sinseeho/iStock via Getty Images

Prologue

Contrary to my alter-ego’s Elon Musk-Driven Pair Trade, I promise you three things regarding my suggested pair trade:

- Shorter writing [but only slightly]

- Less controversial [but still controversial; as if one can expect anything else when Tesla (TSLA) and/or Twitter (TWTR) is/are involved…]

- It has nothing to do with Elon Musk [As long as he doesn’t intend to come up with a buyout offer to any of the two biotech that are the focus of this piece]

Pairs trading is a non-directional, relative value investment strategy that seeks to identify 2 companies or funds with similar characteristics whose equity securities are currently trading at a price relationship that is out of their historical trading range. This investment strategy will entail buying the undervalued security while short-selling the overvalued security, all while maintaining market neutrality. It can also be referred to as market neutral or statistical arbitrage. – Source: Fidelity

Moreover, readers should keep in my mind the following important aspects:

- Non-Directional: A pair trade isn’t about being against the company on the short side (of the trade) rather about being in favor of the stock on the long side relative to the stock on the short side.

- Relative Value: A pair trade isn’t about choosing one stock that is expected to move up (long leg) and one stock that is expected to move down (short leg). It’s great if this is the outcome, but the main purposes of a pair trade are hedge (lower risk trade) and edge (relative value).

- Similar Characteristics, e.g. same sector, same industry, similar yield, product/s, or customers.

- Out of Historical Trading Range. In most cases, this is quite obvious. However, when it comes to stocks that are subject to an immediate/near-term buyout – things are more complicated, surely not that simple.

Merck & Co

Let me start by saying loud and clear: Not only do we have nothing against Merck & Co (NYSE:MRK), but we actually like the company. After all, how can we dislike a company like Merck shortly after declaring that we’re bullish on Healthcare & Biotech?

Nonetheless, there’s a difference between a company’s operations and the valuation of the exact same company. While the former can be great, the latter might be nowhere near as great.

Is there anything wrong with MRK’s valuation right now? No, there isn’t.

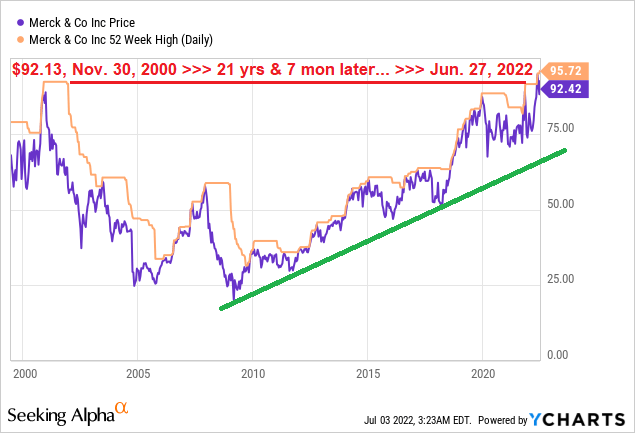

As a matter of fact, the stock just broke into a new all-time high, after a waiting period of 21.5-year!

Y-Charts, Author

Technically, this is a bullish pattern, however:

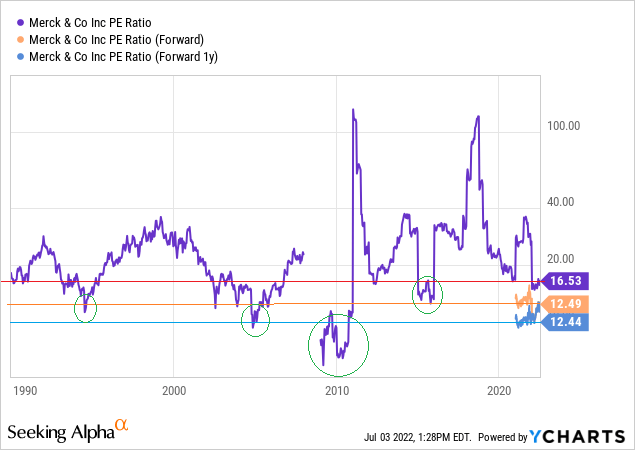

1) There’s nothing particularly exciting about MRK’s current valuation (TTM multiple of 16.5).

The stock been there, done that, and most of the past runs-up started from the stock trading with lower multiples.

Y-Charts, Author

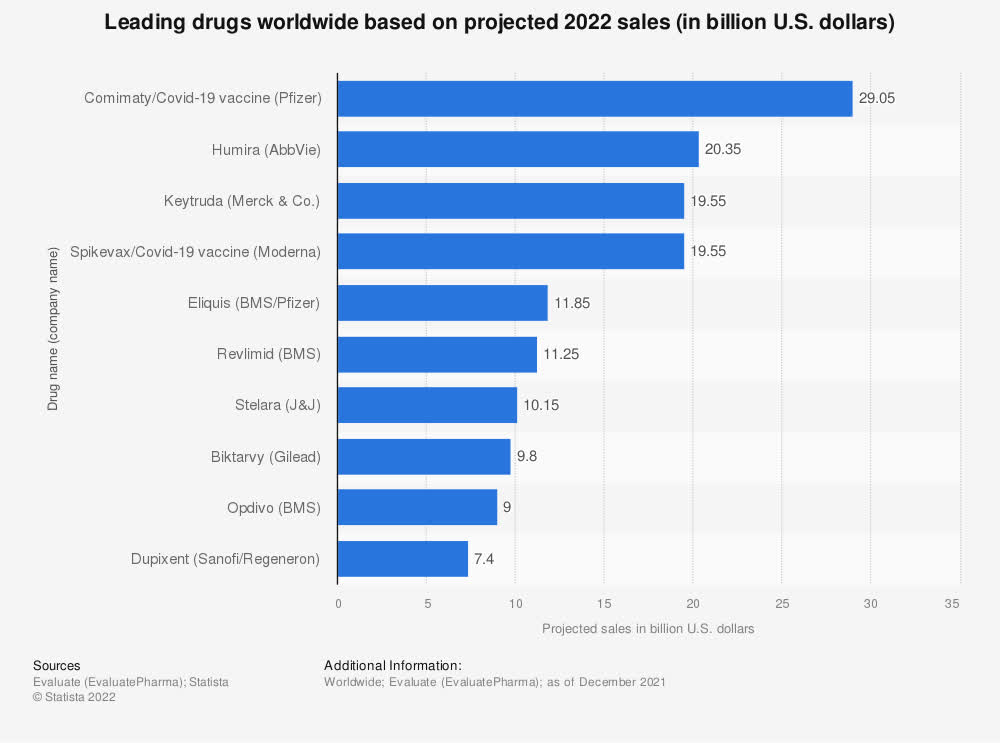

2) The near-term future (12-24 months) doesn’t tell the full story regarding Merck’s mid-term future (3-7 years). Merck’s Keytruda is one of the world’s top selling drugs, with projected sales of ~$20B in 2022.

Statista

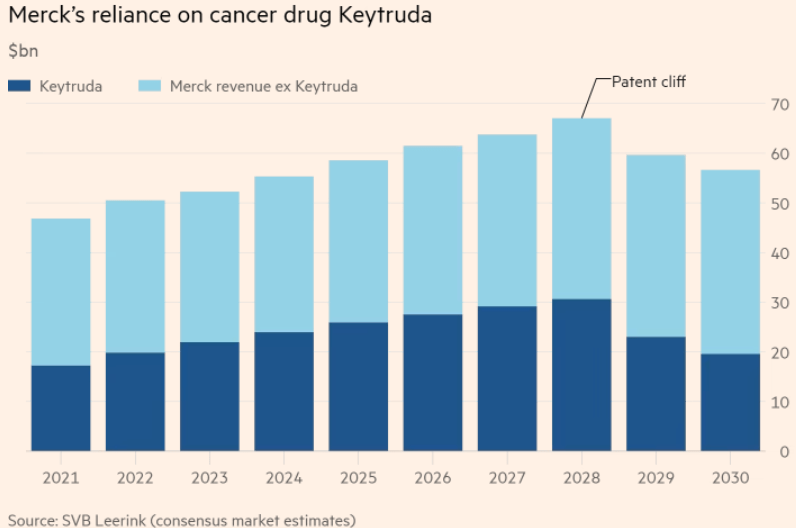

Sometime after 2028, Keytruda will lose its patent exclusivity and Merck is already looking to fill what is expected to be an over $30B/year loss to its top line.

When the time of the patent expiration comes, Keytruda sales are projected to account for more than half of Merck total sales. Therefore, this is a real threat for Merck; a threat that must be addressed way before 2028.

