FatCamera Alpine

“If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.” – Warren Buffett

Author’s Note: This article is an abridged version of an article originally published for members of the Integrated BioSci Investing marketplace on October 25, 2022.

Biotech investing is a noble endeavor that can be highly profitable for you in the long run. Of ten companies that you invest in, you’d simply need two to three to become multi-bagger investments for your portfolio to outperform the market. Now, there are many hurdles (especially clinical data reporting) that the company must clear over the years. As such, you should adjust your position accordingly based on changes in the stock’s fundamentals.

That being said, Alpine Immune Sciences (NASDAQ:ALPN) is undergoing significant fundamental changes. The company recently dropped one of its key molecules dubbed davoceticept. In this research, I’ll feature a fundamental analysis of Alpine while focusing on the recent development relating to clinical trial stoppage.

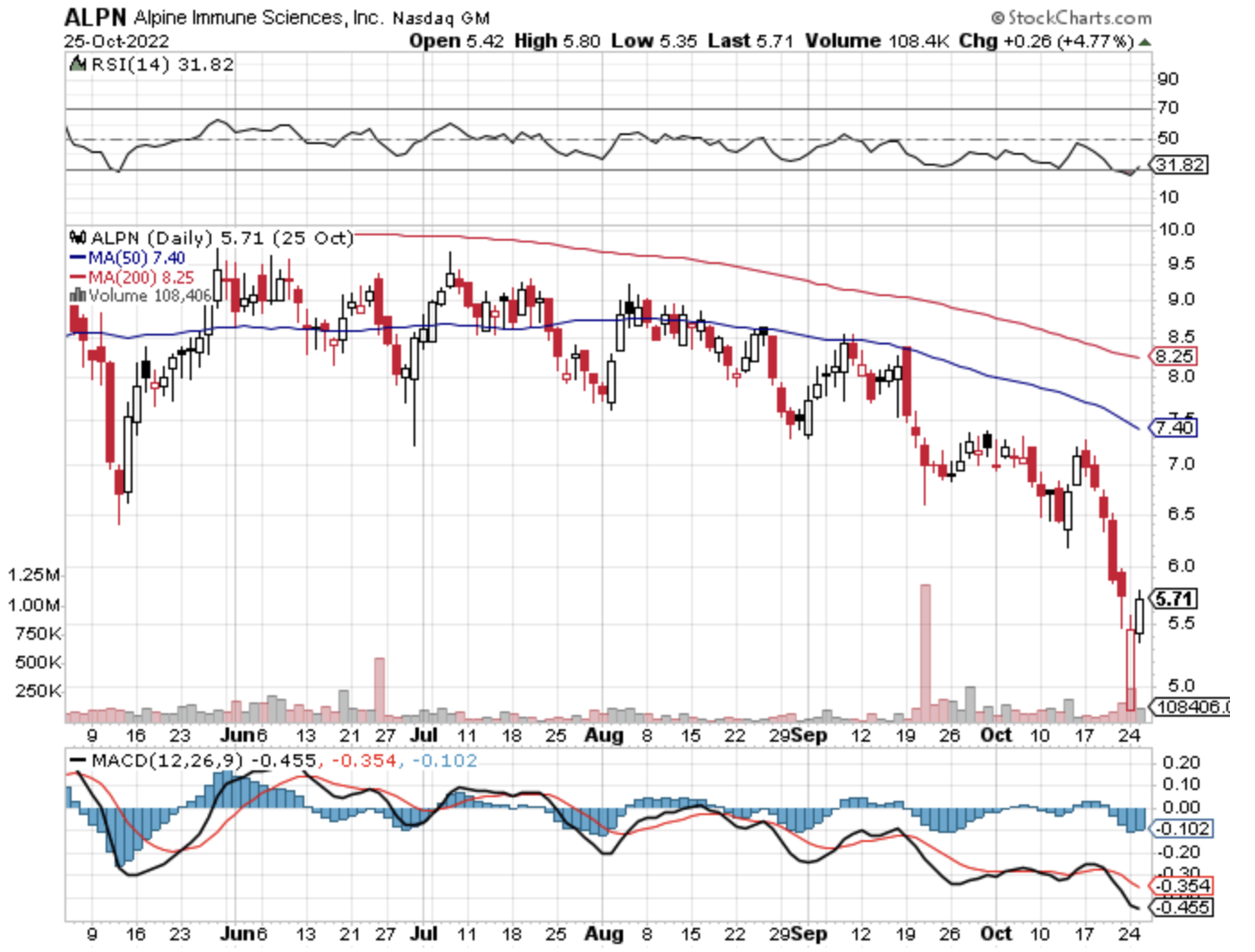

StockChart

Figure 1: Alpine chart

About The Company

As usual, I’ll present a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Operating out of Seattle, Washington, Alpine dedicates its efforts to the innovation and commercialization of novel medicine to fulfill the unmet needs of cancer as well as inflammatory and autoimmune conditions. I noted in the prior research:

