NunoMonteiro

A Quick Take On Acutus Medical

Acutus Medical (NASDAQ:AFIB) reported its Q3 2022 financial results on November 10, 2022, missing revenue estimates but beating EPS estimates.

The company is commercializing cardiac ablation imaging, mapping and other tools.

While management appears to be making rational decisions to focus on its existing customer base, it is not likely to result in a material upside catalyst to revenue growth.

In the near term, I’m on Hold for AFIB.

Acutus Medical Overview

Carlsbad, California-based Acutus was founded to develop cardiac ablation tools including its AcQMap imaging and mapping system to assist in mapping the ‘drivers and maintainers of arrhythmias.’

Arrhythmias are when the heart beats in an irregular manner which can lead to failure, stroke and sudden death.

Management is headed by president and Chief Executive Officer David Roman who has been with the firm since 2021 and previously held senior roles at Baxter International and was a Managing Director at Goldman Sachs.

The company’s primary offerings and product candidates include:

-

AcQMap – Imaging and mapping system

-

AcQTrack – Analysis tool

-

AcQBlate – Ablation system and catheter

-

Various other tools

The firm seeks to sell its products to physicians via a direct sales and marketing force, through events, conferences, trade shows and educational processes, and outside the U.S. through distribution partners.

Acutus Medical’s Market & Competition

According to a 2020 market research report by MarketsAndMarkets, the global market for cardiac ablation is believed to have grown at a CAGR of 12.5% from 2014 to 2019.

2019’s expected value of all types of cardiac ablation treatment was approximately $883 million.

Key elements driving this expected growth are a growing elderly population increasing demand for procedures, increased awareness and continued technological innovation in the field.

Also, emerging market regions have also shown growth in demand, including countries such as China, India, Brazil and Mexico.

Major vendors that provide or are developing treatments or related systems include:

-

Abbott Laboratories

-

Advanced Cardiac Therapeutics

-

Alcon Laboratories

-

AngioDynamics

-

AtriCure

-

Biosense Webster

-

Boston Scientific

-

CONMED

-

Medtronic

Management says its system provides ‘unmatched speed and precision’ in mapping the drivers and maintainers of arrhythmias.

