Lauren DeCicca

Alibaba Group Holding Limited (NYSE:BABA) has continued its incredible recovery from its October lows. Accordingly, BABA has surged more than 100% from its October bottom, easily surpassing the S&P 500’s (SPY) struggles.

We presented an update in early December, articulating that a progressive easing from its COVID lockdowns is more likely than a “rapid-fire” exit.

However, Beijing has likely taken many observers by surprise, including us. Why? China has reopened its borders and emerged from its COVID lockdowns with such pace, conviction, and confidence that it could be near its peak.

Not just that. China could also avoid the multiple “peaks and troughs” of infection waves, culminating in one giant peak wave that will likely be over after its Chinese New Year holiday.

We think China has timed its rapid exit from its COVID lockdowns remarkably well. Criticism has been leveled against the government for leaving vulnerable rural and senior residents to the risk of COVID infections. However, the Chinese government’s resolve to lift the nation from its economic doldrums is steadfast and unwavering.

As such, economists and strategists have also become more sanguine over China’s 2023 GDP outlook, further revising their forecasts and seeing a faster recovery.

The government is also keen to leverage the domestic economy to lift its recovery, as export growth is expected to remain tepid. Hence, the focus will likely be predicated on the recovery of the property sector, consumption, and industrial activity.

As China’s leading e-commerce and cloud computing leader, Alibaba is well-placed to participate in this recovery, even though the recovery in consumption is likely to be uneven.

Notwithstanding, astute market operators have likely focused on the recovery in H2’23, even though the global economy could continue to weaken. Given Alibaba’s exposure to Chinese consumers, the optimism seen in its price action has likely anticipated the uplift. As such, we believe the normalization in its valuation is justified, which has surpassed our expectations, given the pace of China’s reopening efforts.

However, before investors start to chase the surge in BABA over the past three months, it’s essential to understand that China’s population growth could potentially fall into a structural decline in the medium and long term. Hence, there could be significant implications for China’s manufacturing and consumption engine of growth.

As such, India could be a significant threat to China, with its population growth expected to overtake China. However, we don’t expect India to be an imminent threat as China boasts a massive supply chain that has taken decades to build up. Furthermore, India’s manufacturing share of its economy remains relatively low for now, suggesting China has time to lift its productivity gains, augmented by the quality of its leading AI research and output.

We also believe Beijing has likely pulled back on the tech crackdown on its leading Internet companies. However, investors need to be wary about a structural shift in policy, as Beijing is planning to take up “golden shares,” suggesting the government is keen to maintain its supervision.

As such, the “glory days” of the pre-COVID era are likely over as Beijing attempts to balance growth and equality. Investors need to remember that China’s President Xi Jinping’s common prosperity theme remains alive. As such, while the worst of the tech crackdown days should be well over, it doesn’t necessarily imply a return to previous years of “disorderly expansion.”

Therefore, we believe investors should accord a valuation more appropriate for a slower-growth company over the medium term.

Accordingly, the revised consensus estimates suggest that Alibaba could post revenue growth of 3% in FY23 (year ending March 2023) before recovering further to 12% in FY24.

However, the projections are way below Alibaba’s pre-COVID growth cadence. Back then, BABA posted FY19 growth of 50.6% and FY20 growth of 35.3%.

Hence, we believe it’s prudent and reasonable for investors to apply a generous margin of safety to BABA’s relative valuation, given a potentially slower-growth environment moving ahead.

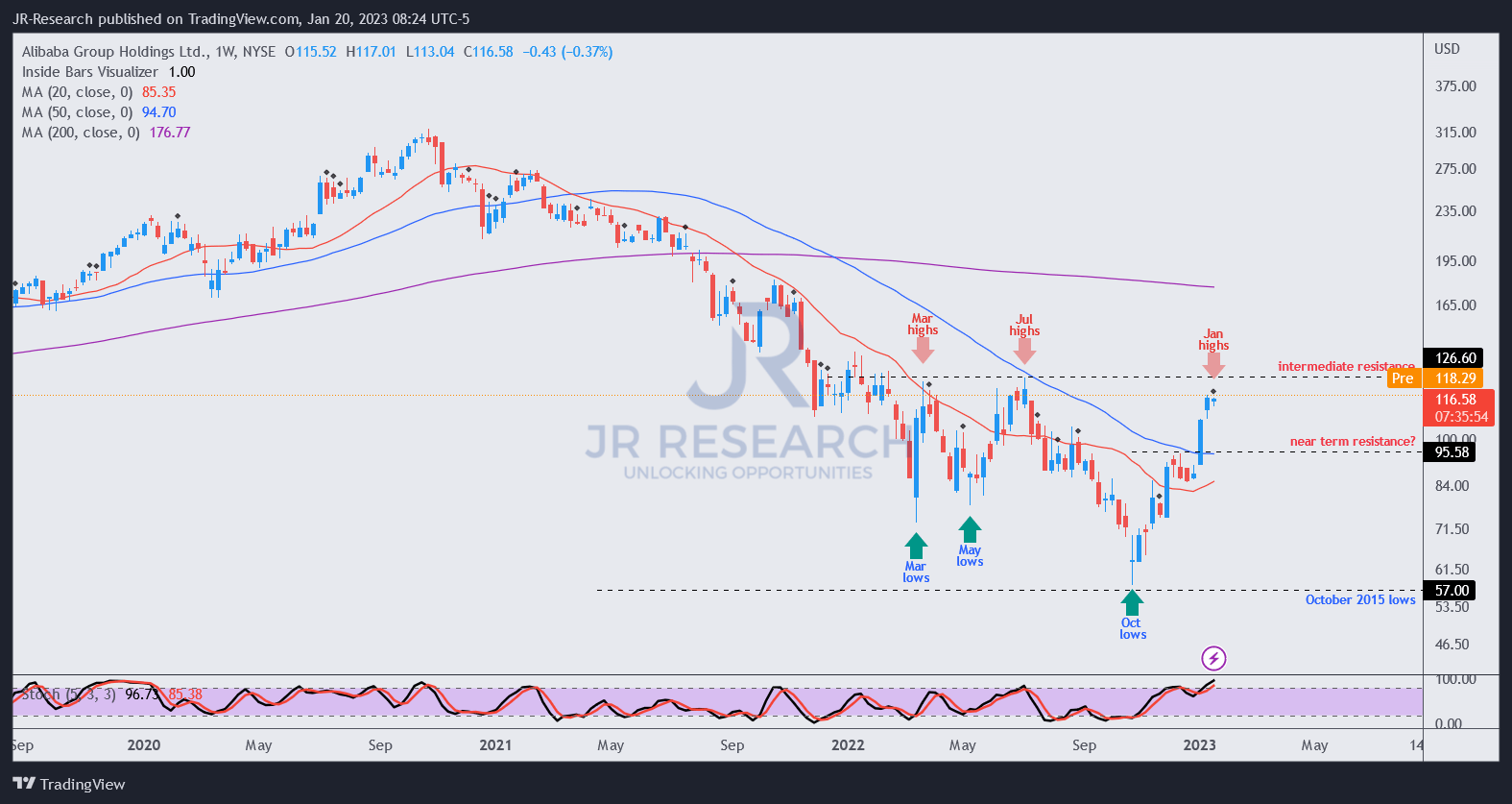

BABA price chart (weekly) (TradingView)

BABA last traded at an NTM EBITDA of 10.3x, in line with its peers’ median of 9.2x, and closer to Amazon (AMZN) stock’s 13.5x.

Coupled with price action reminiscent of a momentum spike, drawing in overly-optimistic buyers rapidly, we believe investors need to be extra cautious about adding more positions now.

Rating: Hold (Reiterated).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment