Roland Magnusson/iStock Editorial via Getty Images

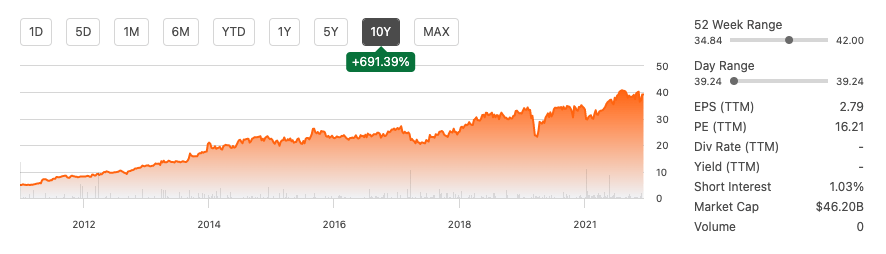

Alimentation Couche-Tard Inc. (OTCPK:ANCUF), (OTCPK:ANCTF) or (TSX:ATD:CA) is the second-largest operator of convenience stores in the States and a global convenience merchandise and fuel competitor. This company has been profitable since its IPO in 1986 and has generously rewarded long-term investors with returns of 691.39%. It has a market cap of $46.065 billion and, for such a stellar performance, is seemingly undercovered.

Ten-year stock trend (SeekingAlpha.com)

Irrespective of market conditions, this company has managed to perform, generating strong cash flow and investing in growth through international acquisitions and rewarding shareholders with upward-trending stock prices and a consistent dividend program. The company invested in a complete unified global rebranding which has given it scalability and competitive advantages in a fragmented industry. There is a lot more upside potential for this company if we look at the 53 new stores completed this year and the 73 stores under various stages of construction to open in the next quarters. Furthermore, it has a long history of solid fundamentals and a healthy balance sheet. It is a safe and sturdy company to invest in, so I recommend taking a bullish stance.

Overview

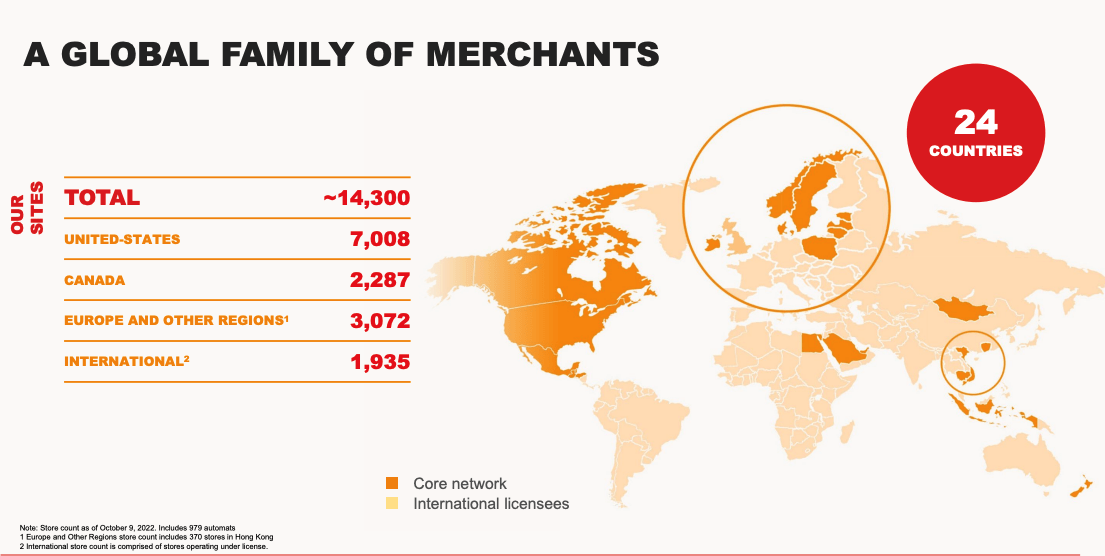

In my previous article, I gave an overview of ANCUF. ANCUF was founded in 1980 as a single convenience store in Canada. Fast forward to today, and we see a company present all over Canada, in 47 US states, with a leading market share across many European markets and entering Asian markets.

International Regions (Investor Presentation 2022)

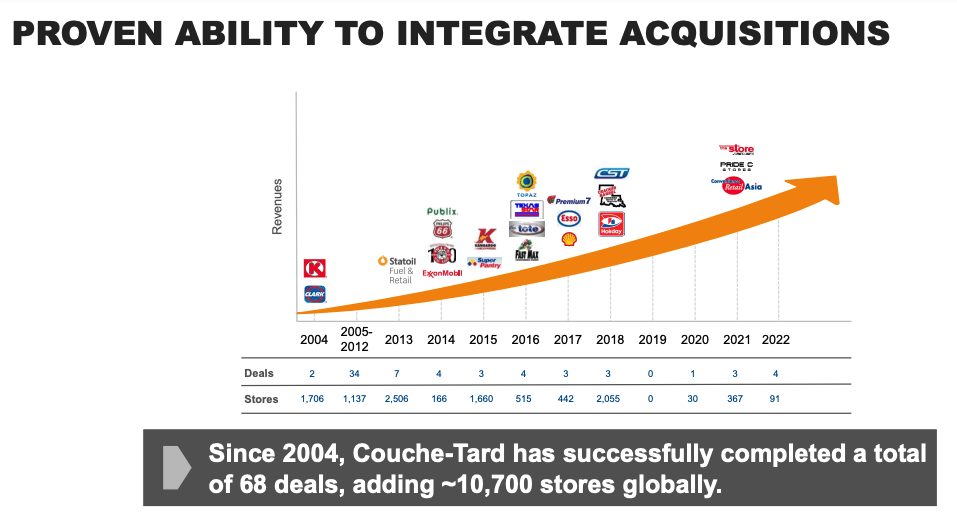

Most of the company’s growth has been through strategic acquisitions, as seen in the image below.

Acquisition History (Investor Presentation 2022)

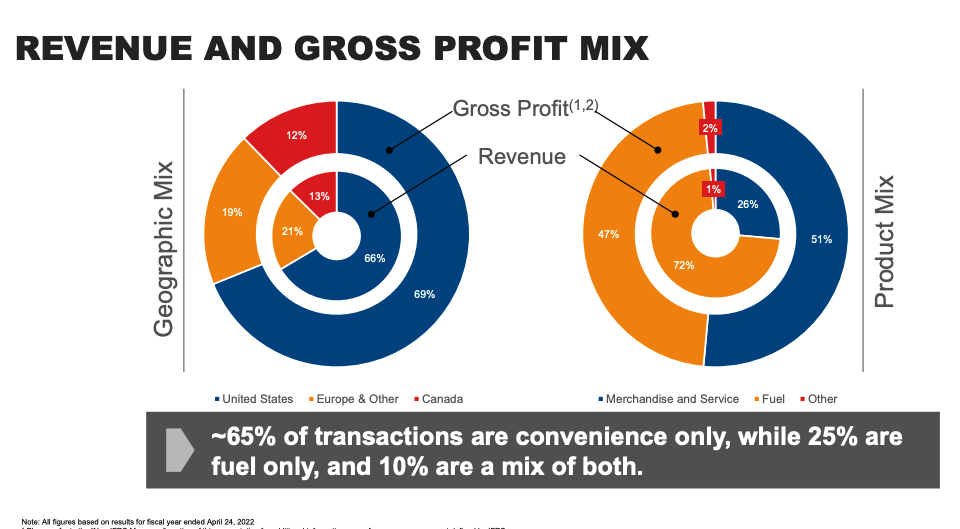

ANCUF geographic markets are, in terms of largest to smallest, the United States, Europe & Other and lastly, Canada. Its product mix is split between Merchandise & Services, Fuel and other. We can see the revenue and gross profit mix of the financial year end of April 2022 below to get an idea of the mix.

Region and Product Mix (SeekingAlpha.com)

ANCUF operates in 14000 stores globally and growing. This fiscal year it has completed the construction of 53 stores in total. Furthermore, there are another 73 stores under construction which will be opening in the next few quarters. Although stores have decentralised operations, the company implemented a massive unification project under the brand Circle K, allowing it to benefit from economies of scale and buying power in a fragmented industry. Currently, 91% of the stores in the States operate under the Circle K brand, 97% in Canada, and 100% in the European region. The company is also tapping into the EV market with its Norway-based EV laboratory.

Financials and Valuation

This company is impressive on many financial fronts. It has maintained an EBITDA CAGR of 20% since 2012 and has remained profitable since its IPO in 1986. Since 2012 it has kept a track record of generating shareholder value averaging return on capital employed of 14.8%. On top of that, the company has maintained a healthy balance sheet.

Although the company is facing considerable challenges concerning high inflation, increased global energy and fuel prices and uncertain market conditions, ANCUF has delivered another consecutively upward quarterly result. ANCUF had a strong Q3 with net earnings of $810.4 million. It works across three regions, namely the United States, Canada, Europe, and other areas. Total merchandise and service revenue was $4.1 billion. The company saw increases in the United States, Europe and other regions but decreased sales in Canada.

Gross margin increased in the USA and Canada to 34% and 33.2%. However, there was a decrease in Europe and other regions to 38.3%. Road transport fuels decreased in all regions. However, the fuel gross margin increased in the United States, with a decrease in Canada, Europe, and other areas. The margins are still high due to favourable market conditions and better supply chain optimisation.

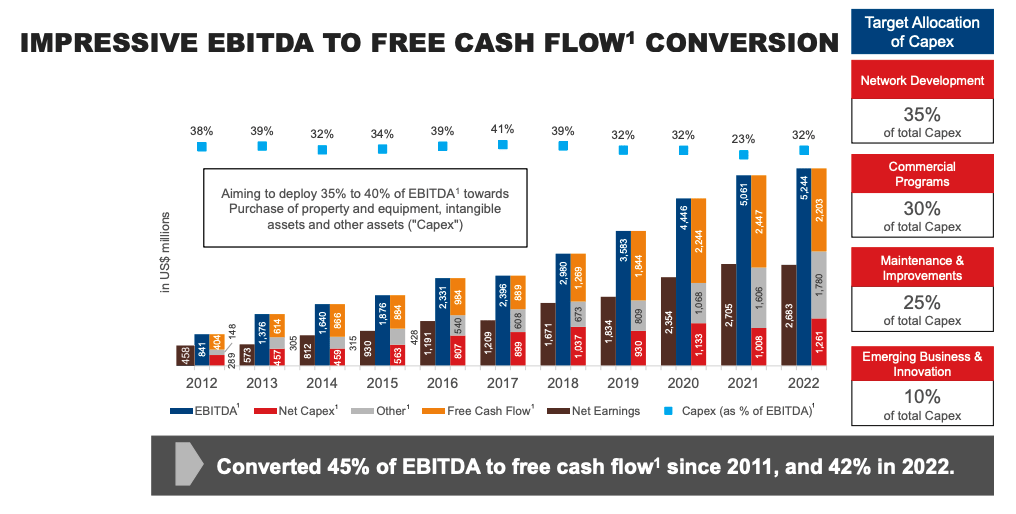

ANCUF has repurchased shares for $205.2 million in the second quarter and $683.2 million in the first half of the fiscal year of 2023. At the end of the quarter, shares were repurchased for $396.2 million. Furthermore, it has increased its quarterly dividend by 27.3% per share. The company has healthy fundamentals. It has shown strong earnings, and this has driven a good leverage ratio of 1.20 and a return of capital employed of 16.4%. The company has been successful in maintaining a healthy level of free cash flow as seen in the graph below.

EBITDA Breakdown per year (Investor Presentation 2022)

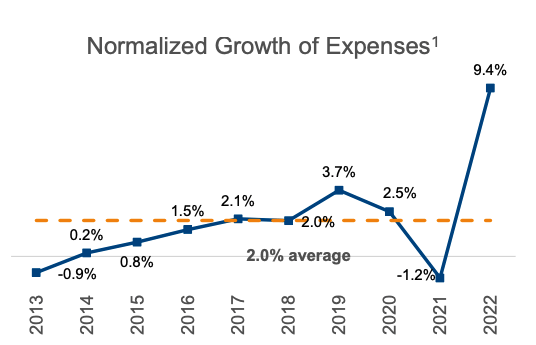

In the last quarter, we saw a spike in expenses due to inflation and wage pressure. However, the company has historically been able to maintain expenses at a 2% average.

Impact of inflation and wage pressure (Investor Presentation)

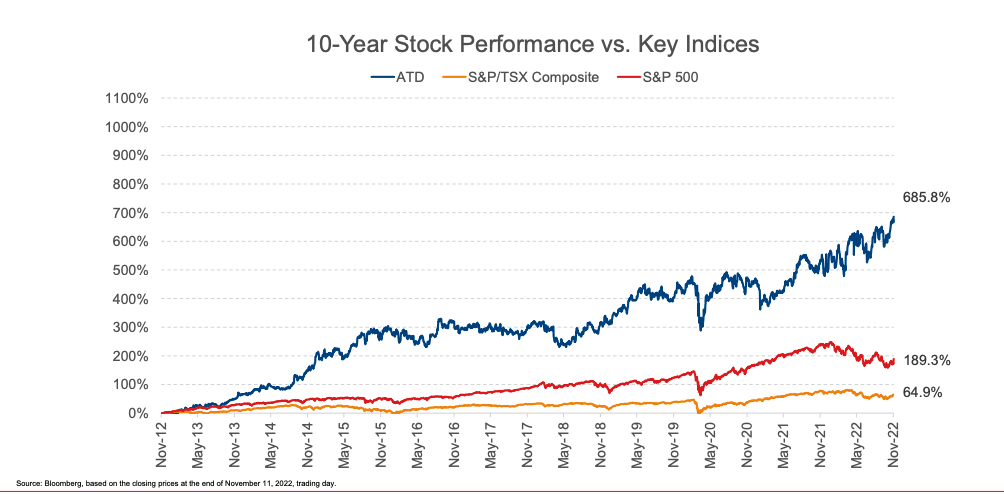

If we look at the stock performance over ten years compared to key indices, the number and trend for this consistently solid stock speak for themselves. It has rewarded shareholders 685.8% in returns over ten years, well above S&P 500 and TSX Composite.

Stock Performance versus Indices (Investor Presentation 2022)

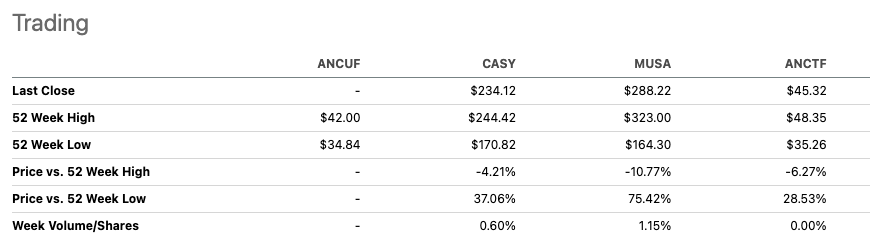

I have compared ANCTF (or ANCUF) to two of the top convenience store peers, Casey’s General Store Inc. (CASY) and Murphy USA Inc. (MUSA), both of which are priced much higher. However, ANCUF has a much larger market cap of $46.20 billion.

Peer Trading (SeekingAlpha.com)

ANCUF has mixed analyst reviews. Wall Street has a Buy rating for the stock. The company had earnings per share of $1.28 earnings per share, which was higher than expectations by $0.01. It has a price-to-earnings ratio of 16.21, under the Seeking Alpha sector value of 21.68, which could indicate that the company is currently undervalued.

Risks

The market continues to head towards a recession, which could impact the consumption of convenience store goods, typically for immediate consumption and short-term pleasures. Furthermore, geo-economic factors such as the Ukraine-Russia conflict continue to impact pricing fluctuations. Inflation is increasing upward, impacting the company’s expenses this most recent quarter. Inflation is directly moving consumer purchasing power and willingness to purchase discretionary goods like those provided in ANCUF convenience stores. Despite this, we have seen ANCUF maintain its margins.

Final Thoughts

ANCUF is a 14000 store strong company with a strong history of performing irrespective of market conditions. The company has ambitious goals to double its adjusted EBITDA through ongoing organic growth and increasing the value per customer. With ambitious goals and historical performance to prove the company’s ability to deliver results, this company still has a lot more upside potential, and investors may want to take a bullish stance on this undervalued stock.

Be the first to comment