bennymarty

Introduction

I’m sorry I wrote you such a long letter. I didn’t have time to write you a short one.

Blaise Pascal – 17th Century French mathematician

This (often misattributed) quote says something about this article. In our marketplace Best Anchor Stocks, we have 5 elaborate articles in which we explain everything there is to know about Adobe Inc. (NASDAQ:ADBE), but this article is a distillation of everything there. We do this for all our holdings for our subscribers.

The idea is that if you that are not familiar (enough) with a company, you can get a 360º vision without spending too much time on it. After this article, you should be able to decide if you want to dig deeper into the company or simply ignore it. We did the same earlier with Constellation Software Inc. (OTCPK:CNSWF).

With that, let’s start with some basic info about the company.

Basic info about the company

Made by Best Anchor Stocks

Company Overview

-

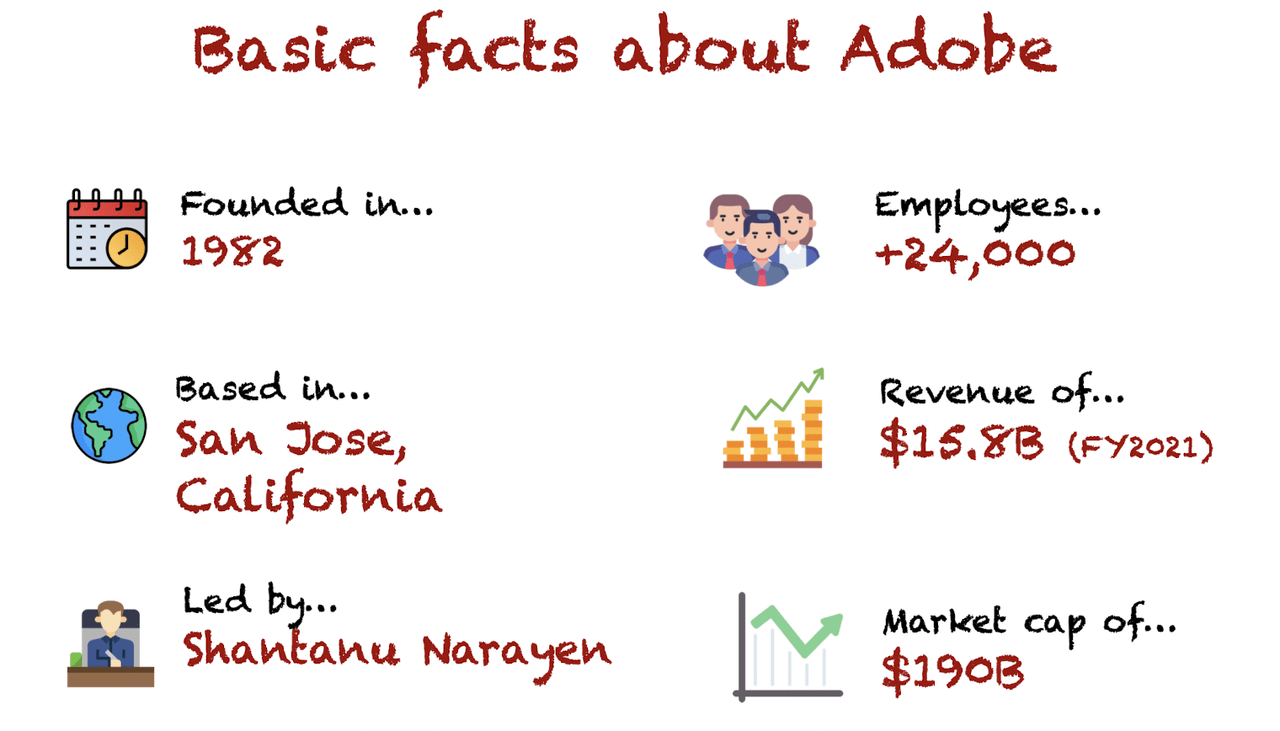

Adobe is a highly-diversified software company founded in 1982 by Charles Geschke and John Warnock. The name comes from Adobe Creek, the river behind the garage where the company was founded.

-

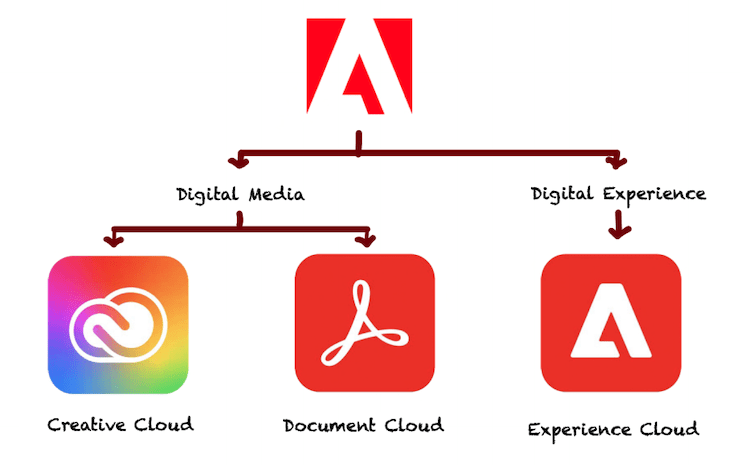

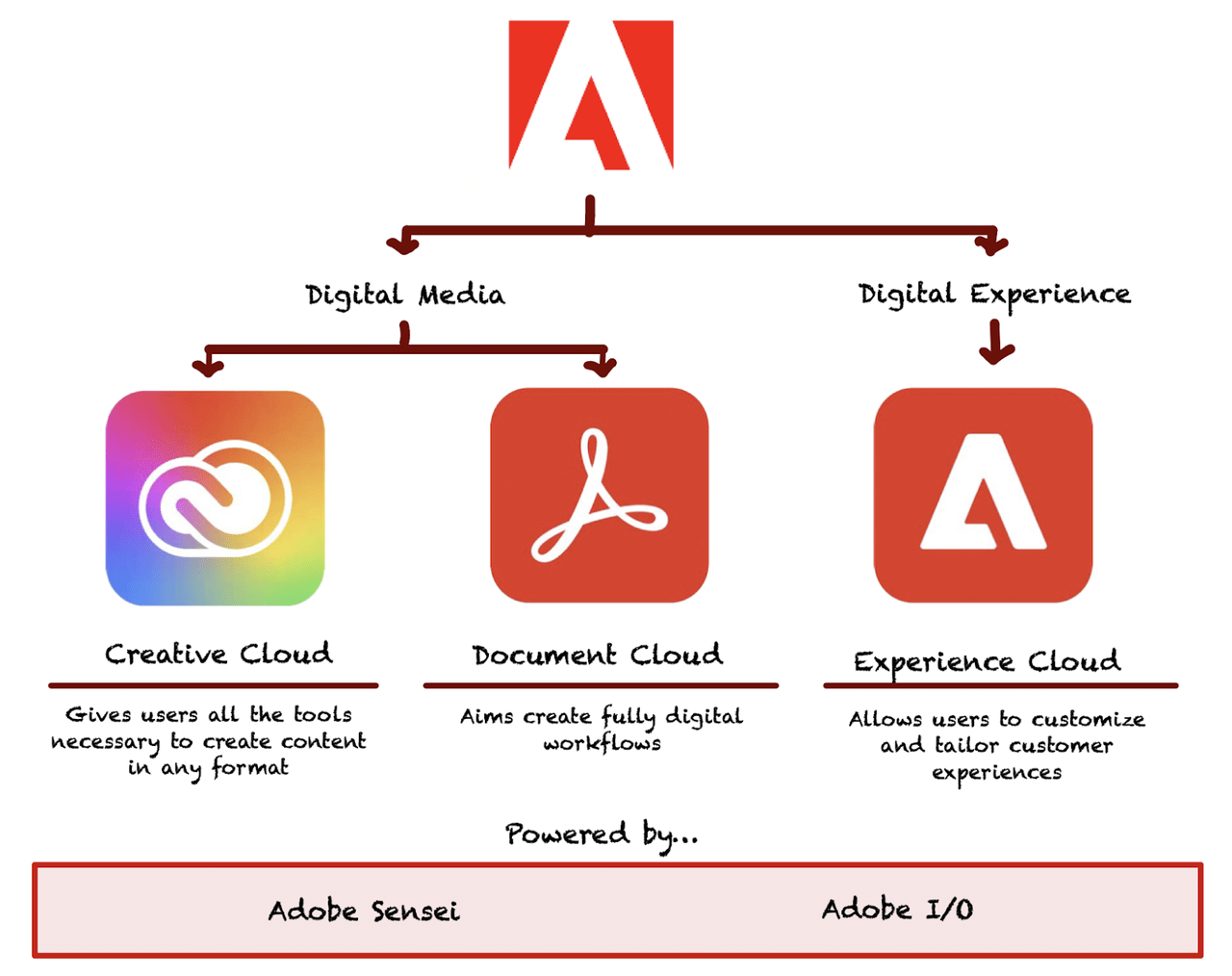

Adobe has two main operating segments (Digital Media and Digital Experience), further divided into three clouds (Creative, Document, and Experience Cloud). One company, two segments, three clouds.

Made by Best Anchor Stocks

-

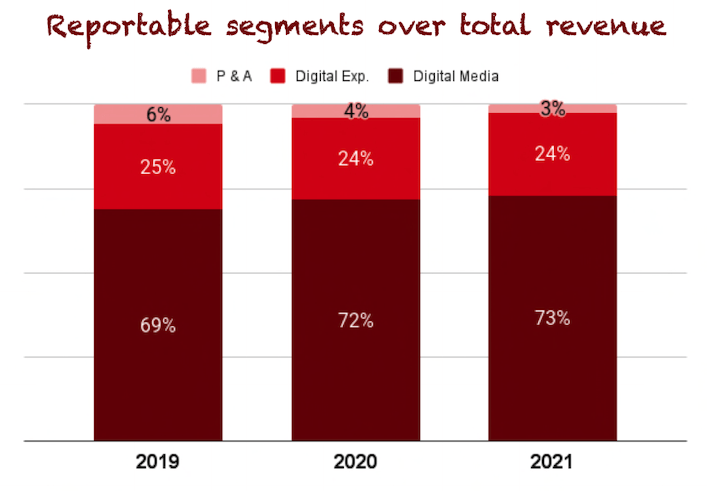

Most of its revenue (+70%) comes from Digital Media, the more mature segment. The sales distribution across Digital Media and Digital Experience has remained fairly stable in the last couple of years.

Made by Best Anchor Stocks Adobe

-

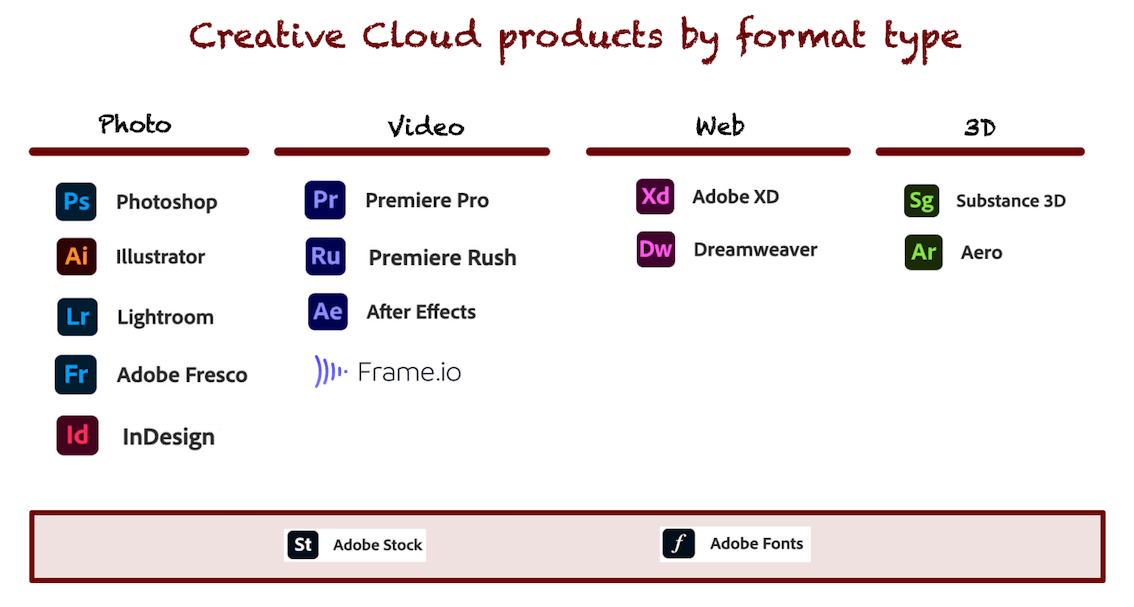

Adobe Creative Cloud provides users with various products and services to create, publish and promote content. Flagship products such as Photoshop and Illustrator have become core components of the creative community and have achieved “verb” status.

-

The objective of the Creative Cloud is to offer a one-stop-shop where individuals, teams, and enterprises go to get all their content creation needs sorted out.

-

The company currently offers more than 30 products that can be purchased individually or bundled in some cases. These products cover almost every content creation format and are supported by two content libraries.

Made by Best Anchor Stocks

-

Adobe enjoys a dominant position in the creative space thanks to this product breadth and its market penetration.

Adobe

-

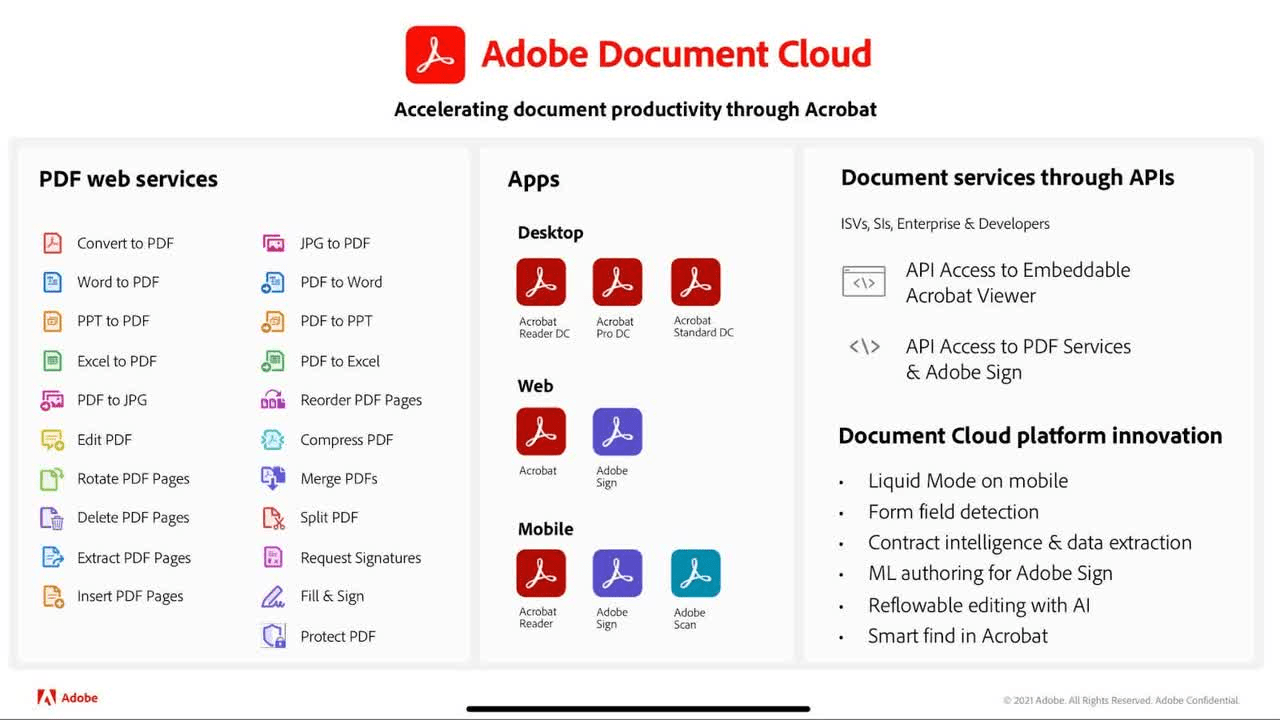

Adobe invented the PDF in 1993 and has been focused on providing customers with a comprehensive suite of products around it since then.

-

The Document Cloud aims to help customers accelerate their productivity by redesigning how they view, share and engage with documents.

Adobe Analyst Day Presentation

-

The Document Cloud benefits from its large user base as Acrobat is installed on over 2.5 billion mobile and desktop devices.

Adobe

-

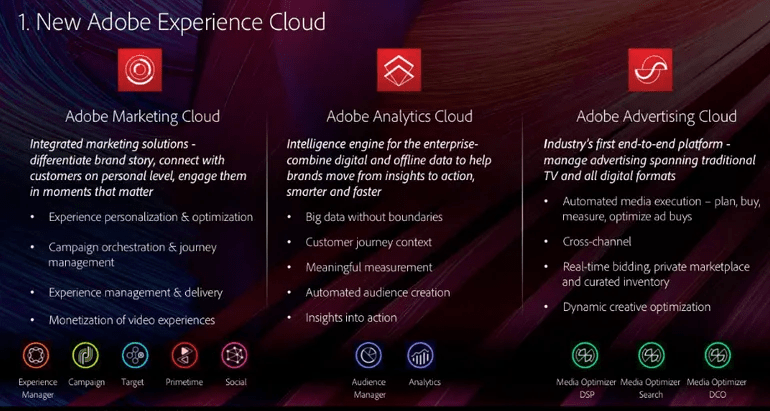

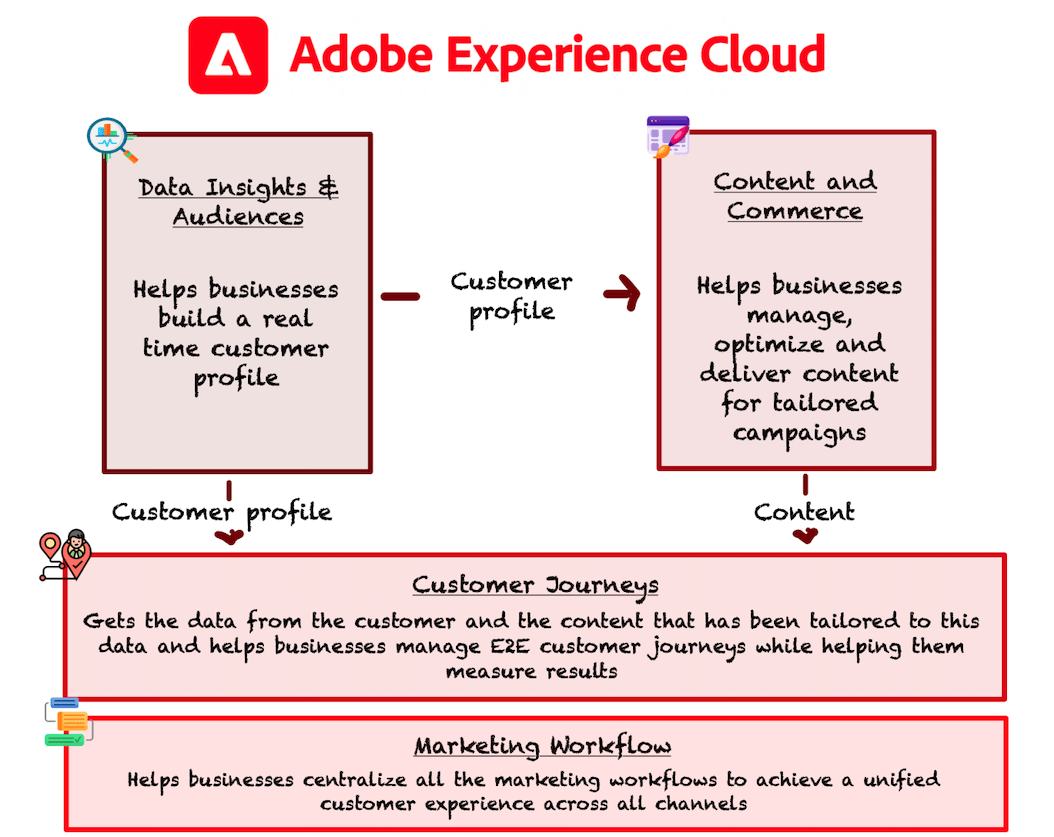

Products included in the Experience Cloud are not new to the company, but the idea of offering a one-stop shop for businesses to sort their marketing, advertising, and analytics needs only dates back to 2018.

Zdnet

-

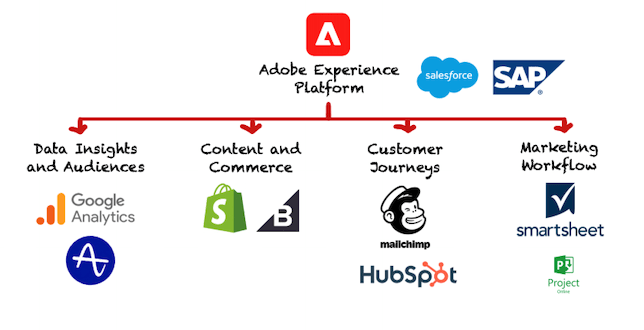

The Experience Cloud aims to help brands and businesses create, manage, execute, measure, monetize and optimize customer experiences.

-

It’s divided into 4 different segments that interact in the following way:

Made by Best Anchor Stocks

-

Besides the three clouds, Adobe has built two transversal products to enhance its capabilities: Adobe Sensei (machine learning and artificial intelligence) and Adobe I/O (allows the personalization of products through open APIs).

-

A summary of Adobe’s offering can be found in the image below:

Made by Best Anchor Stocks

-

Adobe’s products are at the intersection of digitization, a powerful trend that should not stop anytime soon.

How does the company make money?

-

Adobe follows a SaaS (Software as a Service) model, making most (92%) of its revenue from subscriptions. If customers stop paying their fees, they automatically lose access to the software, which makes Adobe’s sales more predictable and resilient.

-

Back in 2008, Adobe followed a product-based business model (customers only purchased the product once and then decided if they wanted to renew), but the impact the GFC (Global Financial Crisis) had on its financials made management start the transition to SaaS.

Sources of revenue growth

-

Adobe has three ways to grow its top line:

-

Selling more subscriptions

-

Coming up with new offerings

-

Increasing prices.

-

Management is currently executing on all three sources. The shift to a freemium model in some offerings is an example of the first source. The launch of the Experience Cloud is an example of the second source, and the company has recently started hiking prices on some products.

Management

-

Adobe’s management is experienced and aligned with shareholders. The key manager is CEO Shantanu Narayen, who has been working for the company since 1998.

-

Despite the company not being founder-led, John Warnock, one of the founders, still serves on the board at the age of 82. Charles Geschke passed away last year.

-

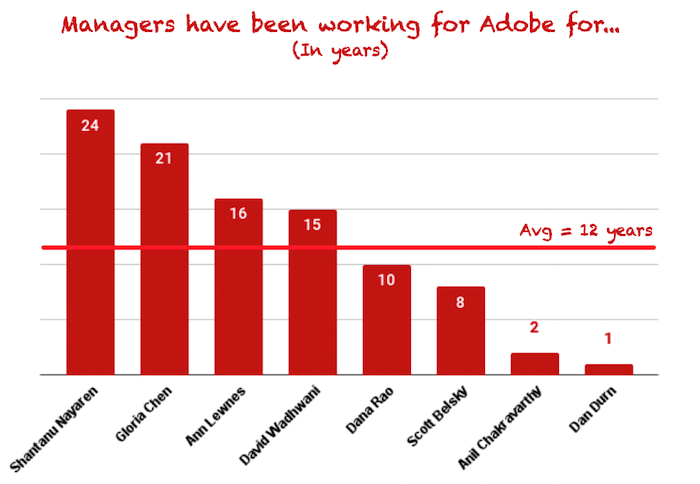

Experienced: Adobe’s managers have been working for the company for an average of 12 years:

Made by Best Anchor Stocks

-

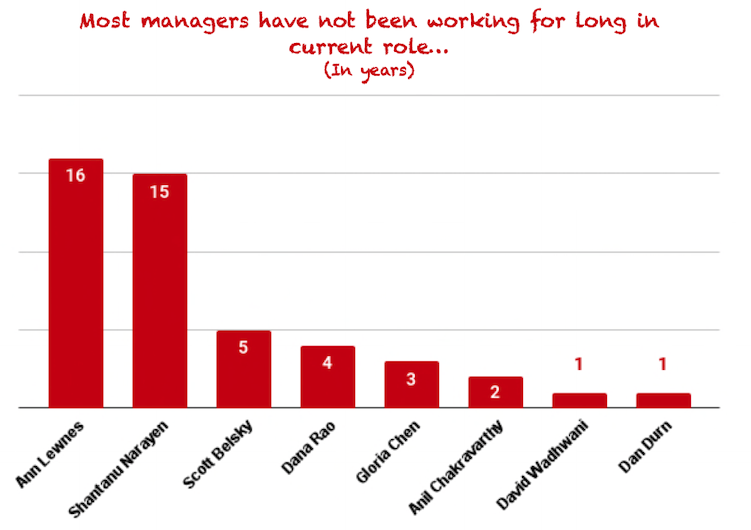

Despite their long stay at the company, some of these managers are relatively new to their current roles:

Made by Best Anchor Stocks

-

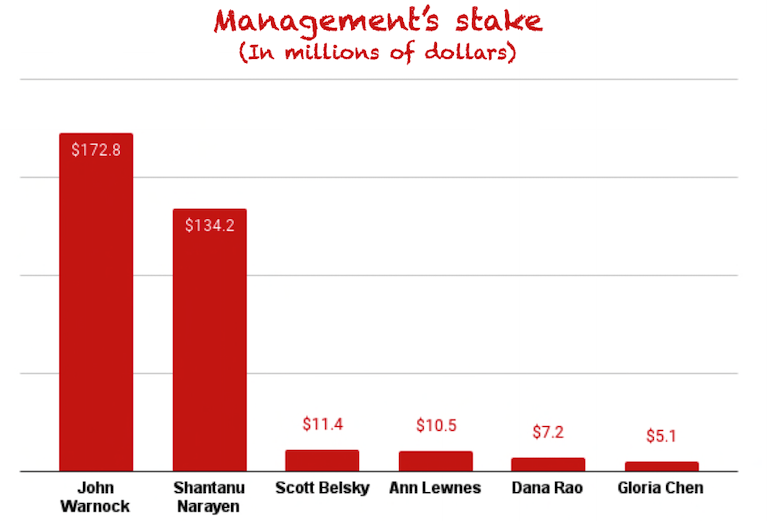

Aligned: insiders collectively own a mere 0.3% of the outstanding shares, which is normal for a company that has been traded for so long. If we look at ownership across managers, we can see how two people stand out: the CEO (Shantanu Narayen) and the Founder (John Warnock):

Made by Best Anchor Stocks

-

We would prefer a higher stake by the management team, but it’s nice to see how two of the most critical managers hold a substantial stake.

Financials and KPIs

-

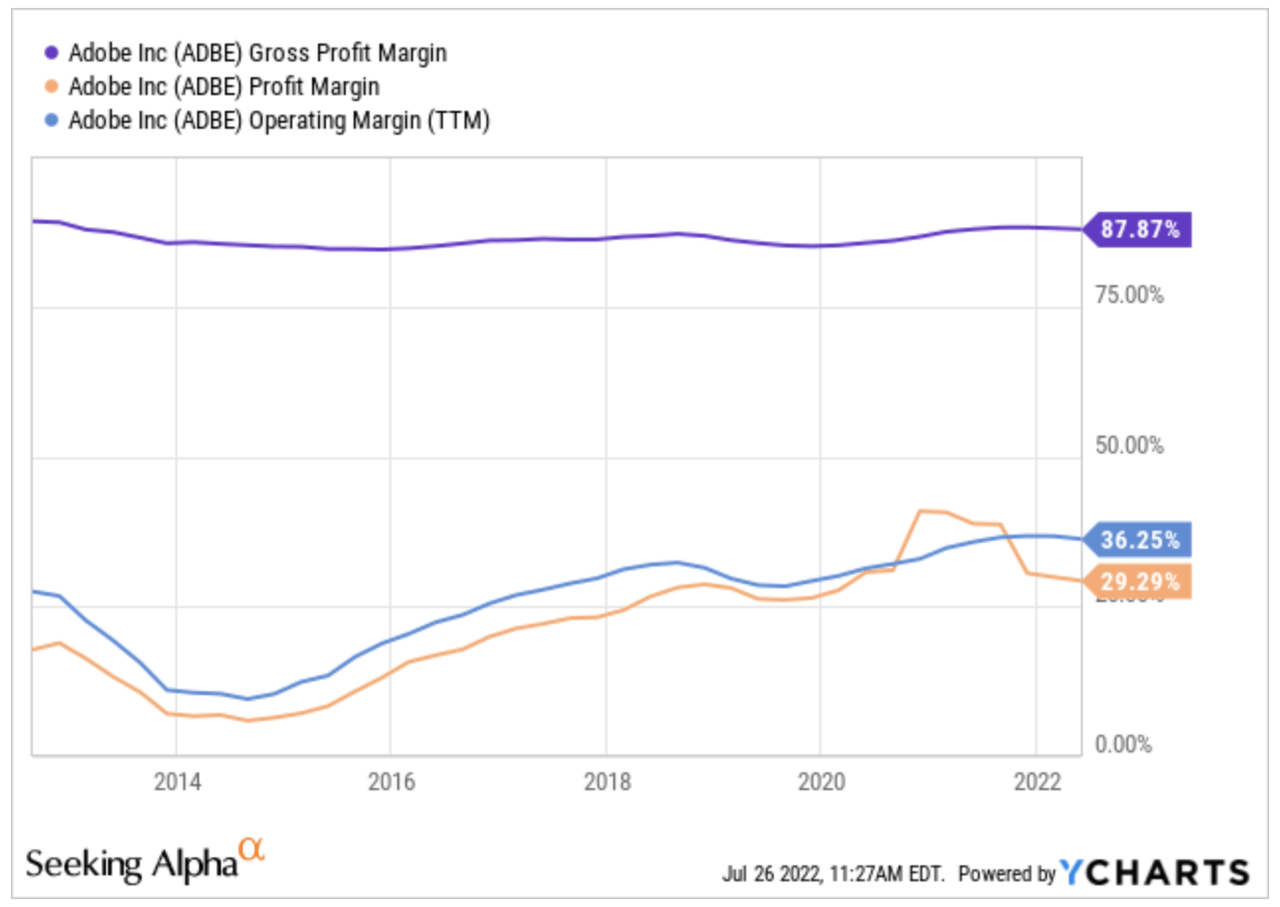

Adobe generated $15.8 billion in revenue in fiscal year 2021. Margins are very high already, so we should expect growth in EPS and FCF per share to come more from growth and share repurchases than operating leverage:

Ycharts

-

The company’s growth has stagnated a bit as some of its products have reached maturity. Still, we believe the company can post 10%+ growth for years to come, aided by nascent offerings (Document and Experience Cloud), coupled with Creative Cloud’s optionality and pricing power.

-

Regarding the balance sheet, Adobe has a solid financial position with $5.8 billion in cash and $4.5 billion in debt. The company’s interest coverage ratio stands at 53x.

-

Adobe is very efficient in translating profits into cash. Its cash conversion ratio (the amount of accounting profits that convert to cash profits) is 150%, and its FCF margin stood at 43% in FY 2021.

Competition

-

Due to its diversified nature, Adobe suffers competition from many players, although the competitive intensity differs across its clouds.

-

In Creative Cloud, there’s no competitor of Adobe’s scale and product breadth, although smaller competitors with point solutions are increasingly successful on the non-professional side. Adobe’s offering is especially strong on the enterprise side (colors measure competitive intensity)

Made by Best Anchor Stocks

-

To fight these offerings, Adobe is launching a series of freemium products (Photoshop web, Creative Cloud Express…) to stimulate the top of the funnel and drive conversions.

-

AI (Artificial Intelligence) is also considered a threat to the Creative Cloud, but management is well aware of this and is investing accordingly.

-

On the Document Cloud side, Adobe is far behind DocuSign (DOCU) in eSignature and Contract Lifecycle Management (‘CLM’). The company is leveraging its extensive device reach to close the gap.

-

Adobe has numerous competitors in the different sections of the Experience Cloud, but the closest competitor by far when it comes to product breadth is Salesforce with its Digital Experience Platform (‘DXP’):

Made by Best Anchor Stocks

-

The company operates in a dynamic and competitive industry across all three clouds. Still, we believe the company has a solid moat to defend its position in Creative and take share in the Document and Experience Clouds.

Risks

We believe Adobe suffers three main risks, one of which can be considered short-term.

-

Competition on the non-professional side: as discussed, smaller competitors are taking share among individual creators. Adobe is trying to fight this, but it remains a risk nonetheless.

-

Key man risk: Shantanu Narayen (Adobe’s CEO) is responsible in a great deal for what Adobe is today. He led the company through the transition to SaaS, and we believe he is important for our thesis. If he were to leave, the thesis would be impacted.

-

Revenue slowdown incoming? (short-term risk): Adobe saw a pull-forward of demand during the pandemic as the world came online. Now, its growth is decelerating slightly, and the growth levers that should carry the company forward are still not large enough to move the needle. We might come across a period of slower growth, but we believe the growth of the business is durable.

The moat

-

Adobe’s moat comes from its product breadth, which, together with its leadership position and brand, gives the company a loyal and sticky user base.

-

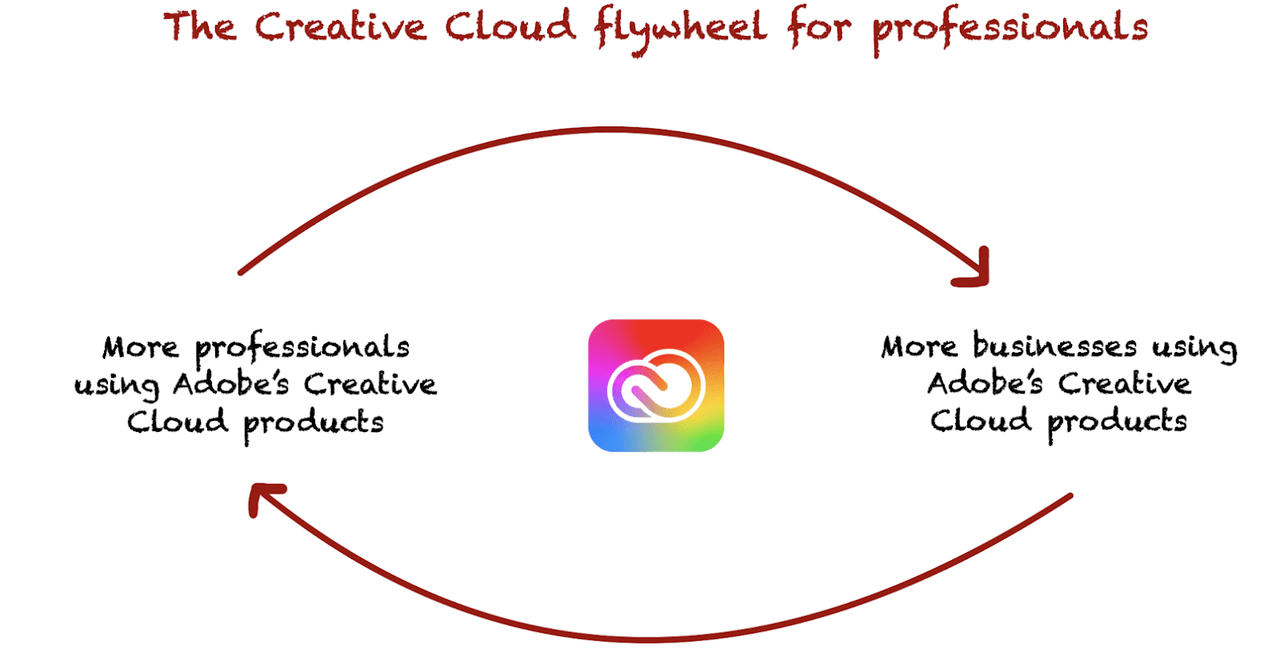

In Creative Cloud, the company has managed to build a powerful network effect. As Adobe’s products are dominant, students are “forced” to learn to use them if they want to find a job. As most students come with the “Adobe skillset,” enterprises’ incentives to switch to other products are significantly reduced:

Made by Best Anchor Stocks

-

In Experience Cloud, Adobe’s moat is in the switching costs, as very few customers are willing to switch to a competing solution once all systems and data run on Adobe. As a result, the challenge is not customer retention but customer growth, which the company leverages on partners such as Accenture.

Accenture

Tailwinds and Optionality

-

Optionality for Adobe comes from its large and established user base and its dominant position in dynamic industries. The Creative industry is constantly evolving, and Adobe can benefit from new trends and formats such as the Metaverse and 3D editing. On the Experience Cloud side, customers are always trying to differentiate themselves from the competition through innovative user experiences, which opens up a universe of unmet needs for Adobe to fulfill.

-

Adobe’s tailwind lies in the advance of digitization. With the world going online, there is an increasing need for digital content creation, omnichannel experiences, and digital document processing. The company lies at the intersection of these three trends.

In the meantime, keep growing!

Best Anchor Stocks helps you find the best growth stocks to outperform the market with the lowest volatility. They can anchor your portfolio on the stormy market sea, still allowing you to outperform.

Best Anchor Stocks have a long track record of revenue growth combined with below-average volatility. The first pick is up 16,000% from its IPO but has never been down 30%, not even during in 2008-2009.

Best Anchor Stocks can serve several purposes: stabilize your high-growth portfolio, or add low-volatility growth to your index, dividend or value investing.

There’s a 2-week free trial, so don’t hesitate to join Best Anchor Stocks now!

Be the first to comment