JuSun

Oaktree Specialty Lending (NASDAQ:OCSL) is having a hard time catching a break, and that’s ok, because high yield, combined with dividend growth and reinvestment can lead to market beating returns. This can be especially helpful when stocks like OCSL are held in retirement accounts, considering that the full dividend without immediate tax considerations can be reinvested, leading to faster compounding.

As shown below, OCSL has been range bound over the past 6 months, and currently trades well below the $7 resistance level. In this article, I highlight why OCSL presents an attractive high yielding opportunity right now, so let’s get started.

OCSL Stock (Seeking Alpha)

Why OCSL?

Oaktree Specialty Lending is an externally-managed BDC that was formerly known as Fifth Street Finance. It got its name change when Oaktree Capital bought out the former asset manager and took over investment advisory duties for the company. OCSL underwent another transformation earlier this year, when Oaktree merged Oaktree Strategic Income into OCSL.

I view OCSL as being in far better hands than before, considering the external manager, Oaktree Capital Management was founded by famed value investor, Howard Marks, who is well-recognized for his prescient calls on the markets and investments throughout his career.

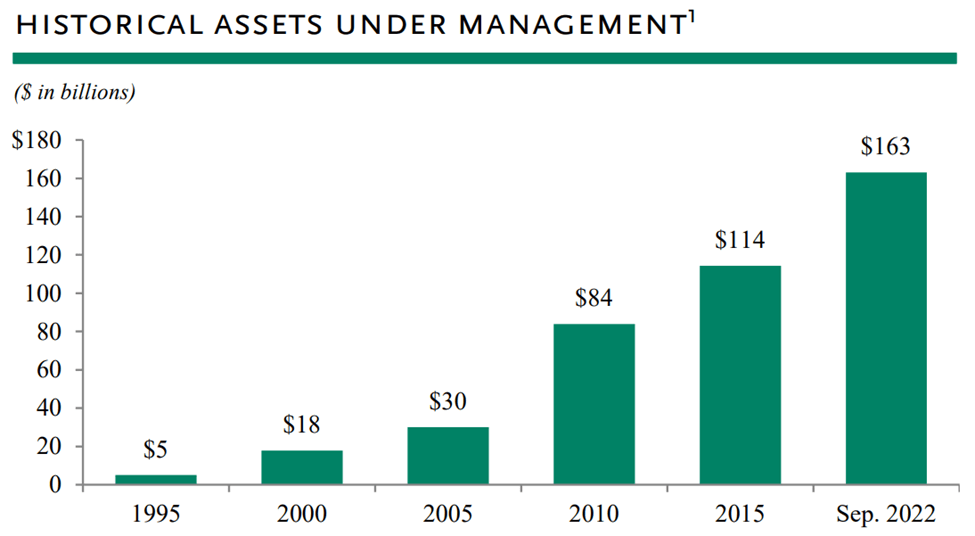

OCM was founded in 1995 and currently has $163 billion contrarian, value-oriented investments across a variety of asset classes. As shown below, OCM has a solid track record of attracting investor capital through its sound investment practices.

OCM AUM Growth (Investor Presentation)

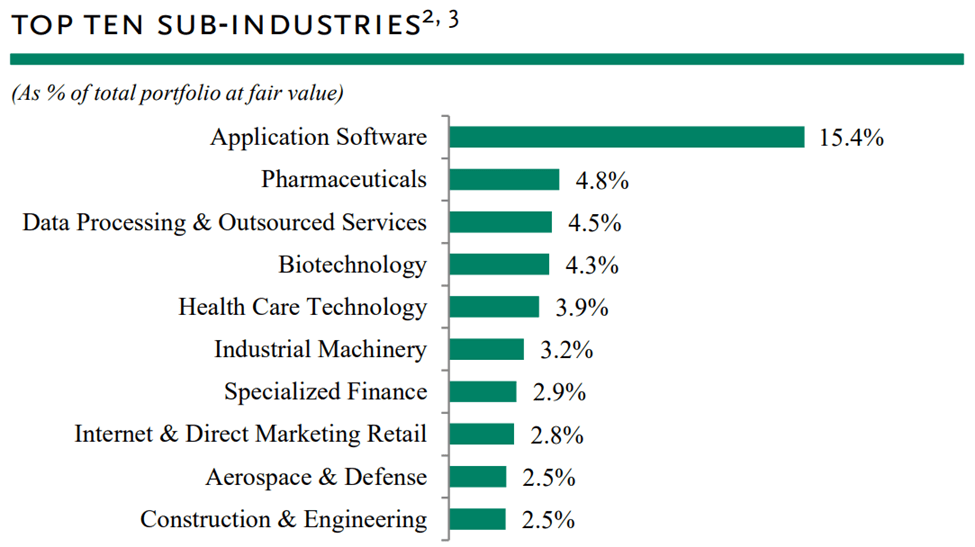

At present, OCSL has $2.5 billion in total investments spread across 149 portfolio companies. It also employs an overall conservative strategy, with 87% exposure to secured loans, at 71% first lien and 16% second lien, followed by 7% invested through joint ventures, and 6% exposure to unsecured loans and equity for a higher yield and more capital appreciation potential.

The portfolio is well diversified with higher exposure to technology and healthcare segments. However, unlike BDCs such as Hercules Capital (HTGC) and Horizon Technology Finance (HRZN), OCSL doesn’t limit itself to just those segments, and invests wherever it finds the potential for risk adjusted returns, as shown below.

OCSL Portfolio Mix (Investor Presentation)

OCSL is also benefitting from higher interest rates, as 86% of its debt portfolio is floating rate. It’s now generating a 10.6% weighted average yield on debt investments, up by 130 basis points sequentially from 9.3% at the end of the second quarter. Also encouraging, OCSL currently has no investments on non-accrual status, and carries a strong balance sheet, with a net debt to equity ratio of 1.06x, sitting far below the 2.0x statutory limit.

Looking forward, OCSL is well positioned to fund its deal pipeline, as it has $24 million in cash on hand plus an additional $500 million in undrawn capacity on credit facilities. It’s also positioned to drive efficiencies and scale through its upcoming merger with one of OCM’s other managed funds, Oaktree Strategic Income II (otherwise known as OSI 2). Management noted that this transaction will be accretive to shareholders during the recent conference call:

As we end the fiscal year, I also want to touch on our entry into a merger agreement with Oaktree Strategic Income II, Inc., or OSI 2, which was announced in September. We believe this transaction represents a compelling opportunity for shareholders of both OCSL and OSI 2. We expect it would create a larger, more scaled BDC with just over $3 billion in total assets, increase our trading and liquidity and should improve our access to the debt capital markets. We also anticipate that will create efficiencies and cost savings to drive NII accretion over both the near and long term.

Meanwhile, OCSL again raised its dividend, this time by 6% to $0.18 per quarter, representing a 16% increase over the same time last year. While the NII to dividend coverage ratio is tight at 100%, I see potential for OCSL to out-earn the current dividend run rate through additional deals and the impending merger with OSI 2.

Lastly, I find OCSL to be attractive at the current price of $6.70, trading at a discount to its NAV per share of $6.79. While NAV/share is down from $6.89 at the end of the second quarter, this has to do with widening credit spreads and unrealized losses on certain equity investments due to higher interest rates and economic uncertainty, and it could bounce back with a clearer economic picture.

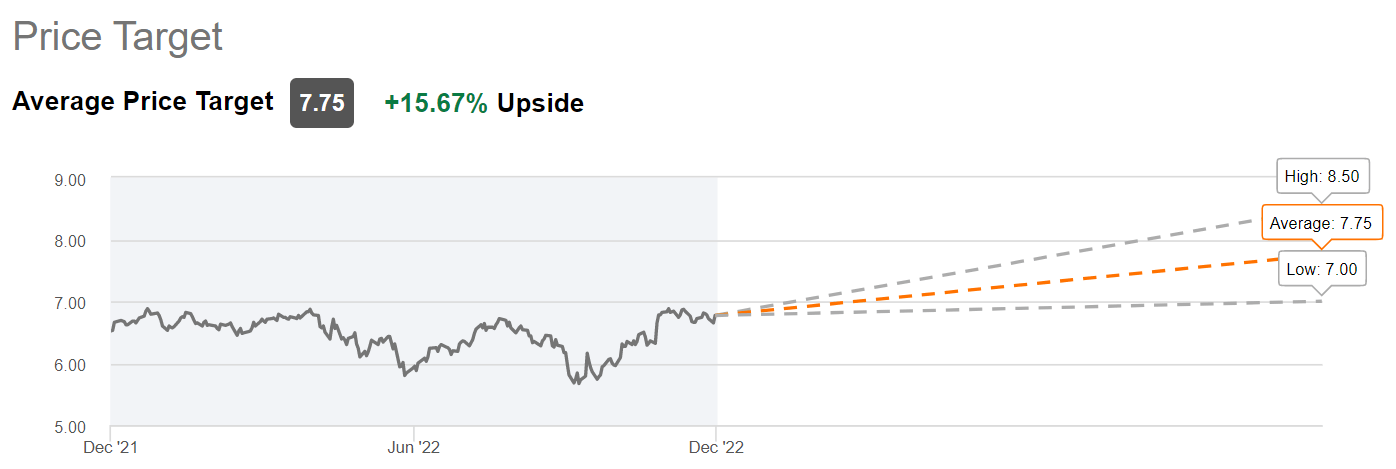

I believe that OCSL deserves to trade at a premium to net asset value, and analysts seem to agree, with a consensus Strong Buy rating on OCSL with an average price target of $7.75. This equates to potentially very strong total returns including the dividend.

OCSL Price Target (Seeking Alpha)

Investor Takeaway

OCSL is a well-diversified BDC with conservative loan exposure, a strong balance sheet, and a high portfolio yield. It has no debt investments on non-accrual status, and the proposed merger with OSI 2 should help create additional efficiencies and cost savings going forward. OCSL currently trades at a discount to NAV, giving investors the potential for very strong total returns from here.

Be the first to comment