With risk-off gripping markets across all asset classes, market volatility has increased dramatically. The VIX index, which measures the implied volatility of put and call options on the S&P 500 stocks, rose to its highest level since December 2008 when it moved to 61.62 on March 9. Options are price insurance, and market participants typically flock to the options market to protect positions when risk levels rise.

After the Fed cut interest rates three times for a total of 75 basis points in 2019, the price of lumber began to rise. Lower rates tend to increase the demand for new housing as mortgage rates decline. Nearby lumber prices rose steadily starting in late May 2018 when the price hit a low of $286.10 per 1,000 board feet. In mid-February, the price of wood on the futures market was knocking on the door at the $470 level. The CatchMark Timber Trust (CTT) owns timberland throughout the United States. As of Monday, March 9, the price of May lumber futures settled at $356.70 per 1,000 board feet, 25.3% below the high from February 20.

CTT owns wood

The CatchMark Timber Trust, headquartered in Atlanta, Georgia, strategically harvests its high-quality timberlands to supply lumber to the market. CTT began operations in 2007 and owns interests in 1.5 million acres of timberlands in Alabama, Florida, Georgia, North Carolina, Oregon, South Carolina, Tennessee, and Texas. The Trust has a market cap of $405.085 million and trades an average of 201,877 shares each day, making it a liquid product. The price of CTT shares correlates well with the price of lumber futures over time. In September 2015, the price of lumber hit a low of $214.40 per 1,000 board feet. In August of the same year, CTT traded to a low of $7.90 per share. In May 2018, when the price of lumber reached an all-time high of $659 per 1,000 board feet, CTT shares rallied to a peak of $13.73 in March 2018. Lumber is a highly volatile commodity, but it is more than a challenge to trade.

Lumber futures are untradable

Over the past four decades, I have traded in almost all of the commodities futures markets. I have experienced the ease of executing buy and sell orders in highly liquid markets like crude oil, natural gas, gold, grains, and many others. I have also faced the challenge of markets that suffer from far less liquidity like frozen concentrated orange juice, cotton, and others. The one market I have never traded and will continue to stay away from is lumber.

{kind=link}

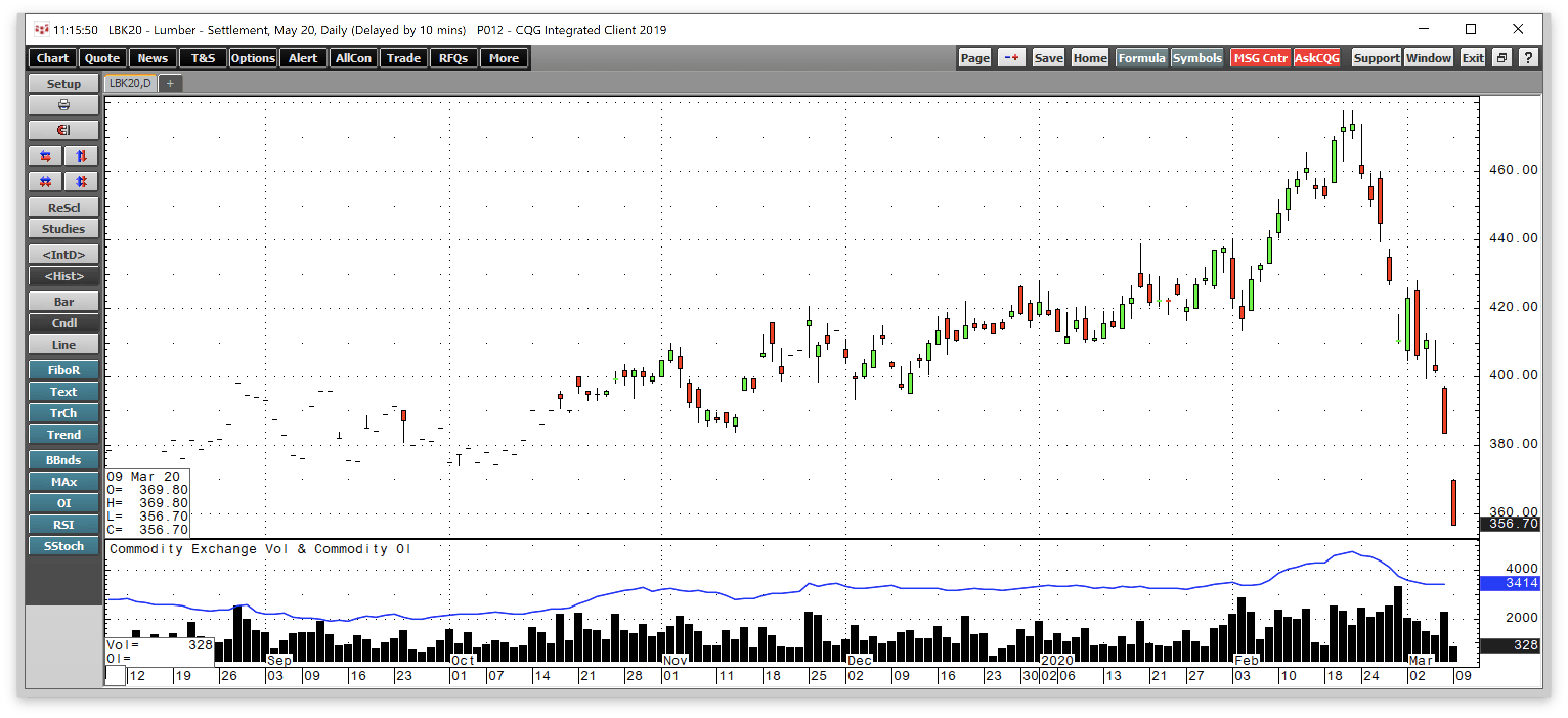

Source: CQG

The daily chart shows that the total number of open long and short positions in the lumber futures market stood at 3,414 on Friday, March 6. Each contract represents 110,000 board feet, and the price is quoted in dollars per 1,000 board feet. The level of open interest at the end of last week equates to 375.54 million board feet of lumber. At $356.70, the total value of open interest is just over $133.8 million, less than one-third the size of the market cap of the CatchMark Timber Trust. At the same time, a busy day in the lumber market is when over 1,000 contracts change hands. Many days, fewer than 500 contracts change hands. Futures markets like lumber that offer limited liquidity tend to experience price gaps higher and lower when bids and offers disappear, which adds to the volatility. Managing risk in an illiquid market is no easy task. A product like the CTT or other wood-related instruments that correlate with the futures price can offer alternatives.

The recent sell-off in the lumber market that took the price over 25% lower since February 20 means a buying opportunity is on the horizon for three reasons.

Reason one: Risk-off will send lumber towards the buy-zone

The price of lumber is falling as market participants panic over coronavirus. Markets across all asset classes have experienced wild bouts of volatility. The stock market has corrected sharply. Crude oil traded down to $27.34 per barrel on Sunday night, March 8, after OPEC did not cut production at its latest meeting and the Saudis decided to flood the market. The price of gold traded to over $1700 per ounce. The yield on the US ten-year Treasury declined to a record low of just over 0.50%. The markets are in the midst of the most volatile period since the 2008 financial crisis. In early 2009, the price of lumber fell to a low of $137.90, which could mean that there is a lot of downside if the current risk-off environment persists. 2008 was a financial crisis, but coronavirus is different. Scientists and the global medical community are hard at work on a vaccine and treatments for the virus, but the death toll will tragically rise. Eventually, calm will return to markets, and central banks will continue to pull out all the stops to ease the decline of asset prices.

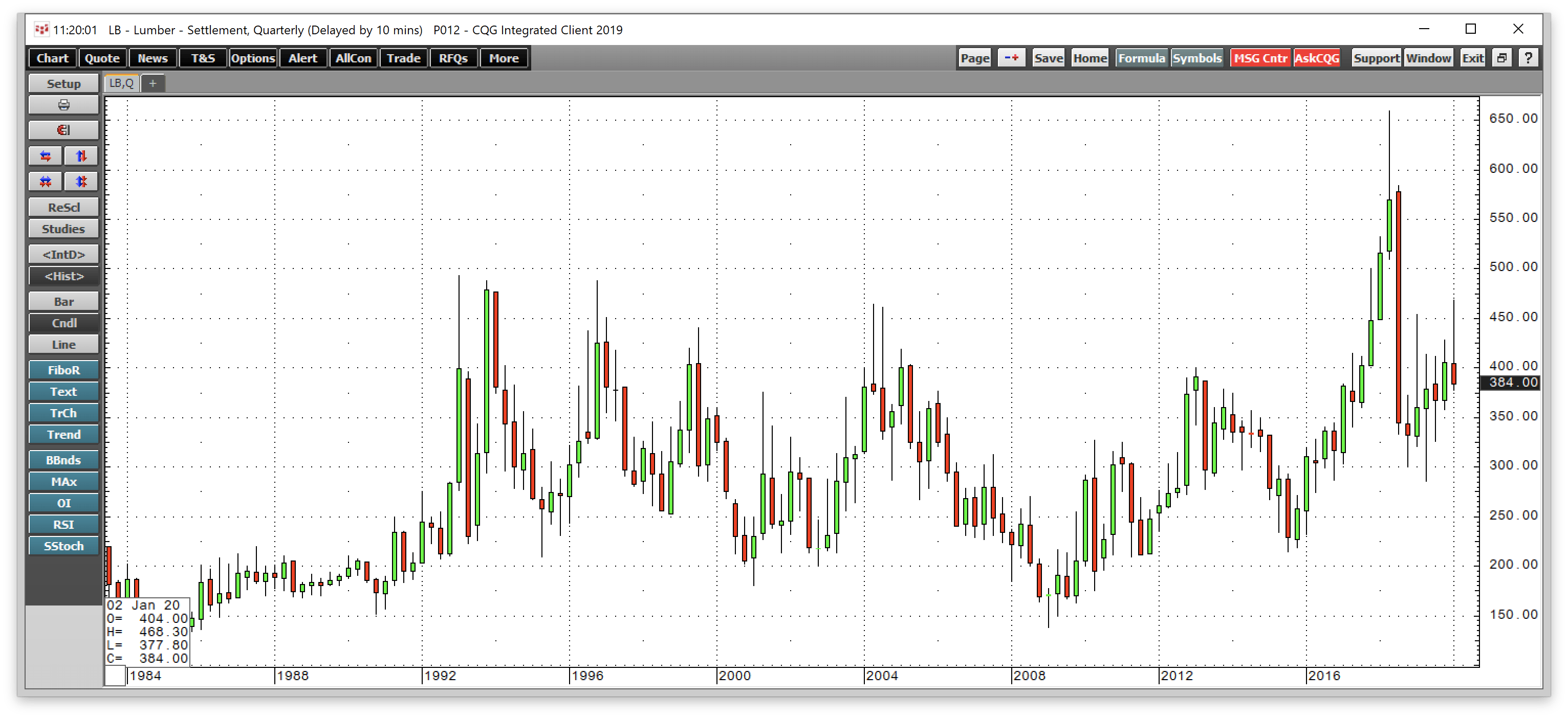

Source: CQG

The quarterly chart shows that lumber has made higher lows since early 2009. In the current risk-off environment, anything is possible, and we could see a return to prices below $200 per 1,000 board feet. At those prices, lumber would be a bargain, and lower rates will fuel the demand for new homes.

Reason two: Fed rate cuts will cause demand for wood to rise

As the Fed and central banks continue to pump liquidity into markets, rates will plunge. It is undoubtedly time for caution, and I am not suggesting running into any markets that have become falling knives. Meanwhile, rates will not move higher at the same pace they are declining. It will be a long time before any central bank decides the waters are calm enough to tighten credit.

Coronavirus is triggering what could turn out to be the worst risk-off period in history. The Fed Funds rate is heading for zero, and quantitative easing will send mortgage rates to new lows.

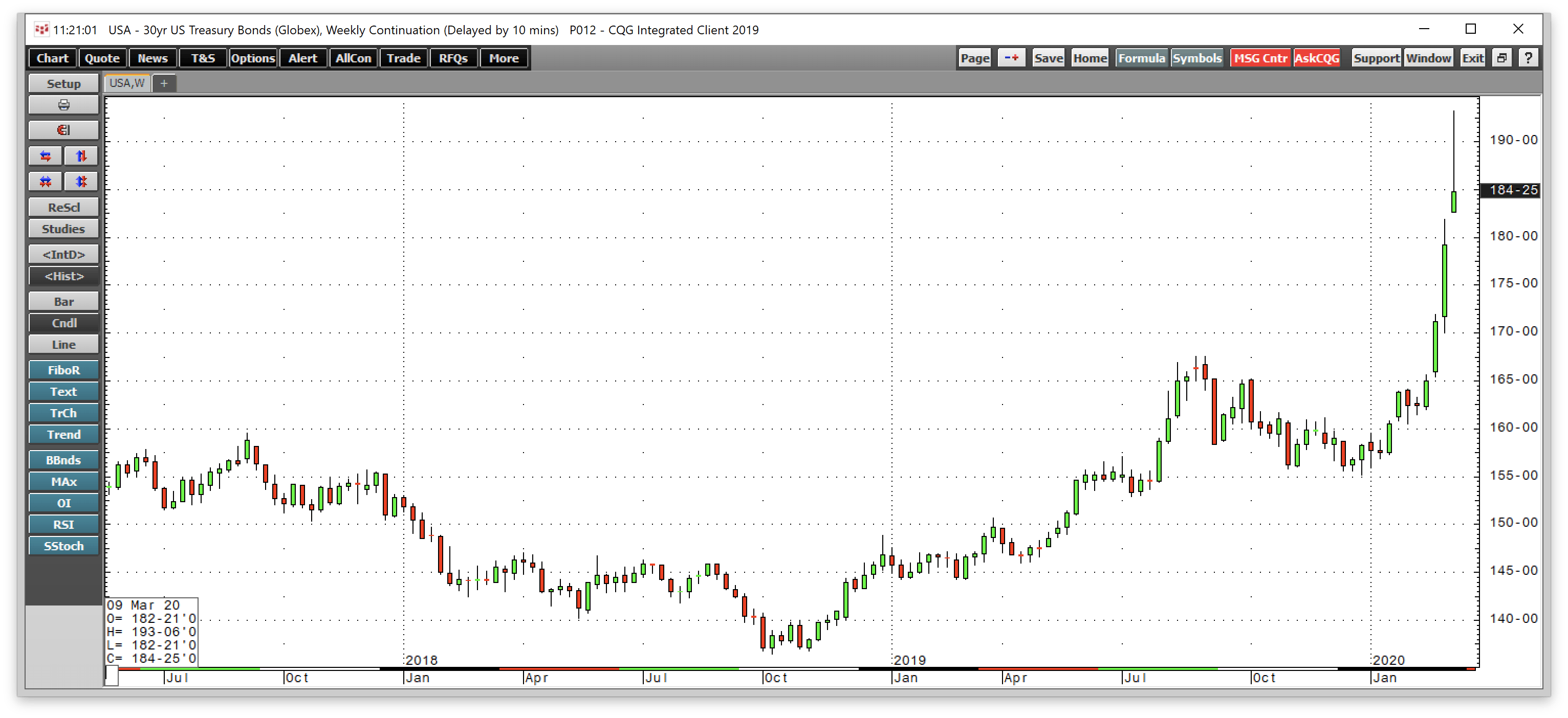

Source: CQG

The weekly chart of the 30-Year Treasury bond futures shows the move from 155-05 at the end of 2019 to a high of 193-06 on March 9. Market volatility reached a frenzy on Sunday evening and Monday as fear over coronavirus continued to reach new heights. Crude oil traded to $27.34 per barrel, the lowest level since the energy commodity hit $26.05 in February 2016. The low level of interest rates should eventually support new home construction. However, the price of lumber could continue to fall in the current environment as falling knives often send prices to levels far below what seems rational.

Reason three: A juicy dividend alongside the opportunity for capital growth

At $8.26 per share for CTT and $356.70 per 1,000 board feet on Monday, March 9, the shares and price of lumber have downside potential as risk-off conditions grip markets across all asset classes. At the price on March 9, CTT offered shareholders an attractive 6.50% dividend. A prolonged period of market correction could cause the dividend to fall or disappear. However, buying CTT on a scale-down basis could be an optimal approach as low rates should eventually ignite the demand for new homes.

Lumber can be a wild market, and the price of wood may decline like a two-by-four falling from a roof over the coming days and weeks. However, the addiction of central banks to lower rates and the willingness to do whatever is necessary to stabilize markets is a sign that mortgage rates will fall to levels that support new home building. I am a buyer of CTT shares but will use wide scales to build a long position.

The Hecht Commodity Report is one of the most comprehensive commodities reports available today from the #2 ranked author in both commodities and precious metals. My weekly report covers the market movements of 20 different commodities and provides bullish, bearish and neutral calls, directional trading recommendations, and actionable ideas for traders. I just reworked the report to make it very actionable!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The author always has positions in commodities markets in futures, options, ETF/ETN products, and commodity equities. These long and short positions tend to change on an intraday basis.

Be the first to comment