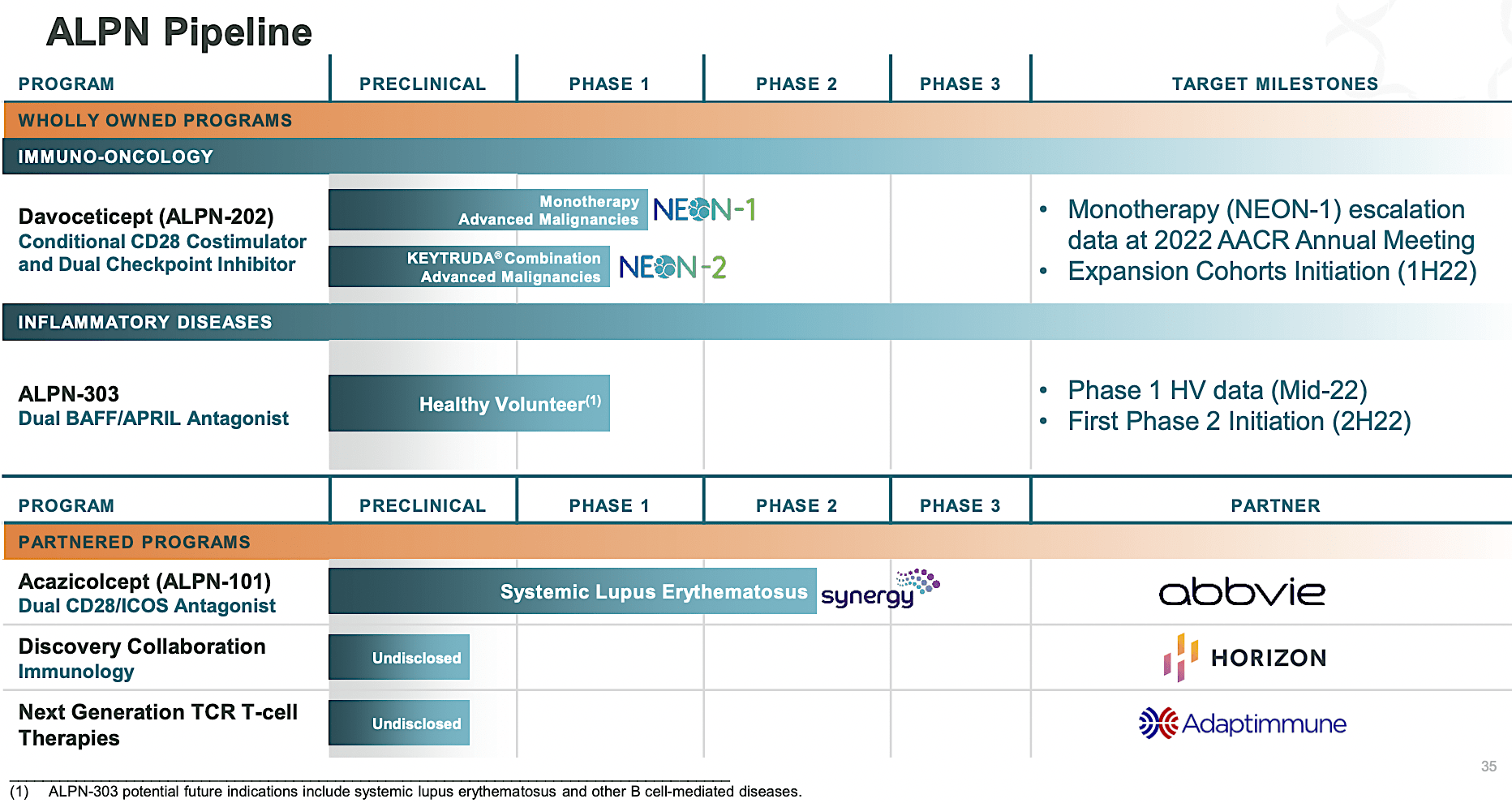

Riding the Directed Evolution platform, Alpine is brewing a deep pipeline of highly promising therapeutics. As such, the company is poised to lead the innovation landscape in immunotherapy. As shown below, ALPN101 (acazicolcept, i.e. Acazi) and ALPN303 are catered for inflammatory diseases. Meanwhile, ALPN202 (davoceticept, i.e., Davo) is being developed as an immuno-oncology medicine to treat various cancers. That aside, there are other preclinical assets in the discovery phase with partners, Horizon (HZNP) and Adaptimmune (ADAP).

Alpine

Figure 2: Therapeutic pipeline

Tracking Alpine Investment Thesis

Before proceeding with the analysis, you should put Alpine into the appropriate investment category. That way, you can better track its progress to know whether the thesis (i.e. story) is playing out as it should. In doing so, you’d know when to buy, sell, or hold your shares.

Alpine fits into the usual “growth biotech” category. As such, you want to monitor developments pertaining to their lead molecules: ALPN202, ALPN101, and ALPN303. Here, you want to see clinical trial advancing and with results. Moreover, you should keep track of any research/development/commercialization partnership.

Significant Partnership

As you can appreciate, a partnership provides several functions for a small/young biotech company. First and foremost, the partner would help absorb the costs associated with the capital-intensive therapeutic development process. Second, they can either take over the future launch or co-launch the drug with the smaller operator. Third, they provide their development expertise as well as their relationship with the FDA. Fourth, they instill confidence in investors. After all, there is no point in doing a partnership unless the partner sees great value in the development pipeline. I shared in the prior article:

Back on December 16, Alpine disclosed the mega partnership with Horizon Pharma for the development of up to four pre-clinical molecules for $1.52B in total milestone. Then, there are tiered royalties of net sales. You can see that the deal was financed by all the big-name funds such as De Cheng Capital, OrbiMed, and Frazier. Therefore, Alpine certainly has the support of “heavy hitting” funds.

Aside from Horizon, Alpine formed a substantial partnership with AbbVie (ABBV) for Acazi. The agreement enabled Alpine to earn $60M upfront coupled to various payment options (i.e., $45M, $30M, and $75M) and different milestones (i.e., $205M and $450M) payouts. Moreover, Alpine is set to receive the high single and low double-digits on sales royalty. With AbbVie’s vast sales infrastructure, Acazi has the best chance of becoming a blockbuster.

Previous ALPN202 Debacle

Shifting gears, let us walk through other shifting fundamental developments of Alpine. As an investigational CD28 costimulator and dual immune checkpoint inhibitor, Davo is one of Alpine’s three most advanced molecules. Accordingly, Davo’s efficacy and safety were put to the test in two trials for advanced/resistant cancers: NEON-1 (i.e. monotherapy) and NEON-2 (combo with Keytruda).

As you recall, the FDA previously placed a “partial clinical hold” on NEON-2 due to a report of Grade 5 serious adverse event. That is to say, one patient on the trial died. Notably, the death was due to cardiogenic shock which was caused by either immune-mediated myocarditis or possibly infection. During the time, there was no definitive evidence that the drug caused the death. Importantly, the “Disease Context” is that the patient was already extremely sick and failed multiple therapies.

You can see that CD28 modulation has historically been associated with a higher chance of seeing patient death related to cardiovascular causes. As such, there are only a few (i.e., only six) current studies targeting CD28.

Bernstein

Figure 3: Thin pipeline targeting CD28

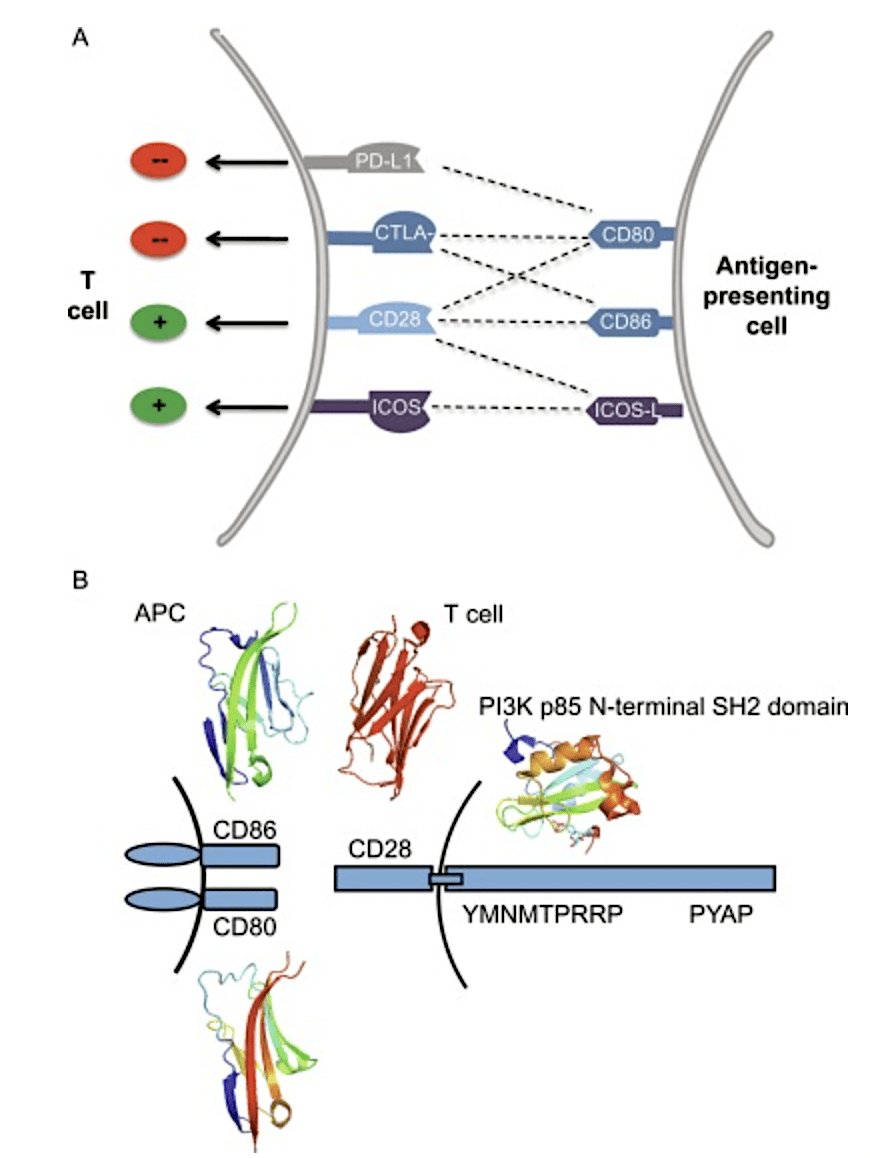

Now, the reason that companies are still tinkering with CD28 modulation is that it is a highly promising target/receptor on T-cells. As the “the General” of the body’s natural defense (i.e., immune) system, T-cells are crucial to the destruction of cancers and viruses.

When an immune cell eats up and thereby processes an invader, it would then present fragments of the foreign entity (i.e., antigen) to the T-cells. Then, bidding between the antigen-presenting cells occurs with the CD28 receptor occurs. And, that interaction would then activate the body’s defense system to get rid of either the virus or cancer.

Frontiers

Figure 4: CD28 roles in T-cell and antigen-presenting cells

Due to its crucial roles, companies like Alpine are still tinkering with the “right dosage” of CD28 and/or a combo drug. Following the partial clinical hold, Alpine went back to the drawing board to find the proper dosage as well as adjust clinical protocols. As such, the FDA correspondingly removed the said hold on May 24 as I forecasted.

Current Davo Problem

As loose ends, Alpine has not been able to get the optimal dosage. Moreover, I believe that the combo with Keytruda may be the issue. Consequently, another patient died on the NEON-2 trial. Like the first death, the Disease Context is similar for the second patient. That is to say, the patient was also very sick with metastatic colorectal cancer and exhausted multiple prior therapies. Importantly, the cause of death is also related to cardiogenic shock.

Following the event, Alpine issued a press release on October 24 stating that the company terminated Davo’s development to focus on Acazi and ALPN303. As a ramification, both NEON-1 and NEON-2 would be halted.

In my view, the problem with ALPN303 is likely that the dosage was too strong. Moreover, the drug already has a built-in dual target-hitting “Mechanism of Action.” That is to say, it (1) turns on CD28 and (2) removes another immune checkpoint break. As such, when you put that dual function into a combo treatment with another immune checkpoint inhibitor (i.e., Keytruda), the drug becomes too strong. Consequently, the “aggressive hit” must have overwhelmed the immune system which leads to the patient’s demise.

Of note, a drug with adverse effects can still be approved and launched so long as the overall benefit trumps the risks. Nevertheless, after two or more deaths, you can see that Alpine is right for Alpine to terminate Davo’s development. That way, they can focus on more promising development with Acazi and ALPN303. Else, future safety data would likely be bleak. Commenting on the unfortunate event, the Chairman and CEO (Dr. Mitchell Gold) remarked:

Patient safety remains our highest priority. We have determined it is in the best interest of all patients to terminate enrollment in the davoceticept studies and we will continue to work with the FDA, Merck, the study Safety Monitoring Committee, and the study investigators to further understand this important safety issue. Davo has shown encouraging signs of clinical activity and it is unfortunate we have not yet been able to identify a safe dose regimen for the combination with pembrolizumab. We will now prioritize the bulk of our development resources towards advancing our lead wholly-owned program ALPN303 in multiple autoimmune and inflammatory indications, as well as acazicolcept in SLE in collaboration with AbbVie.

Path Ahead

As Dr. Gold mentioned, Alpine is now highly focused on ALPN303 and Acazi. While you might not like to hear this, I believe that’s a prudent move rather than trying to pick the higher-hanging fruit (Davo). In the therapeutic development process, many molecules will fail, and only a few succeed. Hence, it’s best to terminate programs at the earliest signs of failure. That way, the company can conserve cash and not waste precious time.

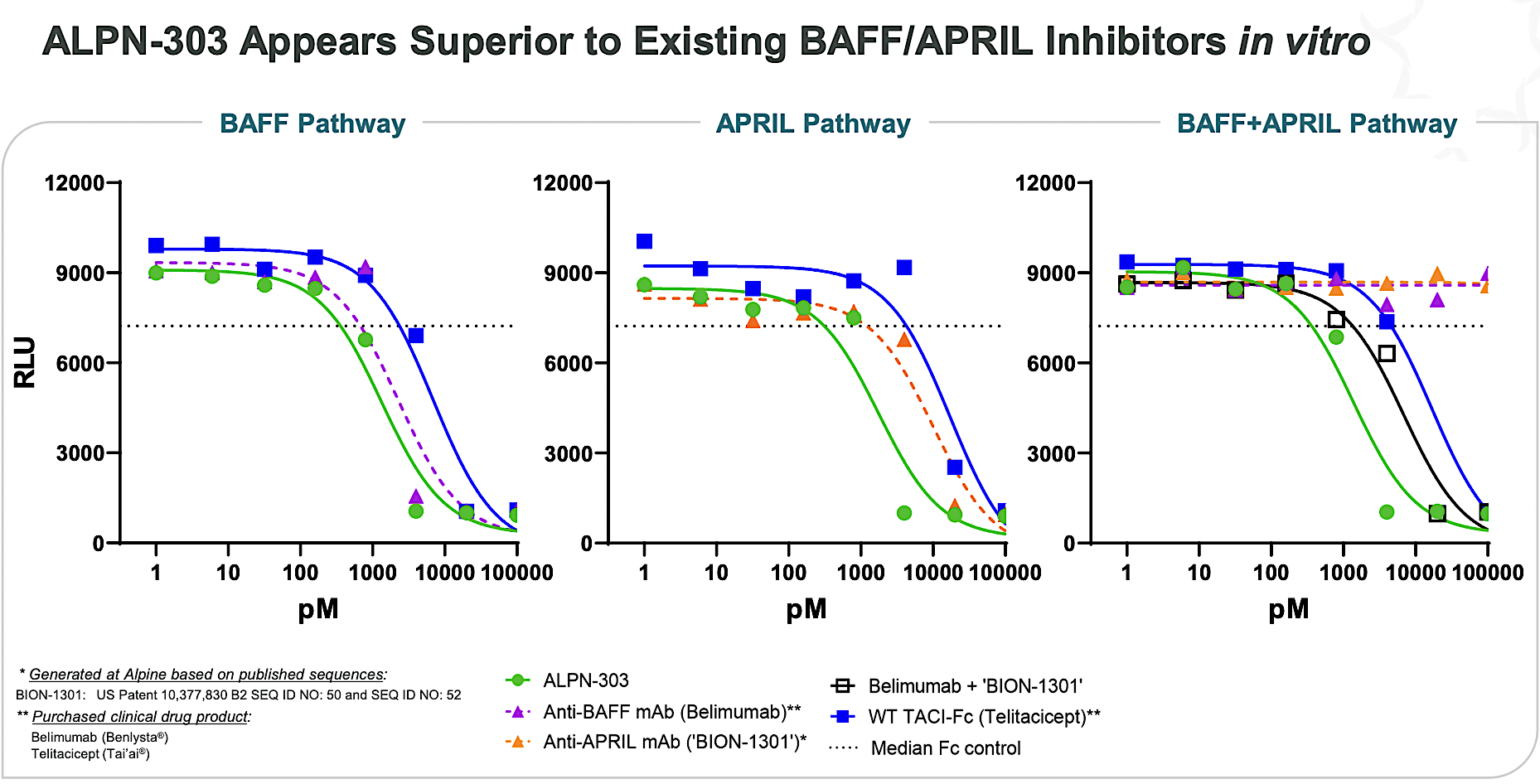

Of ALPN303 and Acazi, the dual BAFF/APRIL B cell cytokine inhibitor (ALPN303) is designed to potentially be the “best-in-class.” When you develop a new drug, you either want your drug to be the “first” or completely different from competing molecules. After all, that would help you garner the most market success.

On that note, I believe that Acazi is a better molecule than ALPN303 because the latter is indeed a “first-in-class” dual CD28/ICOS inhibitor in development for SLE in collaboration with AbbVie. It’s quite likely that AbbVie formed the partnership because Acazi is the “first” in class rather than another “me too” molecule. Just as important, Acazi posted strong early data as shown below.

