pandemin

Williams (WMB) reached an agreement to acquire MountainWest Pipelines Holding from Southwest Gas (SWX) for $1.5 billion in cash and debt. The acquisition gives WMB further midstream reach in the Rocky Mountains, and in our view is a long-term play on Rockies gas supply growth.

In a press release, WMB reported the transaction was priced at an 8x multiple on 2023 EV/EBITDA, implying expected EBITDA of ~$188 million next year. The package includes a mix of assets regulated by the Federal Energy Regulatory Commission (FERC) with predictable cash flows and others with more risk-reward potential.

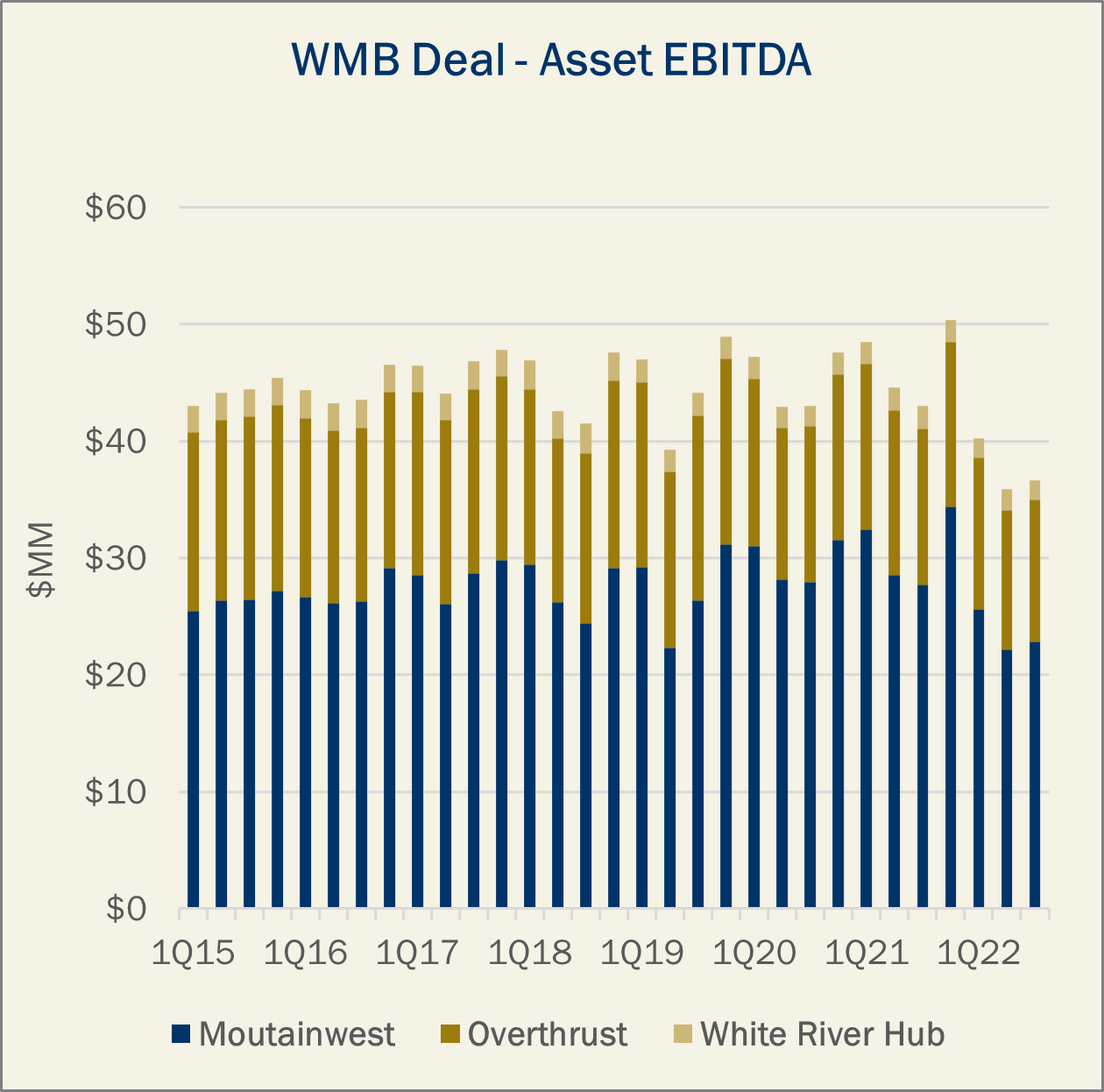

The MountainWest Pipeline, the largest asset in the package, connects Rockies natural gas basins to markets in the West and Midwest. The ~2,000-mile interstate pipeline can ship up to 2.5 Bcf/d of gas. MountainWest has stable cash flow and generates over 70% of its revenue from gas transportation services, with another ~25% of revenue from the Clay Basin storage facility. The pipeline earned $123 million EBITDA in 2021, according to FERC financial data, while EBITDA for the trailing twelve months (or TTM) was $105 million.

The second-largest asset in the deal, Overthrust Pipeline, is a smaller and riskier asset. Overthrust includes 260 miles of pipeline connecting Rockies gas supply to long-haul transmission lines (Ruby, Rockies Express, Kern River, Wyoming Interstate, and Questar). The Overthrust system can move up to 2.4 Bcf/d. Overthrust earned ~$56 million in EBITDA in 2021 while earning $51 million EBITDA on a TTM basis, according to FERC financial data.

Over 50% of current contracts on Overthrust are held by marketers and producers. Overthrust has legacy contracts with Occidental (OXY), Wyoming Interstate Gas, and BP that roll off in the next five years. In addition, Rockies Express Pipeline holds a 625 MMcf/d lease on Overthrust for west-to-east service that expires in 2028. This contract accounts for $29 million in annual revenue. All of these contracts could be at risk if production does not recover in the region.

But there are also reasons to expect upside from the Overthrust system. Overthrust connects the Colorado Interstate Gas (CIG) and Opal market hubs, and transport capacity on Overthrust has been extremely valuable recently given the blowout in West Coast gas prices. WMB noted the acquisition provides further reach into the Salt Lake City market, which is priced off Opal. Opal day-ahead gas traded last week (Dec. 12-16) over $47/MMBtu as below-normal temperatures blanketed the West.

Totaling all the assets, 2021 EBITDA on the package equates to $186 million, assuming WMB consolidated the White River Hub. On a TTM basis, total asset EBITDA is $163 million, with MountainWest EBITDA declining into 2022 (shown in Figure). With WMB’s upstream joint venture and other gathering and processing (G&P) assets, we see the purchase as a long-term bet by WMB on supply growth from the Rockies basins.

{kind=link}

East Daley agrees the Rockies could become a key part of long-term gas supply as demand grows for LNG exports.

Be the first to comment