SimonSkafar/E+ via Getty Images

Investment Thesis

The last time I checked Align Technology (NASDAQ:ALGN) was a few years ago when it was already overpriced based on the company’s discounted cashflows, but then it skyrocketed to the moon to over $700 a share. Today I decided to investigate this company once again to see if anything has changed in the last few years and since the share price has retreated quite considerably with the rest of the market, I wanted to see if there is an opportunity here.

In short, no. The company is still overvalued, and based on the management’s forward-looking guidance for the next few quarters and my conservative assumptions on revenue growth, the company’s share price has a long way to drop still before investors should be jumping in. My analysis below will show why this is a strong sell at these levels.

Revenue Declines

The company’s revenues rely on two segments, their biggest revenue segment Clear Aligner, and Systems and Services, which has seen quite erratic growth patterns in the past. Clear aligners, the more attractive alternative to the metal braces makes up 80% of the company’s revenues has seen a decrease in demand in the latest 10-Q report, showing all the revenue segments decreasing in double digits from last year and it is no wonder the share price tanked 23% on the news of the numbers and weak consumer sentiment.

The management has reiterated long-term growth of 20% to 30%, however, will miss this guidance for the fiscal 2022 year (transcript).

Earnings are around the corner and things are not looking any better. With decreases in revenues in all sectors, I could see the price plummeting further if the guidance by the management takes a cautious and not upbeat tone for the next few years.

What the Future Holds

Another thing that has impacted the company’s revenues is that a lot of its revenue is being generated abroad in currencies other than the US Dollar, which impacts their overall numbers negatively as the dollar increases in value against other currencies due to high inflation in the EU and war on Ukraine. They have a big presence in Russia as they employ a significant number of R&D personnel and sales and marketing teams there. As they employ a lot of people in Russia, they expect operational issues to continue because of conscription into the military, which may reduce their headcount and overall operations. The company could see severe ramifications from other countries in terms of sanctions because a lot of its workforce is still located in Russia. That is a big risk that they are taking. I’m Lithuanian, and the country is quite close to Russia geographically. I see many news articles still talking about the invasion and everyone is still on high alert, so I don’t see tensions subsiding in all of the neighboring countries any time soon.

A lot of uncertainties in the market they operate, which could lead to a further decrease in the top and bottom-line growth. Although the share price is up 12% this year alone, this just tells me that the speculation is back in the markets. We could also see a return of meme speculators as we did back in 2021 which could propel the stock back up quite a bit. It is impossible to predict what can happen to the stock in the short term, however, if we go by fundamental analysis, that the company’s intrinsic value depends on its ability to generate positive cash flow in the future, we can come up with a reasonable share price that we would pay for the company today. With the mentioned comments by the management earlier, we can see that the immediate future may be quite bleak.

Financials

Now let’s have a look at the company’s internals and see what they are doing well and what not so much.

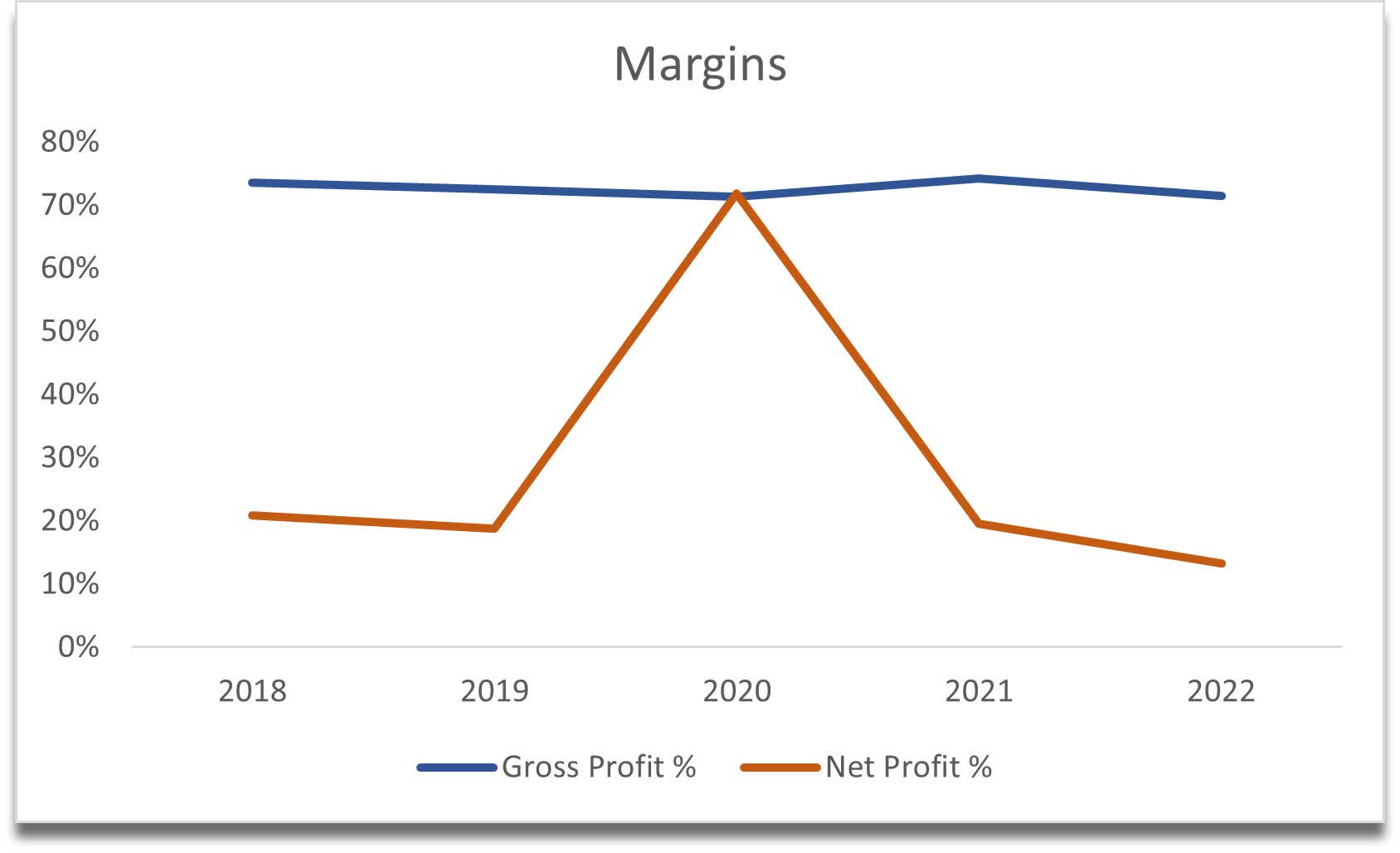

Revenues, income, and margins are all down year-on-year, however, still very healthy gross margins, around 70%, and around 20% net margins, which fell to 13% in 2022. The fall in net margins is a bit worrying, and we will have to wait until the next batch of numbers come out for the full year of 2022 and forward guidance to see if the trend will continue or will reverse and go back to an average of 20% net margins.

An odd net margin of 72% in 2020 can be attributed to a deferred tax benefit due to the transfer of intellectual property to a Swiss subsidiary (2020 10-K).

Margins (Own Calculation)

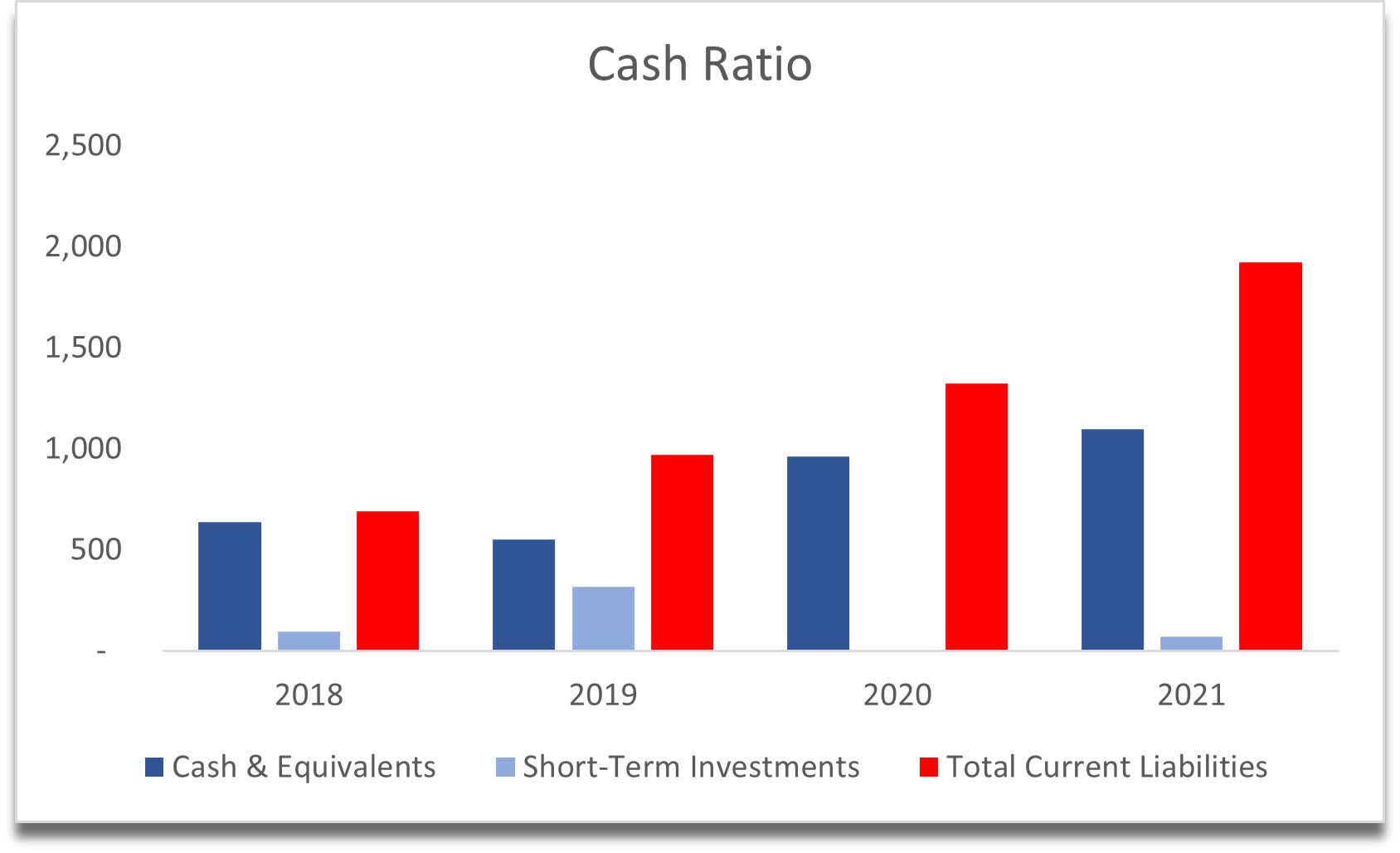

They have some cash and short-term investments; however, the cash ratio is quite poor as it does not cover the company’s current liabilities. If this trend continues, the company might have financial difficulty ahead. The good news is that the company does not have any debt on its books, although as we will see below that is not the only factor that makes a good company.

Cash and Cash Ratio (Own Calculations)

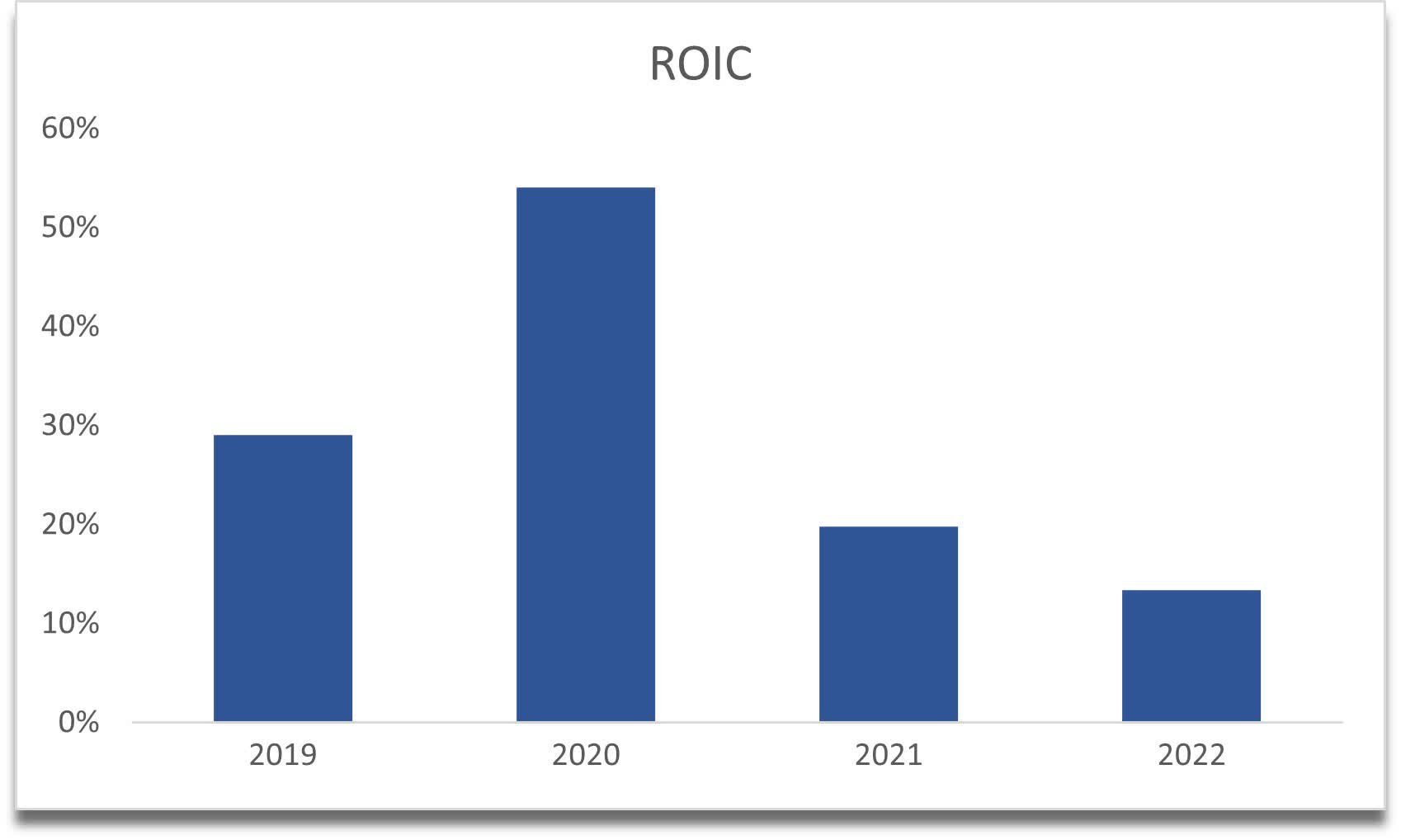

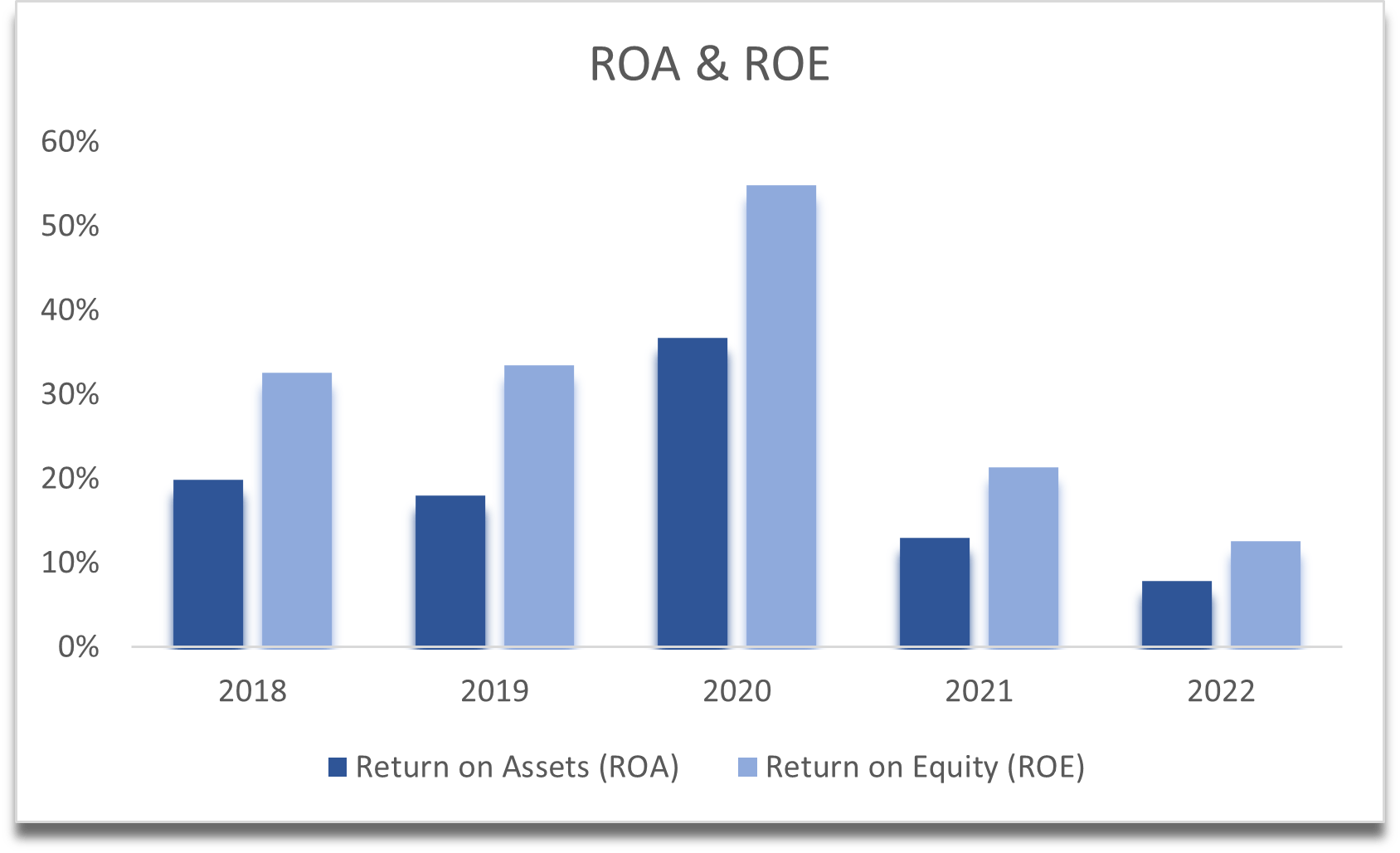

ROIC, ROE, and ROA have all declined considerably in the last couple of years and may stay there for the foreseeable future.

Return on Invested Capital (Own Calculations) ROA and ROE (Own Calculations)

We can see a sharp drop in returns on the above 2 graphs which worries me, as I don’t know where these numbers are going to go next, but what I do know right now is that these numbers will stay depressed for the next while until the uncertainties in Europe subside and demand picks back up. With a recession predicted for 2023, these low numbers can get lower and stay low for quite a while.

They have a high tax rate due to foreign laws and other US state laws – ranging from 27% to 40% of income. This has affected the DCF model considerably, and so I had to play around with different numbers to see what valuation is the most appropriate.

DCF Valuation

Considering all the comments by the management on the short-term hurdles the company will face, I have put in my conservative assumptions on revenue growth by segments, and their erratic effective tax rate, I concluded that the company is still overvalued at the current price, and it still has ways to fall before it becomes a viable investment.

Even with my forgiving tax assumptions in the optimistic case, where I lowered the income tax to 17%, it is still an overvalued company. Based on the three cases (conservative, base, and optimistic), the valuation for the 10-year DCF model is 106.81 which means it is 56% overvalued. For the 5-year model, it is 56.05 which is 76% overvalued, with a margin of safety set at 25%. This requires a good margin of safety due to how volatile the market might get again when the gamblers of meme stocks come back into play. Maybe the margin of safety is still a little low, but I will leave it as is because if I set the margin higher it is just going to give me an even stronger sell position on the company.

The growth estimates I took were based on a re-iteration from the CFO that they see 20%-30% growth in the future. I took the average of that number and went with 25% for the years 2025 to 2027 and then decreased it by 1%. For the years 2023 and 2024, I took an average estimated revenue of analysts.

Opinions of Others

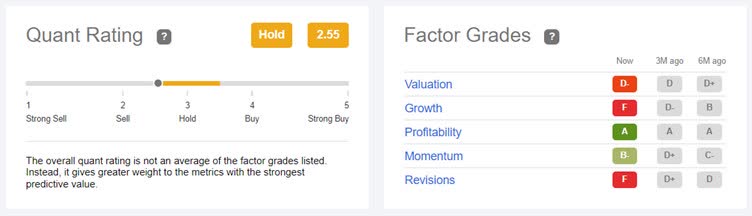

Let’s have a look at what the quant ratings here on SA are telling us about the company and its prospects.

It is not surprising to see a close-to-sell rating here, with most of the Factor Grades only getting worse in the last 6 months.

Quant Ratings (Seeking Alpha)

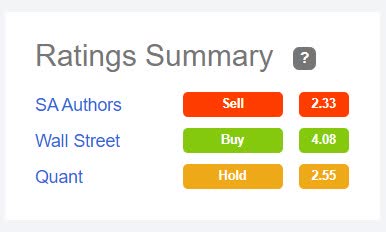

What is surprising to see is Wall St sentiment being a buy right now. They must know something that we don’t (or are being paid to be optimistic as usual).

Sentiments (Seeking Alpha)

I always try to do my calculations of any company before I look at ratings here on SA as I do not want to be influenced by others. I take comfort in seeing that my opinions are quite closely correlated with the opinions of other, more talented, and knowledgeable contributors on the website and I continue to strive to give my best, unbiased opinions on future analyses of companies.

Conclusion

With the uncertainty of high inflation in the EU and Russian military presence in Ukraine, there is more bad than good showing up in the magical crystal ball for the company. The company may face some sanctions from the EU because they are still operating within Russia. That could mean higher taxes and other penalties. With the fiscal 2022 earnings just around the corner, it will be important to pay close attention to the management’s tone about the future growth of the company and how optimistic, or pessimistic they feel about the dentistry market in the immediate future.

With the above metrics, we can see that the company is still overpriced and does have a lot of room to fall, based on my conservative assumptions of revenue and more lenient effective tax rates. In the short-term, price action does not follow the fundamentals of the company at all, so I would expect a lot of volatility in the share price over the next year or two, with unexplainable booms like we have seen in 2021 to come back and distort the value of the company further. In the long-term, however, it all comes down to the company’s ability to generate good cash flow and hopefully great returns to the company’s shareholders. Right now, I cannot say Align Technology is that company.

I will revisit this company once again if something new happens that would change my opinion about the company, whether that is a sharp drop in the share price that would justify its valuation or some groundbreaking innovation in the dentistry space that promises to be the next big revenue machine for the company.

Be the first to comment