Carsten Koall/Getty Images News

After the weak digital advertising numbers from Snap (SNAP), the market expected general weakness from the advertising focused Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL). The company actually delivered numbers generally in line with expectations in a surprise to the market. My investment thesis remains ultra Bullish on the stock as the company continues producing massive results while the market has so many doubts.

Ignore Headlines

Technically, Alphabet missed Q2’22 analyst estimates on both the top and bottom line. Crucial revenue grew at a 13% clip, but the constant currency revenues were actually up 16% YoY to nearly $70 billion.

The tech giant is so large that 16% growth is very impressive. The company has run into prior periods where growth dipped due to currency issues and the stock quickly bounced back when currency issue ultimately normalizes. Remember, Alphabet had tough comps with revenues growing a massive 62% last Q2.

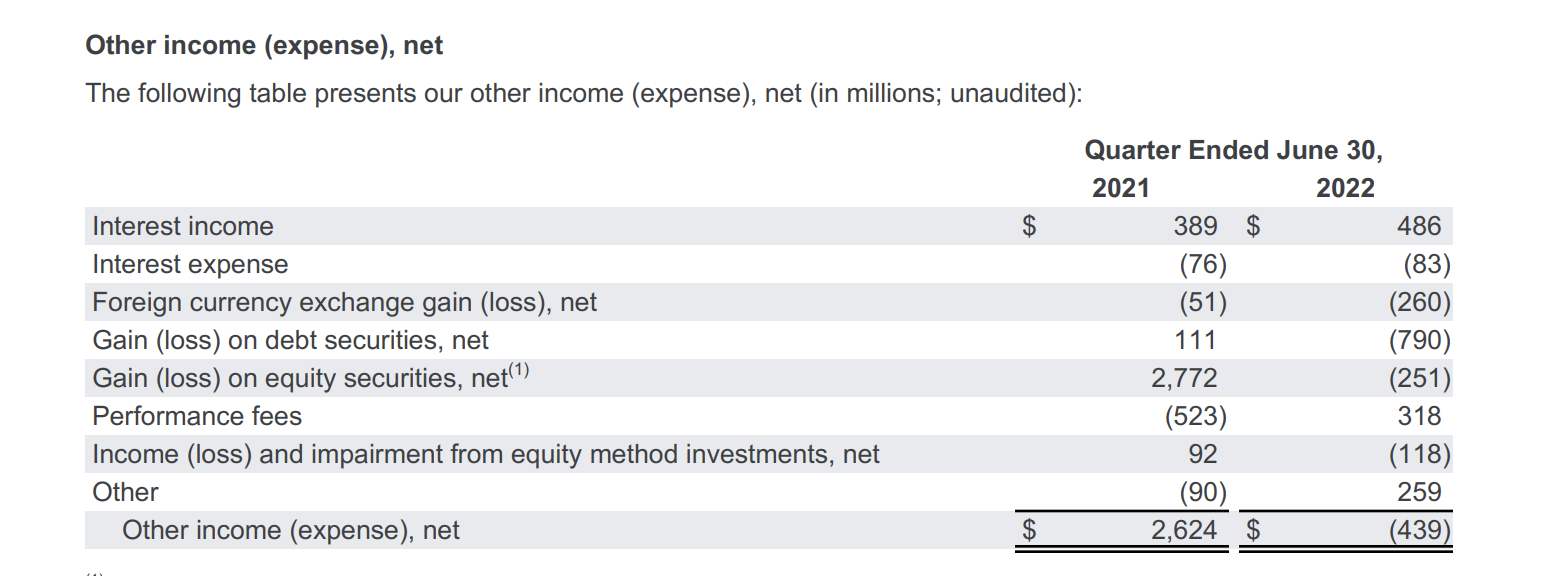

As usual, the GAAP EPS number is virtually worthless due to one-time adjustments and non-cash charges. Alphabet sees the EPS hit with other expenses when the large cash balance and $403 million in net interest income should actually boost net income. For the quarter, other income actually fell $439 million due to over $1 billion in losses from debt and equity securities.

Source: Alphabet Q2’22 earnings release

If Alphabet would provide non-GAAP numbers that excluded these costs, investors could actually compare the EPS targets of analysts. Instead, the company technically missed EPS targets of $1.21 by $0.06, but this number is virtually worthless. Throw in high stock-based compensation costs and Other Bets losses, the GAAP numbers just aren’t very worthwhile.

The tech giant continued to see impressive growth with Google Search ad revenues while YouTube ads were rather weak with growth below 5%. Alphabet continues to report impressive growth in Google Cloud revenues, but the business saw the operating income decline in the sector with a loss of $858 million.

Overall, revenue growth wasn’t the issue with Alphabet adding substantial revenues over the last couple of years.

Stripping Out Costs

The whole tech sector appears set to lower costs with signs Google is going to slow or pause hiring while Meta Platforms (META) might cut staff by up to 10% in a positive move. Alphabet has a similar ability to improve profits via either constraining costs or outright cutting costs.

The tech giant reported June ending employees at 174K, up an amazing 30K from last year. Alphabet grew employees by 20% during a period where revenues only grew 16% on a constant currency basis.

The company should probably have only added about 10% additional employees in order to grow more efficiently. For the quarter, combined R&D and S&M expenses were up ~$3.6 billion YoY providing a clear path to where Alphabet can likely constrain spending in the next year to improve profits.

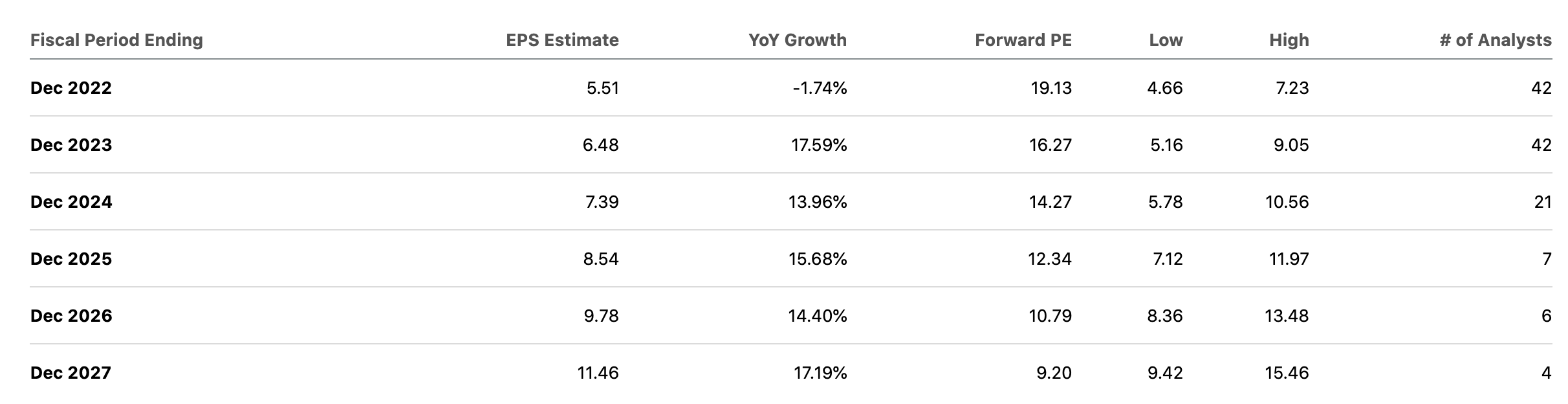

The stock is just too cheap considering the company maintains strong growth, but the stock valuation has dipped. After the stock split, analysts now have Alphabet earning $6.48 per share and these Q2’22 numbers should solidify those estimates.

Source: Seeking Alpha

As highlighted in the past, these numbers are for GAAP earnings that don’t strip out high stock-based compensation. The estimates typically don’t include much impact from other income due to the inability to predict those numbers, which is why the actual quarterly numbers fail to predict the reported GAAP numbers.

Without considering non-GAAP numbers or the large cash balance, Alphabet already trades at only 16x 2023 EPS targets. Considering stock-based compensation reached an incredible $4.8 billion in the quarter, the non-GAAP impact is substantial.

Slower hiring might reduce the SBC charges, but Alphabet is running toward a $20 billion annualized clip. After taxes, the impact is ~$17 billion, amounting to a large $1.25 per share hit to earnings. In essence, Alphabet would be on pace for a non-GAAP 2023 EPS of $7.73 versus the current GAAP estimate of $6.48.

The EV is only ~$1.3 trillion once stripping out the $125 billion net cash balance. The stock only trades at a minimal EV of 12x earnings. Alphabet grew revenue faster than the multiple while the stock should trade at a premium to the growth rate.

Takeaway

The key investor takeaway is that Alphabet remains an insanely cheap stock. Investors should ignore the headlines focusing on the company missing analyst targets and instead focus on the constant currency growth rates and cheap multiple. In addition, the tech giant could generate some leverage in the next year with slower hiring leading to some leverage in the system despite the tough economic scenario unfolding.

Be the first to comment