Acutus Medical’s Recent Financial Performance

-

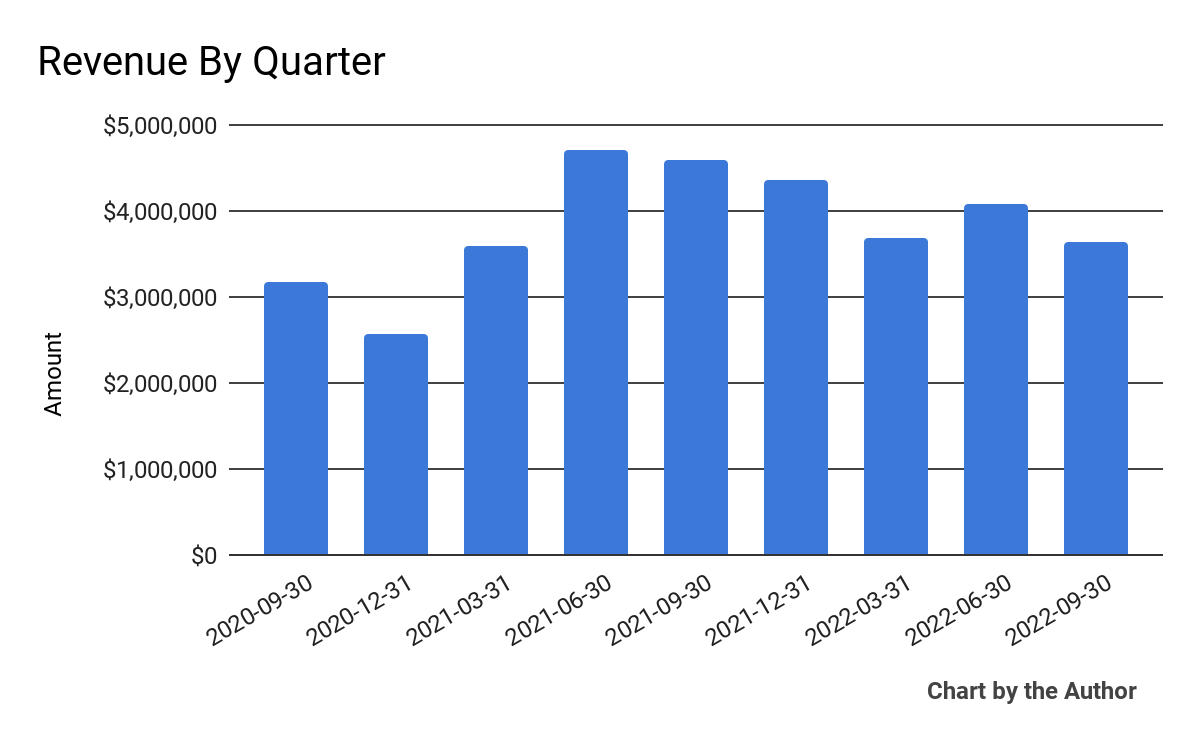

Total revenue by quarter has dropped in recent quarters, as the chart shows below:

9 Quarter Total Revenue (Financial Modeling Prep)

-

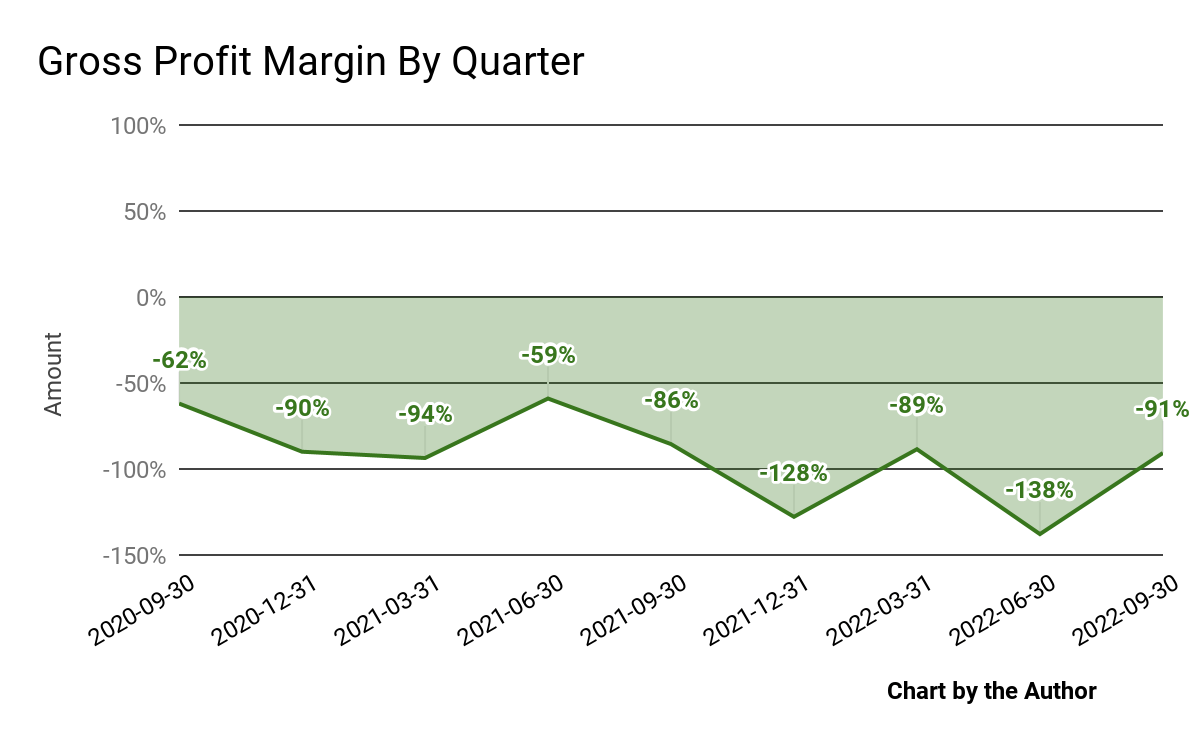

Gross loss margin by quarter has worsened markedly in recent reporting periods:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

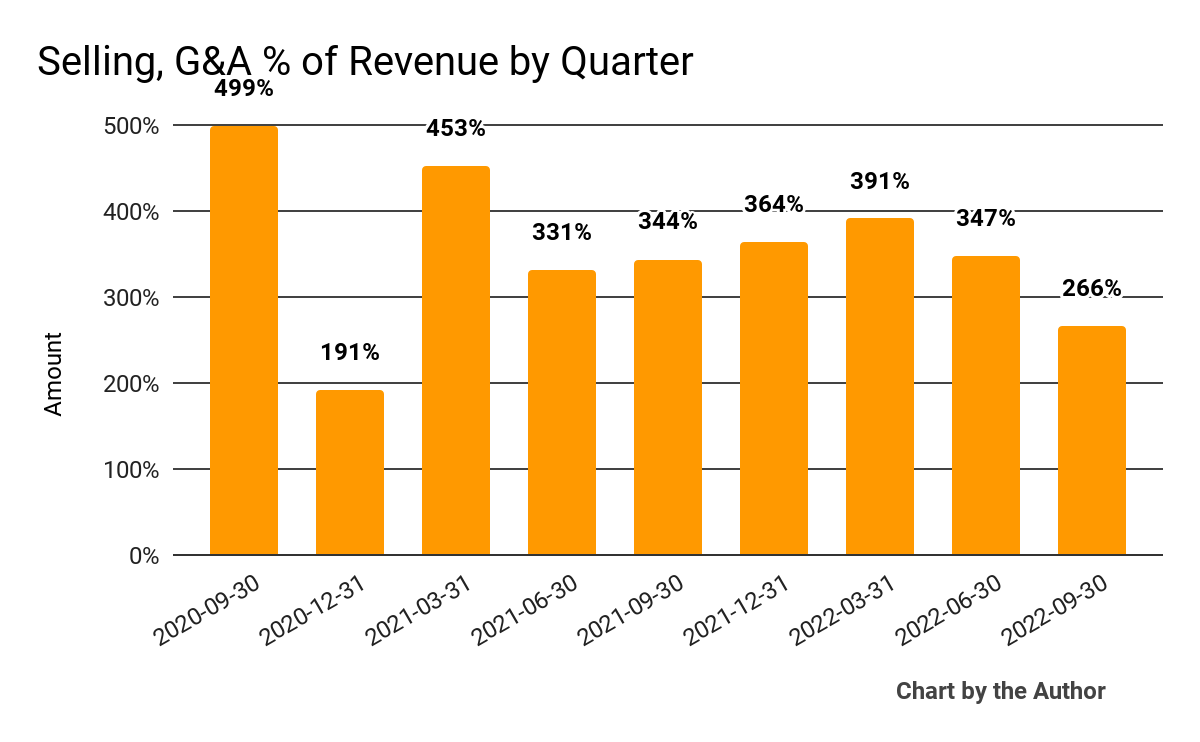

Selling, G&A expenses as a percentage of total revenue by quarter have remained very high as the firm seeks to ramp up its sales efforts:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

