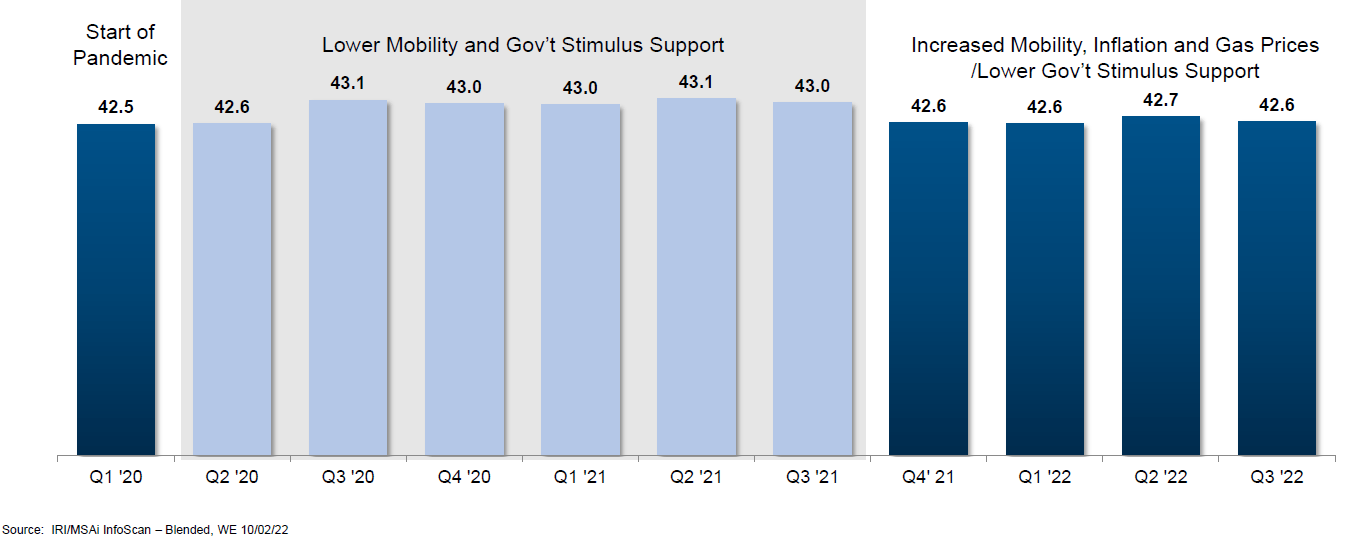

Altria’s volume decline is also partly a reversal of a temporary boost during COVID-19, when pandemic-related factors pushed Marlboro’s retail share from 42.5% to a peak of just over 43%, before returning to 42.6% in Q3 2022:

|

Marlboro U.S. Retail Share By Quarter (Since Q1 2020)  Source: Altria results presentation (Q3 2022). |

We do not believe competition from Reduced Risk Products (“RRP”) has been a factor in the acceleration of Altria’s cigarette volume decline this year. E-vapor category volume fell by 7% sequentially in Q1 2022 following FDA actions against the category, and stagnated in Q2; Oral Tobacco volume, on a trailing-six-month basis, was flat year-on-year as of September; Heated Tobacco products remain unavailable in the U.S. following the ITC import ban that was implemented in November 2021.

What is more cornering is that Altria’s strategic position has worsened considerably for the future.

Altria’s Strategic Situation Has Worsened

Altria has announced key changes in its relationships with Philip Morris and Japan Tobacco.

On October 20, Altria announced that it has agreed to return its exclusive U.S. license for PM’s IQOS Heated Tobacco products after April 2024, in return for $2.7bn in cash ($1.0bn paid immediately, the rest to be paid with interest by July 2023). PM had guided to IQOS becoming available in the U.S. again in H1 2023 with domestic manufacturing.

Philip Morris is set to compete with Altria in its U.S. home market. PM has a pending offer for Swedish Match (OTCPK:SWMAY) with an acceptance deadline of this Friday (November 4). We expect this offer to fail, but PM has explicitly stated at its Q2 results that it will enter the U.S. market in any case, if necessary by building its own sales and distribution. In addition to IQOS, PM has other products that it can launch in the U.S. over time, including:

- VEEV e-vapor device, now on sale in several European countries and for which PM will apply for a PMTA (Pre-Market Tobacco Product Application) in “early 2023”

- ILUMA Heated Tobacco device, the next-generation product now on sale in Japan and several European countries, and for which PM will apply for a PMTA in H2 2023; it is not affected by the ITC import ban

- VEEBA disposable e-vapor product, launched in Canada in Q2 2022

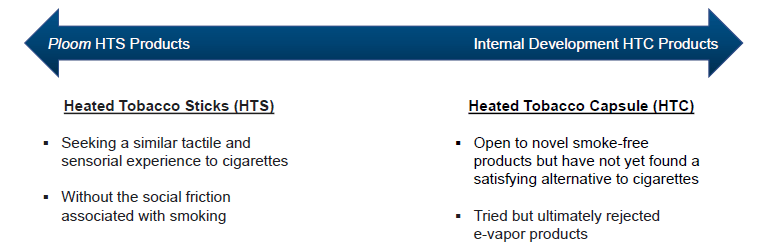

Altria’s answer to the pending loss of its U.S. IQOS license is a new 75/25 joint venture with Japan Tobacco (referred here as “JT”), announced on October 27, under which JT will supply Altria with a future Heated Tobacco Stick device under its Ploom brand. Altria is funding the JV with a $150m capital injection and will be making its own Marlboro-branded consumables. The two companies expect to file a PMTA for Ploom in H1 2025.

Separately, Altria continues to develop its own Heated Tobacco Capsule device, and expects to file a PMTA for it by 2024 year-end. This device is targeted at a different demographic from Ploom, specifically smokers who are “open to novel smoke-free products”, including those who have “tried but ultimately rejected e-vapor products”. We believe Altria intends this to be its answer to Juul, for which Altria has opted to terminate its non-compete in September.

|

Altria Planned Heated Tobacco Products  Source: Altria results presentation (Q3 2022). |

Atria has also agreed to launch its Heated Tobacco Capsule product in an international test market with JT’s sales and distribution network. However, the agreement on the global partnership is described as “non-binding”.

We are pessimistic about these Altria initiatives.

- First, Altria will not be able to launch either Heated Tobacco product in the U.S. for a while, and will almost certainly be launching them after PM has started selling IQOS in the U.S. directly. As a PMTA typically takes several years for the FDA to approve (two for IQOS, four for Swedish Match’s snus), Altria’s products will likely be available no earlier than 2016, at which point PM would have been selling IQOS in the U.S. directly for more than 18 months.

- Second, Ploom has so far not been a viable competitor to IQOS. Even in Japan, JT’s home market where it has nearly 50% of the cigarette market, Ploom has less than 8% of the Heated Tobacco category, a distant #3 behind PM IQOS’ roughly 65% and British American Tobacco’s (BTI) glo’s roughly 20%. Ploom is only on sale in three countries in Europe.

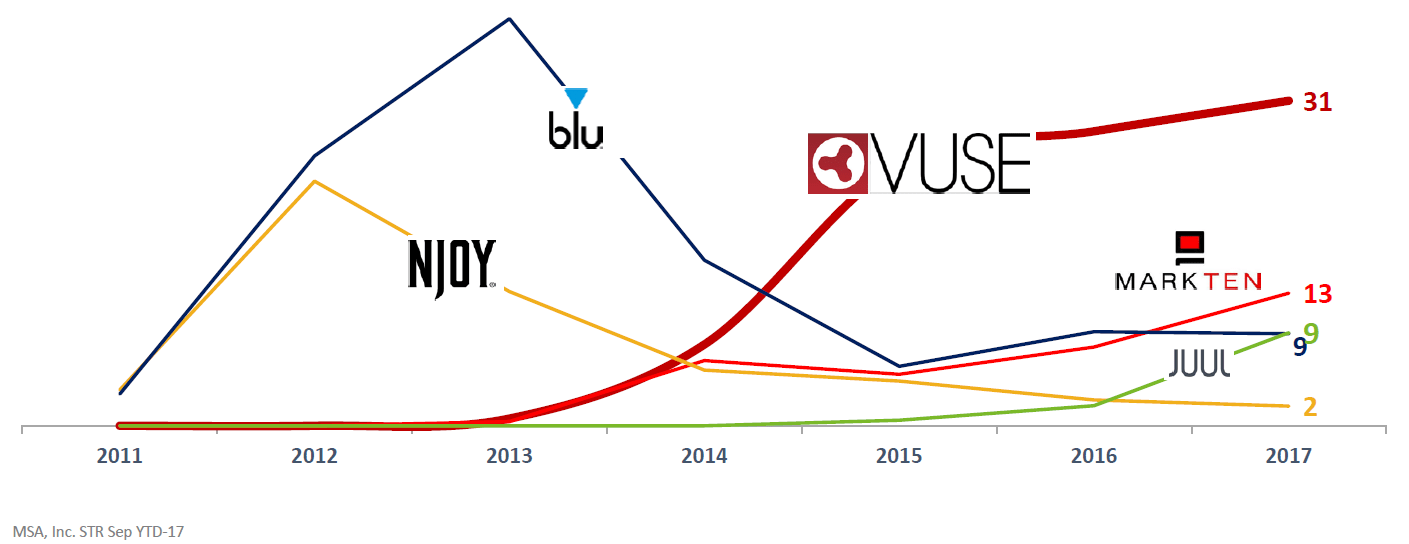

- Third, Altria itself has a poor track record in launching new products. MarkTen, its attempt at closed tank e-vapor before Juul, had mostly been an also-run #3 player in the U.S., becoming #2 briefly in 2017 before being overtaken by Juul:

|

U.S. E-Vapor Players By Market Share (2011-17)  Source: British American Tobacco investor day (2017). |

Ultimately, we believe it was unwise for Altria management to have allowed the relationship with PM to have broken down so completely, especially with its historically lukewarm efforts in selling IQOS, reaching the minimal market share required to renew its license before the ITC ban.

Altria’s weakness in competing in new product categories was also visible in its Oral Tobacco results in Q3.

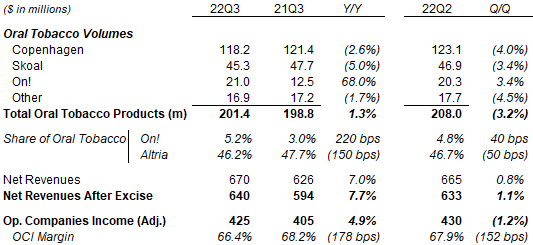

Altria Still Losing Share in Oral Tobacco

Altria’s total Oral Tobacco volume grew just 1.3% year-on-year in Q3, with growth in its On! nicotine pouches offset by losses in its larger Copenhagen and Skoal moist snuff lines. While On! gained 2.2 ppt share in the oral tobacco category compared to last year, Altria ‘s overall category share fell 1.5 ppt to 46.2%:

|

Altria Oral Tobacco Financials (Q3 2022 vs. Prior Periods)  Source: Altria results releases. |

Oral Tobacco Net Revenues After Excise were up 7.7% year-on-year in Q3, but Adjusted OCI rose just 4.9%, “primarily due to higher investments behind On!”. Year-to-date Adjusted OCI was down 1.2%.

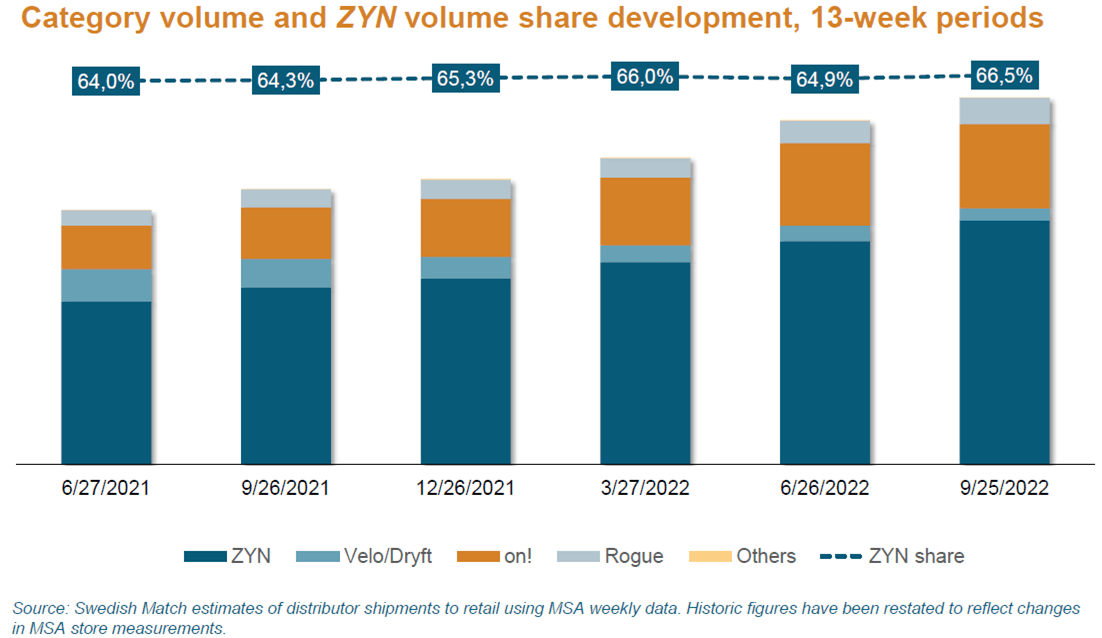

We know from Swedish Match that its ZYN nicotine pouches continue to dominate the category with a 66.5% share in Q3 2022, up 0.6 ppt sequentially and 2.2 ppt year-on-year; Altria has achieved some volume growth for On!, but British American Tobacco’s Velo/Dryft has actually been losing volume in absolute terms, showing that existing scale and distribution are not always sufficient for an incumbent to triumph in a new category:

|

U.S. Nicotine Pouches Volume & Market Share (Since Q2 2021)  Source: Swedish Match results presentation (Q3 2022). |

Altria may end up struggling similarly in Heated Tobacco when it competes with Philip Morris.

How Bad Can Things Get for Altria?

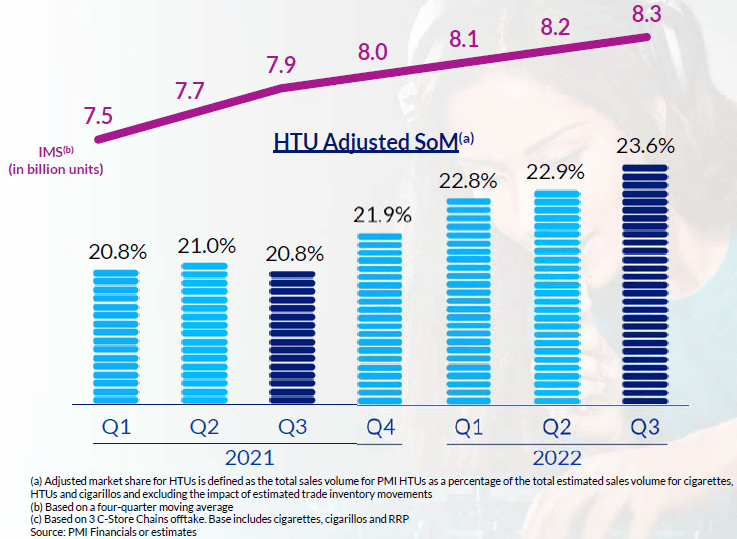

Japan Tobacco’s domestic business offers clues on what a worse-case scenario may look for Altria.

Since an initial launch in 2016, PM’s IQOS has taken nearly 24% of the total tobacco market in Japan, while the Heated Tobacco category overall is now more than 30% of the market:

|

PM IQOS Share of Japan Tobacco Market & Volume (Since 2021)  Source: PM results presentation (Q3 2022). |

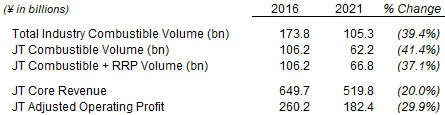

During 2016-21, total industry combustible volume fell by 39% in Japan, with JT’s own Combustible volume falling 41%. Even with price increases and cost savings, by 2021 (the last year JT disclosed Japan-only financials), JT’s domestic tobacco business has lost 20% of its Core Revenue and 30% of its Adjusted Operating Profit:

|

JT Domestic Tobacco Volume & Financials (2021 vs. 2016)  Source: JT company filings. |

JT’s share price has fallen 29% in JPY in the past 5 years.

An outcome for Altria would be disastrous for shareholders.

Why Is Altria Still A Buy?

We still have a Buy rating for Altria because our base case is still for the U.S. market to shift to RRPs relatively slowly, and because MO stock has an undemanding valuation.

Regulations may still reduce the availability of RRPs. IQOS’s entry into the U.S. is certain, because it has already been authorized by the FDA in 2019 and in fact given a Modified Risk Tobacco Product (“MRTP”) status in 2020. We also believe ZYN will be approved, being similar to the already-approved snus (which also have MRTP status), and with Swedish Match having submitted its PMTA in 2020. However, the vast majority of e-vapor products remain unapproved, and several key players such as Juul and Imperial Brands’ (OTCQX:IMBBY) myblu have received Marketing Denial Orders.

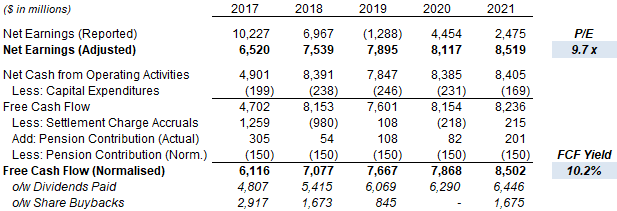

Altria stock also has an undemanding valuation. At $46.14, relative to 2021 financials, MO stock has a 9.7x P/E and an 10.2% Free Cash Flow (“FCF”) Yield (normalized):

|

Altria Valuation & Cashflows (2017-21)  Source: Altria company filings. |

Relative to the midpoint of the latest 2022 EPS guidance ($4.81-4.89), Altria’s P/E multiple is 9.5x.

The Dividend Yield is 8.1%, from a dividend of $0.94 per quarter ($3.76 annualized). Altria targets an 80% Payout Ratio, and the dividend was raised by 4.4% in August 2022.

Buybacks totalled $1.45bn in Q1-3 including $368m in Q3 at an average price of $43.68. The current buyback program has $375m left and will be completed by year-end.

Altria finally wrote down the value of its Anheuser-Busch InBev (BUD) stake by $2.5bn at Q3 results. Management still believes “ABI’s share price will recover”, though it “will take longer than previously expected”. This means that Altria is unlikely to sell its ABI stake in the near term.

We expect a new share repurchase program to be authorized next year. Net Debt / EBITDA was 2.1x at Q3 (with Net Debt of $23.8bn), and Altria will receive another $1.7bn plus interest from PM before July 2023.

Altria Stock Forecasts

We update the assumptions in our forecasts only slightly, as the effects of PM entering the U.S. market may not be material within our forecast period. However, we reduce our exit multiple significantly to reflect Altria’s higher competition risks. Our assumptions now include:

- 2022 EPS of $4.85 (unchanged)

- 2022 share count of 1,799m (was 1,827m)

- From 2023, Net Income growth of 4% (unchanged)

- Share count to fall by 2% annually (was 1%)

- Dividend Payout to be 80% (unchanged)

- P/E at 9.5x at 2025 year-end (was 11.0x), implying an 8.4% Dividend Yield

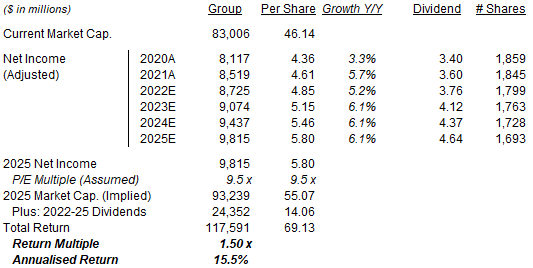

Our new 2025 EPS forecast of $5.80 is 3% higher than before ($5.62):

|

Illustrative Altria Return Forecasts  Source: Librarian Capital estimates. |

With shares at $46.14, we expect an exit price of $55 and a total return of 50% (15.5% annualized) by 2025 year-end.

These figures reflect our base case, our view of what is most likely to happen. However, there is a material risk of an outcome much worse than the base case, namely PM disrupting the U.S. market quickly and significantly.

Is Altria Stock A Buy? Conclusion

We reiterate our Buy rating for now but will monitor the company closely.

Be the first to comment