Alex Wong

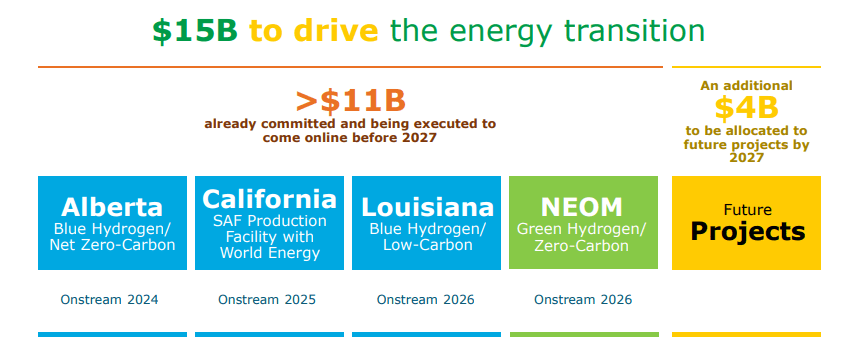

After Air Liquide S.A. (OTCPK:AIQUF, OTCPK:AIQUY), the American competitor Air Products and Chemicals (NYSE:APD) reported its three-month accounts. As usual, APD seems more inclined to share new project developments and as we mentioned last time, Air Products is currently building:

- the largest blue hydrogen project located in Alberta (Canada),

- the largest blue ammonia project ubicated in Louisiana (USA);

- the largest and the world’s most advanced Sustainable Aviation Fuel facility located in California (USA);

- the largest green hydrogen project called NEOM located in the Saudi Arabia peninsula.

On top of that, the company is now allocating more than $4 billion more to additional CAPEX investments maintaining unchanged its shareholder’s remunerations policy and its credit ratings (A/A2). According to the latest rumors, future projects include a green hydrogen facility in Oman (very similar to NEOM) and there is some indication to build a facility also in the European continent (mainly in the Netherlands but also in the UK). During the quarter, Air Products and Chemicals also announced a supply agreement with “the Indian Oil Corporation Limited to build, own and operate a new industrial gases complex supplying hydrogen, nitrogen and steam to IOCL’s Barauni Refinery in Bihar (India) in 2024″.

Last time, in our buy case recap, we explicitly said that Air Products and Chemicals has additional room to build new projects while increasing shareholder returns.

Air Products and Chemicals additional CAPEX

Source: Air Products and Chemicals Q3 results

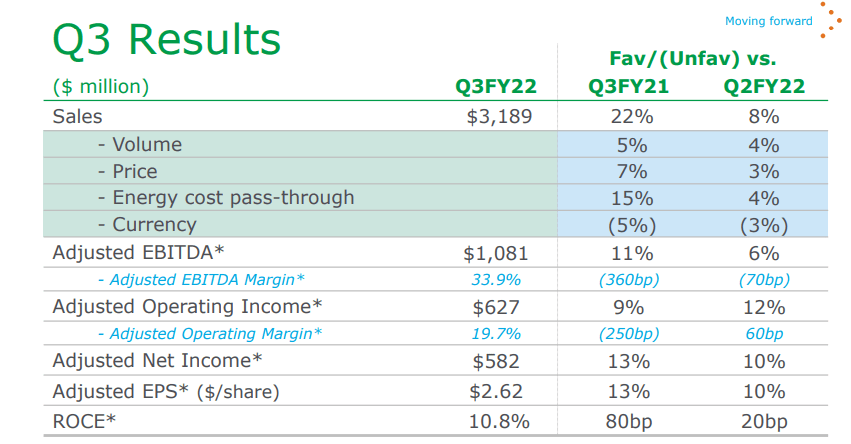

Q3 results

All in all and in abs value, EBITDA grew by 11% compared to last year’s quarter and was supported by a plus 5% in volume.

Air Products and Chemicals Q3 results

Source: Air Products and Chemicals Q3 results

However, looking at the margin, the company was still impacted by the ongoing gas price environment. Checking at the geographical performance:

- America’s EBITDA was above Wall Street analysts’ expectations. This was due to volume recovery in hydrogen;

- Asia’s EBITDA was below estimates. Top-line sales were in line with last year’s numbers, however, an unfavorable FX led to a margin decrease.

