melis82/iStock via Getty Images

Investment Thesis

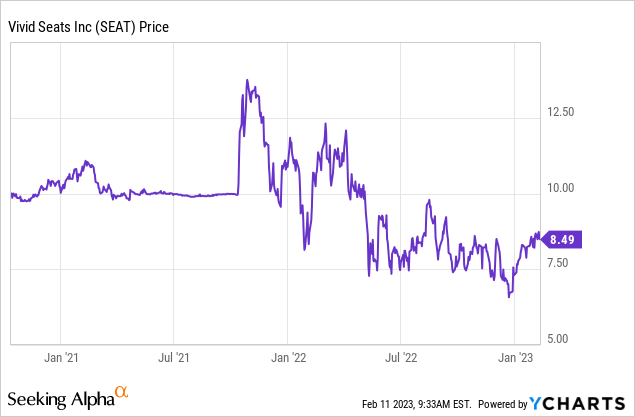

Vivid Seats (NASDAQ:SEAT) went public through a SPAC deal with Horizon Acquisition Corp in 2021. The company has been performing badly since and is now down nearly 40% from its all-time high due to macro headwinds. Unlike the share price, the company’s fundamentals are actually solid. It has a huge TAM (total addressable market) and the industry is benefiting from the reopening tailwind. On the financial side, the latest earnings result reported decent operating income growth as the company demonstrated strong operating leverage. However, after the recent 30% run-up, the current valuation seems a bit stretched. I do not see much further upside therefore I rate the company as a hold.

Why Vivid Seats?

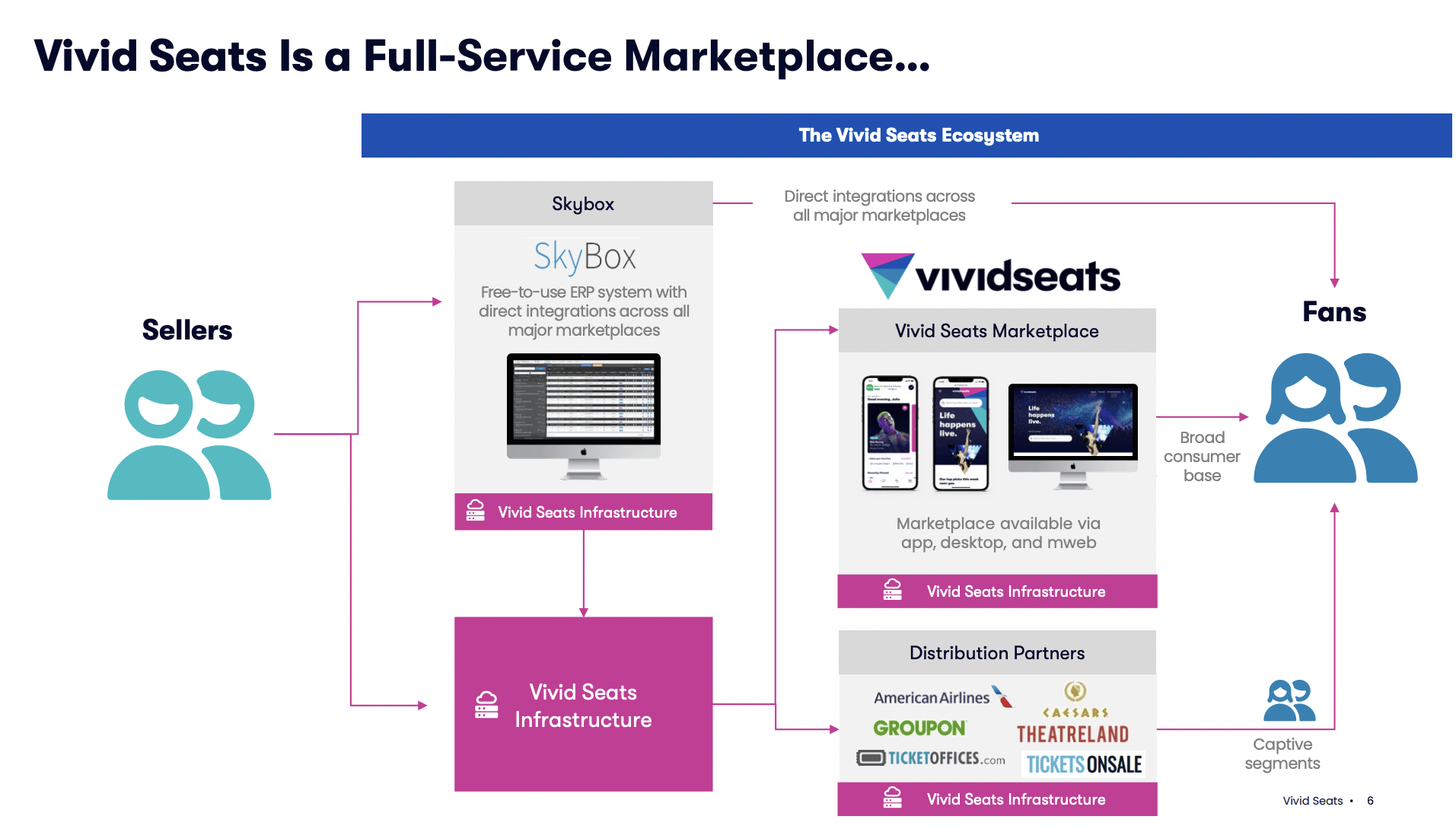

Vivid Seats is a US-based digital ticketing marketplace. The platform allows consumers and resellers to easily buy and sell tickets for sports, concerts, musicals, etc. It provides buyers with loyalty reward programs and personalized discovery feeds for a better user experience and engagement. While sellers will have access to its Skybox platform which provides inventory management, pricing, fulfillment, reporting, and other features. The company has over 12 million customers with over 100 million tickets sold.

The online ticketing market is huge, although growing at a moderate rate. According to Grand View Research, the TAM is estimated to grow from $54.26 billion in 2019 to $67.99 billion in 2025, representing a CAGR (compounded growth rate) of 4.3%. Most of the expansion is driven by the increasing adoption of mobile apps, which is able to offer a much more convenient purchasing process. The market is also benefiting from the re-open tailwinds. Performers stopped their shows from 2020 to 2021 due to lockdowns and they are now hosting more shows than ever. Many consumers also saved up a lot of money for their desired shows and are now spending more than before. These tailwinds are continuing to benefit the company.

Stanley Chia, CEO, on concert trends:

As we look to 2023, we are seeing positive indications of a robust concert calendar. Artists often announce their tours for the following year, during the fourth quarter. In the third and fourth quarters to date, we’ve already had exciting tour announcements from top artists, including Taylor Swift, George, Ed Sheeran, and Blink 182.

Vivid Seats

Financials

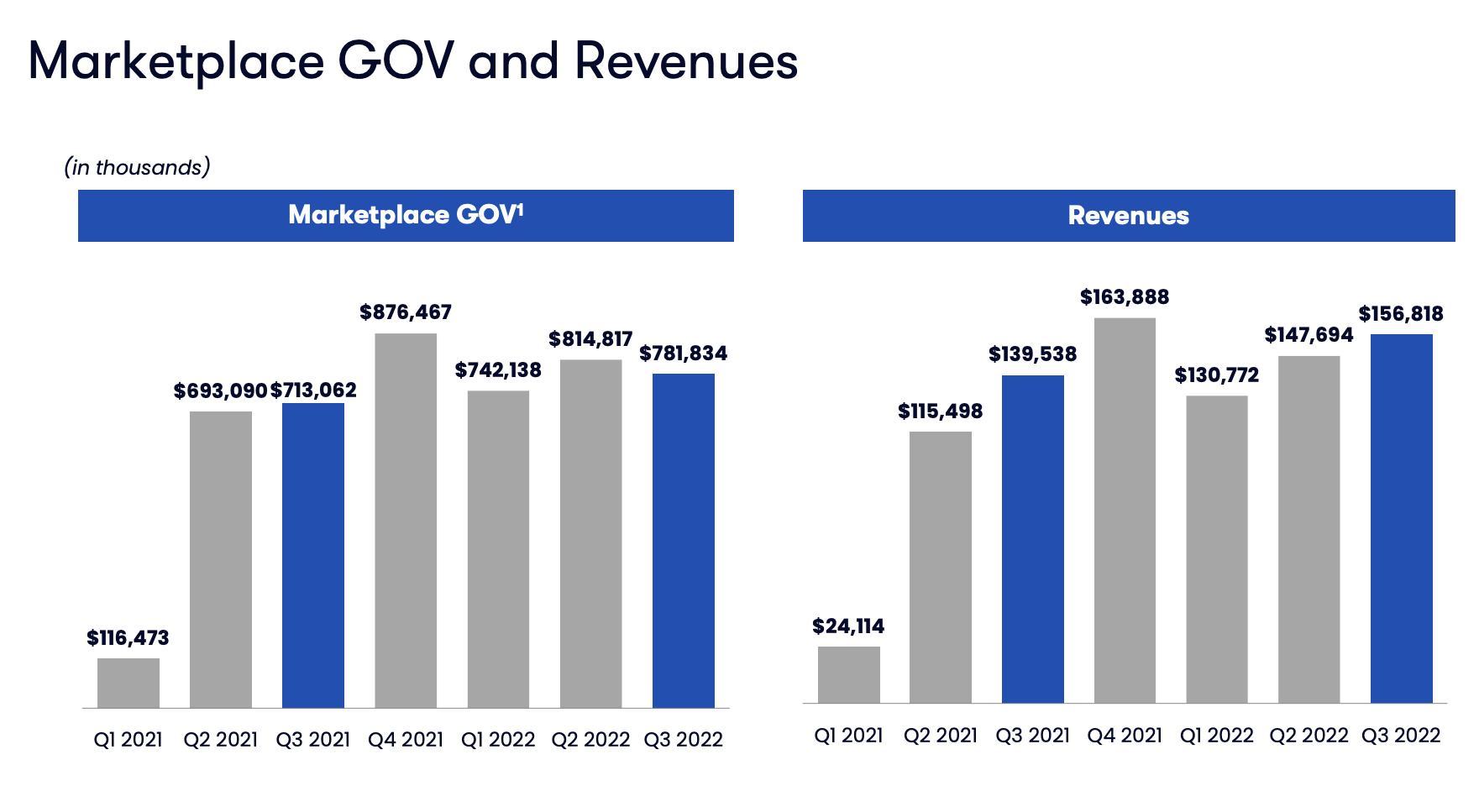

Vivid Seats’ latest earnings were solid all things considered, especially the bottom line as it turned profitable. The company reported revenue of $156.8 million, up 12% YoY (year over year) compared to $139.5 million. Total marketplace GOV (gross order value) increased 10% YoY from $713.1 million to $781.8 million. The growth is mostly driven by an increase in total marketplace orders, which was up 9% YoY from 2.35 million to 2.57 million. The demand for live events continues to be strong. The average order size was $304 while the take rate was 16.7%, in line with previous levels.

Lawrence Fey, CFO, on Q3 results:

Demand for live events remained healthy and resilient in the third quarter, and Vivid Seats converted industry strength to strong results while remaining highly profitable.

The most notable highlight of the quarter was definitely the bottom line. The management team did a great job of controlling expenses and demonstrated strong operating leverage. Despite revenue increasing by 10%, operating expenses were only up 4.3% YoY from $93.5 million to $97.5 million. The increase in S&M (sales and marketing) spending was mostly offset by the decrease in G&A (general and administrative) spending. This resulted in operating income increasing 40% YoY from $15.5 million to $21.7 million. The operating margin also expanded 210 basis points from 11.1% to 13.8%. Net income for the quarter was $18.7 million compared to a net loss of $(1.8) million. The company’s balance sheet remains very healthy with $273.9 million in cash and $283.55 million in debt.

Vivid Seats

Investors Takeaway

I don’t think now is the time to buy Vivid Seats yet. The company has a large and expanding addressable market that is benefiting from the reopening trend. This should be a solid tailwind but the valuation seems a bit elevated after the recent rally. It is currently trading at an fwd PE ratio of 25.3x which is not cheap by any means. The current low double-digit growth rate is decent but still not enough to support the valuation in my opinion. Due to tougher comps, the growth next year should slow down which may cause a downward revision in multiples. The recession is also a notable risk as the economy is starting to slow down. This will impact the company significantly as concerts and event spending are highly discretionary. I don’t think the current price levels offer much upside potential therefore I rate the company as a hold.

Be the first to comment