Alpine

Figure 5: Preclinical data of ALPN303

You might also raise concerns that Acazi also has the CD28 target. However, the Disease Context here is that the patient with SLE is not as sick as those afflicted by resistant cancer. In contrast to cancers where the immune system is already suppressed, SLE patients suffer from an overactive immune system. As such, treating SLE patients with CD28 would be lifesaving whereas it would be devastating for patients afflicted by cancers. Hence, I forecast that inhibiting CD28 for patients with an overactive immune would lead to excellent safety/efficacy. For a detailed analysis of ALPN303 and Acazi, you can refer to the previous research.

Competitor Landscape

Competition in the immuno-oncology space is intense. Notwithstanding, the differentiation quality of Alpine’s drugs confers a market advantage. As I shared in the prior article:

Alpine goes toes-to-toes with conventional chemoradiation therapies for various cancers. Then, there are novel treatments like CAR-T, CAR-NK, and CAR-macrophage. Notably, CAR-T is already approved for blood cancers. Though these novel CARs have not been proven effective for solid tumors, that’s where future developments are heading. You can bet there will be some CARs that would be highly effective against solid tumors.

That aside, there are also the tumor-infiltrating lymphocytes (i.e., TILs) of Iovance Biotherapeutics (IOVA) that have demonstrated robust efficacy for cancers. Regardless of the competition, there is always a strong demand for novel therapeutics like those of Alpine. The oncology space is vast and thereby affords many blockbusters.

