FedBul/iStock via Getty Images

I know I tout real estate investment trusts (REITs) for their higher but dependable dividends. I’m on record for praising the sector over and over again.

However, I’m also on record for pointing out REITs that don’t live up to the set standard. Because there certainly are lackluster examples out there. Less-than-reliable and outright failures as well.

As with any other investment, there are no full-on guarantees you’re going to get what you expected.

REITs are designed to be safer, it’s true. They’re also designed to be able to offer higher yields. But there are still ways to mess them up, whether on purpose, through negligence or ignorance, or due to circumstances out of their control.

There are also examples of REITs that pay very subpar dividend yields, comparatively speaking. The entire cell tower category, for example, tends to underwhelm in this area. People usually buy into them more for their share price appreciation potential.

Their payouts are a far-off secondary consideration. An afterthought, even.

This doesn’t mean towers aren’t worth considering, mind you. Though, I prefer to buy into them when they’re cheap and their yields are therefore elevated.

Then again, that’s my overall strategy when it comes to dividend investing: Buy smart stocks with solid dividends that have found themselves unfairly out of market favor.

This is especially true when it comes to sleep-well-at-night (SWAN) stocks. They’re always important to keep in mind.

These SWANs Never Stop Singing

You all know how much I love a good SWAN song. The positive kind, mind you, not the traditionally mournful definition.

Miriam-Webster Dictionary defines a (lower-case) swan song as:

- A song of great sweetness said to be sung by a dying swan

- A farewell appearance or final act or pronouncement.

Fair enough. But it also adds that:

“Swans don’t sing. They whistle or trumpet, or in the case of the swan most common in ponds, the mute swan, they only hiss and snort. But according to ancient legend, the swan does sing one beautiful song in its life-just before it dies.

References in English to the dying swan’s lovely singing go back as far as Chaucer, but the term swan song itself didn’t appear in the language until the 1830s, when Thomas Carlyle used it in Sartor Resartus. Carlyle probably based his “swan song” on the German version of the term, which is Schwanengesang or Schwanenlied.”

That just isn’t true about my kinds of SWANS. They sing over and over and over again.

Look, I can make the case for owning SWANs because we’re headed into a recession. Been there and done that.

Moreover, I’m sure I’ll do so again, especially if the economy really does take a downturn.

Incidentally, the debate is still raging about whether the Fed can achieve a soft landing. Also incidentally, I’m still rooting for a recession.

In which case, it only makes sense to own sleep-well-at-night stocks. Who wouldn’t want that kind of income-producing stability when other sources start slipping and sliding?

But even if I’m wrong – and people like Yahoo Finance’s Jared Bilke, who wrote an interestingly angled Morning Brief article on January 19, are right – now is still the time to own SWANs.

Here’s why…

The Case For SWAN Stocks

There are actually two major reasons why you should own SWAN stocks – even when the economic sun is shining bright and optimism is in the air everywhere you turn.

Stated bluntly, that could change in the next instant.

It has before. It will again. Count on it.

That’s part of the whole “sleep well at night” premise. You don’t have to be worrying about what the market will do tomorrow. You can enjoy the moment instead, whether that moment involves working your 9-5, hanging out with family and friends…

Or pulling the covers up over your shoulders, closing your eyes, and drifting off to dreamland.

You know it doesn’t matter what the market is going to do tomorrow. You’ll still get paid.

Now on to my second point.

Remember that while you hold onto a stock, all you have is a paper gain or a paper loss. On the plus side, that loss could turn into a gain the next day, allowing you to cash out in the clear. On the negative side, that gain could turn into a loss the next day, prompting you to panic-sell in the red.

The shares are really yours. But their value isn’t until you part ways with them.

But SWAN-style dividends? They’re yours four times a year or even 12 times a year, depending on the company in question.

You have real money in your hands that you reinvest into the stock in order to reap even greater rewards. Or you can spend it right then and there to purchase what you need.

It’s your money and therefore your choice.

Combine that “actual” factor with the perpetual promise of more to come, and you’ve got a stock worth owning.

Especially at these prices.

2 SWANs For Infinite Income

When referring to a “SWAN” within this article, we are not necessarily alluding to a fast growing dividend as much as we are referencing two REITs that continue to hike their dividend in a consistent and safe manner.

SWAN #1 – Realty Income (O)

When an investor thinks about REITs, increasing dividends, and dividend safety, you can’t help but think of The Monthly Dividend Company, which is none other than Realty Income.

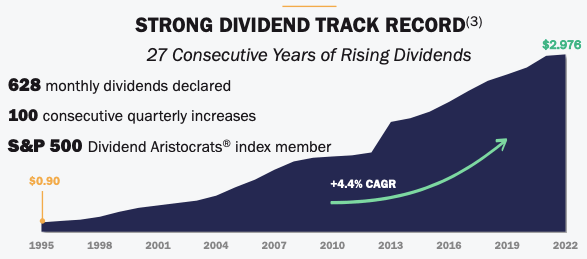

To begin, Realty Income is one of only three REITs that are on the prestigious Dividend Aristocrats list. The other two REITs to make the list are Federal Realty Investment Trust (FRT), which is actually a Dividend King, and Essex Property Trust (ESS).

As of this month, the company has now declared 631 consecutive monthly dividends, and they have increased the dividend for 100 consecutive quarters, which is quite impressive.

Realty Income Investor Presentation

Since going public in 1994, the company has had a 4.4% compound annual dividend growth rate. The dividend does not grow at a fast pace, but it grows at a consistent pace.

The company currently pays an annual dividend of $2.98 per share with a payout ratio of 75%, meaning the dividend is plenty covered by its AFFO.

Companies like Realty Income are unable to increase their annual dividends without having a strong portfolio of properties that generate growing cash flows.

Stocks go up and down all the time, more down than up in the past 12 months. However, regardless of what a stock price is doing, a Realty Income shareholder can count on a safe, reliable, and growing dividend.

Since 1995, the company has maintained a 5.1% CAGR in terms of AFFO share growth. Over that time span, we have seen a financial crisis, multiple recessions, and a global pandemic, yet Realty Income has continued to produce. In fact, the company has generated positive AFFO growth in 25 out of 26 years.

Part of this production is due to the company maintaining and adding great properties that are in demand, and another part is due to the strong leadership team the company has.

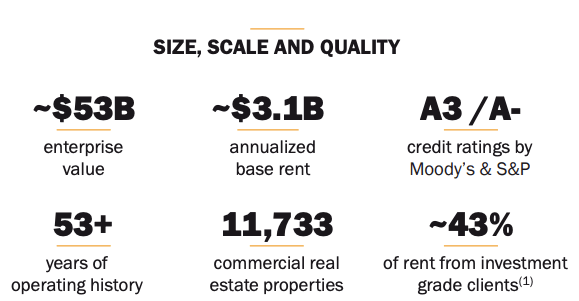

The company has a strong balance sheet with credit ratings of A3/A- from Moody’s and S&P.

Realty Income Investor Presentation

Due to the company’s size and scale, along with strong credit rating, they are able to obtain credit in order to continuously grow the portfolio at reasonable credit terms, which is a huge advantage when compared to its competitors.

So, when it comes to Realty Income, we have:

- Strong Management team

- Consistent Results year in and year out

- Excellent portfolio or properties that are in demand

- A growing dividend that is paid out on a monthly basis

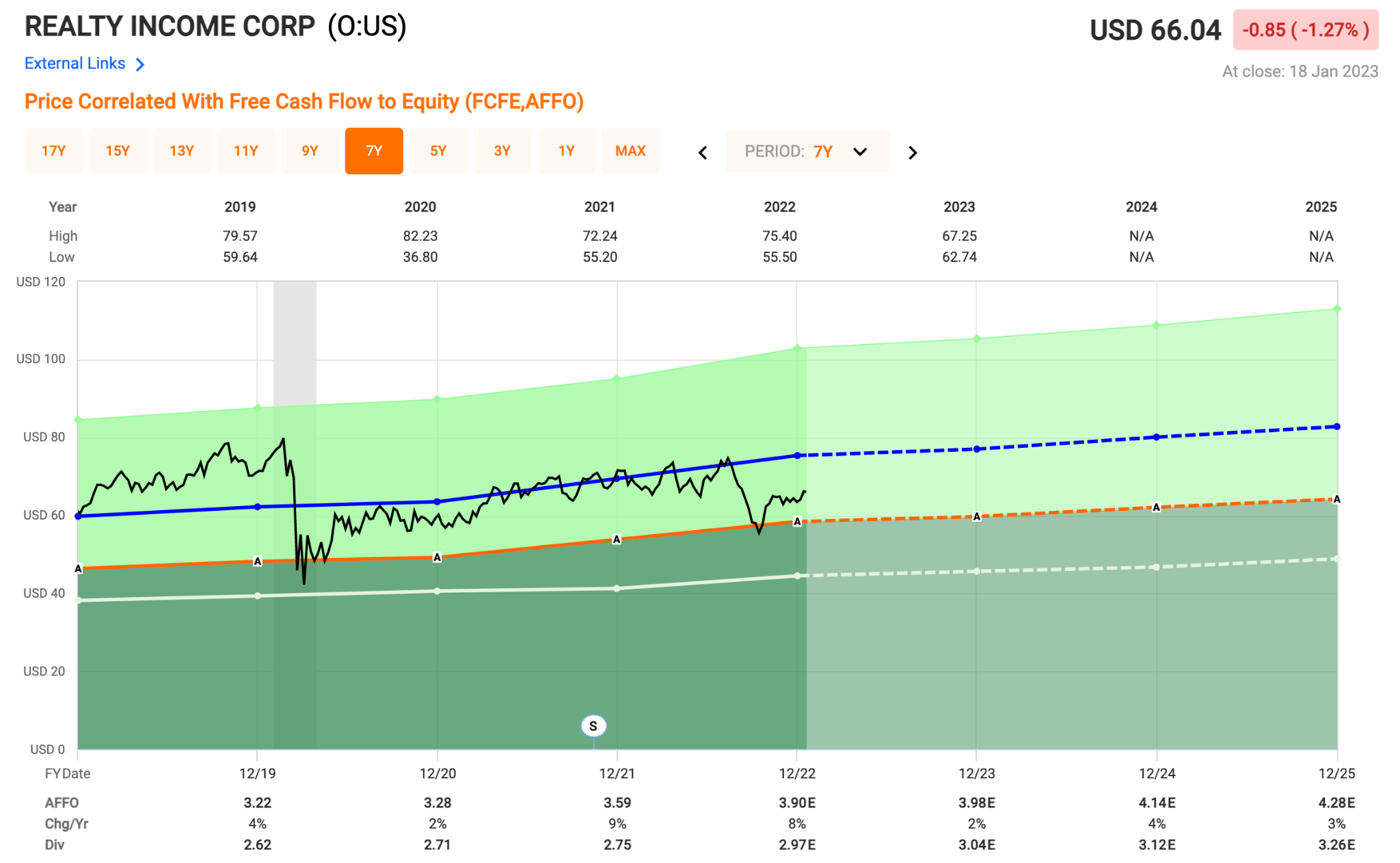

So what does valuation look like? Actually, it looks quite intriguing. Realty Income currently trades at a P/AFFO of 16.9x and a forward AFFO multiple of 16.5x. This is well below their historical average of 19.3x.

Fast Graphs

In an environment with many unknowns economically, investors can take solace knowing their dividend is safe and growing with Realty Income.

SWAN #2 – VICI Properties (VICI)

Realty Income is a name that is well-known to the REIT community and has been around since the mid 1990, but VICI Properties is less-known, but has burst onto the scene.

VICI Properties is the largest landlord on the Las Vegas strip and owns some of the best assets in that region. Some of the properties they own along the strip include:

- Caesars Palace

- MGM Grand

- Park MGM

- Mandalay Bay

- Luxor

- Excalibur

- New York New York

- The Mirage

- The Venetian

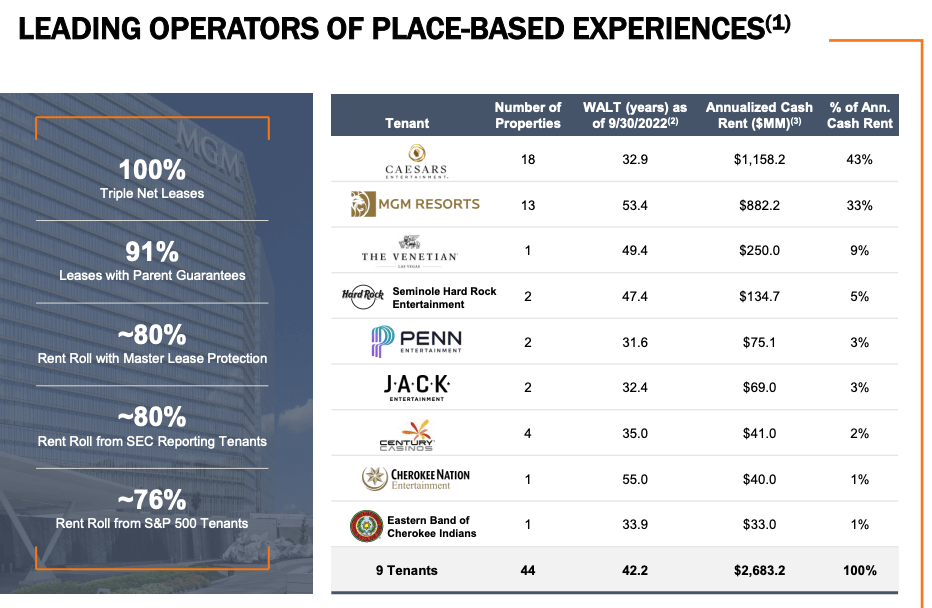

In total, the company owns 49 properties that amount to 124 million square feet and approximately 59,300 hotel rooms. VICI is the landlord and leases the properties out to some of the best and well respected operators in the sector.

VICI Investor Presentation

As you can see, 91% of the company’s leases have parent guarantees and roughly 80% report their financials as public companies, and roughly 76% are S&P 500 companies.

These leading nine tenants make up the majority of the properties, and have a weighted average lease term of 42.2 years, which is incredible.

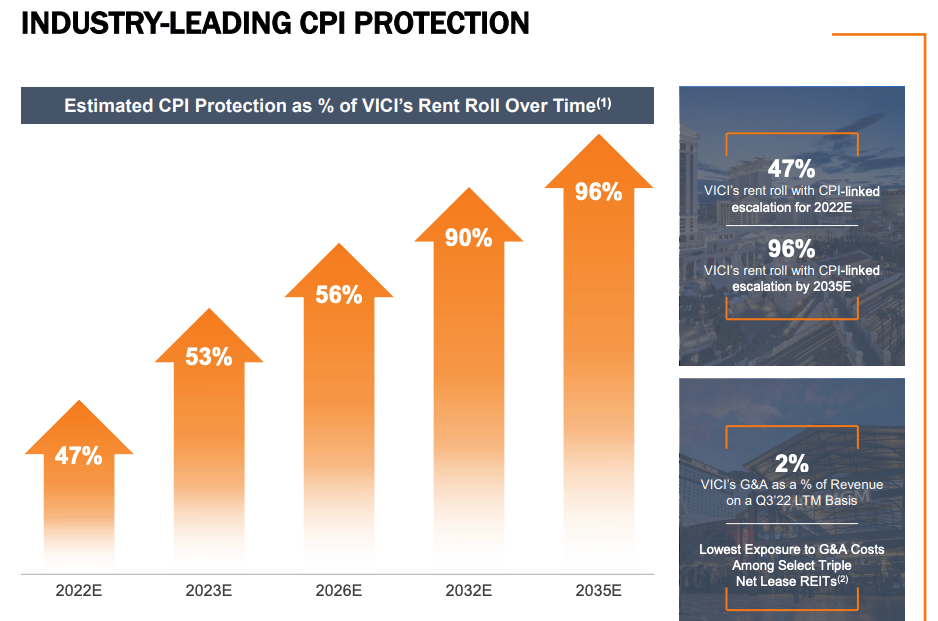

Many have asked, with the uptick in CPI over the past few years, would it negatively impact a company with locked in leases? The answer is NO.

VICI, like many of the other REITs we cover, have built in rent escalators which increase at either a fixed rate or some are linked to CPI. In 2022, nearly 50% of the company’s rent roll was linked to CPI and by 2035, nearly 100% will be related to CPI, which will fully protect the company against periods of high inflation.

VICI Investor Presentation

So as we saw, the company has some great assets, which are protected against CPI, and these properties turn great cash flows. During the depths of the pandemic, when many REITs saw their rental collections cut in half, VICI properties maintained a 100% collection rate.

Not a 75% or 80%, but a perfect 100%, every dime was collected. This speaks not only to the quality of the company’s assets, but to the strength and quality of their tenants/operators as well. Thus, heading into a potential recession, shareholders can feel more confident in a company like VICI.

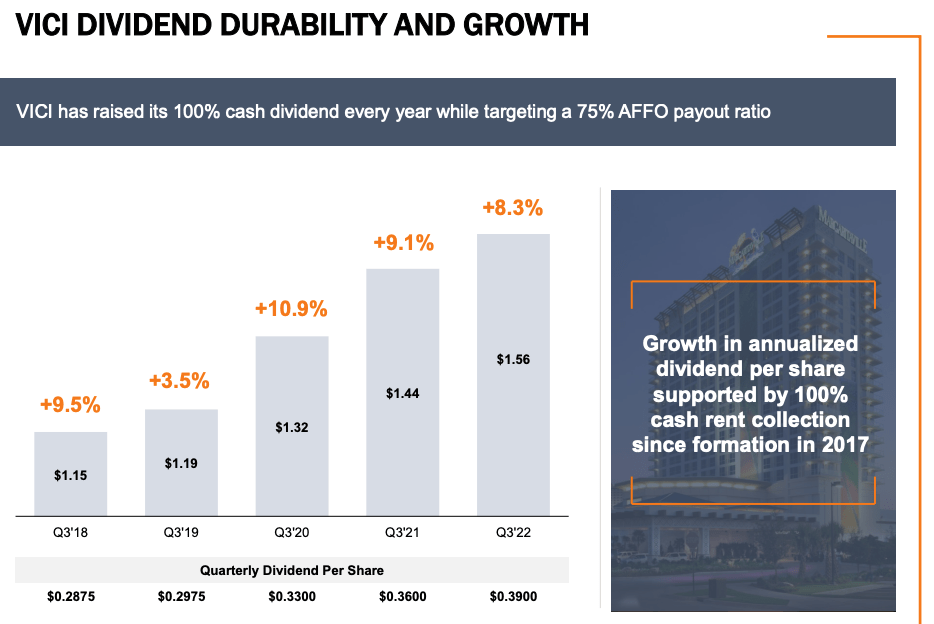

This performance has generated strong cash flows which have led to a growing dividend.

VICI does not have the dividend history that Realty Income has, largely due to the fact that the company did not go public until early 2018. Since going public, you can see that the dividend has been increased EVERY year.

VICI Investor Presentation

The dividend has been growing at an average annual growth rate north of 10%. So with VICI, you do not have the dividend history but you have solid dividend growth. The current dividend yield for the stock is 4.8% and is well covered by a payout ratio of 75%.

VICI is a company that continues to expand aggressively as they recently acquired the remaining equity in the MGM Grand from Blackstone Real Estate Income Trust for $1.27B plus they continue to raise money for future acquisitions.

Shares of VICI have increased nearly 20% over the past 12 months, but the stock still appears to have further upside. Shares currently trade at a forward AFFO multiple of 15.5x compared to their short historical average of 16.3x.

FAST Graphs

That’s How I Roll…

What’s with all of these acronyms anyway?

- REIT (Real Estate Investment Trust)

- SWAN (Sleep well at night)

- FFO (Funds from Operations)

- NAV (Net Asset Value)

- REVPAR (Revenue per available room)

I know these terms can be confusing, especially if you’re a newbie investor.

In my new book (REITs For Dummies) I plan to help readers demystify the REIT sector and to help break down the wonderful world of REITs so that anyone can build a fortress REIT portfolio.

And speaking of fortresses, check out the license tag on my car. I posted this on LinkedIn a few days ago:

LinkedIn (Brad Thomas)

Yes, another strange word, MOAT, which is not an acronym, but the mantra behind our research platform, Wide Moat Research.

Just like the two SWANs – Realty Income and VICI Properties – I have purposely built our research platform around “fortress” picks (like these) that have “wide moats”.

Selecting “wide moat” stocks is the secret to our success and the reason that our growing subscriber list (over 15,000 across all platforms) is able to “sleep well at night”.

As always, thank you for reading and happy SWAN investing!

Be the first to comment