Hazal Ak/iStock via Getty Images

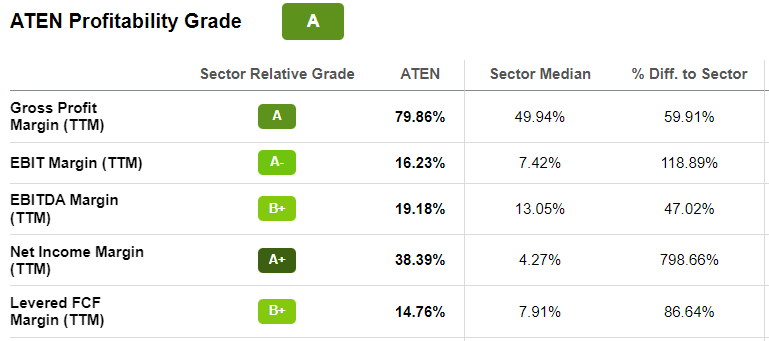

Cash remains king when the market fluctuates especially at a time when the Federal Reserve is both increasing interest rates and carrying out quantitative tightening. In this case, it is better to invest in companies like A10 Networks (NYSE:ATEN) which possesses a superior free cash flow margin metric when compared to the median for the IT sector. Coincidentally, the company, which provides networking solutions, also enjoys better profitability metrics as shown in the table below.

Profitability Grades (Seeking Alpha)

However, despite all these green attributes, the stock has lost nearly 14% of its value in the past month alone, a period which coincided with Federal Chairman Powell’s more hawkish stance as to hiking interest rates. One reason could be that the stock is being indiscriminately punished as a tech company, whose valuations are seen as high. However, this is not the case for both the Price-to-Earnings (GAAP) and the Price-to-Cash flow, which remain below the sector median.

My objective with this thesis is to lay emphasis on the cash-generating capability of A10’s business model, especially at a time when QE (Quantitative Easing) is coming to an end.

Importance of Cash at the End of QE

QE is coming to an end, whether it is in Europe, Japan, England, or the U.S. Now, the easing of monetary policy is all about purchasing government bonds and mortgage-backed securities. It was implemented soon after Covid was declared a pandemic in April-May 2020 to boost up the economy which was in a frozen state due to lockdown measures severely impeding business activities. Also, with interest rates already low, there were no other valid alternatives. Without delving into the inflation problematics, QE worked, just as it did during the financial crisis of 2008 triggering an increase in the money supply which led to a further reduction in corporate borrowing rates.

Currently, the opposite is happening, implying that liquidity is being drained out of the system and conversely, this increases borrowing rates. Additionally, the fact that the Fed is hiking rates amounts to a “double tightening”, which could lead to turbulence in the credit market and thus impact money flows to businesses.

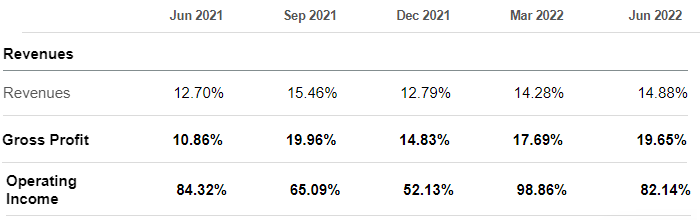

In these conditions, you want to own a company that not only has a solid balance sheet, but also one which good cash metrics. This is the case with A10, which also has superior profitability metrics too, but an understanding of the business model is also warranted. In this respect, growing quarterly revenues at a rate of 12.7% to 15.46% in the last five quarters as per the table below, the operating income has grown at a much faster pace of 52% to 99%.

Growth of Quarterly Revenues on a Year-on-Year Basis (Seeking Alpha)

This appears quite unusual in an environment where supply chain issues increase the cost of sales and depress gross margins. However, this was not the case for A10, which on the contrary has managed to raise gross margins to 80.16% in its last reported quarter or Q2-2022. This was up both sequentially and on a year-on-year basis and was attributed to a better product mix as well as “successful navigation of short-term input cost pressures”.

Singling out the product mix, investors will note that the company designs purpose-built solutions to ensure that corporate applications are not only highly available but also accessible at an accelerated speed by end-users, while not forgetting the security aspect. This all helps to reduce downtime and ensure business continuity across corporate data centers and multiple clouds.

High Demand for Security but Headwind from Strong Dollar

Looking further, demand is high due to U.S. corporations facing a higher threat of cyberattacks. This was already the case since 2020 as hackers took advantage of the fact that IT workloads were being frantically migrated to the cloud to allow employees to access applications from their homes as part of remote work. The situation has now been made worse by the conflict in Eastern Europe and geopolitical tensions in East Asia with nation-backed cybercriminals now constituting a more severe threat.

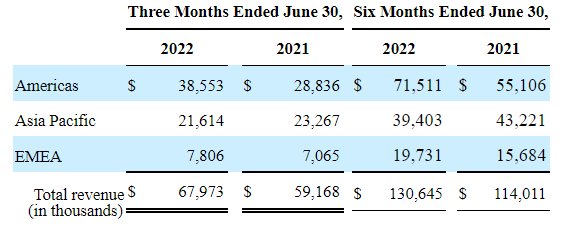

Thus, in order to protect themselves, CEOs have to strengthen IT security measures while at the same time not compromising on speed. It is here that A10 Networks’ gear proves handy as the company was initially a strong player in load balancers which as its name implies are used to balance workloads to provide users with the best working experience by increasing their access times to applications. Thus, out of the 14.9% increase in year-over-year revenue growth for Q2, 33.7% came from the Americas region, which includes the U.S.

Comparing Revenues for the first 3 months (Seeking Alpha)

On the flip side, with organizations prioritizing security amid macroeconomic concerns, there has been reduced demand for the company’s standalone ADC or Application Delivery Controller. However, the fact that this weakness is offset by strength in security-enabled products is a positive as there is no indication yet of events that can lead to a de-escalation of geopolitical tensions.

This said, with more than 40% of sales coming from outside the U.S., the company is suffering from the strong dollar, namely in Japan where the yen reaching new lows against the greenback and has led to a 7.1% reduction in Q2 revenues compared to the same period last year.

Mitigatory Actions Vs. Downturn and Valuations

Now, as the Fed tightens further, the economic situation may get really tough with companies prioritizing survival and operational projects over IT security and optimization. Looking for mitigatory factors, I found that A10 can rely on recurring revenues which amounted to $29.2 million in Q2 after increasing by 7%. This translates to 43% of its overall sales, or a significant portion, and is similar to SaaS companies relying on more stable subscriptions.

Along the same lines, deferred revenues which are prepayments made by customers for services that have to be delivered in the future increased to $127.9 million and represent around half of 2021 revenues. These can be envisioned as a cushion for hard times.

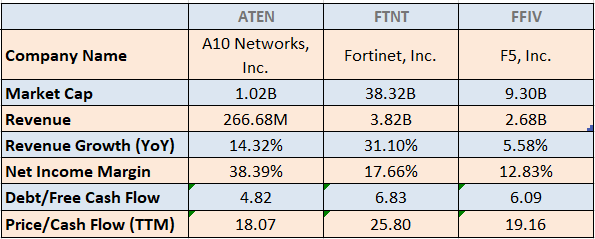

In addition to revenues, hard times do warrant the capacity to execute on cost reduction and for this purpose, a comparison with Fortinet (NASDAQ:FTNT) and F5 (NASDAQ:FFIV) reveals that despite exhibiting a much low annual revenue level due to its smaller scale, A10 has been able to deliver higher net income margins as shown in the table below.

Comparing key metrics with peers (Seeking Alpha)

One of the reasons for this as I mentioned above is profitability increasing faster than revenues which in turn implies a reduction in operating expenses. Looking deeper, it is the SG&A (sales, general and administrative) expenses that have been reduced on a sequential basis since the September 2021 quarter while R&D remains stable at 20-21% of revenues.

For this purpose, according to the CEO, they are using a differentiated approach for the sales and marketing functions, which is not necessarily based on increasing the headcount, but rather, on making the staff more productive in selling.

This is more of a balanced strategy making use of productivity improvements, instead of outright recruitment to beef up the sales team and is effectively working in delivering more profitable growth. It also serves to partly alleviate the effects of higher wage inflation and helps to preserve cash. Now, it is exactly based on the trailing Price-to-Cash flow of 18.07x that A10 is undervalued with respect to peers. Making an adjustment based on Fortinet’s value of 25.8x (above table), I obtain a target price of $18.8 (25.8/18.07 x 13.14) based on the current share price of $13.14.

Conclusion

Therefore, based on its lower valuations, A10 is a buy. This optimism is supported by its business model which enables accelerated profitable growth. Also, the company possesses the necessary cash-generating capacity to face the forthcoming period of monetary tightening implying lower liquidity. To this end, it had cash of $166.8 million and debt of only $23.9 million at the end of June. Still, do not forget that September is likely to be volatile for stocks as is usually the case when the Fed hikes interest rates.

Finally, by paying a dividend yield of 1.14%, at a payout ratio of 22.39%, the company has the capacity to pay more. In this respect, with an average quarterly capital expense of around $1.9 million and primarily focused on organic growth, there is less likely to be an acquisition to perturb the flow of free cash in the coming quarters.

Be the first to comment