Financial Assessment

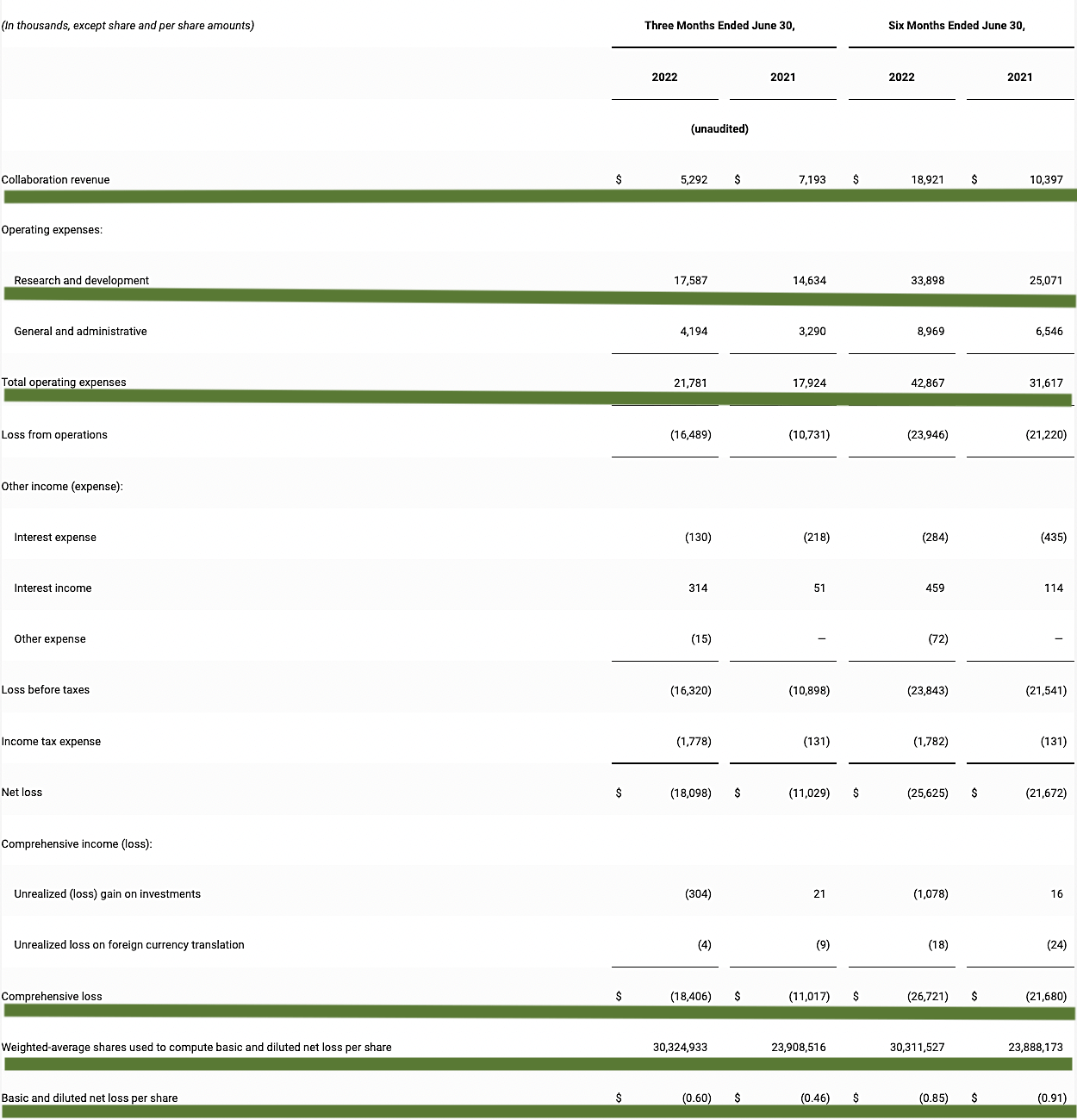

Just as you would get an annual physical for your well-being, it’s important to check the financial health of your stock. For instance, your health is affected by “blood flow” as your stock’s viability is dependent on the “cash flow.” With that in mind, let us assess the 2Q 2022 earnings report for the period that ended on June 30.

As it’s a clinical-stage company, Alpine has yet to make huge revenues beyond some money from the collaborative agreement. Of which, the company procured $5.7M compared to $7.1M for the same period a year prior. The collaborative revenue for this quarter comes from both AbbVie and Horizon.

That aside, the research & development (R&D) for the respective quarters registered at $17.6M and $14.6M. I like an increasing R&D trend because the money invested today can turn into blockbuster profits tomorrow. After all, you have to plant a tree to enjoy its fruits. Given that Davo is gone, Alpine would need to ramp up R&D on more pipeline assets to fuel long-term growth.

Additionally, there were $18.4M ($0.60 per share) net losses versus $11.0M ($0.46 per share decline) for the same comparison. On a per-share basis, the bottom-line depreciation widens by 30.4%.

Alpine

Figure 6: Key financial metrics

About the balance sheet, there were $201.2M in cash, equivalents, and investments. On top of the $100M offering recently raised, the total cash position is increased to $301.2M. Against the $21.7M quarterly OpEx, there is adequate capital to fund operations into 3Q2025. Simply put, the cash position is extremely robust relative to the burn rate.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strengths. More importantly, the risks are “growth-cycle dependent.” At this point in its life cycle, the biggest concern for Alpine is whether Acazi and ALPN303 would continue to deliver positive data with big safety issues. The fact that the company ran its trial in Australia entails a termination risk as you saw with Davo. The other risk is if Alpine can maintain its partnership with both Horizon and AbbVie after the recent debacle.

Final Remarks

In all, I reduced my buy recommendation on Alpine Immune Sciences to a hold. Moreover, I lowered my star rating from 4.8 to 4.5/5. Alpine is an interesting growth stock that has undergone many ups and downs over the past few years. And that is reflective of the nature of the therapeutic development process as well as Alpine’s specific fundamental developments. Contrary to the market, I believe that the recent decision to drop davoceticept from development is a prudent move. That way, the company can focus on the low-hanging fruits (Acazi and ALPN303).

Going into next year, Alpine would advance multiple Phase 2 studies for ALPN303 for SLE and three other Phase 1b basket studies. As such, it would be a big catalyst that moves the needles of Alpine’s stock. Last but not least, you want to pay attention to where those studies would be conducted to size up the risks. If they would conduct them in Australia, there’s substantially higher risk than in the USA.

Be the first to comment