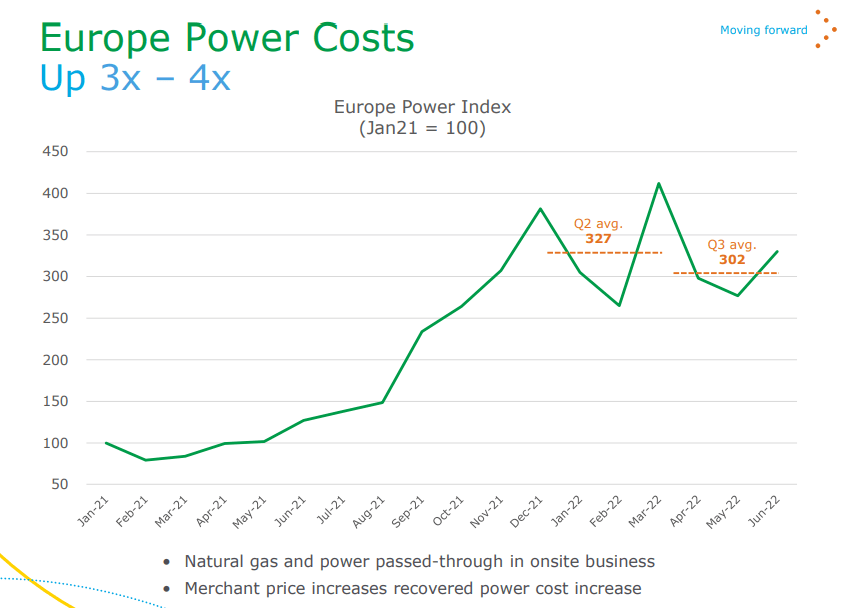

- The EMEA was the region most impacted. Volume was down by 3% and the currency effect impacted the EBITDA’s margin by more than 15%. The European gas environment is hard to forecast (two follow-up notes on natural gas Engie and Uniper). In the quarter, as we can see in the presentation, merchant gas prices in Europe rose by 25%.

Gas price in the EU

Source: Air Products and Chemicals Q3 results

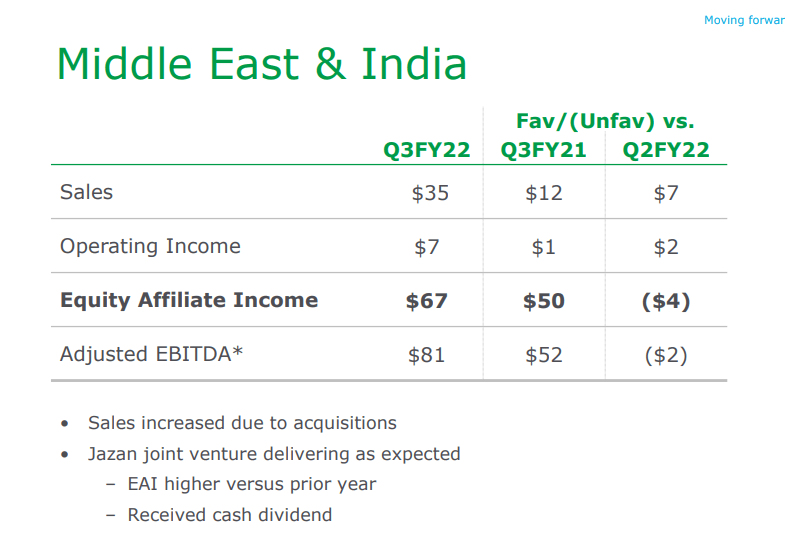

Important to mention is the positive contribution of Jazan, which contributed more than $17 million from the same period one year ago.

Jazan equity investment

Source: Air Products and Chemicals Q3 results

Conclusion and Valuation

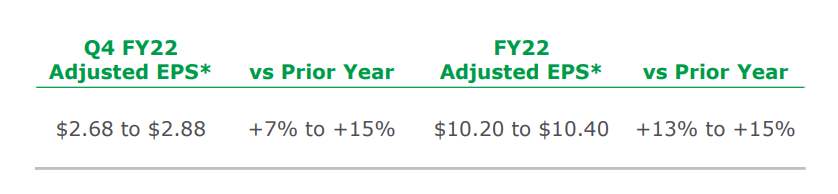

Aside from our six points in our buy case recap, Air Products and Chemicals is one of the most sustainable companies across the globe. They just announced to reduce scope 3 emissions by one-third before 2030. Sustainability presentation here at this link. Last time, we derived a valuation of $300 per share using an NTM multiple of ~24.3x based on an earnings per share of $12.35 in 2024. Based on the latest numbers provided by the management, we left our rating unchanged.

Air Products and Chemicals guidance

Source: Air Products and Chemicals Q3 results

Be the first to comment