Andrii Yalanskyi/iStock via Getty Images

There aren’t many investments out there that I have been adding to in the last couple of months. I have been adding to my investments in the cannabis sector because they seem like wildly mispriced assets. More specifically, I have been adding to income producing REITs in the sector, like Innovative Industrial Properties (IIPR), NewLake Capital Partners (OTCQX:NLCP), and Advanced Flower Capital Gamma (NASDAQ:AFCG). I have been adding to my investments in the REITs that focus on the sector, because they produce significant current income with the potential for continued dividend growth. Today’s article will focus on AFCG, a cannabis lender with a juicy 12.9% yield.

Investment Thesis

AFCG is an mREIT that lends directly to cannabis companies. Due to the lack of investment and capital in the space, they generate significantly higher interest rates on their loans. They continue to add loans to their portfolio and have been very picky with their new investments. Book value increased in Q1 along with the dividend, and I think we will see both continue to grow with the loan portfolio. The dividend yield is now 12.9%, and that doesn’t take into account any potential dividend increases from here. Shares now trade at 8x earnings

An Update On The Business

After the most recent loan to Bloom, the cash interest rate for the portfolio is 11.4%. When you include fees and other consideration, the yield to maturity on the portfolio is 18%. 8 of their 13 loans are fixed rate, while the other 5 are floating. I think they will continue to grow the loan portfolio as fast as they can without taking on too much risk, but I did notice a couple of things from the most recent earnings call that are worth noting.

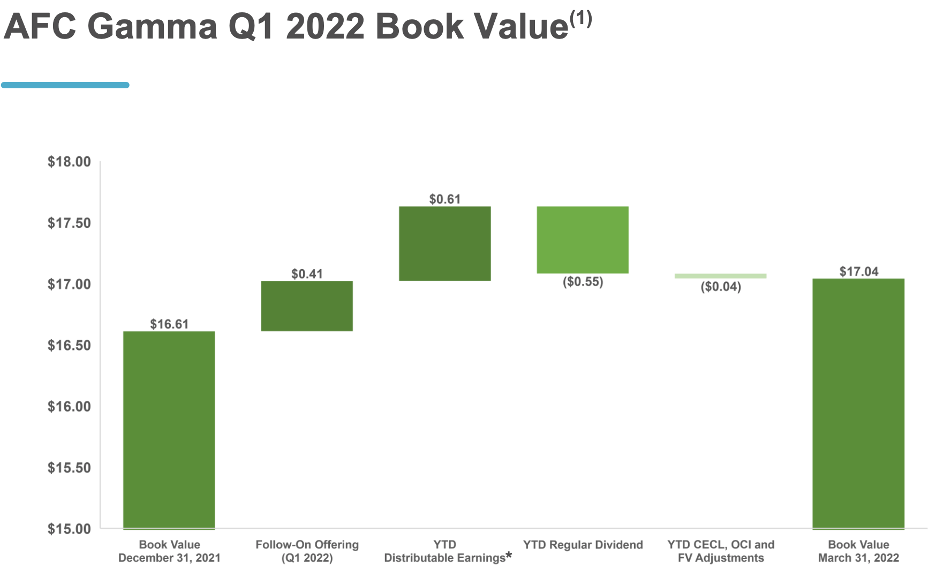

Book Value (afcgamma.com)

They increased the book value of their shares to just over $17 in Q1 by issuing shares over book value. I’m not the biggest fan of the continued equity issuances, but I can understand why they do it to fuel loan portfolio growth. One of the things that stood out was that the CEO explicitly stated that they wouldn’t issue stock below book value. The other piece that stood out when I was skimming the earnings call was that they have no exposure to unlimited license states like Washington, Oregon, California, and Oklahoma.

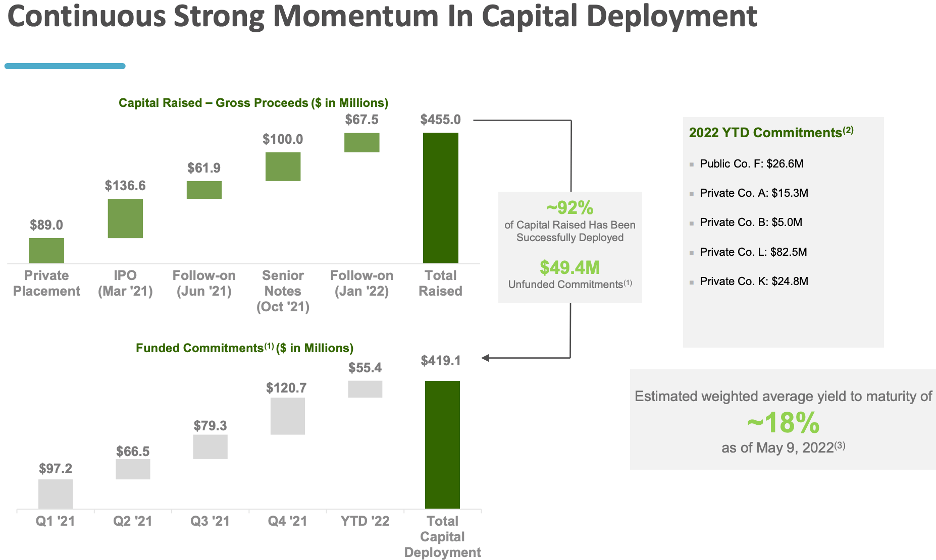

Loan Portfolio Growth (afcgamma.com)

If you look at the portfolio since the IPO, it shows consistent growth that looks poised to continue in 2022. As long as your base case assumption for the cannabis industry and related regulation are gridlocked at the federal level, AFCG will continue to grow the portfolio with new investments at double-digit interest rates. I think shares are still very attractive as they are trading right around book value and seem very cheap on an earnings basis.

Valuation

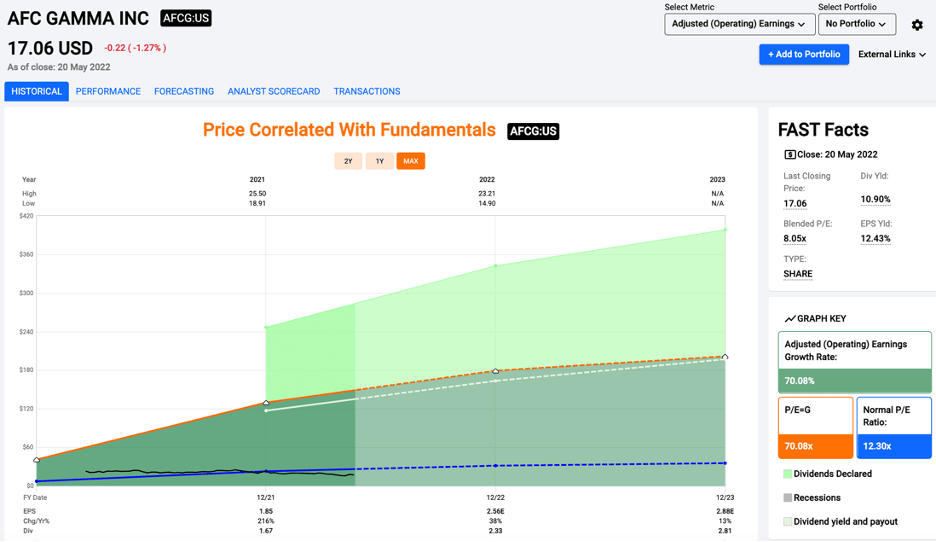

Shares have had a rough start to 2022 and are down approximately 25% YTD. I think that’s mostly due to the broader market weakness, but I have been adding to my position on the way down. Shares currently trade for 8x earnings, which I think is cheap given the growth potential for the company and its loan portfolio, along with the potential for continued growth of book value and the dividend.

Price/Earnings (fastgraphs.com)

Some investors see a 12.9% dividend and just assume that it’s a yield trap. However, all it takes is a quick peek at the dividend history to see that the dividend has grown rapidly and will likely continue to grow as the loan portfolio increases in size.

The Dividend

There aren’t many stocks that have double-digit yields, and investors have typically avoided high yield picks with good reason. Unless you can find the exception to the rule, high yields typically see dividend cuts in bad times. With AFCG’s underlying fundamentals, I think it is the exception worth buying. If the dividend stays at $0.55 a quarter, that works out to a 12.9% yield at the current price. If the dividend grows from here (like it has every quarter since going public), you can get an even higher yield.

Conclusion

If you are an investor looking for investments that are out of favor or off the beaten path, the cannabis industry is a good place to start. It’s a young industry that has a lot of growth potential, but that has also come with growing pains over the last couple of years. One of the more interesting sectors I have found is the REIT sector focused on the cannabis industry. They are providing capital and real estate to a sector that is rapidly growing but has been starved for capital due to federal regulations.

The first one I bought was Innovative Industrial Properties, and I have been buying NewLake Capital Partners and AFCG over the last six months. I think all three REITs will continue to have impressive dividend growth and attractive forward returns, and the selloff to start 2022 means I have been adding to all three this year. AFCG has taken a different approach to providing capital to the sector from IIPR and NLCP. Some avoid mREITs as a sector, but investors can get paid a juicy 12.9% dividend while AFCG continues to grow its loan portfolio, book value, and dividend. I think the risk/reward is skewed to the upside, and I will be looking to add to my position in the coming months.

Be the first to comment