SVB Leerink

This is the main reason behind the recent chatter regarding Merck potentially making a move to buy Seagen (NASDAQ:SGEN), a promising biotech that is:

- boasting marketed drugs

- having an impressive pipeline

- operating without a CEO (over the last couple of months)

SGEN is a perfect fit for MRK (as well as a few others), and so it’s anything but a surprise that many believe a Seagen takeover (by Merck) is inevitable.

Nonetheless, in this article, we’re not going to analyze the potential and/or merits of such a deal. Instead, we’re only going to focus on the (likely) possibility that Merck is about to push forward with an acquisition.

As we all know, following most buyouts, the stock price of the acquiring entity tends to move down (especially if there’s dilution) and the stock price of the acquired entity tends to move up (due to the premium that is almost always being paid).

If so, it would only be natural for MRK to move down and for SGEN to move up, if and when a buyout is announced.

Thing is, there’s more to it than just this.

The Seagen Factor

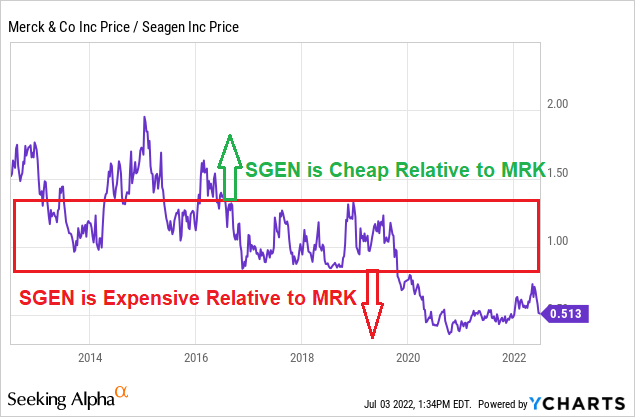

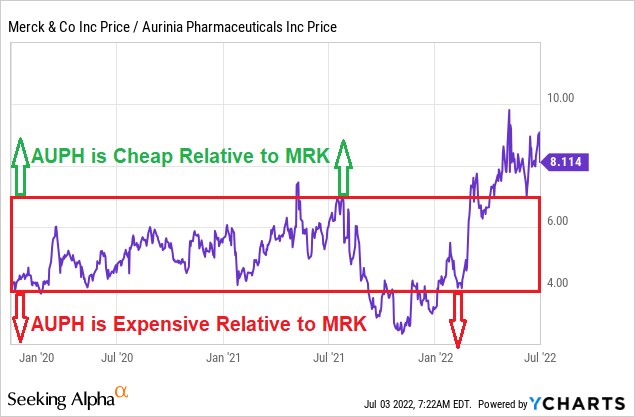

Remember the “Out of Historical Trading Range” that we’ve mentioned above? Well, if you look at the MRK/SGEN ratio, you can clearly see that it’s trading out of the historical trading range.

Based on this ratio, SGEN is too expensive relative to MRK.

Y-Charts, Author

Does it mean that buying SGEN isn’t a worthwhile move for MRK? No, it doesn’t, but it does suggest that such a deal would be an expensive one.

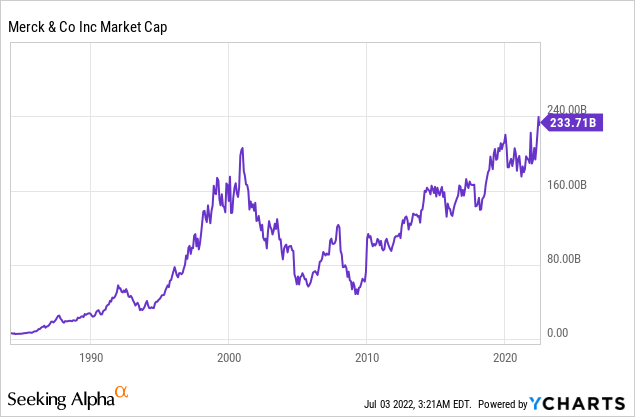

Merck has a market-cap of ~$234B.

Y-Charts

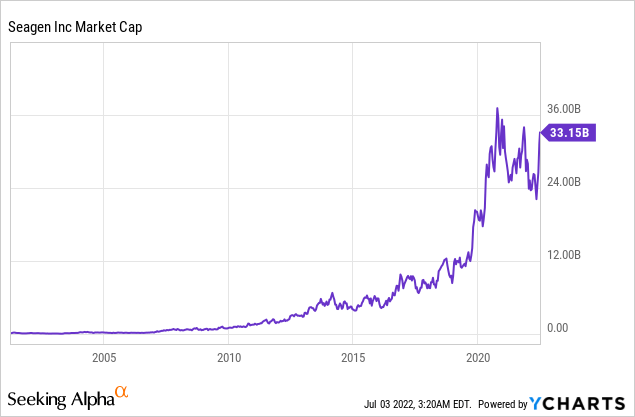

Seagen has a market-cap of ~$33B.

Y-Charts

Even if MRK makes a move, we don’t know whether the deal would be cash only, stock only, or a combination of both.

That’s key to understand what would be the impact on MRK, because not only the exact valuation is important (SGEN is expected to be taken out for at least $200/share, or about $38.5B), but also the mean of payment.

Since MRK is trading at an all-time high, it would be tempting (for the company) to pay in the form of its stock, however that would be a fairly significant dilution (even if the value of SGEN for MRK justifies this).

No matter what, SGEN is going to be a big deal for anyone buying it, and it’s likely that the market is going to “punish” the acquiring company, for the inherited risk that comes with paying ~$40B (no matter how good/promising is the purchased item), regardless of the exact mean of payment.

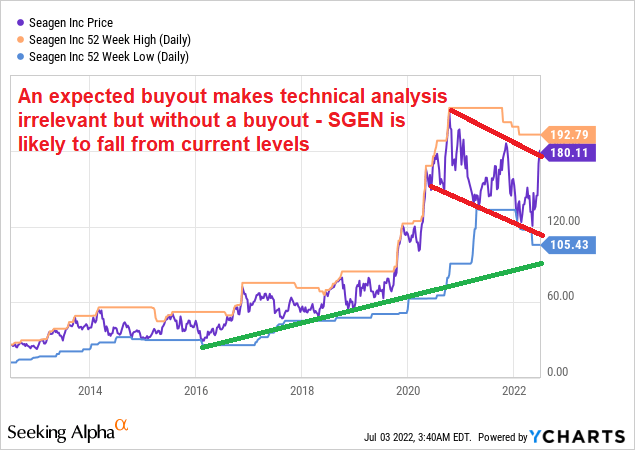

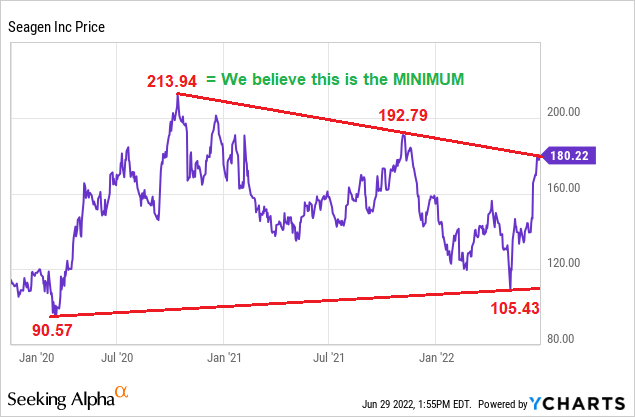

Side note: Without a deal, SGEN is likely poised to decline from here.

Y-Charts, Author

Why do we touch upon all of this? Because if you ask yourself why do we use MRK, and/or why don’t we use SGEN, on the short leg of the pair trade, there are a few answers:

- If a deal doesn’t happen, we believe that MRK’s upside is limited.

- If a deal happens, we believe that MRK is poised to lose steam.

- If a deal doesn’t happen, we believe that SGEN’s downside is limited because if it won’t be MRK now – it would be someone else (or MRK…) later on.

- If a deal happens, we believe that SGEN is likely to soar. We expect a deal (no matter who is the buyer) to be for at least $214.

Y-Charts, Author, Wheel of Fortune

All in all, while MRK on the short side is little risk (that we’re willing to take), SGEN on the short side is a big risk (that we don’t want to take).

Aurinia Pharmaceuticals

Aurinia Pharmaceuticals (NASDAQ:AUPH) has been subject to buyout speculations for well over a year now.

It was as early as May 2021, when The Times mentioned AstraZeneca (AZN) or GSK (GSK) are “sniffing around” Aurinia. Later on, GSK itself denied the report.

In October 2021, it was Bloomberg reporting that Bristol Myers Squibb (BMY) might come up with an offer for AUPH, after losing to Merck (MRK) in the battle to acquire Acceleron Pharma.

In late October Cantor analyst Alethia Young said AUPH could be sold for $45-$53/share, with Amgen (AMGN), AbbVie (ABBV), Johnson & Johnson (JNJ) and Japanese Otsuka Pharmaceuticals (OTCPK:OTSKF) mentioned as potential bidders aside of BMY. Betaville added Roche (OTCQX:RHHBY) to the mix.

A month later, it was Novartis’ (NVS) R&D day, where the company put the focus on smaller deals that refueled takeover speculation chatter.

In January 2022, a Stat News report added Biogen (BIIB) to the long list of interested parties, as part of the company’s search for potential targets.

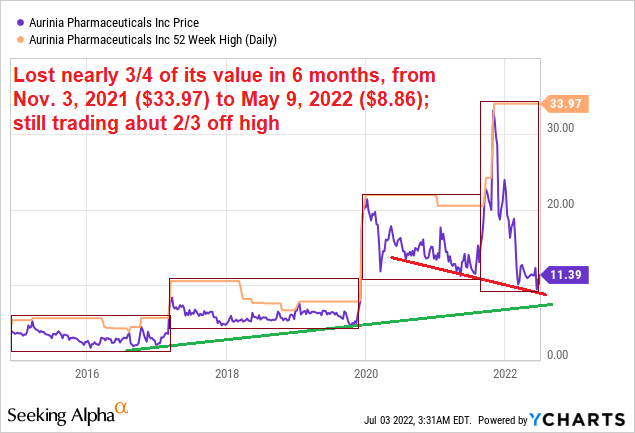

Over recent months, the non-stop stream of rumors has (somewhat) stopped, and AUPH’s share price is reflecting this.

Y-Charts, Author

However, just like a Phoenix arising from the ashes, the AUPH takeover chatter emerged (from the rumors) last Friday after Betaville issued an “uncooked” alert, once again pointing to Otsuka as a potential buyer.

As a result, the stock surged as much as 13% and expectations are for a fairly quick buyout.

Going back to trading “Out of Historical Trading Range”, it’s clear that based on the current MRK/AUPH ratio, AUPH is cheap relative to MRK.

[Perhaps MRK should be buying AUPH instead, or at least before SGEN?…]

Y-Charts, Author

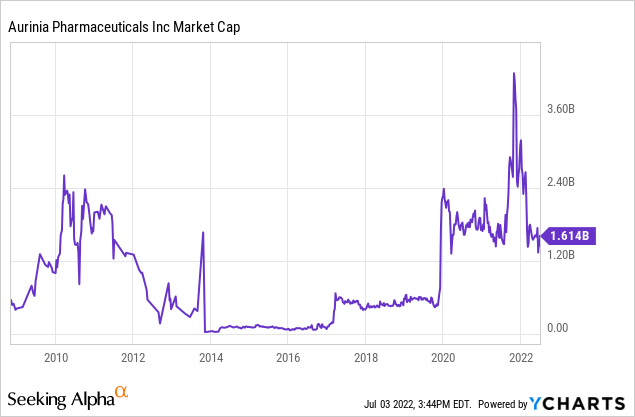

Unlike SGEN, let alone MRK, AUPH is a small fish, with a market-cap of only $1.6B. That makes a buyout an easy deal/pill to swallow for any large-cap, let alone mega-cap, pharma, even if a premium of 100%-150% is being applied.

[Note that Otsuka Pharmaceuticals, the most recent suspect to acquire AUPH, has a market-cap of $19.36B]

As such, it’s no wonder that most investors (including the ones that participated in our survey) are seeing a deal for AUPH coming before SGEN.

[We’re not so sure about this, but again – that’s a separate discussion which is less relevant for the immediate pair-trade idea we present in this article]

Valuations and Risks

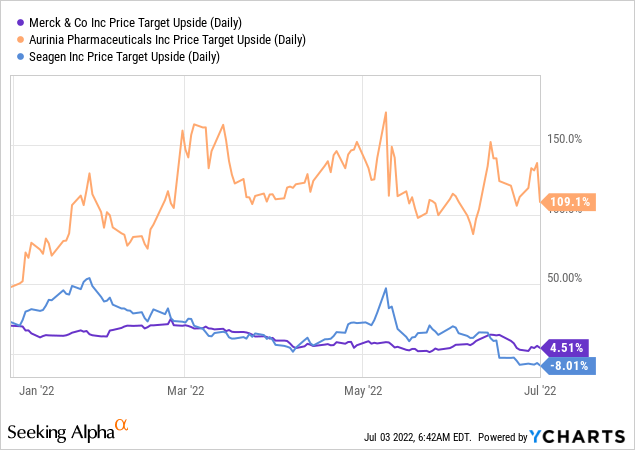

Let’s look at what Wall Street analysts are expecting from the relevant stocks:

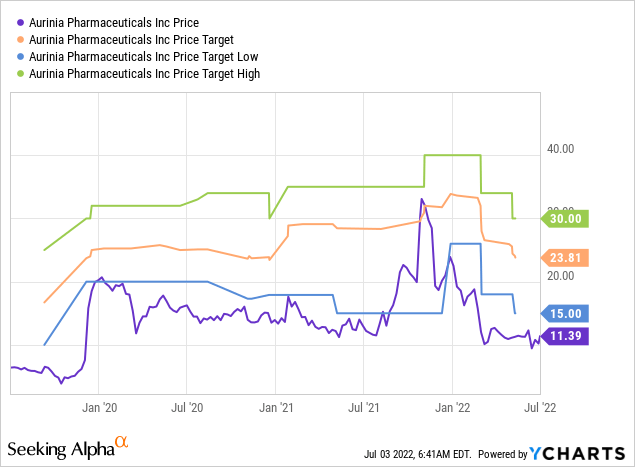

AUPH:

- Expected Upside (to average price target): More than double.

- Max. Downside: None.

- Max. Upside: +163%

Conclusion: Little downside risk; a significant upside (especially in a buyout)

Our take: We agree with Wall Street. AUPH buyout should be inside the 20-30 range, with a bias towards the upper half of the range.

Y-Charts

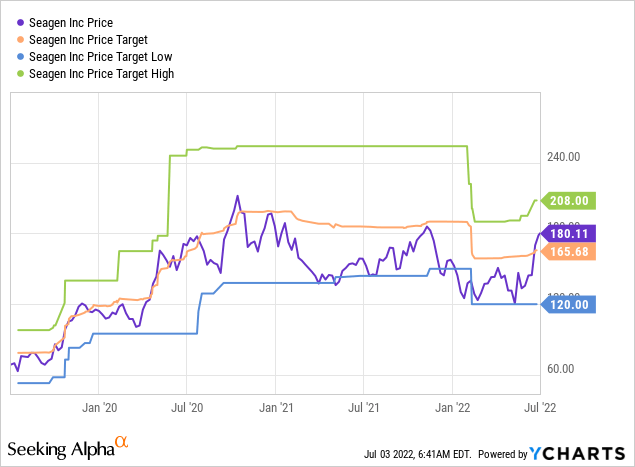

SGEN:

- Expected Upside (to average price target): None.

- Max. Downside: -33%

- Max. Upside: +16%

Conclusion: Even in a buyout, the upside potential isn’t greater than the downside risk.

Our take: We disagree with Wall Street. As mentioned above, we believe that the stock is well-buoyed (limited downside risk), and we expect a 20%+ upside (at the very minimum) if a near-term deal is announced.

Y-Charts

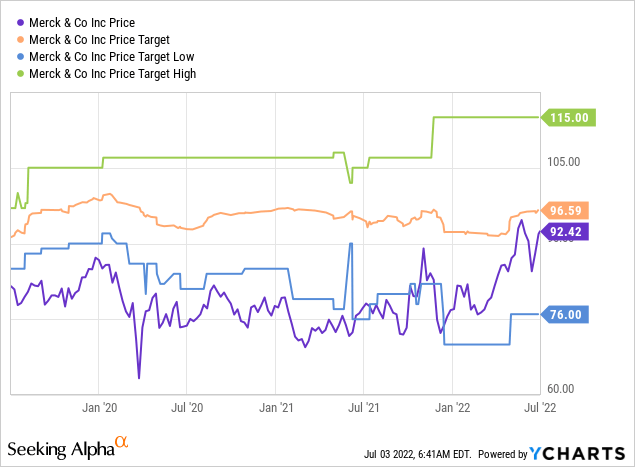

MRK:

- Expected Upside (to average price target): <5%.

- Max. Downside: -18%

- Max. Upside: +24%

Conclusion: Fairly valued, with a continued upward trajectory expected, but nothing out of the ordinary.

Our take: We agree with Wall Street, but if we look at the 12 months, both our downside and upside would be smaller than the extreme points Wall Street sees. +/-10%, 15% top, would be our expectation of the stock in an “extreme” scenario.

Y-Charts

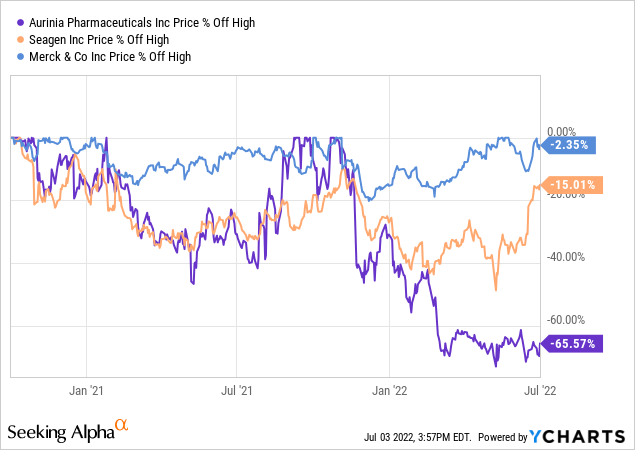

Let’s not also forget:

- AUPH is trading 2/3 off its November 2021 high

- SGEN is trading 15% of its October 2020 high

- MRK is trading near its June 27, 2022 high

There’s no guarantee that after losing a lot of ground, a stock price is poised to recover. Nothing is preventing a stock that has halved from halving again, and then again, if “needed”…

Still, when we talk about a small-cap biotech that is clearly drawing the interest of some big pharma guys, we can say that AUPH’s current valuation is very low, without but surely with buyout chatter running in the air.

Epilogue

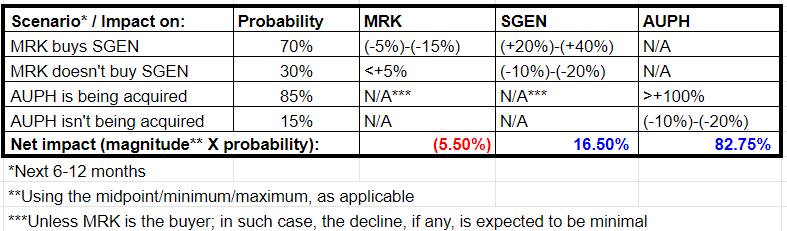

Going back to what we started with, when we look at AUPH-SGEN-MRK we can certainly construct a pair-trade that meets the basic requirements:

- non-directional: we expect AUPH to perform better no matter what.

- relative value: a buyout is a clear catalyst to create that.

- similar characteristics: same sector/industry.

- trading out of their historical trading range: we already ticked these boxes.

One (simple) way to look at it is to count on Wall Street and to expect AUPH to perform much better than either MRK or SGEN, without making too much of a story out of recent rumors regarding any of the trio.

Y-Charts

A more comprehensive way is to analyze the situation based on the following table:

[Of course, our assumptions, projections, and expectations are built into this, and you may wish to use different figures, but the concept is the main thing to take out of this]

Author

Note that since MRK is paying a dividend, the impact of the yield should also be taken under consideration. Nevertheless, since the yield is relatively small relative to the differences in the net impact – therefore, won’t change the bottom line – we ignore it.

I assume that AUPH being the long leg of this pair-trade is something very few readers might have an issue with. Contrary to that, many readers are likely finding MRK being the short leg to be questionable.

The above table is the ultimate explanation why we prefer to short MRK, and not SGEN, against going long AUPH.

and just to be very clear about this: We don’t suggest shorting MRK, and the only reason we would short MRK is if it’s part of a pair-trade.

Theoretically, one may use SGEN instead of MRK, and (as per the above) we actually believe that this might work. Nonetheless, in such a case the expected return (out of the pair-trade) would be lower and the risk (of the pair-trade) would be higher, simply because SGEN is obviously a more risky investment than MRK – and that goes both ways.

Be the first to comment