alexsl/iStock via Getty Images

I have covered Airspan (NYSE:MIMO) two times already, stressing this little-known American company specializing in wireless RAN or radio access network equipment. This time around, the aim is to cover it together with Hewlett Packard Enterprise (NYSE:HPE) and highlight the financial opportunities of a partnership for private 5G services through the use of commoditized hardware and open technologies.

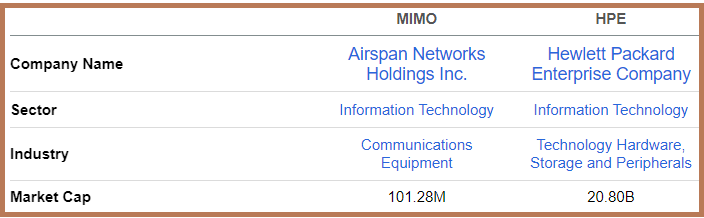

While both come from the IT sector, they are from two completely different industries as pictured below with their market cap also varying considerably.

Comparison of Key Metrics (seekingalpha.com)

Also, with the current uncertainty at the macroeconomic level and supply chain issues that are impacting equipment manufacturers, it is also important to think out of the box and specifically for opportunities revolving around cost savings, in a sector also impacted by geopolitics.

Thus, I start by providing insights as to how 5G deployment has evolved with the removal of China’s Huawei, which also explains the reasons for the emergence of the likes of Airspan, as well as HPE tweaking its product offering to enable rapid deployment of Open RAN.

Opportunities Created Through Opening of the RAN

After Huawei was sidelined by the Trump administration in 2019, only two legacy service providers were left, Ericsson (NASDAQ:ERIC) and Nokia (NOK). As a result, apart from some smaller RAN plays like Samsung (OTCPK: OTCPK:SSNLF) which mainly specializes in radio antennae, the new market configuration was a duopoly in terms of providers which could provide end-to-end solutions.

Thus, costs went higher for 5G radio which can consume up to 60% of capital and operating expenditures for related projects, which also creates barriers to entry for smaller MNOs (mobile network operators) or large corporations setting up private cellular networks. Here, I specifically talk about private 5G in contrast to public ones which are accessible by people like you and me, with the former seeing more development driven by applications like IoT, AR (augmented reality), video surveillance, drones, and remote maintenance.

As a result of these higher costs, there was a move towards opening the RAN with open-RAN whereby the radio access network part was disaggregated so different components, like antennae, base stations, servers, and software, could be sourced from more than one supplier. At this stage, another problem cropped up whereby projects involving many suppliers were taking too long to be completed in contrast to turnkey ones contracted to either Nokia or Ericsson in an end-to-end fashion.

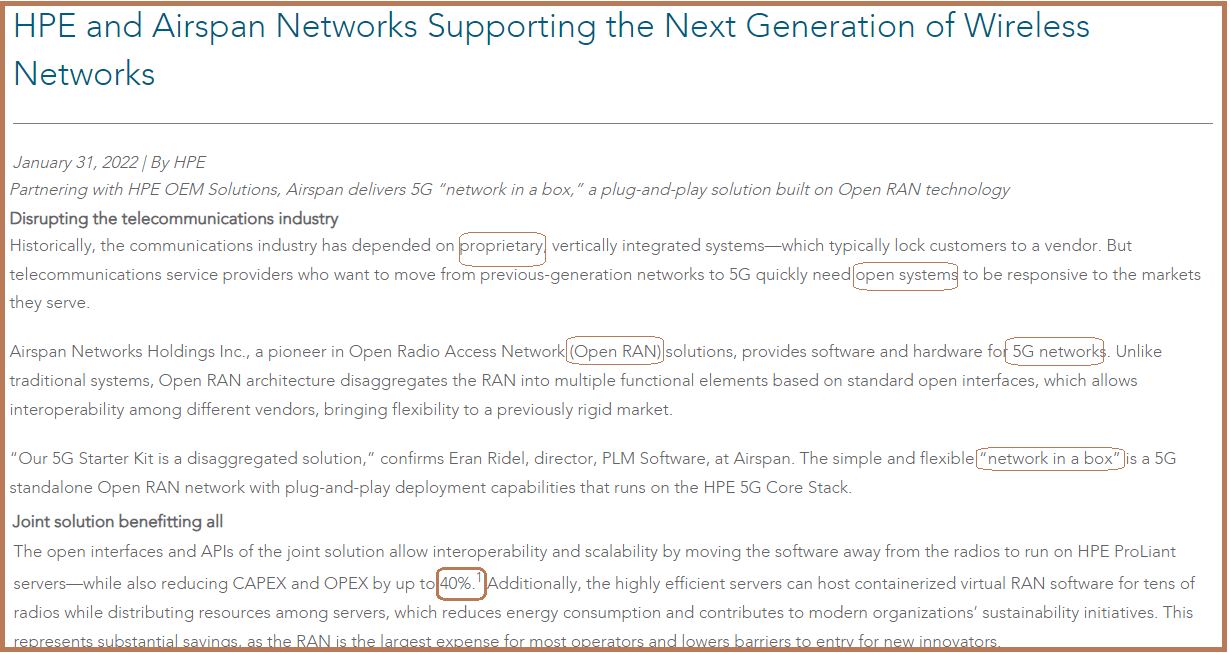

This is where Airspan’s partnership with HPE takes all its importance as it enables the deployment of RAN solutions in a “network-in-a-box” fashion. In this case, instead of having to source the server from HPE and calling Airspan’s team for the software installation, which takes time, the two companies jointly designed a pre-installed packaged product, only necessitating minor customizations during deployment. This permits clients to turn on their private 5G network in days compared to months previously. In more concrete terms, the network-in-a-box enables cost savings of up to 40% as shown below.

Next-generation wireless networks (www.airspan.com)

Thus, by lowering the barrier to entry, by 40%, and reducing implementation complexity, the partnership should benefit from the $7.7 billion of opportunities in the private 5G market forecasted for 2027, after growing at a CAGR of 48% from 2022. This high growth represents a bright spot in the tech sector as overall IT expenditure including cloud is expected to decelerate considerably in 2023, to 2.4%, according to a survey by Gartner.

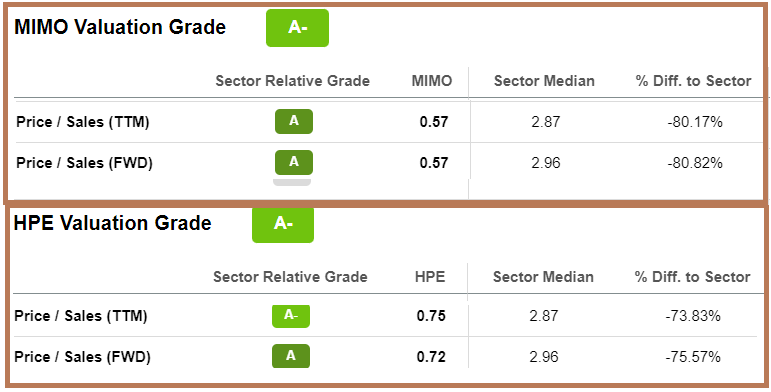

Given the sales opportunities, both companies are considerably undervalued with respect to the sector median as shown in the table below when considering the trailing price-to-sales multiples, or Airspan by 80% and HPE by 74%. Adjusting for just a 20% increase, Airspan and HPE should be trading at $1.7 (1.4×1.2) and $19.7 (16.4×1.2) respectively, based on their current share prices.

Valuation metrics (seekingalpha.com)

Therefore, I am optimistic for both companies in view of the 5G opportunities, but, there are competition and supply chain issues to consider.

The Challenges and Product Differentiation

Now, with only $100 million in market cap, tiny Airspan has to compete with legacy behemoths like Ericsson and Nokia valued at billions of dollars, making it imperative that for the U.S. company to subsist, it should possess a high degree of product differentiation. Thus, while its competitors focus on hosting their wide range-covering radio antennae on top of tall tower masts, Airspan’s small cell units can instead be fitted atop street lamps or utility poles. In this way, it can target a specific region in the overall network for data traffic to be boosted in a process called densification, and at a lower cost compared to traditional providers.

Thus, demand for its products remains strong with the company benefiting from its strongest quarter with over $35 million in bookings from its three largest customers. However, these third-quarter (Q3) results also reveal the challenging supply chain environment with the top line falling below the guidance range. This was due to component supply issues, responsible for a shortfall of $3 million, which should be recouped in the fourth quarter (Q4). As a result, the mid-point of $53 million would represent a $2.6 million year-on-year increase, but less than the $53.6 million consensus revenue estimates. Looking further into the income statement, profitability is being impacted by higher component prices which the company is trying to offset by charging customers higher prices.

However, since supply chain issues are expected to persist into the middle of this year, it is difficult to see a revenue or even an earnings beat when the company earnings next week.

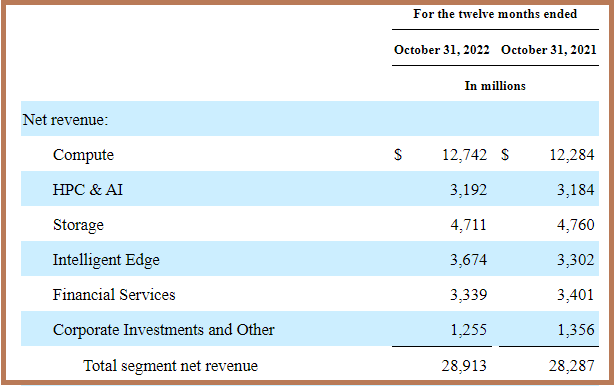

As for HPE, its GreenLake self-service and managed platform enables customers to benefit from the public cloud-like feel on their premise’s IT infrastructure. In this respect, it competes with the hyperscalers but, it also has its own hardware brand which permits it to provide a broad range of services. Furthermore, it is also an end-to-end networking service provider with a combination of private wireless and its Aruba Wi-Fi technology and as pictured below, HPE remains well diversified across the IT space.

Different Revenue segments for HPE (seekingalpha.com)

Equally important, compared to hardware suppliers like Dell (DELL), with GreenLake, HPE has moved a step further towards an infrastructure-as-a-service that enables customers to invest in hardware in a capital-light way. Hence, in Q4-FY2022 which ended in October, which was a record quarter for sales, as-a-service orders represented approximately 12% of the total bookings, after increasing at a rate of 68% during the fiscal year.

Interestingly, as-a-service revenues have helped the company offset some of the supply chain issues it has been facing recently.

Discussion and Cautionary Note

Looking forward, it is HPE that should benefit more from the network-in-a-box product because of the multiplier effect that it should have on GreenLake as-a-service revenues as a larger number of smaller MNOs and large corporations opt for a capital-light strategy to implement private fifth-generation wireless. Thus, I have a bullish position on the stock, but, with the Federal Reserve likely to keep rates at an elevated level in 2023, expect volatility to continue.

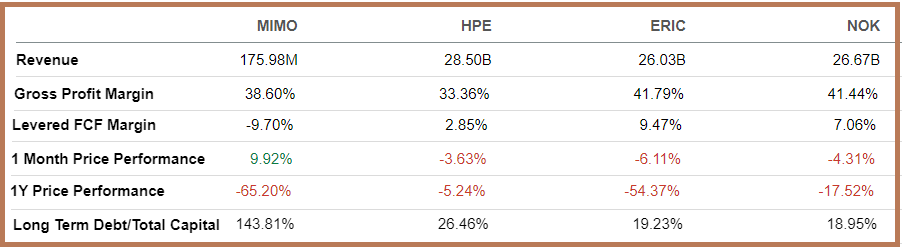

Along the same lines, Airspan’s stock as evidenced by its one-year downside of -65% (table below) exhibits a higher degree of volatility. However, its one-month upside of nearly 10% while peers (including Ericsson and Nokia) have all suffered from negative price performance suggests that some investors seem to trust the stock despite its negative free cash flow status and high debt level.

Comparison between Airspan, HPE, Ericsson and, Nokia (seekingalpha.com)

Well, it is true that the company has taken steps to reduce Opex, resulting in about $4 million of reduction in cost savings plus more planned in 2022. Additionally, it is accelerating payments for its $42.2 million by the end of Q3 of customer receivables or amounts due for service already delivered. This should bolster its cash position of $27.3 million and enable the company to continue meeting operational obligations.

Furthermore, as I already elaborated in my previous thesis, another factor that should help is the gross profit margin of 38.6% despite its revenue base being much lower than peers, all because it has been able to introduce a higher dose of software in its product offerings as part of the Open RAN strategy.

This is the reason Airspan is a stock to watch out for, but beware that the company is facing the possibility of its warrants, which are each exercisable for one share of Airspan’s common stock being delisted due to their low trading price. This can create volatility in the stock depending on the way investors digest the news. Therefore, it would be better to get some clarification during the Q4 earnings call before buying the stock.

Conclusion

This thesis has shown how Airspan and HPE have taken advantage of the high costs and complexities involved in implementing private 5G to come up with a simple product that can be rapidly deployed. Thus, I have valued the two companies accordingly.

Finally, in addition to opportunities, I have also listed the challenges including stock volatility risks, which are higher for Airspan.

Be the first to comment