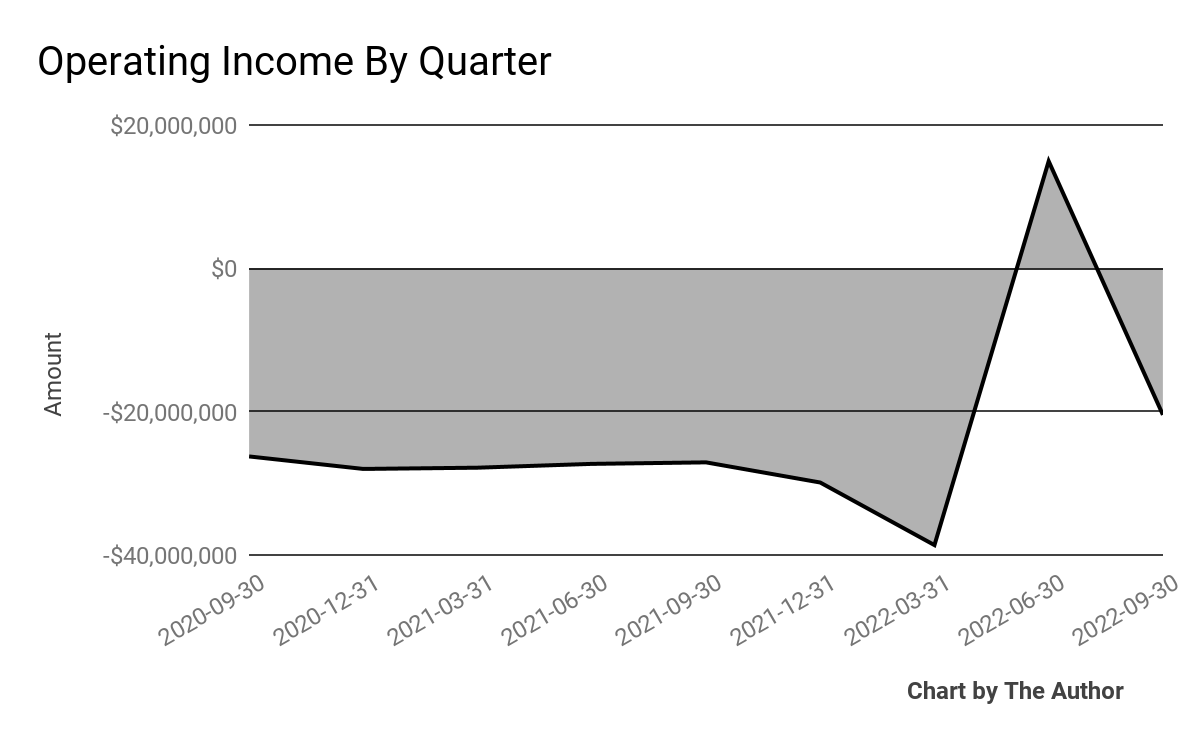

Operating income by quarter has generally remained negative in recent quarters, with the exception of Q2 2022:

9 Quarter Operating Income (Financial Modeling Prep)

-

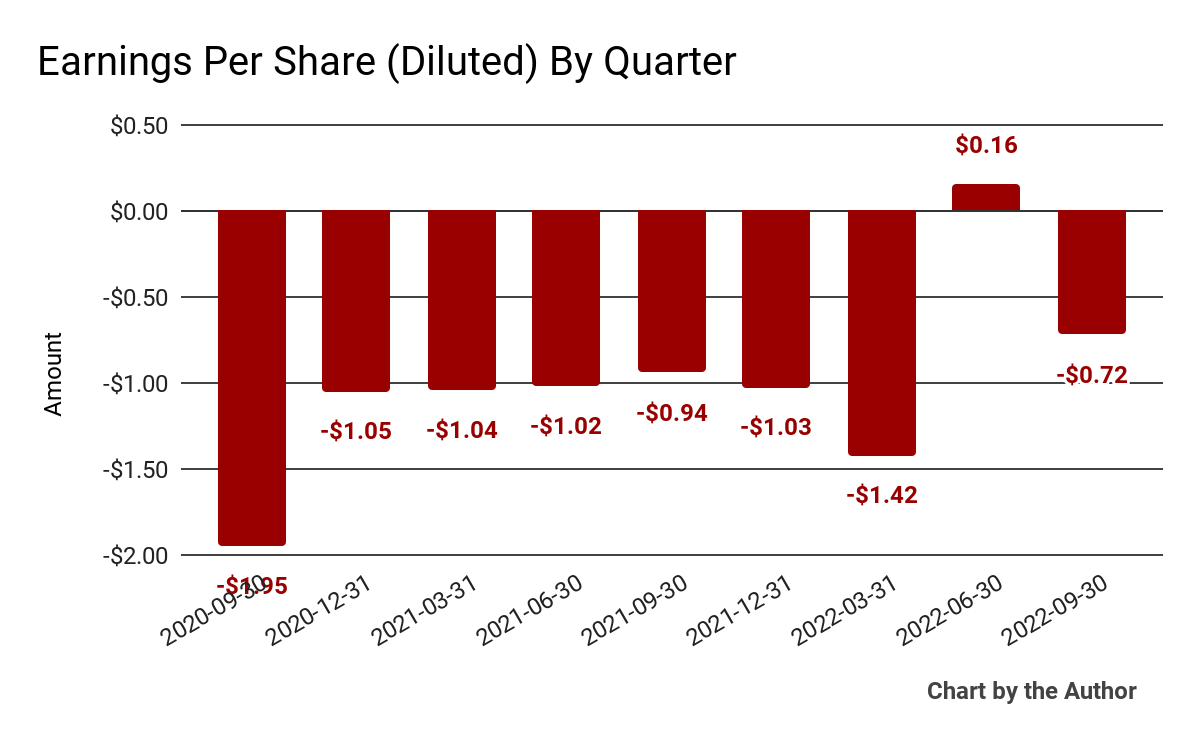

Earnings per share (Diluted) have also remained negative except for Q2 2022:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

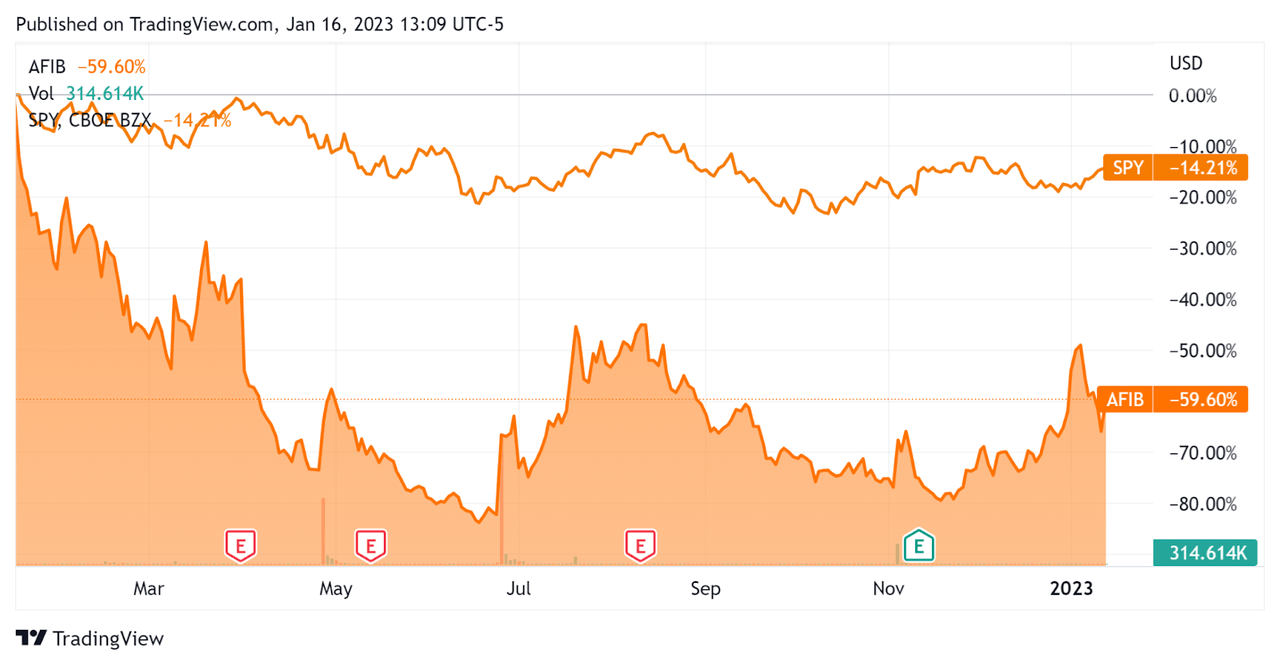

In the past 12 months, AFIB’s stock price has fallen 59.6% vs. the U.S. S&P 500 index’s drop of around 14.2%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Acutus Medical

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

2.9 |

|

Enterprise Value / EBITDA |

-0.6 |

|

Revenue Growth Rate |

1.9% |

|

Net Income Margin |

-545.5% |

|

GAAP EBITDA % |

-488.5% |

|

Market Capitalization |

$34,711,684 |

|

Enterprise Value |

$45,501,610 |

|

Operating Cash Flow |

-$44,719,000 |

|

Earnings Per Share (Fully Diluted) |

-$3.01 |

(Source – Financial Modeling Prep)

Commentary On Acutus Medical

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the progress of its shift in AcQMap commercialization strategy.

The company has reduced focus on expanding its customer base and increased focus on growing utilization volume and activity within its existing customer base.

Acutus has pursued this strategy as it has downsized its organization to save money and reduce cash use.

As to its financial results, revenue dropped 23.9% year-over-year due to lower equipment sales, although management says procedure volume rose by 17%.

Gross profit margin worsened year-over-year, although operating loss and negative earnings per share were less than the previous year’s same period.

For the balance sheet, the company ended the quarter with $66.3 million in cash, equivalents and short-term investments and $34.3 million in long-term debt.

Over the trailing twelve months, free cash used was $100.5 million, of which capital expenditures accounted for $5.9 million. The company paid $11.0 million in stock-based compensation, which is high for such a low revenue base.

Looking ahead, full-year 2022 revenue is expected to be around $15.75 million at the midpoint of the range.

Regarding valuation, the market is valuing AFIB at a Price/Sales multiple of around 2.9x.

The primary risk to the company’s outlook is continued supply chain challenges, foreign exchange headwinds for its European sales and its strategy of reduced capital equipment sales.

A potential upside catalyst to the stock could include an easing of supply chain problems affecting its AcQGuide MAX product.

While management appears to be making rational decisions to focus on its existing customer base, it is not likely to result in a material upside catalyst to revenue growth.

In the near term, I’m on Hold for AFIB.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment