umdash9/iStock Editorial via Getty Images

Volkswagen (OTCPK:VWAGY) is a German Automaker with multiple brands under its name. The company had been facing headwinds in recent times, but now is back to growing and the latest quarter showed that the results are once again coming in strong.

Note: I had previously covered Volkswagen in another article titled:

Volkswagen Is Undervalued And Is Perfectly Positioned For A Cyclical Upturn:

In the article, I noted that Volkswagen’s price is trading quite cheaply and that despite the pandemic-led declines, the stock was clearly undervalued over the longer period, mainly due to the correct product mix. Since then, Volkswagen has brought on multiple new models, and clearly established itself as a leader in EV sales, especially in Europe. This is further explained in the article.

Volkswagen’s Future Better Than The Current Stock Price Suggests

Overall, the company’s finances point to a relatively cheap valuation, and although there is a reasonable expectation that car companies will struggle in 2023, as financing costs continue to rise, Volkswagen’s current single-digit valuation points to a stock that is relatively cheap. The company currently has a valuation that is around 5x earnings, which is usually reserved for companies in the decline. But Volkswagen is anything but declining, the company has in fact been on the upturn. Considering that revenue is increasing, despite global passenger sales decline, and margins continue to increase, combined with clear dominant market dynamics, which point to Volkswagen stock is relatively cheap.

Despite Passenger Car Volumes Being Under Pressure, VW Continues To Outperform

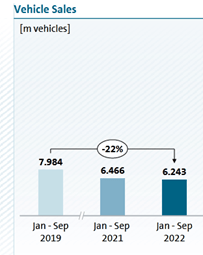

Between January and September 2022, the volume of the passenger car market worldwide declined moderately overall year-on-year (-4.3%), impacted primarily by bottlenecks and disruption in the global supply chains as a consequence of the semiconductor shortage, the coronavirus pandemic and the repercussions of the Russia-Ukraine conflict. While the overall markets in the Asia-Pacific, Middle East, South America, and Africa regions posted slight to moderate growth, the other sales regions saw a drop in volumes. The North America and Western Europe regions recorded a considerably weak sales volume. Sales volume fell very sharply in Central and Eastern Europe.” – Third quarter call

Electric vehicle sales drove the total deliveries, which grew by 10%, YoY for the third quarter. In large part, these deliveries were led by the sale of their electric vehicles which grew by 25%.

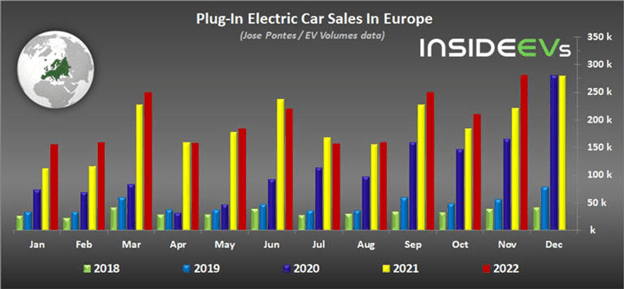

Europe has seen a significant increase in plug-in-car sales mainly with a record 2.18 million cars being sold. Meanwhile, passenger car registration also continued to show significant improvement to 17%, showing that things are returning slowly after post-pandemic effects. The general trend shows electric vehicles are improving significantly as are passenger car sales.

Another factor that is driving car sales is the average age of the vehicle/car market. Cars were already old in 2020, but the pandemic set back car sales further, making the average car even older. Furthermore, shutdowns in China, and North America and inflationary factors led many people to hold back on buying new cars. Now as the base effects wear off and China starts to re-open companies such as VW are primed to once again take advantage of newer models, and product refreshment set to continue the recent momentum of positive revenue growth.

Volkswagen has done relatively well with its ID models and is now slated to increase momentum again with the new ID.4 and ID.7 being highly affordable and globally competitive plug-ins with ranges of up to 275 miles on the ID.4. The competitive nature of the EVs has held up relatively well compared to their counterparts, and even higher-end models. This bodes well for Volkswagen which is looking to run a two-segment strategy, where it continues to offer traditional engines in its luxury segment but offers an electric alternative as well in its more affordable segment. Electric vehicles as a percentage of total car sales continue to increase as well. The ID series now ranks as one of the top-selling models in Europe, which means that at a time when electric vehicles are making up a significant percentage of total sales, VW is right in the middle of the boom.

Increasing Financing Costs Not Likely To Deter Car-Buyers

Financing costs are on the rise as well, but Volkswagens demographics with those buying the higher-end cars, and those buying the more affordable segments may not need as much financing. Financing costs have been on the rise in both Europe and North America, and this has meant that car companies are continuing to struggle. Therefore, I expect VW to weather the effects of the changes much better than its counterparts.

The national average for the US was 5.27% in terms of financing, and costs in other countries are rising as well. But with vehicle age, what it is and Volkswagen’s portfolio targeting the affordable and luxury segments means that financing costs are less likely to be an overall issue.

Indeed EV

Backlog and Margins

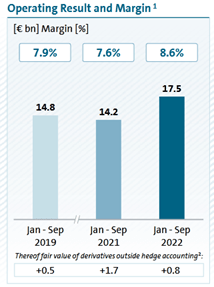

Currently, there is a significant backlog for the company; there was a semiconductor shortage in the latest quarters which led to the company facing adverse effects. These adverse effects resulted in revenue being likely shorter than it was previously. Vehicle sales were down from 2019, but revenue has continued to increase for the past few years. This is due to a mix of improved product sales mix and rising prices. The sustainability of the strategy remains in question as we head into 2023, as consumers have already started showing a slowdown in spending, as savings from the pandemic era wear off. Some of the increase in pricing has led to an improvement in margins, but this is not likely sustainable as there are only so many price increases, that consumers will accept.

Investor Presentation Investor Presentation

Furthermore, Volkswagen should benefit from reopening in China. As more and more consumers who had previously held back spending now do continue to do so. This is another significant factor, as VW continues to be a relatively well-known, and successful brand in China.

But risks remain also, as the global slowdown continues to affect consumer purchasing power. Inflation has been on the rise in Europe and has remained sticky in the US. So while revenue continues to be robust for now, it may be in the future that the company ends up in a situation, where falling savings, and continued inflation, with increasing unemployment dampens sales to the point where the current valuation may not hold up.

But, for now, the future remains bright, and Volkswagen is likely to continue to face multiple tailwinds, as people continue to buy its vehicles. Cars such as the Audi models, the affordable electric, sedan, and hatchback segments are likely to continue to see strong returns relative to their counterparts. This could mean the stock will eventually head back up. Although the broader market continues to be under pressure Volkswagen remains a value stock, with a robust business model, and an improving future, due to the fact that price-to-earnings valuation remains low, the revenue is under no real threat.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment